Viscosity Index Improvers Market by Type, End-User, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

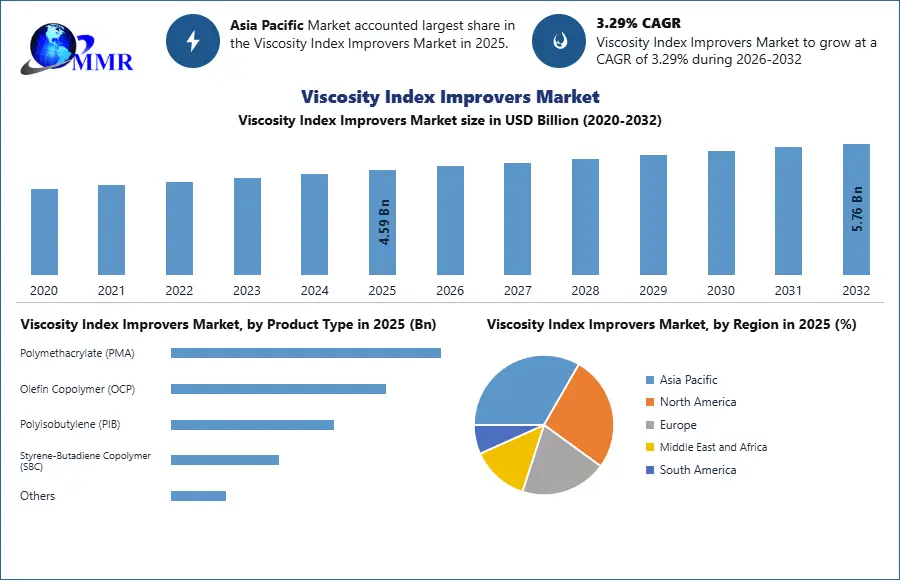

The Viscosity Index Improvers Market size was valued at USD 4.59 Billion in 2025 and the total Viscosity Index Improvers revenue is expected to grow at a CAGR of 3.29% from 2025 to 2032, reaching nearly USD 5.76 Billion.

Viscosity Index Improvers Market Overview:

A liquid's viscosity is defined as its inherent resistance to flow. Also, the viscosity index indicates a liquid's sensitivity to temperature changes. If a lubricant's viscosity changes dramatically at different temperatures, it is said to have a low viscosity index. Polymers used in a lubricant to make it resistant to changes in viscosity as the temperature rises are known as viscosity index improvers. A viscosity index improver is a complex polymer addition that thickens the lubricant and ensures a more stable and consistent viscosity at high temperatures. Also, high molecular polymers with a flexible primary molecular chain are viscosity index improvers.

The interactions between molecular chains are significant at low temperatures. The interactions decrease as the temperature rises, compensating for the loss of viscosity. This guarantees that the lubricant provides complete protection to the equipment at both high and low temperatures. Viscosity improvers also make it possible to make multigrade oils, eliminating the requirement for seasonal oil changes. When low-viscosity oils are thickened with viscosity index improvers, the oil thickens as the temperature rises. As a result, mineral oils' lubricating properties can be extended over a larger temperature range. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Viscosity Index Improvers Market Dynamics:

Despite a shift toward shared transportation, which increased demand for lubricants following the COVID-19 pandemic, vehicle unit sales will continue to rise:

The automotive industry is the largest consumer of lubricants. While driving, the temperature of the automobile's engines changes dramatically. Automobile lubricants serve four purposes: they control engine friction and wear, protect the engine from rust, cool the pistons, and protect the engine oil in the sump from combustion gases. When an engine oil / lubricant added to an automobile engine is exposed to extreme temperature swings, typically between 40 and 100 degrees Celsius, it begins to thin, which can cause the engine oil / lubricant to evaporate, causing damage or knocking out of the engine due to high friction between internal engine parts.

The viscosity of lubricating oil is the most important factor that influences its consumption. Viscosity index improvers (VIIs) are added to lubricants to prevent motor oil / lubricant from evaporating. These VIIs are lubricant additives that improve the quality of the base stock under a variety of operating conditions and help machines fulfil their high performance standards. As a result, the global VIIs market is likely to be driven by rising automotive sales around the globe, notably in the Asia Pacific region, which is raising demand for high-performance lubricant additives like VIIs.

Unorganized and fragmented markets are increasing competition:

Unorganized players who sell cheap and sub-standard products compete fiercely with major VII manufacturers. Local and grey market players are unorganized players in the market; local players offer products created in-house under their own brands, whilst grey market players import and sell goods through unlicensed dealers. With their reduced costs, competitiveness, and local supply network, these unorganized firms outperform the large players, which is tough for global players to do. Increased sales by both local and grey market businesses limit multinational players' opportunities to grow their market share. This limits global players' entry into local markets, restricting their investment in this market.

Increasing market opportunities for emerging economies:

During the forecast period, the BRICS countries (Brazil, Russia, India, China, and South Africa) are likely to account for a considerable market for VIIs market. According to World Bank estimates, the BRICS countries account for around 41% of global population, which is 31% higher than the G7 countries (Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States), and this population is likely to grow even more. The BRICS countries collectively account for about a fifth of global GDP. The global economy is expected to increase 5.50% in and 4.20% in , according to the International Monetary Fund (IMF).

Governments in these countries place a strong priority on industrial development in order to meet the demands of their huge populations. Foreign and domestic investments are likely to expand tremendously in the next five years as these countries' financial infrastructure improves. This is expected to enhance all involved sectors, driving related industries like VII forward.

Price fluctuations in crude oil affects VII manufacturers:

Because oil prices are so important in the lubricant additives industry, any structural changes in the oil market have an impact on this industry. The change in crude oil prices puts lubricating oil additives companies in a difficult position, affecting profitability. Crude oil is the raw material for lubricant oil additives, therefore fluctuating crude oil prices have had an impact on the lubricant oil additives value chain in recent years. Oil prices have been above US $100 per barrel in countries that consume a lot of energy since , and have recently plummeted to around US $50 per barrel in March .

As a result, lubricating oil additives makers are facing uncertainty due to shifting crude oil prices. The decision to buy crude oil becomes problematic due to shifting base oil prices, as manufacturers are unaware of the prices at which they should buy crude oil.

Surging adoption of Electric Vehicles (EVs) to eliminate carbon footprints:

Consumers have begun to change their demand from gasoline-powered automobiles to electric hybrid vehicles as a result of rising environmental concerns and technological improvements. Various e-vehicle manufacturing plants are being built in various nations. For example, according to the European Automobile Manufacturing Association, e-vehicle production in the EU increased to 11% in from 3% in , and according to the International Energy Agency, global electric car registration increased by 41% in , with China and Europe being the largest electric vehicle markets.

Nio, Volvo, and Xpeng Motors, among others, have established significant e-vehicle facilities in central and south-eastern China, according to the International Council for Clean Transportation report . As a result of the increased demand for and manufacturing of EVs, gasoline and diesel vehicles, which are the primary consumers of lubricant, may be banned, posing a challenge to the VIIs market growth.

The oil drainage period:

In the automotive sector, viscosity index improvers play a significant role as an intermediate in lubricants. However, the oil draining interval is longer, limiting the market growth of the viscosity index improver. The engine oil drain interval has been increased from 25,000 miles to 50,000 miles as a result of ongoing technological improvements. This increase in engine oil draining intervals is likely to reduce lubricant demand, which will, in turn, reduce demand for viscosity index improvers.

Viscosity Index Improvers Market Segment Analysis:

Based on Product Type:

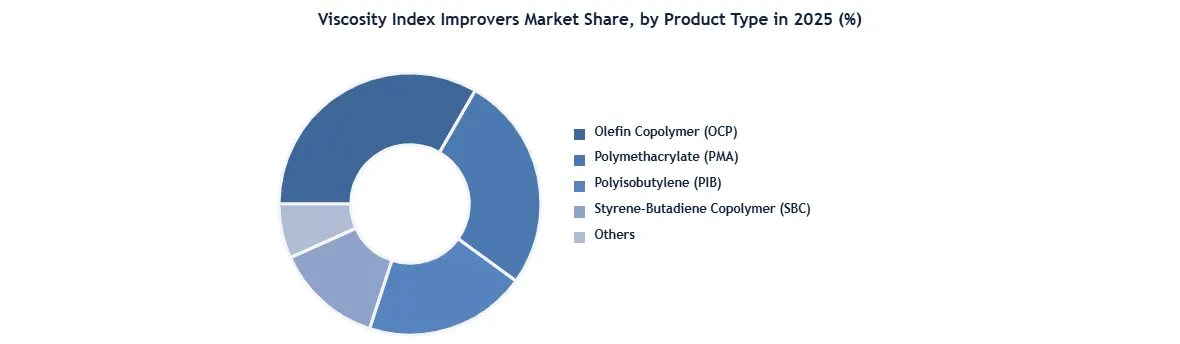

The Viscosity Index Improvers Market is segmented by product type into Polymethacrylate (PMA), Olefin Copolymer (OCP), Polyisobutylene (PIB), Styrene-Butadiene Copolymer (SBC), and others. Among these, Olefin Copolymer (OCP) dominates the market in 2025 due to its strong shear stability, cost efficiency, and broad compatibility with automotive engine oils and industrial lubricants. OCP is widely preferred by lubricant manufacturers because it provides excellent viscosity control under extreme temperatures, supporting demand from passenger vehicles and commercial fleets.

Polymethacrylate (PMA) holds a significant share as it offers superior low-temperature performance and oxidation stability, making it suitable for premium synthetic lubricants. Polyisobutylene (PIB) is growing steadily owing to its use in multifunctional additive formulations, especially in fuel-efficient oils. Styrene-Butadiene Copolymer (SBC) serves niche applications requiring enhanced thermal resistance. The others segment includes emerging polymer blends designed for advanced lubricants. Rising automotive production, demand for fuel-efficient engine oils, and stricter emission norms continue to drive product innovation across all viscosity index improver segments.

Viscosity Index Improvers Market Regional Insights:

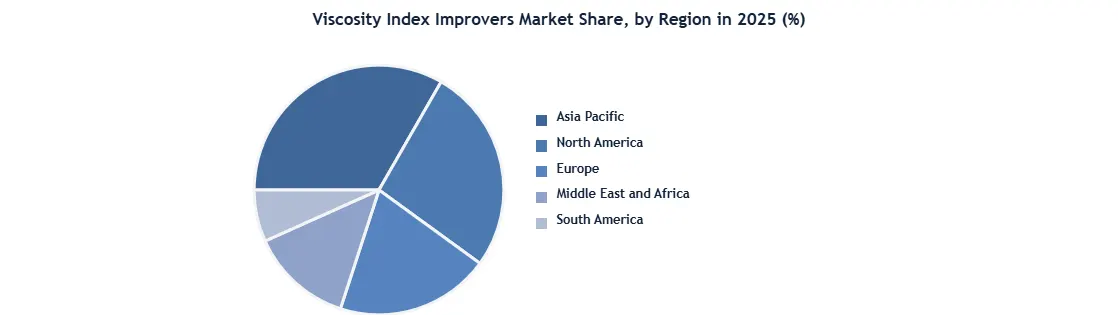

In terms of value, the Asia Pacific was the largest consumer of viscosity index improvers in 2025, and it is expected to grow at a CAGR of 3.61% throughout the forecast period. The Asia Pacific is an interesting market for lubricating industry due to rapid economic growth in emerging countries and rising disposable income. The region's high consumption of lubricating oil is mostly due to the great development of industrial production, which expanded commerce, and the increase in the number of automobiles. Also, increased demand for lubricating oil in the region is driven by growing investments in India's industrial sector. Also, government rules and policies promoting environmental sustainability are impacting the lubricating oil additives market, which is likely to raise demand for lubricating oil additives over the forecast period.

The European market is one of the most important. The important countries in the European market are Spain, Italy, and the United Kingdom, which collectively account for a large portion of the overall European market. The European lubricating oil market is extensively regulated, with REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) closely monitoring and providing guidelines to maintain a high level of environmental and human health protection from chemical dangers. The market is likely to perform moderately in the years ahead due to the introduction of rigorous environmental rules in the EU and increased demand for lubricants in the European market.

Viscosity Index Improvers Market Scope: Inquire before buying

| Viscosity Index Improvers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 4.59 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.29% | Market Size in 2032: | 5.76 USD Billion |

| Segments Covered: | by Product Type | Polymethacrylate (PMA) Olefin Copolymer (OCP) Polyisobutylene (PIB) Styrene-Butadiene Copolymer (SBC) Others |

|

| by Application | Automotive Lubricants Industrial Lubricants Hydraulic Fluids Marine and Aviation Lubricants Others |

||

| by End-User Industry | Automotive Industrial Machinery Aerospace Oil & Gas Others |

||

Viscosity Index Improvers Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Viscosity Index Improvers Market Key Players

- Exxon Mobil Corporation

- BASF SE

- Chevron Oronite Company LLC

- Evonik Industries AG

- The Lubrizol Corporation

- Sanyo Chemical Industries, Ltd.

- Shanghai High-Lube Additives

- Bariyan Oil & Lubricants Pvt. Ltd.

- BPT Chemicals Co., Ltd.

- Brad-Chem Ltd.

- Environ Specialty Chemicals

- Chetas Biochem

- Innov Oil Pte Ltd.

- Afton Chemical Corporation

- Croda International Plc

- The Elco Corporation

- BRB International BV

- Asian Oil Company

- Infineum International Limited

- Xingyun Chemical Co., Ltd.

- Shenyang Great Wall Lubricating Oil Manufacturing Co.,Ltd

- LANXESS AG

- Jinzhou Kangtai Lubricant Additives Co., Ltd.

- Shanghai Minglan Chemical Co., Ltd.

- Eni SpA

- PXL Chemicals

- TRiiSO

- Functional Products Inc.

- Kusa Chemicals Pvt. Ltd.

- Paras Lubricants Limited

Other Key Players

nd Others are the key players covered.