Welding Electrode Market by Type, End-User and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

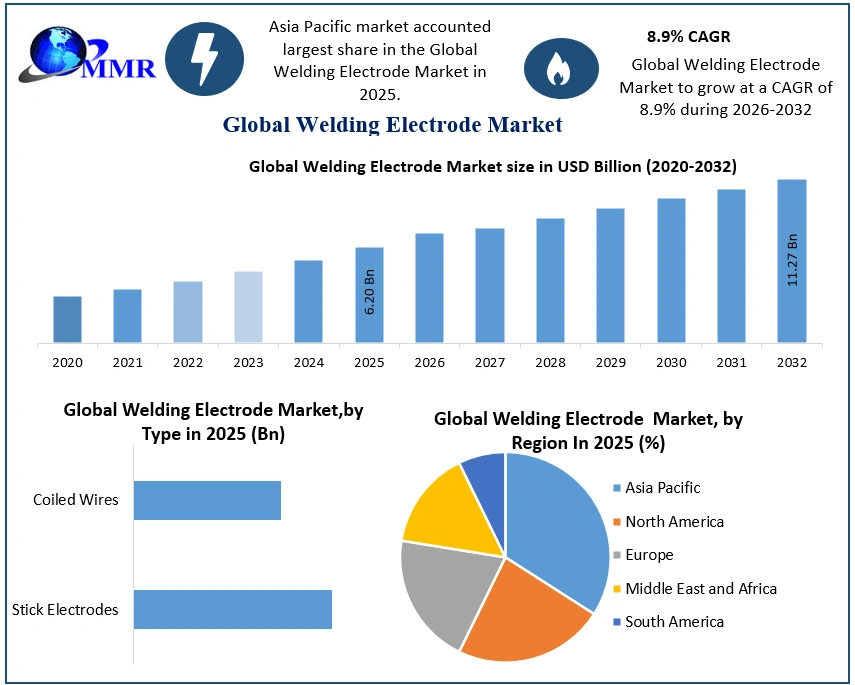

The Welding Electrode Market size was valued at USD 6.20 Billion in 2025 and the total Welding Electrode revenue is expected to grow at a CAGR of 8.9% from 2025 to 2032, reaching nearly USD 11.27 Billion by 2032.

Welding Electrode Market Overview

The welding electrode market is a segment of the broader welding industry. A welding electrode is a consumable metal rod or wire that conducts electricity and is used in various welding processes to join two pieces of metal together. These electrodes are used in various welding processes to join two pieces of metal together by creating an electric arc that melts the base metal and the electrode, forming a molten pool that cools and solidifies into a strong, durable bond.

The welding electrode market is highly competitive, with a wide range of manufacturers and suppliers operating globally. The market is driven by factors such as increasing demand for infrastructure development, industrialization, and construction activities worldwide. The report details the impact of the growing use of welding electrodes in various end-use industries such as automotive, construction, and oil & gas is also contributing to the growth of the market.

The market is segmented based on the type of electrode, coating type, welding process, end-use industry, and region. The most common types of electrodes used in welding include stick electrodes, flux-cored electrodes, and metal-cored electrodes. Coating types can include rutile, basic, and cellulose coatings, among others. Welding processes that use electrodes include shielded metal arc welding (SMAW), gas metal arc welding (GMAW), and submerged arc welding (SAW).

The major players in the welding electrode market included in the report are Lincoln Electric Holdings Inc., ESAB, Colfax Corporation, Ador Welding Limited, and ITW Welding, among others. These companies are involved in developing new and innovative welding electrode products to cater to the changing needs of customers and to remain competitive in the market.

The welding electrode market is expected to continue to grow in the forecasted period, driven by the increasing demand for infrastructure development and industrialization globally. Additionally, the growing popularity of automated welding technologies is expected to provide further opportunities for growth in the market.

To know about the Research Methodology :- Request Free Sample Report

Welding Electrode Market Research Methodology

The research conducted utilized both primary and secondary data sources to ensure that all possible factors affecting the market were thoroughly examined and validated. The market size for top-level markets and sub-segments is normalized and the impact of inflation, economic downturns, regulatory & policy changes, and other variables is factored into the market forecast.

The bottom-up approach and multiple data triangulation methodologies are used to estimate the market size and forecasts. The percentage splits, market shares and breakdowns of the segments are derived based on weights assigned to each of the segments on their utilization rate and average sale price. The country-wise analysis of the overall Welding Electrode market and its sub-segments are based on the percentage adoption or utilization of the given market Size in the respective region or country. Major players in the market are identified through secondary research based on indicators that include market revenue, price, services offered, advancements, mergers and acquisitions, and joint.

Extensive primary research was conducted to acquire information and verify and confirm the crucial numbers arrived at after comprehensive market engineering and calculations for market statistics, market size estimations, market forecasts, market breakdown, and data triangulation.

Welding Electrode Market Dynamics

The rise in industrialization and manufacturing activities across the world is driving demand for welding electrodes. The increasing production of automobiles, machinery, and other equipment requires welding, which, in turn, drives demand for welding electrodes. The use of welding electrodes is growing in various end-use industries such as automotive, construction, and oil & gas. The demand for low-hydrogen electrodes is expected to drive market growth in the coming years. Low-hydrogen electrodes are designed to produce high-quality welds with minimal hydrogen content, which reduces the risk of cracking and other defects in the welded joint. As a result, they are preferred for critical applications such as nuclear power plants, oil and gas pipelines, and pressure vessels.

For instance, in February 2021, Bohler Welding, a subsidiary of voestalpine AG, launched a new range of low-hydrogen welding electrodes for the oil and gas industry. The new electrodes are designed to provide excellent performance in challenging environments, such as sour gas and high-pressure applications. The report consists of a comprehensive analysis of the impact of all such drivers of the market.

The welding electrode market faces several challenges that could hinder its growth in the forecasted period. One of the major challenges is the increasing competition from alternative welding technologies, such as laser welding and friction stir welding, among others. These technologies offer several advantages over traditional welding processes, such as higher welding speeds, reduced heat input, and better weld quality. For instance, in March 2021, Researchers at the Fraunhofer Institute for Laser Technology ILT developed a new laser welding process that enables the production of lightweight components with high-strength welds.

The new process offers several advantages over traditional welding processes, such as lower distortion, reduced heat input, and better weld quality. Moreover, the welding electrode market is also facing challenges due to increasing concerns regarding worker safety and health. Welding involves several hazards, such as exposure to harmful fumes, radiation, and noise, among others. As a result, several governments and regulatory bodies have implemented regulations and guidelines to ensure worker safety and health. The report contains an exhaustive list of laws concerning the welding electrode industries on basis of region to help manufacturers take informed decisions.

Despite these challenges, the welding electrode market offers several opportunities for growth in the forecasted period. One of the major opportunities is the increasing demand for welding electrodes in emerging economies, such as China, India, and Brazil, among others. These countries are witnessing rapid industrialization and urbanization, which is driving the demand for infrastructure development and expansion.

For instance, in September 2020, the Indian government announced a new National Infrastructure Pipeline (NIP) project, which aims to invest $1.4 trillion in various infrastructure projects across the country by 2025. The project is expected to boost the demand for welding electrodes in India in the forecasted period.

The adoption of Industry 4.0 technologies is expected to create new opportunities for growth in the welding electrode market. Industry 4.0 technologies, such as artificial intelligence, the Internet of Things (IoT), and robotics, among others, are transforming the manufacturing sector by enabling automation, efficiency, and productivity.

For instance, in October 2020, Lincoln Electric announced the launch of its new Power Wave C300 welding system, which is equipped with Industry 4.0 technologies such as cloud-based software and remote monitoring capabilities. The new system is designed to provide high-quality welds and improve productivity in the welding process.

There is a growing trend towards environmentally sustainable welding electrodes, which are free from harmful substances such as hexavalent chromium and nickel. Manufacturers are focusing on developing these sustainable products to cater to the changing needs of customers.

Regulatory Scenario for Welding Electrode Market across the World:

The welding electrode market is subject to various regulations and standards across the world, which aim to ensure the safety and quality of welding products and processes. These regulations cover several aspects of welding, such as the composition of welding electrodes, the safety of welding equipment, and the health and safety of workers involved in welding activities.

One of the main areas of regulation in the welding electrode market is the composition of welding electrodes. Another area of regulation in the market is the safety of welding equipment. Welding equipment can pose a fire or explosion hazard if not properly maintained or used, and can also emit harmful fumes and radiation during welding operations. To address these risks, various organizations have established standards and guidelines for welding equipment, such as the National Fire Protection Association (NFPA) in the United States and the International Electrotechnical Commission (IEC) in Europe. These standards cover topics such as equipment design, maintenance, and operation, and aim to ensure the safe and efficient use of welding equipment.

Welding Electrode Market Segmentation

Welding Electrode Market by End-use industry:

Automotive: Welding electrodes are used extensively in the automotive industry for the manufacture of car bodies, frames, and other components.

Construction: Welding electrodes are used in the construction industry for the fabrication of steel structures, bridges, and other infrastructure.

Oil & gas: Welding electrodes are used in the oil & gas industry for the fabrication of pipelines, tanks, and other equipment.

Shipbuilding: Welding electrodes are used in the shipbuilding industry for the manufacture of ships, boats, and other marine vessels.

Aerospace & defence: Welding electrodes are used in the aerospace and defence industry for the manufacture of aircraft, spacecraft, and other equipment.

Others: This category includes other industries such as agriculture, mining, and power generation.

Welding Electrode Market by Region

North America: The welding electrode market in North America is driven by the increasing demand for welding electrodes in various end-use industries such as construction, automotive, and aerospace. The United States and Canada are the major contributors to the growth of the market in this region.

Europe: The European welding electrode market is driven by the increasing demand for welding electrodes in the automotive and construction industries. Germany, France, and the United Kingdom are the major contributors to the growth of the market in this region.

Asia-Pacific: The Asia-Pacific region is expected to be the fastest-growing market for welding electrodes due to the increasing demand for welding electrodes in various end-use industries such as automotive, construction, and shipbuilding. China, India, and Japan are the major contributors to the growth of the market in this region.

Latin America: The Latin American welding electrode market is driven by the increasing demand for welding electrodes in the construction and automotive industries. Brazil and Mexico are the major contributors to the growth of the market in this region.

Middle East & Africa: The Middle East & Africa welding electrode market is driven by the increasing demand for welding electrodes in the oil & gas and construction industries. Saudi Arabia, the United Arab Emirates, and South Africa are the major contributors to the growth of the market in this region.

Welding Electrode Market Competitive Analysis

The market is highly competitive, with several players operating in the market, ranging from large multinational corporations to small and medium-sized enterprises. The market players compete on various factors, including product quality, price, brand image, and innovation.

One of the major players in the welding electrode market is Lincoln Electric Holdings, Inc. The company focuses on product innovation and has introduced several new products in recent years, such as the Excalibur® 7018 XMR™ electrode, which offers improved performance in demanding welding applications.

Another significant player in the welding electrode market is ESAB Group, Inc. The company is also focused on innovation and has introduced several new products such as the OK Tubrod 15.15, a low hydrogen flux-cored wire designed for offshore and shipbuilding applications.

Other players in the welding electrode market include Kobelco Welding of America Inc., Air Liquide S.A., Illinois Tool Works Inc., The Linde Group, Hyundai Welding Co., Ltd., Tianjin Bridge Welding Materials Group Co., Ltd., and voestalpine Böhler Welding GmbH.

In recent years, the welding electrode market has seen several strategic initiatives by key market players, such as mergers and acquisitions, partnerships, and product launches.

For example, in 2020, Lincoln Electric Holdings, Inc. acquired Baker Industries, Inc., a provider of custom tooling, parts, and fixtures for the aerospace and automotive industries. The acquisition is expected to strengthen Lincoln Electric's position in the aerospace and automotive sectors.

Welding Electrode Market Scope: Inquire before buying

| Global Welding Electrode Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 6.20 Billion. |

| Forecast Period 2026 to 2032 CAGR: | 8.9 % | Market Size in 2032: | USD 11.27 Billion. |

| Segments Covered: | By Type | Stick Electrodes Coiled Wires |

|

| By End User | Automotive Construction Oil & gas Aerospace & defence Others |

||

Global Welding Electrode Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Leading Companies in the Welding Electrode Market

The report has covered the profiles of Welding Electrode companies from a strategic perspective. Selection of these key Welding Electrode Manufacturers has been done on certain criteria.

1. The Lincoln Electric Company

2. ESAB Corporation

3. Illinois Tool Works Inc.

4. Kobelco Welding of America Inc.

5. Hobart Brothers LLC

6. Weld Mold Company

7. Select-Arc, Inc.

8. voestalpine Böhler Welding GmbH

9. EWM AG

10. GYS

11. Hilarius Haarlem Holland BV

12. Welding Alloys Group

13. Air Liquide S.A.

14. The Linde Group

15. Hyundai Welding Co., Ltd.

16. Kobe Steel, Ltd.

17. Obara Corporation

18. Ador Welding Limited

19. Superon Schweisstechnik India Ltd.

20. Mishra Dhatu Nigam Limited (MIDHANI)

21. Gedik Welding

22. Weldcomelectrodes

23. Afrox

24. Ador Welding

25. Superon Schweisstechnik India

Frequently Asked Questions:

1. Which region held the largest Welding Electrode Market share in 2025?

Ans: Asia-Pacific region held the largest Welding Electrode Market share in 2025.

2. What is the expected Global Welding Electrode Market size by 2032?

Ans: The expected Global Welding Electrode Market size by 2032 is USD 11.27 Billion.

3. What is the expected CAGR of the Global Welding Electrode Market during the forecast period?

Ans: The Global Welding Electrode Market is expected to grow at a CAGR of 6.9% during the forecasting period 2026-2032.

4. What segments are covered in Global Welding Electrode Market report?

Ans: Global Welding Electrode Market is segmented into type and end user.

5. What is the Forecast period of the Welding Electrode Market research?

Ans: The Forecast period of the Welding Electrode Market research is from 2026-2032.