Zero Emission Vehicle Market Size by Vehicle Class, Price, Vehicle Type, Vehicle Drive Type, Vehicle Speed and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

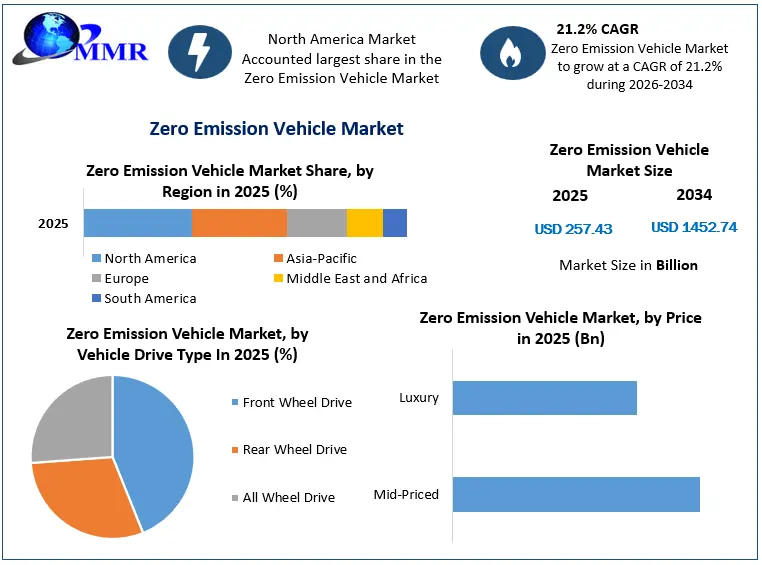

Global Zero Emission Vehicle Market size was valued at USD 257.43 Bn in 2025 and is expected to reach USD 1452.74 Bn by 2034, at a CAGR of 21.2%.

Zero Emission Vehicle Market Overview:

Zero Emission Vehicles (ZEVs) are automobiles powered by energy sources that produce no tailpipe emissions during operation, thereby minimizing their contribution to greenhouse gases and air pollutants. ZEVs are characterized by their environmental friendliness, reliance on alternative energy sources such as electricity or hydrogen, and their ability to significantly reduce carbon emissions compared to traditional internal combustion engine vehicles. The surge in ZEV sales is expected to be attributed to various factors, including heightened environmental awareness, stringent emissions regulations, technological advancements, and government incentives. Countries like China, the United States, Norway, Germany, and the United Kingdom have seen substantial increases in ZEV sales due to government support, increased charging infrastructure, consumer demand for eco-friendly vehicles, and policies promoting electric vehicle adoption.

This increase in demand has significantly influenced the zero emission vehicle market, prompting intense competition among automotive manufacturers to develop more efficient batteries, extend vehicle range, and enhance overall performance. The zero emission vehicle industry witnessed a rapid shift toward electric mobility, with governments all across the world implementing initiatives to accelerate ZEV adoption. These initiatives include setting ambitious targets to phase out fossil fuel-powered vehicles, investing in charging infrastructure growth, offering tax incentives, subsidies, and rebates to incentivize consumers, and promoting research and development in the ZEV sector.

In addition, with established automakers scaling up electric car manufacturing to meet rising demand, the zero emission vehicle industry has witnessed a significant shift in recent years. Companies like Tesla, Nissan, and Chevrolet have introduced popular electric models, while established automakers like Volkswagen, Ford, and BMW have also committed substantial investments to expand their ZEV lineups. Additionally, the emergence of startups focusing solely on electric vehicles, such as Rivian and Lucid Motors, has added dynamism to the zero emission vehicle market, fostering innovation and competition.

The commitment of governments to phasing out internal combustion engine vehicles in favor of ZEVs has accelerated the transition, with several countries setting ambitious targets to ban the sale of new fossil fuel-powered cars in the coming decades. The zero emission vehicle market growth extends beyond passenger vehicles, including commercial vehicles and public transportation. Companies are developing electric trucks, buses, and delivery vans to address emissions in logistics and urban mobility. Additionally, advancements in battery technology and charging infrastructure are paving the way for the electrification of heavy-duty machinery and even marine vessels, contributing further to a comprehensive reduction in carbon emissions across various sectors, and further boosting the zero emission vehicle market revenue growth.

Zero Emission Vehicle Market Analysis from 2025 to 2034

To know about the Research Methodology :- Request Free Sample Report

Zero Emission Vehicle Market Dynamics:

Supportive Government Policies and Regulations all across the world

Supportive government policies and regulations all across the world for accelerating the shift toward cleaner transportation is expected to be the major factor driving the zero emission vehicle market growth. Initiatives like the UK's plan to achieve 100% zero-emission vehicle sales for cars by 2035, alongside a trajectory of 80% by 2030, are crucial in fostering certainty for manufacturers while spurring consumer adoption. These regulations also bolster investments in charging infrastructure, stimulating market growth by facilitating EV ownership and addressing range anxiety concerns. Governments are taking comprehensive steps, offering incentives, tax reliefs, and grants to encourage electric vehicle (EV) adoption. Measures like plug-in van grants and reduced charging infrastructure costs in the UK exemplify this trend, incentivizing both manufacturers and consumers.

Initiatives Driving Electric Vehicle Manufacturing and Critical Minerals Development

| Country/Region | Policy/Initiative | Key Objectives | Key Actions/Incentives |

| China | Support for EV manufacturers, local incentives | Stimulate national EV uptake, encourage major EV companies | Direct incentives along supply chains, joint ventures, and local targets for NEV production |

| United States | Inflation Reduction Act (IRA) | Build a clean energy economy, accelerate EV adoption | Clean Vehicle Tax Credit, funding for incentives and infrastructure, Advanced Manufacturing Production Tax Credits |

| European Union | Green Deal Industrial Plan | Net Zero Industry Act, Critical Raw Materials Act | Faster permitting, financial support, enhanced skills, open trade, focus on battery technologies, tightening CO2 standards |

| India | Production Linked Incentives (PLI) | Boost domestic EV and battery manufacturing | ACC Battery Storage PLI, Automobile, and Auto Component PLI, Battery Waste Management Rules, inferred lithium deposits |

| Other Countries | Various initiatives | Develop domestic battery industries, secure critical minerals | Australia's battery plan, Argentina's domestic market quota, Japan's Green Growth Strategy, Russia's battery industry development, Iran's identified lithium reserves |

Additionally, the government's commitment to a ZEV (zero-emission vehicle) mandate provides manufacturers with a flexible trading scheme, ensuring compliance with annual targets while allowing adaptation to market dynamics. This approach extends beyond the UK, with countries like France, Germany, Sweden, and Canada setting similar targets, indicating a global momentum toward zero-emission vehicles. Thus, increasing countries' commitment towards clean transportation further increases the zero emission vehicle market size globally. Collaborations between governments and private investments further stimulate infrastructure growth, exemplified by the Local Electric Vehicle Infrastructure (LEVI) fund, spurring widespread charging infrastructure development across regions.

Such policy measures and investments support the automotive industry's efforts to scale up production of zero emission vehicles and foster innovations in EV technology. They create an enabling environment for market growth, addressing critical concerns like affordability, infrastructure accessibility, and consumer confidence in EVs. Ultimately, these initiatives aligned with aggressive zero-emission vehicle targets contribute significantly to decarbonizing the transport sector, representing a pivotal stride toward achieving overarching climate goals and a sustainable future.

High Demand For Fuel-Efficient & High-Performance Vehicles

The increasing demand for fuel-efficient and high-performance vehicles is further expected to be the major factor driving the growth of the zero emission vehicle (ZEV) market all across the world. This trend in consumer preferences toward more environmentally friendly vehicles is the result of an interaction of necessitate driving higher demand for such vehicles. Concerns about environmental sustainability and the urgent need to mitigate climate change have heightened consumer consciousness. As a result, there's a substantial shift towards vehicles that minimize carbon emissions and dependency on fossil fuels. This shift aligns with the global push to combat climate change and reduce the carbon footprint of transportation. In addition, advancements in technology have significantly improved the performance of zero emission vehicles. This factor further supports the zero emission vehicle market growth.

Modern electric vehicles (EVs) boast impressive acceleration, range, and overall performance, dispelling traditional perceptions of EVs being inferior in performance to internal combustion engine vehicles. This enhanced performance, coupled with the allure of zero emissions, has spurred consumer interest, leading to increased sales. Supportive government policies and incentives across various countries have further bolstered the adoption of Zero emission vehicles (ZEVs). Nations offering tax incentives, rebates, subsidies, and infrastructure development grants for electric vehicles have seen a notable surge in sales. Countries like Norway, the Netherlands, China, and the United States have witnessed remarkable increases in ZEV sales due to such policies, fostering a conducive environment for consumers to opt for electric and hybrid vehicles.

Moreover, rising fuel prices globally and the increasing awareness of long-term cost savings associated with electric vehicles have played a pivotal role in driving consumer interest. The economic advantage of reduced operational costs, including lower maintenance and fuel expenses over the lifetime of Zero emission vehicles (ZEVs), has swayed consumers towards embracing these vehicles. Furthermore, automakers' concerted efforts to introduce a wide array of electric and hybrid models, catering to various consumer preferences, have significantly contributed to the zero-emission vehicle market size.

Vehicles that offer both fuel efficiency and high performance are becoming more commonplace in the market, appealing to a broader spectrum of consumers seeking eco-friendly options without compromising on performance. Ultimately, the growing demand for fuel-efficient and high-performance vehicles in the zero emission category is driving innovation and competition in the automotive industry. This trend not only benefits the environment by reducing greenhouse gas emissions but also fosters a competitive market that spurs technological advancements, resulting in better-performing, more accessible, and diverse zero-emission vehicles for consumers all across the world.

Inadequate Charging Or Refueling Infrastructure

The scarcity of charging and refueling infrastructure for zero-emission vehicles (ZEVs) like electric or hydrogen fuel cell vehicles is a major factor restraining the widespread adoption of zero emission vehicles all across the world, thereby limiting the zero emission vehicles market growth. This lack of adequate infrastructure, particularly prevalent in rural or less populated areas, significantly hampers market growth. Consumers often face a common apprehension known as "range anxiety," fearing that they might not find charging or refueling stations when needed, limiting their travel options. The absence of a reliable and accessible network of charging stations reinforces this anxiety, dissuading potential buyers from transitioning to ZEVs. In addition, the sparse infrastructure discourages automakers from aggressively producing ZEVs due to concerns about insufficient demand in regions lacking adequate support systems. As a result, the limited availability of charging and refueling stations acts as a significant deterrent, slowing down the market growth of zero-emission vehicles.

Zero Emission Vehicle Market Segment Analysis:

By Vehicle Type: The zero-emission vehicle (ZEV) market experienced a notable shift in 2025, with the fuel cell electric vehicle (FCEV) segment emerging as a dominant force. This trend is driven by increasing consumer awareness of the advantages associated with clean air and a heightened understanding of the adverse effects of traditional automobile emissions. The FCEV segment is poised for further expansion, buoyed by escalating government initiatives and investments aimed at enhancing the infrastructure for electric vehicle charging outlets. The battery electric vehicle (BEV) segment is positioned to be the fastest-growing category from 2026-2034. The surge in demand for environmentally friendly mobility solutions, driven by a desire to mitigate pollution levels, coupled with the allure of tax refunds, is propelling the growth of electric vehicle batteries (EVB). Government programs and incentives designed to promote the adoption of sustainable mobility solutions will play a pivotal role in fostering the expansion of the BEV segment and reducing car pollution.

Based on vehicle class, the commercial segment held the largest market share in 2025. This dominance is attributed to government initiatives fostering the production and adoption of zero-emission vehicles, particularly in the public sector and institutional settings. The integration of electric buses and trains in urban mobility, coupled with government incentives for electric taxis and rickshaws, has been instrumental in driving the growth of the commercial vehicles segment on a global scale. Also, these electric vehicles find extensive use in various government-operated, owned, or controlled industries, serving as a model for both commercial and private sectors within the economy. The impetus for this adoption is not only environmental but also economical, as the escalating prices of crude oil and gas incentivize commercial operators to transition to electric vehicles, offering potential long-term savings in operational costs.

Zero Emission Vehicle Market Regional Insights:

North America led the global zero emission vehicle market with the highest market share of 43.78% in 2025. The region is further expected to grow at a CAGR of 18.45% during the forecast period. Certain States like California have witnessed a rapid increase in ZEV consumption as a result of strict pollution regulations and lucrative EV incentives. The Zero-Emission Vehicle (ZEV) program in California, led by CARB's Advanced Clean Cars initiative, plays a pivotal role in aligning vehicle emissions with health-based air quality standards and greenhouse gas reduction objectives. Designed to augment ZEV requirements and bolster the adoption of zero-emission technologies, this regulation within ACC II aims for all new vehicles in California to transition to 100% zero-emission and clean plug-in hybrid-electric models by the 2035 model year.

Notably, the program encompasses innovative measures such as warranties, durability requirements, and serviceability standards to facilitate consumers in transitioning to new or used zero-emission and plug-in hybrid electric vehicles. As California grapples with extreme ozone non-attainment in areas like greater Los Angeles and the San Joaquin Valley, ZEV regulation emerges as a hub in addressing air quality issues and curtailing the state's impact on climate change. The significance of the ZEV regulation is evident in its contribution to substantially reducing smog-forming and greenhouse gas pollutants compared to vehicles complying with 2025 stringent fleet standards.

However, its impact extends beyond emissions reduction. The regulation mandates large and intermediate volume vehicle manufacturers to ensure a certain proportion of their sales comprise plug-in hybrids or zero-emission vehicles, thereby driving automakers to invest in and produce environmentally friendly vehicle options. This factor is expected to support the North American zero emission vehicle market size. As a result, manufacturers such as BMW, Ford, General Motors, Toyota, and others are compelled to align their offerings with ZEV standards. Moreover, smaller manufacturers like Tesla and Volvo, while obligated to comply, have the flexibility to meet requirements through plug-in hybrids. Credits generated by these manufacturers are closely monitored by CARB, underscoring the accountability in complying with ZEV mandates.

California's regulations have reverberations beyond its borders due to the Section 177 provision in the Clean Air Act, allowing other states to adopt similar stringent standards. These states, commonly known as Section 177 states, have the potential to mirror California's approach to ZEV adoption, thereby creating a broader market for zero-emission vehicles across the United States. This interplay between stringent regulatory frameworks and their adoption by other states significantly influences the growth and expansion of the zero emission vehicle market, fostering innovation, investment, and a more sustainable automotive landscape nationally.

Timeline of Regulatory Activities

| 2022 | The Advanced Clean Cars II regulations were adopted in 2022, imposing the next level of low-emission and zero-emission vehicle standards for model years 2026-2035 that contribute to meeting federal ambient air quality ozone standards and California’s carbon neutrality targets. |

| 2017 | In March 2017 CARB staff presented the Board with the results of CARB's Midterm Review. In addition, staff already provided yearly status updates to the Board since the ACC regulations were first adopted in January 2012. |

| 2015 | 2015 Regulatory Activities | The 2015 modifications were developed to ensure that any additional ZEV credits awarded to fast refueling ZEVs were awarded on a one-to-one basis. The proposed rulemaking action was withdrawn on December 1, 2015. |

| 2014 | 2014 Regulatory Activities | The 2014 amendments provided greater flexibility to intermediate volume manufacturers in complying with their ZEV credit obligations, while still maintaining the Board’s commitment to a strengthened ZEV regulation. On October 12, 2015, the Office of Administrative Law (OAL) approved amendments to the ZEV regulation that were adopted by the Board on May 21, 2015. The rulemaking became effective on January 1, 2016. |

| 2013 | 2013 Regulatory Activities | Staff proposed minor modifications for the ZEV regulation to include clarifying the Section 177 state optional compliance path provision, defining how caps apply to an auto manufacturer's requirement, and excluding battery swapping as a "fast refueling" technology. OAL approved the 2013 rulemaking and filed it with the Secretary of State on July 10, 2014. The rulemaking became effective the same day. |

| 2010 - 2012 | 2010-2012 Regulatory Activities | The Board adopted regulatory changes to the ZEV program in 2012 that substantially increased and simplified requirements for 2018 and subsequent model years. California's Low-Emission Vehicle (LEV) regulations were amended, known as LEV III, to increase the stringency of tailpipe and greenhouse gas emission standards for new passenger vehicles. The 2012 modifications combined the control of smog-causing pollutants and greenhouse gas emissions into a single coordinated package of standards called Advanced Clean Cars. OAL approved the 2012 rulemaking and filed it with the Secretary of State on August 7, 2012. The regulation became effective the same day. |

The Zero-Emission Vehicle (ZEV) regulations adopted by New York State, following California's LEV program model, signify a pivotal commitment to reducing emissions from on-road motor vehicles and engines, emphasizing stringent emission control systems. The program mandates adherence to California's more rigorous emissions standards for all new vehicles sold in the state, aiming to curtail smog-forming pollutants like hydrocarbons, carbon monoxide, and oxides of nitrogen. ZEV standards within this program encompass a variety of vehicles, including Battery Electric Vehicles, Fuel Cell Vehicles, and Plug-in Hybrid Electric Vehicles (PHEVs), designed to significantly diminish tailpipe emissions and foster a cleaner environment.

Particularly, the state's focus on Medium- and Heavy-Duty (MHD) ZEVs, underscored by a joint memorandum of understanding signed by several states, including New York, aims to ensure that 100% of new MHD vehicle sales will be ZEV by 2050, with an interim target of 30% by 2034. This initiative aligns with New York's Climate Leadership and Community Protection Act, which outlines aggressive greenhouse gas emission reduction goals. The program's focus on decarbonizing transportation systems and offering incentives through various initiatives like the New York Truck Voucher Incentive Program and the Public Service Commission Make Ready Program reflects the state's concerted efforts to promote and facilitate the adoption of ZEVs.

This regulatory framework significantly influences the zero emission vehicle market by setting a precedent and creating a demand for cleaner vehicles, particularly in the medium- and heavy-duty sectors. By mandating more stringent emissions standards and prioritizing ZEV technologies, New York State not only shapes its local market but also contributes to the broader national push towards zero-emission vehicles. The focus on reducing GHG emissions and pollutants from medium- and heavy-duty vehicles, which disproportionately contribute to overall emissions, highlights the program's crucial role in achieving climate goals and improving air quality. Moreover, the state's commitment to developing action plans, seeking stakeholder input, and collaborating with partner states underlines its dedication to fostering a robust ZEV infrastructure and is further expected to boost the zero emission vehicle industry in North America, creating an environment conducive to innovative technologies and sustainable transportation solutions.

Zero Emission Vehicle Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 24 July 2025 | Zhejiang Geely Holding Group | Geely launched the updated Galaxy E5 electric SUV with a price drop to RMB 109,800 (~USD 15,340) and an enhanced CLTC range up to 610 km. | Boosts mass-market competitiveness and drives higher consumer affordability and adoption in the zero-emission vehicle sector. |

| 25 June 2025 | BYD Company Ltd. | BYD signed a strategic agreement with Austrian steelmaker voestalpine to supply high-quality sheet steel for its new passenger car factory in Szeged, Hungary. | Accelerates regional manufacturing scale and establishes a robust local supply chain for European zero-emission vehicle production. |

| 15 July 2025 | Tesla, Inc. | Tesla signed a USD 4.3 billion deal with LG Energy Solution to supply LFP batteries starting August 2027 from its Michigan factory for energy storage systems. | Enhances supply chain resilience by securing domestic production capacity and mitigating reliance on external components. |

| 10 August 2025 | General Motors Company | General Motors announced temporary battery imports from CATL to support affordable EV models, including the upcoming Chevrolet Bolt featuring LFP chemistry. | Accelerates the delivery of low-cost zero-emission vehicles while bridging production gaps ahead of domestic LFP plant opening. |

| 12 July 2026 | Volkswagen Group | Volkswagen showcased its new ID. Cross electric SUV priced below USD 30,000 as part of its strategic rollout for mass-market EVs in Europe. | Expands customer accessibility to zero-emission driving and strengthens market penetration across competitive segments. |

| 18 July 2026 | Zhejiang Geely Holding Group | Geely partnered with Ford to produce its zero-emission electric SUVs at Ford's manufacturing plant in Spain to supply the European market. | Optimizes production capacity, improves operational efficiency, and expands European regional footprint. |

Zero Emission Vehicle Market Competitive Landscape

The zero-emission vehicle (ZEV) market is characterized by intense competition among established players and new entrants seeking to gain market share. Several major automotive manufacturers, including Tesla, Toyota, General Motors, and Ford, have a significant presence in the market. These companies have invested heavily in ZEV technology and have released popular ZEV models, which have contributed to their market share. In recent years, new entrants such as Rivian, Lucid Motors, and Fisker have emerged in the ZEV market. These companies often specialize in a niche market or innovative technology that allows them to differentiate themselves from established players.

As a result, they have been able to capture a portion of the market and increase their market share. Battery manufacturers are also key players in the ZEV market, as ZEVs rely on batteries for power. Panasonic, LG Chem, and CATL are some of the major battery manufacturers in the market, and they often partner with automotive manufacturers to provide batteries for ZEVs. These partnerships are critical for ZEV manufacturers, as battery technology is a key determinant of vehicle range, performance, and cost. Infrastructure providers are another important player in the ZEV market. Charging or refueling infrastructure is necessary for ZEVs, and companies such as ChargePoint, EVgo, and Shell are major infrastructure providers.

The Cars With The Lowest CO2 Emissions In 2022

| Cars With Lowest CO2 Emissions | Green Score |

| Make And Model: Hyundai Sonata Hybrid Blue | 63 |

| Make And Model: Tesla Model Y Rear-Drive EV | 63 |

| Make And Model: Toyota Camry Hybrid LE | 63 |

| Make And Model: Honda Insight Hybrid | 64 |

| Make And Model: Toyota Corolla Hybrid | 64 |

| Make And Model: Mazda MX-30 EV | 65 |

| Make And Model: Hyundai Elantra Hybrid Blue | 65 |

| Make And Model: Kia Niro PHEV | 65 |

| Make And Model: Nissan LEAF EV | 67 |

| Make And Model: MINI Cooper SE EV | 67 |

| Make And Model: Hyundai Ioniq PHEV | 68 |

| Make And Model: Toyota Prius Prime PHEV | 69 |

These companies often partner with governments and businesses to install charging or refueling stations, which is critical for the adoption of ZEVs. Some recent mergers and acquisitions that have taken place in the zero-emission vehicle (ZEV) market: In 2022, Stellantis acquired French electric vehicle startup, e-Legend. In 2022, Hyundai Motor Group acquired Boston Dynamics, a robotics company that is developing robots that could be used in the automotive industry. In 2022, BMW acquired Solid Power, a company that is developing solid-state batteries for electric vehicles. In 2022, Volkswagen acquired QuantumScape, a company that is developing solid-state batteries for electric vehicles. Governments also play a critical role in the ZEV market.

Zero Emission Vehicle Market Scope: Inquire before buying

| Zero Emission Vehicle Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 257.43 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 21.2% | Market Size in 2034: | US $ 1452.74 Bn. |

| Segments Covered: | by Vehicle Class | Passenger Cars Commercial Vehicles Two Wheelers |

|

| by Price | Mid-Priced Luxury |

||

| by Vehicle Type | BEV PHEV FCEV Solar Vehicles |

||

| by Vehicle Drive Type | Front Wheel Drive Rear Wheel Drive All Wheel Drive |

||

| by Vehicle Speed | Less Than 100 MPH 100 to 125 MPH More Than 125 MPH |

||

Zero Emission Vehicle Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Zero Emission Vehicle Key Players

1. Tesla (United States)

2. General Motors (United States)

3. Ford Motor Company (United States)

4. Fisker Inc. (United States)

5. Rivian Automotive LLC (United States)

6. Proterra Inc. (United States)

7. Volkswagen Group (Germany)

8. BMW Group (Germany)

9. Daimler AG (Germany)

10. Volvo Group (Sweden)

11. Jaguar Land Rover Automotive PLC (United Kingdom)

12. BYD Company Limited (China)

13. SAIC Motor Corporation Limited (China)

14. Hyundai Motor Company (South Korea)

15. Kia Corporation (South Korea)

16. Panasonic Corporation (Japan)

17. Toyota Motor Corporation (Japan)

18. Electra Vehicles (UAE)

19. Himoinsa Middle East FZE (UAE)

20. Joule Africa (South Africa)

21. Veecraft Marine (South Africa)

22. Foton Motor Group (China) - operating in Kenya, Algeria, Egypt

23. Renault Group (France) - operating in Morocco and South Africa

24. Volkswagen do Brasil Ltda (Brazil)

25. Nissan do Brasil Automóveis Ltda (Brazil)

Frequently Asked Questions:

1: What are the different types of zero emission vehicles?

Ans: The main types of zero emission vehicles are battery electric vehicles (BEVs), hydrogen fuel cell vehicles (FCVs), and plug-in hybrid electric vehicles (PHEVs).

2: What is driving the growth of the zero-emission vehicle market?

Ans: The growth of the zero-emission vehicle market is being driven by factors such as increasing environmental concerns, government policies and regulations, technological advancements, and growing consumer demand.

3: What are some challenges facing the zero-emission vehicle market?

Ans: Some challenges facing the zero-emission vehicle market include high initial costs, limited driving range, lack of charging/fueling infrastructure, and consumer perceptions and preferences.

4: Which regions are leading in the zero-emission vehicle market?

Ans: North America, Europe, and Asia Pacific are currently the leading regions in the zero-emission vehicle market, with increasing growth and investment also being seen in the Middle East, Africa, and South America.

5: Who are some key players in the zero-emission vehicle market?

Ans: Key players in the zero-emission vehicle market include companies such as Tesla, Volkswagen Group, BYD Company Limited, Hyundai Motor Company, and Toyota Motor Corporation, among others.

6: How is the zero-emission vehicle market expected to grow in the future?

Ans: The zero-emission vehicle market is expected to grow significantly in the coming years, with increasing investment in research and development, government incentives and policies, and consumer demand all contributing to the market's growth. Some projections estimate that ZEVs could account for as much as 30% of all vehicle sales by 2034.