Hazardous Waste Management Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

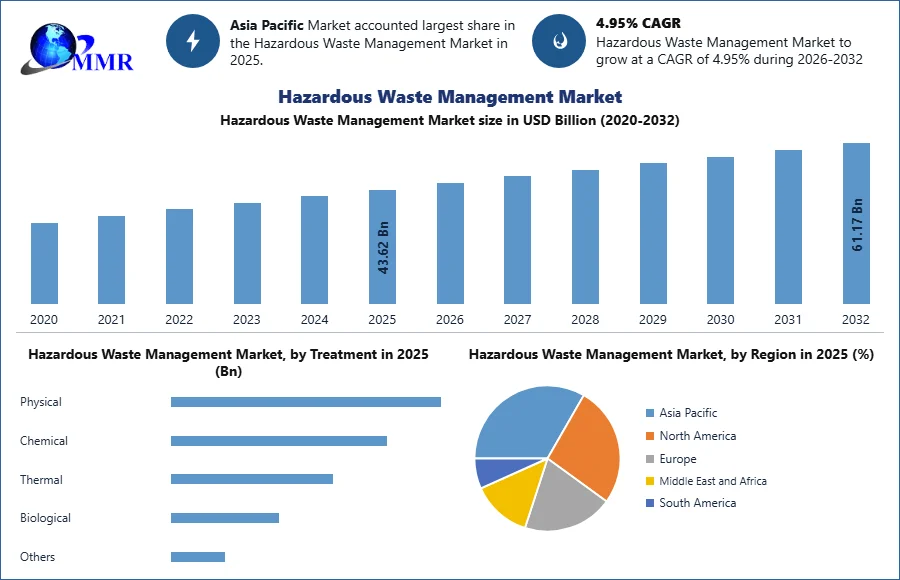

The Hazardous Waste Management Market size was valued at USD 43.62 Billion in 2025 and the total Hazardous Waste Management revenue is expected to grow at a CAGR of 4.95% from 2025 to 2032, reaching nearly USD 61.17 Billion.

Hazardous Waste Management Market Overview:

The rising industrialization, stricter environmental regulations, and increasing hazardous byproducts generated from manufacturing, chemicals, pharmaceuticals, mining, healthcare, and oil & gas industries. Globally, more than 400 million metric tons of hazardous waste are generated annually, with industrial chemicals, solvents, heavy metals, and toxic sludge accounting for a significant proportion of waste streams. Governments across the U.S., China, India, Germany, and Japan are strengthening waste disposal norms and investing in advanced treatment technologies such as incineration, plasma gasification, autoclaving, and secure landfilling. The healthcare sector alone generates nearly 5.3 million tons of hazardous medical waste every year due to growing hospital infrastructure and diagnostic laboratories. Increasing electronic waste volumes, which exceeded 62.26 million metric tons globally in 2025, are further supporting hazardous waste collection and recycling services.

To know about the Research Methodology :- Request Free Sample Report

Hazardous Waste Management Market Dynamics

Stringent Environmental Regulations and Industrial Compliance

Stringent environmental regulations remain a major growth driver for the hazardous waste management industry. Regulatory agencies such as the U.S. Environmental Protection Agency (EPA), China’s Ministry of Ecology and Environment, and India’s Central Pollution Control Board have imposed strict waste treatment and disposal guidelines on industries generating toxic substances. More than 65% of global chemical manufacturing facilities are now required to maintain hazardous waste documentation, traceability, and certified disposal practices. The European Union’s Waste Framework Directive and Basel Convention regulations have significantly increased cross-border monitoring of hazardous waste transportation. Industrial sectors including petrochemicals, pharmaceuticals, batteries, and semiconductors are investing heavily in compliant waste treatment infrastructure to avoid penalties and environmental liabilities. In India alone, over 7.5 million metric tons of hazardous waste are generated annually from industrial operations, increasing demand for treatment, storage, and disposal facilities (TSDFs).

Trend – Adoption of Advanced Waste-to-Energy and Recycling Technologies

Advanced waste-to-energy and recycling technologies are emerging as a significant trend in the hazardous waste management market. Industries are increasingly adopting thermal treatment, pyrolysis, plasma gasification, solvent recovery, and chemical recycling technologies to reduce landfill dependency and recover valuable materials. More than 35% of hazardous waste treatment facilities in developed economies now integrate energy recovery systems capable of generating electricity and industrial heat from toxic waste streams. Battery recycling facilities are witnessing strong investments due to rising electric vehicle production and lithium-ion battery disposal volumes. Europe processed over 1.3 million metric tons of hazardous battery waste in 2025 through advanced recycling technologies. AI-enabled robotic sorting systems and IoT-based waste monitoring solutions are also improving segregation efficiency and reducing human exposure to toxic materials. Pharmaceutical and semiconductor manufacturers are increasingly implementing closed-loop recycling systems for solvents and chemicals. The shift toward circular economy practices and carbon reduction targets is encouraging industries to convert hazardous waste into reusable industrial inputs and alternative fuels.

Restraint – High Treatment and Disposal Costs

High treatment, transportation, and disposal costs remain a key restraint for the hazardous waste management market, particularly in developing economies. Hazardous waste requires specialized containment, labeling, transportation vehicles, incineration units, and secure landfills, significantly increasing operational expenses for industries. Small and medium-sized enterprises often struggle to comply with waste handling regulations due to limited financial resources and inadequate access to certified disposal facilities. Developing countries face shortages of advanced treatment infrastructure, resulting in illegal dumping and improper waste disposal practices. Rising fuel prices and logistics costs also impact hazardous waste transportation expenses, especially for cross-border waste movement. These cost-related challenges continue to limit the adoption of advanced hazardous waste treatment technologies among smaller industrial operators.

Hazardous Waste Management Market Segment Analysis

By Physical State

Solid hazardous waste dominates the market due to the massive volume of industrial, mining, healthcare, and electronic waste generated globally. Solid hazardous waste includes contaminated soil, batteries, chemicals, paints, heavy metals, pesticides, and electronic scrap materials. The manufacturing and construction industries contribute significantly to solid waste generation, especially in China, the U.S., and India. Lithium-ion battery disposal from electric vehicles and consumer electronics is also increasing rapidly, driving demand for specialized recycling and treatment facilities. Governments are implementing stricter landfill restrictions and encouraging material recovery practices, particularly for metals, solvents, and electronic components. Advanced solid waste stabilization, encapsulation, and thermal treatment technologies are increasingly being adopted across industrial waste management facilities.

By Chemical Composition

Inorganic hazardous waste dominates the market due to large-scale generation from mining, metallurgy, chemical processing, power plants, and semiconductor manufacturing industries. This waste category includes heavy metals, acids, alkalis, cyanides, asbestos, mercury compounds, and toxic industrial residues. Mining operations globally generate millions of tons of inorganic tailings and sludge containing arsenic, cadmium, and lead contaminants. Coal-fired power plants continue to produce substantial volumes of fly ash and toxic residues requiring specialized disposal methods. Semiconductor and electronics manufacturing industries are also generating increasing quantities of inorganic chemical waste due to rising chip production and advanced electronics demand. Governments are implementing stricter regulations on heavy metal disposal and groundwater contamination prevention. Advanced chemical neutralization, stabilization, vitrification, and secure landfill technologies are increasingly deployed to manage inorganic hazardous waste safely and reduce environmental risks.

Hazardous Waste Management Market Regional Analysis

Asia Pacific dominated the hazardous waste management market in 2025 due to rapid industrialization, urbanization, and expanding manufacturing activities across China, India, Japan, South Korea, and Southeast Asia. China alone generates more than 90 million metric tons of industrial hazardous waste annually from chemicals, mining, electronics, and metal processing industries. India contributes over 7.5 million metric tons of hazardous industrial waste every year, driven by pharmaceutical manufacturing, petrochemical refining, and automotive production. Governments across the region are strengthening environmental enforcement and investing in treatment infrastructure to address rising pollution levels. Japan and South Korea are major adopters of advanced hazardous waste recycling technologies, particularly for electronic waste and lithium-ion batteries. More than 2,500 authorized hazardous waste treatment facilities operate across Asia Pacific, supporting collection, storage, incineration, and recycling operations. Rising foreign direct investments in industrial manufacturing, increasing healthcare waste generation, and rapid growth in e-waste volumes are further supporting market growth. Smart waste monitoring systems and AI-driven waste segregation technologies are also witnessing strong adoption across urban industrial hubs.

Recent Developments

On March 2025, Veolia Environnement S.A. strengthened its hazardous waste management capabilities by expanding its industrial waste recycling and solvent recovery operations in South Korea and Southeast Asia. The company upgraded multiple treatment facilities with advanced chemical separation and thermal processing technologies capable of handling more than 120,000 tons of hazardous industrial waste annually. Veolia focused heavily on waste-to-energy integration and circular economy initiatives to support petrochemical, semiconductor, and pharmaceutical manufacturers facing stricter environmental regulations. The company also introduced AI-enabled monitoring systems to improve hazardous waste traceability and reduce operational risks. Veolia’s expansion strategy targeted high-growth Asian industrial hubs where hazardous waste volumes are increasing rapidly due to electronics manufacturing and battery production.

On January 2025, Clean Harbors, Inc. expanded its hazardous waste incineration and disposal operations in Nebraska, United States, to address increasing industrial and healthcare waste volumes. The facility expansion increased thermal treatment capacity by nearly 15%, enabling the company to process additional chemical waste, pharmaceutical residues, and contaminated industrial materials generated from manufacturing and refinery sectors. Clean Harbors also invested in upgraded emissions control systems and digital waste tracking technologies to improve regulatory compliance and operational transparency. The company emphasized sustainable waste destruction and energy recovery processes that minimize landfill dependency while supporting industrial decarbonization goals.

Hazardous Waste Management Market: Inquire before buying

| Hazardous Waste Management Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 43.62 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.95% | Market Size in 2032: | 61.17 USD Billion |

| Segments Covered: | by Chemical Composition | Organic Inorganic |

|

| by Treatment | Physical Chemical Thermal Biological Others |

||

| by Disposal Method | Deep Well Injection Detonation Engineered Storage Land Burial Ocean Dumping Incineration Others |

||

| by End-Use Industry | Manufacturing Oil & Gas Healthcare & Pharmaceuticals Chemicals Mining Energy & Power Automotive Construction Electronics & Semiconductors Others |

||

Hazardous Waste Management Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (razil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Hazardous Waste Management Market report in strategic perspective

- Veolia Environnement S.A.

- Clean Harbors, Inc.

- Waste Management, Inc.

- Republic Services, Inc.

- SUEZ Group

- Stericycle, Inc.

- Covanta Holding Corporation

- Biffa plc

- Remondis SE & Co. KG

- US Ecology, Inc.

- Heritage Environmental Services LLC

- EnviroServ Waste Management (Pty) Ltd.

- Tradebe Environmental Services

- FCC Environment

- GFL Environmental Inc.

- Recology Inc.

- Daiseki Co., Ltd.

- Waste Connections, Inc.

- Daniels Health

- Hulsey Environmental Services, Inc.

- Rumpke Consolidated Companies, Inc.

- Averda International

- SharpSmart

- Bechtel Corporation

- Morgan Group

- EcoWise Waste Management Pvt. Ltd.

- Biomedical Waste Solutions, LLC

- Advanced Disposal Services

- Saahas Zero Waste

- Chloros Environmental Ltd.