Chronic Kidney Disease Drugs Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

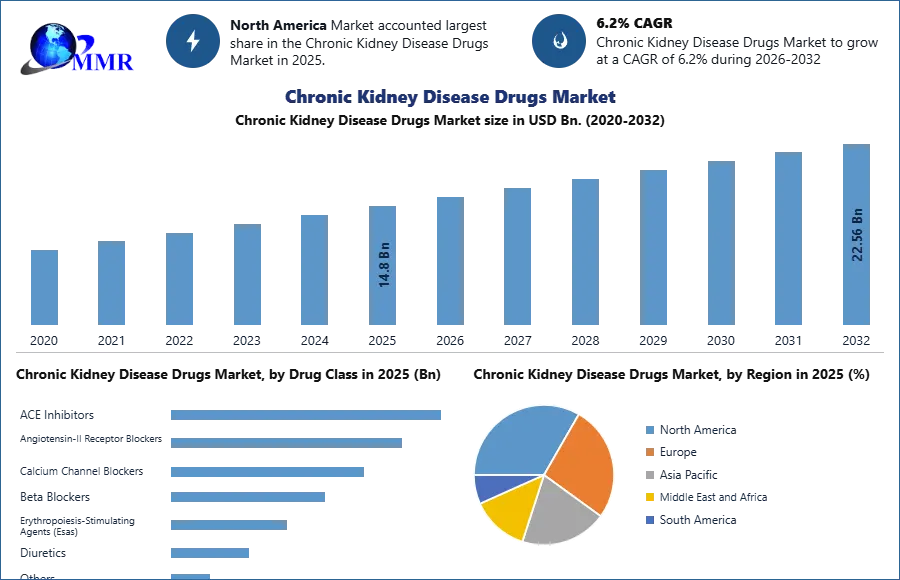

Global Chronic Kidney Disease Drugs Market size was valued at USD 14.8 Bn. in 2025, and the total Chronic Kidney Disease Drugs Market revenue is expected to grow by 6.2% from 2026 to 2032, reaching nearly USD 22.56 Bn.

Chronic Kidney Disease Drugs Market Overview:

The CKD drugs market covers therapies addressing complications such as anemia, hyperphosphatemia, secondary hyperparathyroidism, hypertension, and metabolic acidosis. Key drug classes include erythropoiesis-stimulating agents (ESAs), iron supplements, phosphate binders, calcimimetics, diuretics, and RAAS inhibitors, all of which help slow CKD progression and improve patient outcomes.

To know about the Research Methodology :- Request Free Sample Report

CKD Drugs Market growth has been driven by rising CKD prevalence linked to diabetes, hypertension, and aging populations, alongside expanding pipelines of branded and generic drugs. North America led the CKD drugs market due to advanced healthcare systems, reimbursement policies, and strong pharma presence, followed by Europe with high adoption of innovative therapies. Asia-Pacific is the fastest-growing region, fuelled by large patient pools, government healthcare initiatives, and growing awareness.

Major players include AstraZeneca, Amgen, Bayer, GSK, Pfizer, Johnson & Johnson, Novartis, and Akebia Therapeutics. Hospitals and specialty clinics dominate end-use, while retail and online pharmacies are expanding with rising outpatient demand. Overall, the market presents strong opportunities for innovation, access, and patient-centered care.

Chronic Kidney Disease Drugs Market Dynamics:

Rising population of Kidney Failures across the globe to Drive Chronic Kidney Disease Drugs Market

Kidney failure is a global public health issue with rising incidence and prevalence, high expenditures, and poor results. There is also a much greater frequency of chronic kidney disease (CKD) in its early stages, with negative effects such as renal function loss, cardiovascular disease (CVD), and premature mortality. Strategies for improving outcomes necessitate a global effort focused on the early stages of CKD.

One of the main factors in the increased prevalence of kidney failure is CKD. If the kidneys are harmed by an inability to control risk factors, recurring kidney infections, or medications or chemicals that are toxic to the kidneys, CKD is more likely to progress to renal failure, especially in older persons. Lower-income and related issues such as food insecurity and a lack of access to excellent health care are also linked to worsening CKD. However, not all people with CKD progress to renal failure. Treatment may decrease the loss of kidney function and delay renal failure if CKD is discovered early. Even with medication, kidney failure might occur in some situations.

According to the National Kidney Foundation (NKD), CKD affects around 15% of the global population, with millions of people dying each year. According to the NKD, emerging nations such as China and India have a large aging population. The number of patients receiving treatment with a kidney transplant or dialysis continues to rise at a pace of 7-9% every year. Women are expected to have a higher prevalence of chronic kidney disease than males (15% versus 12%). Other factors driving market growth include a rising number of patients suffering from hypertension and diabetes.

CKD affects over one-third of the diabetic population and is the leading cause of end-stage kidney failure. Hypertension is mostly caused by high blood pressure, which raises the risk of ESRD considerably. According to the WHO statistics in 2019, around 1.13 million people all across the globe have hypertension. Diabetes and hypertension were responsible for about 75% of kidney failure. Diabetes is the leading cause of severe kidney disease, followed by hypertension, which affects an estimated 1 million people across the globe. As a result, the growing number of individuals suffering from hypertension and diabetes is driving the market growth.

Medication dosing errors to restrain Chronic Kidney Disease Drugs Market Growth

Medication dosing errors are one of the most common drug-related issues in patients with chronic kidney disease (CKD). Many medications, drugs, and their metabolites are eliminated through the kidney. To avoid toxicity, adequate renal function is essential. Pharmacokinetic and pharmacodynamics characteristics are often altered in patients with renal impairment. Renal failure reduces the clearance of medicines removed predominantly by renal filtration.

As a result, when these medications are provided to individuals with compromised renal function, particular care should be undertaken. Despite the necessity of dose modifications in CKD patients, they are often overlooked. Physicians and pharmacists can collaborate to ensure safe medication prescriptions. This process can be difficult and requires a step-by-step strategy to assure efficacy, reduce future damage, and avoid medication nephrotoxicity.

Chronic Kidney Disease Drugs Market Segment Analysis:

Based on Drug Class, the Calcium channel blockers segment dominated the market in terms of value and volume in 2025 and is expected to maintain its dominance at the end of the forecast period. Calcium channel blockers (CCBs) are a class of antihypertensive drugs with a wide range of pharmacokinetics and therapeutic effects. Calcium channel blockers relieve the symptoms in a wide range of disorders, including coronary artery disease and high blood pressure, etc., and hence, this is driving the segment growth. The Calcium channel blockers have been widely used in clinical practice because of their antihypertensive capacity. The prevention of renal damage is a critical goal of antihypertensive treatment. This is especially true given the general population's high prevalence of chronic kidney disease (CKD). Recent research has linked CKD to the absence of proper blood pressure regulation, as well as the clustering of additional cardiovascular risk factors found in metabolic syndrome.

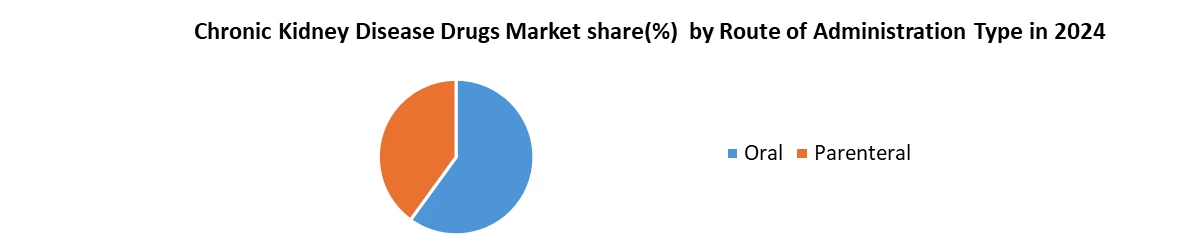

Based on route of administration, oral segment is estimated to contribute the highest market share in 2025, owing to convenience and ease of use advantages over parenteral drugs. High efficacy demonstrated by oral medications over long term has established them as first line treatment choice for chronic kidney diseases. Being non-invasive in nature, oral drugs are generally preferred by patients and clinicians alike for chronic therapy adherence. Self-administration of pills also saves resources by reducing hospital visits for injections. This has led to extensive research and development of novel drug delivery systems like timed and controlled release formulations, thus, enhancing oral bioavailability and stability of drugs. Moreover, ability to take medications conveniently without medical supervision has powered compliant oral administration across care settings for chronic kidney disease patients.

Chronic Kidney Disease Drugs Market Regional Insights:

North America held the largest market share and dominated the market in 2025. It is expected to maintain its dominance at the end of the forecast period. The improved healthcare infrastructure and increased government efforts, which offer attractive reimbursement policies in the country, are the primary drivers driving the market's growth in the United States. According to the American Cancer Society, around 73,750 new occurrences of kidney cancer in the United States in 2020, with roughly 14,830 fatalities from this illness.

According to the source, kidney cancer is one of the top 10 cancers in both men and women. In men, the lifetime chance of having kidney cancer is around 1 in 46 (2.02%). For women, the lifetime risk is roughly 1 in 82 (1.02%). This suggests that the market for kidney disease diagnostics and therapies has significant potential. The market in the United States is expected to grow during the forecast period due to the significant growth in the incidence and prevalence of renal illnesses.

Competition Landscape for the Chronic Kidney Disease (CKD) Drugs Market:

CKD Drugs Market competition landscape offers a strategy-first view of key players’ positioning, innovation, and value chain coverage. Leading companies—AstraZeneca (SGLT2), Bayer (finerenone), Boehringer Ingelheim/Eli Lilly (SGLT2), Amgen (CKD complications), and CSL Vifor (renal franchise)—maintain extensive global, guideline-aligned portfolios. Followers like Otsuka, GSK, Akebia, Takeda, Sanofi, and Pfizer expand via limited indications and lifecycle management, while upstarts Ardelyx, Calliditas, Travere, Vera, Chinook/Novartis, and Ionis focus on niche or first-in-class therapies. Companies are benchmarked on financials, technology delivery (HIF-PHIs, biologics, precision nephrology, IgAN/ADPKD), regulatory momentum, and market coverage. M&A, partnerships, and R&D (2019–2024) are reshaping pipelines, especially in CKD disease modification, inflammatory modulation, and dialysis-adjacent care, providing actionable insights for payers, investors, and manufacturers.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2025 | Novo Nordisk A/S | The US FDA approved Ozempic (semaglutide) as the first GLP-1 receptor agonist to reduce kidney disease progression and cardiovascular death in adults with type 2 diabetes and CKD. | This label expansion secures a first-mover advantage in the non-dialysis CKD market for diabetic patients, competing directly with established SGLT2 inhibitors. |

| 12 May 2025 | ProKidney | The company prioritized its PROACT 1 Phase III trial for rilparencel, a cell therapy, to accelerate regulatory submission for advanced-stage CKD. | Streamlining clinical efforts shortens the time to market for regenerative therapies that offer alternatives to standard dialysis and pharmaceutical management. |

| 10 July 2025 | AstraZeneca | The FDA endorsed eGFR slope as a surrogate endpoint for the accelerated approval of the company's rilparencel pipeline candidate in advanced CKD. | This regulatory validation lowers the barrier for approval of novel CKD treatments, potentially increasing the frequency of breakthrough therapy launches. |

| 15 November 2025 | Bayer AG | Results from the FINE-ONE multinational clinical trial confirmed that finerenone significantly reduced the urine albumin-to-creatinine ratio (UACR) in CKD patients. | The clinical success strengthens the competitive position of mineralocorticoid receptor antagonists (MRAs) as a standard of care for slowing kidney failure. |

| 03 March 2026 | Mineralys Therapeutics | The company published positive updates on Lorundrostat, an aldosterone synthase inhibitor, aimed at managing treatment-resistant hypertension in CKD populations. | The successful trial data expands the addressable market for specialized antihypertensives that target the physiological drivers of CKD progression. |

Key trends are shaping the Chronic Kidney Disease (CKD) Drugs Market:

1. Shift Toward Novel and Targeted Therapies – Companies are expanding beyond traditional CKD treatments by focusing on innovative drug classes, such as oral anemia therapies (e.g., Merck’s daprodustat/Duvroq) and monoclonal antibodies (e.g., Pfizer’s Pacibekitug targeting IL-6). This highlights a clear trend toward precision medicine and inflammation-modulating therapies in CKD drug development.

2. Expansion of Pipeline into Rare and Genetic Kidney Disorders – Several leading pharmaceutical players, including AbbVie and Johnson & Johnson, are investing in investigational therapies for autosomal dominant polycystic kidney disease (ADPKD), a genetic form of CKD. This reflects a growing industry trend to diversify CKD treatment portfolios by targeting niche yet unmet patient needs.

3. Focus on Improving Quality of Life for Dialysis Patients – Amgen’s advancement of AMG 416 (etelcalcetide), an intravenous calcimimetic for secondary hyperparathyroidism in hemodialysis patients, underscores the trend of developing supportive therapies aimed at reducing complications and improving outcomes for dialysis-dependent CKD patients.

Chronic Kidney Disease Drugs Market Scope: Inquire before buying

| Global Chronic Kidney Disease Drugs Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 13.94 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 6.2% | Market Size in 2032: | USD 22.56 Bn. |

| Segments Covered: | by Drug Class | ACE Inhibitors Angiotensin-II Receptor Blockers Calcium Channel Blockers Beta Blockers Erythropoiesis-Stimulating Agents (Esas) Diuretics Others |

|

| by Route of Administration | Oral Parenteral |

||

| by Indication | Diabetic Nephropathy Glomerulonephritis Hypertensive Nephropathy Polycystic Kidney Disease Other Indications |

||

| by End-User | Hospitals Specialty Clinics |

||

Chronic Kidney Disease Drugs Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Chronic Kidney Disease Drugs Market Report in Strategic Perspective:

- Amgen Inc.

- AstraZeneca plc

- Bayer AG

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd.

- Fresenius Medical Care AG & Co. KGaA

- Siemens Healthineers

- AbbVie Inc.

- Pfizer Inc.

- Sanofi S.A.

- GlaxoSmithKline plc

- Johnson & Johnson

- Teva Pharmaceutical Industries Ltd.

- Sanofi S.A.

- Eli Lilly and Company

- Novartis AG

- Takeda Pharmaceutical Co. Ltd.

- Akebia Therapeutics Inc.

- ProKidney

- Zydus Lifesciences Ltd.

- Sun Pharmaceutical Industries Ltd.

- Kissei Pharmaceutical Co., Ltd.

- Novo Nordisk A/S

- Rockwell Medical Inc.

- Mitsubishi Tanabe Pharma Corporation