Trauma Implants Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2030

Overview

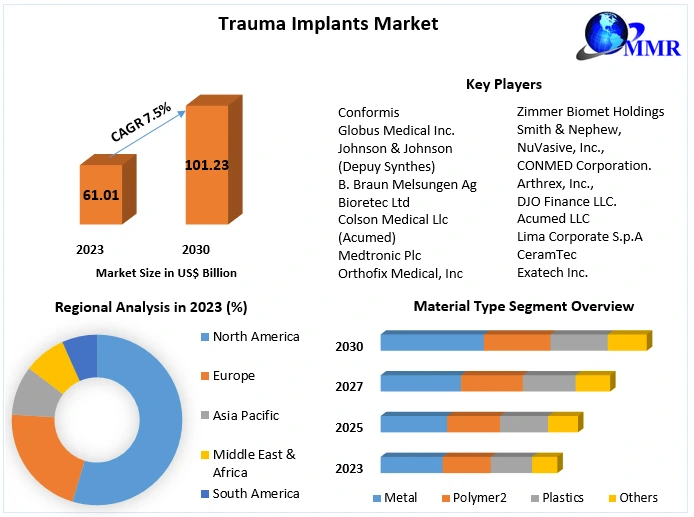

Trauma Implants Market size was valued at USD 61.01 Bn. in 2023 and the total revenue is expected to grow at a CAGR of 7.5% from 2024 to 2030, reaching nearly USD 101.23 Bn.

Trauma Implants Market Overview:

Trauma implants play an essential role in repairing internal fractures and replacing damaged joints. Trauma is a type of physical damage involving the transfer of kinetic energy. Orthopedic trauma includes bone and joint fractures, subluxation, and dislocation. A trauma implant is a medical device designed to repair or support a damaged joint or bone. The operation in orthopedic surgery that involves the implementation of implants to repair a damaged or lost bone is expected to drive the trauma implants market growth during the forecast period. Pins, rods, screws, and plates are just a handful of the medical implants that are commonly used to stabilize damaged bones while they recover.

The rising incidence of orthopedic disorders and injuries, as well as the rapidly growing aging population, are expected to be significant growth drivers for the trauma implants market. According to the NCBI, the majority of artificial joint patients were 65 or older, whereas fixation device recipients were younger than 45. Additionally, technical improvements such as robot-assisted surgical instruments implanted medical device adoption, and widespread use of orthopedic implants to treat musculoskeletal and orthopedic disorders and injuries contribute to market growth. Likewise, a rising number of joint replacements and sports injuries around the world would drive the trauma implant market growth during the forecast period.

In addition, the rapidly increasing number of sports injuries that are more prone to bone fractures is expected to play a significant role in driving the trauma implants market growth during the forecast period. Demand for minimally invasive devices during surgical treatment of bone fractures drives demand for trauma implants during the forecast period. In addition, technological innovation and an increase in new product releases by numerous major players are expected to boost the market during the forecast period.

However, the high cost of treatments requiring orthopedic implants for therapy, as well as stringent government regulations, may restrict the growth of the trauma implants market during the forecast period. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Trauma Implants Market Dynamics:

Rise in road traffic accidents results in high Orthopedic Fractures

Road traffic accidents have been established as one of the causes of orthopedic fractures, and the growth in the incidence of road traffic accidents around the world is expected to raise demand for trauma implants and drives trauma implants market size during the forecast period. According to a report published in the International Journal of Orthopedic Sciences 2020, around 30% of patients in India experienced a tibia bone fracture as a result of a traffic accident.

In many countries, increasing car use and inefficient traffic management are expected to raise the number of road traffic accidents resulting in orthopedic fractures. The increasing growth in the incidence of orthopedic fractures globally is expected to increase revenues for the trauma implants industry during the forecast period.

Increase in an aging population

The global aging population has increased dramatically, and an increase in the frequency of bone disorders combined with poor bone mass density is expected to drive demand for trauma implants throughout the forecast period. According to the World Health Organization (WHO), the percentage of the world's population over 60 years old would nearly double between 2020 and 2050, rising from 12% to 22%. Today, India has one of the world's youngest populations.

However, the share of people over the age of 60 is expected to rise to 19% by 2050. Rapid aging increased life expectancy, and lifestyle changes are expected to be major causes of the growth of osteoarthritis in India. As a result, increasing demand for Trauma Implants and driving the Trauma Implants market growth during the forecast period.

Rising sports injuries and technological advancements by competitors

Rising sports injuries are expected to become a new source of bone fractures, increasing the growth rate of trauma implants at a large pace throughout the forecast period. According to the American Academy of Pediatrics (AAP), around 30 million children and teenagers participate in organized sports in the United States, and over 3.5 million teens and children suffer from sports injuries each year.

Growing awareness of technology advancements and the demand for minimally invasive implant technologies are now the two important factors influencing the growth of the trauma implants market. Additionally, osteoporosis incidence would drive market growth. The International Osteoporosis Foundation (IOF) estimates that around 30.5 million people over the age of 50 will have osteoporosis by 2025.

Many big and mid-sized firms are launching trauma implants, and the participants' collaboration and partnership activities are expected to increase trauma implant sales during the forecast period. In the United States, for example, OSSIO developed the OSSIOfiber Bone Pin Family in 2019 for the preservation of alignment and fixation of bone fractures, osteotomies, arthrodesis, and bone transplants. Increased orthopedic operations and the entry of new companies into the market supplying a wide range of trauma implants are expected to drive the growth of the trauma implants market during the forecast period.

Rising Medical tourism in emerging economies

The healthcare industry has undergone a huge transformation in the past decade. Several significant multispecialty hospital networks have emerged, offering world-class treatment choices and facilities. These hospitals have prospered as a wealthier middle class has demanded higher quality healthcare. A more recent trend has been the emergence of single-specialty chains that provide concentrated, specialized treatment in areas such as cancer, nephrology, and obstetrics. These facilities have also aided in the growth of medical tourism in emerging economies.

Various Asian countries provide high-quality, cost-effective healthcare treatment in global, certified facilities staffed by highly experienced doctors, and are well positioned to increase their part of the medical tourism industry. In 2019, an estimated 184,298 international visitors visited India for medical treatment. To promote medical tourism, the Ministry of Tourism has established a National Medical and Wellness Tourism Board. This Board is designed to serve as a facilitator and to assist the medical/wellness sector in marketing Asian countries as medical and wellness destinations.

If properly advertised, there is tremendous potential to increase revenues in Asian countries for orthopedic implant treatments in the medical tourism segment, as well as the size of the trauma implants market.

High cost of implant surgeries

Knee replacement surgery costs between USD 4500 to USD 8000 for one knee, with computer-aided treatments costing an additional 5-10%. Despite a CAGR of 16% in insurance coverage, less than 300 million individuals are now covered by health insurance through one of several sources: government-provided coverage, corporate group coverage, and private retail plans. The segment's potential as a significant out-of-pocket market is restricted by affordability limits for expensive orthopedic implant operations.

The reduced frequency of hip replacements throughout the world is frequently linked to the affordability issue and the resulting proclivity to postpone or avoid the treatment. As a result, the high cost of surgeries is expected to restrain the trauma implants market growth.

Stringent governmental regulations

The concerns related to prosthetic implants, such as adverse effects linked with metal implants, post-surgery infections, implant dislocations, hypersensitivity, wear debris, and toxicity problems, are causing patient dissatisfaction, which is causing an increase in product recalls. As a result, regulatory bodies are enforcing stringent product approval procedures to guarantee patient safety, resulting in product clearance schedules being pushed back. As a result, the existing stringent regulatory framework is expected to be a significant constraint to the trauma implants market growth during the forecast period.

Trauma Implants Market Segment Analysis:

Based on Material Type, the metal implants segment held the largest market share of 45% and dominated the global trauma implants market in 2023. The segment is expected to grow at a CAGR of 7.4% throughout the forecast period and maintain its dominance by 2030. The metallic biomaterials are cost-effective and enhance better bone healing in comparison to the other types of materials used. Metals' strong tensile and fatigue strength, as compared to ceramics and polymers, make them the material of choice for mechanically loaded implants.

Metallic implants are widely utilized around the world because of their high operational efficacy and low cost, fueling the trauma implants market revenue growth. They are primarily used in the manufacturing of orthopedic implants such as plates, screws, and VCF devices.

Injured people and those suffering from joint illnesses such as osteoarthritis, rheumatoid arthritis, and post-traumatic arthritis may require surgery that includes implants such as total hip and knee replacements. Temporary fracture fixation devices and components such as plates, screws, pins, wires, and nails are also included in orthopedic implants. Because orthopedic implants must function in vivo under a variety of working conditions, a thorough understanding of the fundamental requirements of orthopedic materials and the resulting biological response is critical to the design and optimization of implants under physiological conditions in the human body.

In orthopedic implants, metallic alloys are often utilized. The materials have various physical, chemical, and biological characteristics that are applied to individual uses. Metallic alloys, for example, are commonly utilized in load-bearing joint prostheses and bone fracture devices due to their superior mechanical qualities. The increasing need for better orthopedic materials has driven major advancements in this sector, resulting in the design and manufacture of orthopedic implants with improved performance and unique features.

Metallic materials have long predominated in orthopedic surgery, with a significant role in the majority of orthopedic devices, including temporary devices (e.g., bone plates, pins, and screws) and permanent implants (e.g. total joint replacements). Concurrently, metals are found use in dental and orthodontic procedures, such as tooth fillings and roots. Recently, there has been an increase in research efforts in metallic biomaterials for the application of nonconventional reconstructive surgery of hard tissues/organs, such as the use of NiTi shape memory alloys as vascular stents and the development of new magnesium-based alloys for bone tissue engineering and regeneration. As a result, rise in the number of R&D activities in metallic implants, driving the segment growth during the forecast period.

Metallic materials have long predominated in orthopedic surgery, with a significant role in the majority of orthopedic devices, including temporary devices (e.g., bone plates, pins, and screws) and permanent implants (e.g. total joint replacements). Concurrently, metals are found use in dental and orthodontic procedures, such as tooth fillings and roots. Recently, there has been an increase in research efforts in metallic biomaterials for the application of nonconventional reconstructive surgery of hard tissues/organs, such as the use of NiTi shape memory alloys as vascular stents and the development of new magnesium-based alloys for bone tissue engineering and regeneration. As a result, rise in the number of R&D activities in metallic implants, driving the segment growth during the forecast period.

Stainless steel is a very popular metal that was successfully used as an implant for biomedical due to its excellent corrosion resistance. Meanwhile, titanium alloys have gained popularity due to their unique properties such as lightweight, high strength, and durability. Cobalt chromium molybdenum (CoCrMo) alloys, on the other hand, outperform stainless steel and titanium alloys in terms of wear resistance.

Metallic materials are commonly utilized in medical equipment for cardiovascular, orthopedic, dental, prosthetic, craniofacial, and otorhonology applications. Because of their capacity to replace the function of hard tissues, they are excellent for bone fixation in orthopedics such as plates, screws, pins, and artificial joints. As a result, the rising use of metallic implants is increasing segment revenue and driving the trauma implants market growth during the forecast period.

Trauma Implants Market Regional Insights:

The North American region dominated the global trauma implants market in terms of value and volume in 2023. The region is further expected to maintain its dominance at the end of the forecast period. The growing geriatric population, growing healthcare investment, rising number of R&D activities, rising healthcare industry, and rising awareness among the people about advanced treatment for healthcare are expected to be the major growth drivers for the North American trauma implants market growth.

In addition, the growing technological advancements in orthopedics, rise in obesity, and growing adoption of inactive lifestyles, as also investing in research and development in minimal and cost-effective orthopedic implants are expected to increase global trauma implants market revenue in North America during the forecast period.

The rising prevalence of orthopedic disorders in the United States, such as osteoporosis and other related bone disorders, as well as an aging population with a higher risk of bone fractures, are expected to increase the demand for trauma implants. According to a 2023 Lancet article, the incidence of new fractures was reported to be 178 million instances globally, with a prevalence of 455 million fractures.

The rising incidence of fractures is expected to increase demand for orthopedic operations and increase implant usage. The growing need for orthopedic surgeries, along with an increase in the number of implantations, is expected to drive the growth of the trauma implants market during the forecast period.

The market's focus on inorganic growth strategies, such as collaborations and partnerships, to introduce advanced implants to meet the increased need for patient-centric customization is a major driver driving the market's growth in North America. LimaCorporate S.p.A., for example, announced cooperation with Ortho Carolina Center in New York City, U.S., in March 2022, with successful implantations of ProMade, a patient-specific 3D printed implant.

The market's focus on inorganic growth strategies, such as collaborations and partnerships, to introduce advanced implants to meet the increased need for patient-centric customization is a major driver driving the market's growth in North America. LimaCorporate S.p.A., for example, announced cooperation with Ortho Carolina Center in New York City, U.S., in March 2022, with successful implantations of ProMade, a patient-specific 3D printed implant.

The research highlights the advantages of onsite implant creation paired with surgeon knowledge, such as lowering surgery length and patient-specific implant personalization. Additionally, the strategic presence of significant market participants in the region, including Zimmer Biomet and Stryker, as well as the increasing usage of orthopedic implants, are expected to drive the trauma implants market growth during the forecast period.

Asia-Pacific region is expected to grow at a CAGR of 7.2% during the forecast period, offerings lucrative potentials for the key players operating in the trauma implants market. Additionally, the growing aging population increased awareness of orthopedic implants, increased demand for improved implants, growth of healthcare infrastructure, and increased need for minimally invasive treatments all contribute to the region's growth.

In addition, Advances in bone scan diagnostic tools for determining bone density among clinical laboratories, improved reimbursements by private and governmental institutions, and the improvement of healthcare infrastructure are all contributing to an increase in the number of patients receiving orthopedic treatments. This, together with favorable government legislation to encourage orthopedic operations, is expected to drive the trauma implant market growth in Asian countries.

Trauma Implants Market Scope: Inquiry Before Buying

| Trauma Implants Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 61.01 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 7.5 % | Market Size in 2030: | US $ 101.23 Bn. |

| Segments Covered: | by Implant Type | Cranial/Facial Implant Spinal Implant Hip Implants Knee Implants Extremities Implants |

|

| by Material Type | Metal Polymer Plastics Others |

||

| by Technology | Powder Bed Fusion Vat Photopolymerization Material Extrusion Others |

||

| by End-User | Hospitals Ambulatory Surgical Centers Orthopedic Clinics |

||

Trauma Implants Market, by Region

North America (United States, Canada and Mexico) Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Trauma Implants Market, Key Players are

1. Conformis

2. Globus Medical Inc.

3. Johnson & Johnson (Depuy Synthes)

4. B. Braun Melsungen Ag

5. Bioretec Ltd

6. Colson Medical Llc (Acumed)

7. Medtronic Plc

8. Orthofix Medical, Inc

9. Siora Surgicals Pvt. Ltd.

10. Smith & Nephew plc

11. Stryker Corporations

12. Zimmer Biomet Holdings

13. Smith & Nephew,

14. NuVasive, Inc.,

15. CONMED Corporation.

16. Arthrex, Inc.,

17. DJO Finance LLC.

18. Acumed LLC

19. Lima Corporate S.p.A

20. CeramTec

21. Exatech Inc.

FAQs:

1. What are the growth drivers for the Trauma Implants market?

Ans. The rising incidence of orthopedic disorders and injuries, the rapidly growing aging population, and the rapidly increasing number of sports injuries are expected to be the major driver for the Trauma Implants market.

2. What is the major restraint for the Trauma Implants market growth?

Ans. The High cost of implant surgeries and Stringent Regulations on Trauma Implants surgeries are expected to be the major restraining factor for the Trauma Implants market growth.

3. Which region is expected to lead the global Trauma Implants market during the forecast period?

Ans. The North American market is expected to lead the global Trauma Implants market during the forecast period due to the growing geriatric population, growing healthcare investment, rising number of R&D activities, rising healthcare industry, and rising awareness among the people about advanced treatment for healthcare.

4. What is the projected market size & growth rate of the Trauma Implants Market?

Ans. The Trauma Implants Market size was valued at USD 61.01 Bn. in 2023 and the total Trauma Implants revenue is expected to grow at a CAGR of 7.5% from 2024 to 2030, reaching nearly USD 101.23 Bn.

5. What segments are covered in the Trauma Implants Market report?

Ans. The segments covered in the Trauma Implants market report are Implant Type, Material Type, Technology, End-User, and Region.