Global Water Electrolysis Market Size by Technology Type and End User – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

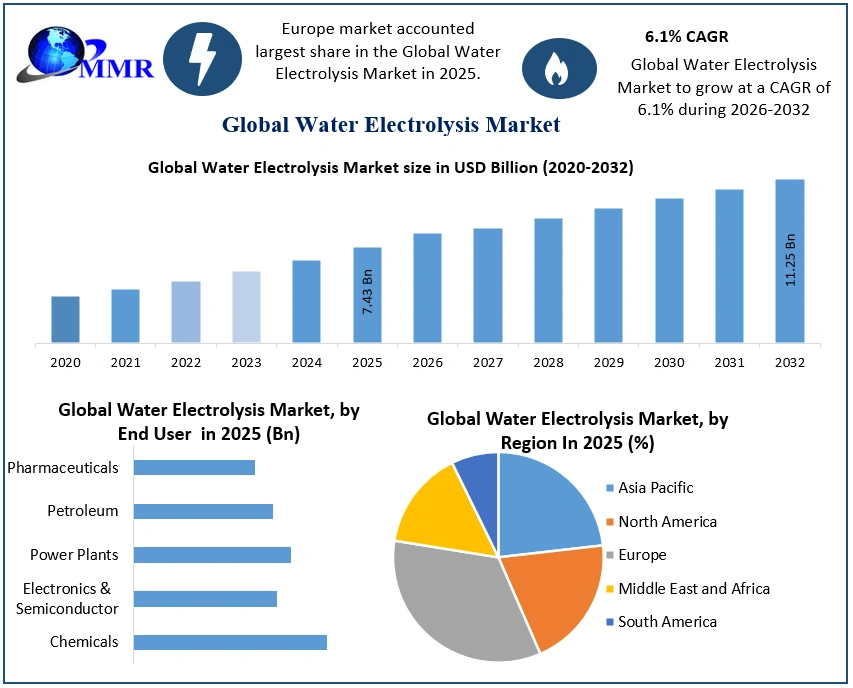

The Water Electrolysis Market size was valued at USD 7.43 Billion in 2025 and the total Water Electrolysis revenue is expected to grow at a CAGR of 6.1% from 2026 to 2032, reaching nearly USD 11.25 Billion by 2032.

Water Electrolysis Market Industry & Technology Overview

Water electrolysis is a key technology for producing green hydrogen by using electricity to split water into hydrogen and oxygen. When powered by renewable energy sources such as solar, wind, or hydropower, the process enables the production of low-carbon or zero-emission hydrogen, making it a critical component of global decarbonization and clean energy transition strategies. Electrolyzers are available in various capacities, ranging from small decentralized systems to large industrial-scale facilities integrated with renewable power plants. Growing government support, investments in hydrogen infrastructure, and technological advancements are accelerating the adoption of water electrolysis across industries including transportation, power generation, chemicals, and steel manufacturing. As countries pursue net-zero emission targets, water electrolysis is expected to play a pivotal role in expanding the global green hydrogen economy.

To know about the Research Methodology :- Request Free Sample Report

Global Water Electrolysis Market Dynamics

Market Drivers

Growing global demand for green hydrogen to support decarbonization across industries such as transportation, power generation, chemicals, and steel manufacturing is driving the adoption of water electrolysis technologies. The Supportive government policies, funding programs, and national hydrogen strategies are accelerating investments in electrolyzer deployment and green hydrogen production projects worldwide.

Rapid expansion of renewable energy capacity, including solar and wind power, is increasing the feasibility of producing low-carbon hydrogen through water electrolysis. Technological advancements in electrolyzers, including improvements in efficiency, durability, and cost reduction, are enhancing the commercial viability of water electrolysis systems.

Market Restraints / Challenges

High capital costs associated with electrolyzers and green hydrogen production remain a major barrier to large-scale adoption. Dependence on affordable renewable electricity can limit project economics in regions with high electricity prices or limited renewable energy infrastructure.

Limited hydrogen storage, transportation, and refueling infrastructure poses challenges to the widespread commercialization of green hydrogen.

Supply chain constraints and the availability of critical materials, such as iridium and platinum used in advanced electrolyzers, may impact manufacturing capacity and increase costs.

Market Opportunities

Increasing investments in green hydrogen projects across developed and emerging economies are creating significant growth opportunities for electrolyzer manufacturers.Growing adoption of green hydrogen in hard-to-abate sectors, including steel, ammonia, refining, and heavy transportation, is expanding the market potential.

Development of large-scale renewable energy and hydrogen hubs is expected to accelerate the deployment of water electrolysis systems globally.

Continuous innovation in electrolyzer technologies, including Proton Exchange Membrane (PEM), Alkaline, and Solid Oxide Electrolyzers (SOEC), is improving efficiency and reducing production costs.

Market Trends

Rapid scaling of gigawatt-scale electrolyzer manufacturing facilities to meet increasing global demand for green hydrogen.

Strategic partnerships and collaborations among energy companies, technology providers, and governments to accelerate hydrogen infrastructure development.

Increasing focus on cost reduction and efficiency improvements through advanced materials, automation, and next-generation electrolyzer designs.

Expansion of integrated renewable energy-to-hydrogen projects, combining solar, wind, and water electrolysis to produce sustainable hydrogen for industrial and energy applications.

Global Water Electrolysis Market Segment Analysis

By Technology Type

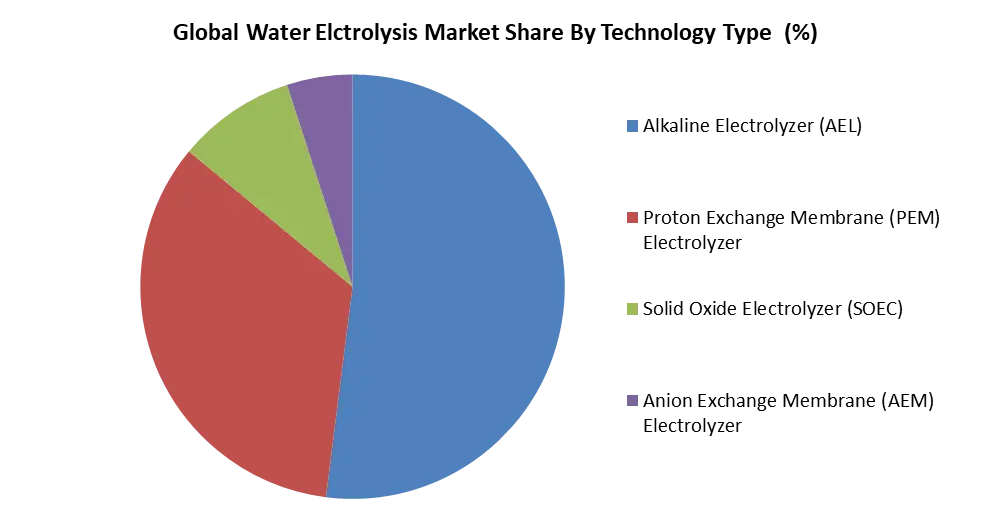

The technology segment of the global water electrolysis market is dominated by Alkaline Electrolyzers (AEL), which accounted for the largest market share in 2025 and are expected to maintain their dominance throughout the 2025–2032 forecast period.

Their widespread adoption is attributed to lower capital costs, proven commercial reliability, long operational life, and suitability for large-scale industrial hydrogen production. Proton Exchange Membrane (PEM) electrolyzers are projected to witness the fastest growth during the forecast period, driven by their high efficiency, compact design, rapid response to intermittent renewable energy sources, and increasing deployment in green hydrogen projects. Meanwhile, Solid Oxide Electrolyzers (SOEC) and Anion Exchange Membrane (AEM) electrolyzers are gaining traction due to ongoing technological advancements, improved energy efficiency, and growing investments in next-generation hydrogen production technologies.

By Application Type

The application segment of the global water electrolysis market is led by industrial feedstock, which held the largest market share in 2025. Hydrogen produced through water electrolysis is extensively used in ammonia, methanol, and petroleum refining processes, with industries increasingly transitioning to green hydrogen to meet decarbonization targets.

The transportation segment is anticipated to register the fastest growth, supported by rising adoption of hydrogen fuel cell vehicles, expanding hydrogen refueling infrastructure, and government initiatives promoting clean mobility. In addition, applications in power generation and energy storage and power-to-gas systems are witnessing significant growth as renewable energy integration and grid-balancing solutions drive demand for sustainable hydrogen production. Continuous investments in large-scale green hydrogen projects are expected to further expand the application scope of water electrolysis worldwide.

Global Water Electrolysis Market Regional Insights

Europe

Europe dominated the global water electrolysis market in 2025 and is expected to maintain its leadership throughout the 2025–2032 forecast period. The region's growth is driven by ambitious decarbonization goals, the European Union's Hydrogen Strategy, substantial government funding, and increasing investments in green hydrogen infrastructure. Countries such as Germany, the Netherlands, France, and Spain are leading the deployment of large-scale electrolyzer projects and renewable hydrogen production facilities.

North America

North America holds a significant market share, supported by growing investments in clean hydrogen production, favorable government incentives, and expanding renewable energy capacity. The United States and Canada are investing in hydrogen hubs, electrolyzer manufacturing, and industrial decarbonization projects to accelerate the adoption of green hydrogen across transportation, power generation, and heavy industries.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market during the forecast period, driven by rapid industrialization, increasing renewable energy installations, and strong government support for hydrogen development. Countries including China, Japan, South Korea, India, and Australia are making substantial investments in hydrogen infrastructure, electrolyzer manufacturing, and large-scale green hydrogen projects to strengthen energy security and achieve net-zero emission targets.

Latin America

Latin America is emerging as a promising market due to its abundant solar and wind energy resources, particularly in Chile and Brazil. Government initiatives, foreign investments, and the development of renewable energy-based hydrogen projects are expected to support steady market growth over the forecast period.

Middle East & Africa

The Middle East & Africa region is witnessing increasing investments in large-scale green hydrogen production, leveraging its abundant solar and wind resources. Countries such as Saudi Arabia, the United Arab Emirates, and Oman are developing hydrogen export projects and renewable energy infrastructure, positioning the region as a future global supplier of green hydrogen.

Global Water Electrolysis Market Competitive Landscape

The global water electrolysis market is moderately consolidated, with competition driven by established industrial gas companies, electrolyzer manufacturers, and clean energy technology providers. Market participants are focusing on technological innovation, capacity expansion, strategic partnerships, mergers and acquisitions, and large-scale green hydrogen projects to strengthen their market presence.

Competitive Strategies

-

- Expansion of gigawatt-scale electrolyzer manufacturing capacity to meet the growing global demand for green hydrogen.

- Continuous R&D investment in alkaline, PEM, SOEC, and AEM electrolyzer technologies to improve efficiency, durability, and reduce production costs.

- Strategic partnerships with renewable energy developers, industrial manufacturers, and governments to accelerate commercial hydrogen projects.

- Geographic expansion into high-growth markets across Europe, Asia-Pacific, North America, and the Middle East.

- Focus on integrated renewable energy-to-hydrogen solutions and turnkey green hydrogen projects.

Recent Developments In Hydrogen Electrolysis Market

| Date | Recent Development |

| March 2026 | thyssenkrupp nucera AG & Co. KGaA announced continued expansion of its large-scale alkaline water electrolysis portfolio to support industrial green hydrogen projects. |

| January 2026 | Nel ASA expanded electrolyzer manufacturing capacity to address increasing global demand for green hydrogen infrastructure. |

| September 2025 | ITM Power plc secured new contracts for large-scale PEM electrolyzer projects supporting renewable hydrogen production in Europe. |

| June 2025 | Plug Power Inc. announced progress in developing integrated green hydrogen production facilities using advanced PEM electrolyzer technology. |

| November 2024 | Siemens Energy AG expanded collaborations on industrial-scale electrolyzer deployments to accelerate green hydrogen production and energy transition initiatives. |

Water Electrolysis Market Scope: Inquire Before Buying

| Global Water Electrolysis Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 7.43 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.1% | Market Size in 2032: | USD 11.25 Bn. |

| Segments Covered: | By Technology Type | Alkaline Electrolysis PEM (Proton Exchange Membrane) Electrolysis Solid Oxide Electrolysis Anion Exchange Membrane (AEM) Electrolyzers |

|

| By Capacity | Less than 500 kW 500kW - 2 MW Above 2 MW |

||

| By Application | Power Generation and Energy Storage Transportation Industrial Feedstock Power to Gas Others |

||

| by End Use- Industry | Chemicals Industry Power Generation Oil & Gas Steel and Petroleum Transportation |

||

Water Electrolysis Market, by Region:

1. North America (United States, Canada, and Mexico)

2. Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

3. Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

4. Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

5. South America (Brazil, Argentina Rest of South America)

Water Electrolysis Market, Key Players

1. Nel ASA

2. Siemens Energy AG

3. Cummins Inc.

4. ITM Power plc

5. McPhy Energy S.A.

6. Plug Power Inc.

7. Toshiba Energy Systems & Solutions Corporation

8. Enapter AG

9. Giner ELX

10. Areva H2Gen

11. Green Hydrogen Systems

12. Kobelco Eco-Solutions Co., Ltd.

13. Next Hydrogen

14. ERGOSUP

15. Ceres Power Holdings plc

FAQs:

1. What are the growth drivers for the Water Electrolysis market?

Ans: The primary growth drivers for the Water Electrolysis market include Increasing focus on renewable energy sources for hydrogen production. Government initiatives and policies promoting green hydrogen. Additionally, Growing demand for clean fuels in various industries like transportation and power generation.

2. What is the major restraint for the Water Electrolysis market growth?

Ans. One significant restraint for the Water Electrolysis market growth is the high initial capital investment required for establishing electrolysis facilities, hindering widespread adoption. Additionally, limitations in grid infrastructure for accommodating renewable energy sources can pose challenges in scaling up electrolysis operations. Regulatory complexities and the need for supportive policies also impede rapid market expansion.

3. Which region is expected to lead the global Water Electrolysis market during the forecast period?

Ans. Europe is expected to lead the global Water Electrolysis market during the forecast period.

4. What is the projected market size & and growth rate of the Water Electrolysis Market?

Ans. The Water Electrolysis Market size was valued at USD 7.43 Billion in 2025 and the total Water Electrolysis revenue is expected to grow at a CAGR of 6.1% from 2026 to 2032, reaching nearly USD 11.25 Billion by 2032.

5. What segments are covered in the Water Electrolysis Market report?

Ans. The segments covered in the Water Electrolysis market report are Technology Type, end user, and Region.