Suture Anchors Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

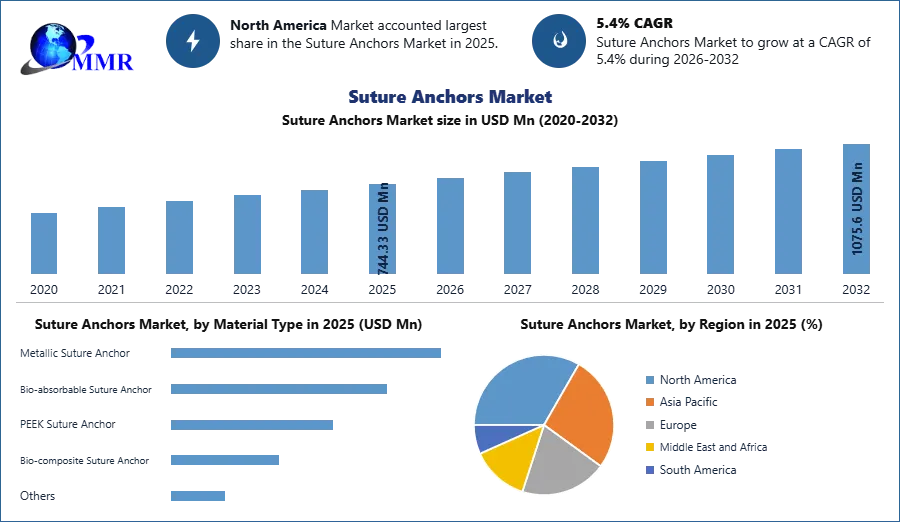

The Suture Anchors Market size was valued at USD 744.33 Million in 2025 and the total Suture Anchors revenue is expected to grow at a CAGR of 5.4% from 2025 to 2032, reaching nearly USD 1075.61 Million.

Suture Anchors Market Overview

Suture anchors are widely used for anchoring soft tissue to bone (e.g., tendons, ligaments, and meniscus) and have become vital instruments in sports medicine and arthroscopic surgery. Suture anchors are typically made of biocompatible materials, such as metals or polymers, and come in various designs and sizes to accommodate different surgical applications. Suture anchors play a vital role in orthopedic and sports medicine procedures, providing stability and support for soft tissue repair. Ongoing advancements in suture anchor technology, including personalized solutions and improved biomechanical properties, continue to drive innovation in the field, enhancing surgical outcomes and patient satisfaction.

The increasing prevalence of musculoskeletal conditions, rising demand for minimally invasive surgeries, advancements in suture anchor technology, and the growing incidence of sports-related activities are expected to be the major factors driving the suture anchor market growth. However, the risk of complications associated with suture anchors, regulatory considerations, and pricing pressures are expected to be the major restraining factors for market growth. According to the MMR analysis, the Asia Pacific region is expected to witness significant growth during the forecast period due to the increasing focus on healthcare infrastructure development, rising healthcare expenditure, and growing awareness of advanced treatment options.

The global suture anchors market is highly competitive, with multiple companies that are involved in the production and distribution of suture anchors. A few major companies dominate the suture anchors industry in terms of market share. Smith & Nephew plc, Zimmer Biomet Holdings, ConMed Corporation, Arthrex, Inc., Johnson & Johnson (DePuy Synthes, Inc.), Medtronic plc, Stryker Corporation, Parcus Medical, LLC., Wright Medical, Orthomed, Teknimed, Enovis, and others are among the market leaders. Key players in the suture anchors market often focus on research and development activities to enhance the performance, durability, and safety of their products. They also strive to expand their market presence through strategic partnerships, acquisitions, and product launches. For instance,

1. With the release of the Grappler Suture Anchor System in May , Paragon 28, Inc. declared an extension of its soft-tissue line. The Grappler Suture Anchor System offers surgeons an alternate fixation option for intraoperative tissue reattachment and fixation in the foot and ankle by limiting implant migration and loss of tension.

2. The US Food and Drug Administration approved Ossio's OssioFiber suture anchors for bone fixation in March . To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Suture Anchors Market Dynamics:

Increasing prevalence of musculoskeletal conditions

The increasing prevalence of musculoskeletal conditions is expected to be the primary factor driving the suture anchors market growth. According to MMR research, about 1.71 billion individuals globally suffer from musculoskeletal disorders. Low back pain is the single largest cause of disability in 160 countries, making musculoskeletal diseases the leading contributor to disability globally. In terms of population, high-income nations are the most impacted (441 million), followed by countries in the WHO Western Pacific Region (427 million) and the South-East Asia Region (369 million). Musculoskeletal diseases are also the leading cause of years lived with disability (YLDs) globally, accounting for roughly 149 million YLDs, or 17% of all YLDs. Low back pain is the leading cause of musculoskeletal disorders (570 million prevalent cases around the world, accounting for 7.4% of global YLDs). Other contributors to the overall burden of musculoskeletal conditions include fractures, which affect 440 million people worldwide (26 million YLDs), osteoarthritis (528 million people; 19 million YLDs), neck pain (222 million people; 22 million YLDs), amputations (180 million people; 5.5 million YLDs), rheumatoid arthritis (18 million people; 2.4 million YLDs), gout (54 million people; 1.7 million. Thus, increasing cases of musculoskeletal conditions are expected to increase the demand for suture anchors for surgeries driving the suture anchors market growth.

Low back pain is the leading cause of musculoskeletal disorders (570 million prevalent cases around the world, accounting for 7.4% of global YLDs). Other contributors to the overall burden of musculoskeletal conditions include fractures, which affect 440 million people worldwide (26 million YLDs), osteoarthritis (528 million people; 19 million YLDs), neck pain (222 million people; 22 million YLDs), amputations (180 million people; 5.5 million YLDs), rheumatoid arthritis (18 million people; 2.4 million YLDs), gout (54 million people; 1.7 million. Thus, increasing cases of musculoskeletal conditions are expected to increase the demand for suture anchors for surgeries driving the suture anchors market growth.

High risk of complications

Suture anchors are generally considered safe and effective, however, like other medical interventions, there are potential risks and complications associated with suture anchors use. The use of suture anchors in surgical procedures carries potential risks and complications. There is a high risk of infection associated with suture anchors in surgical procedures. Infection can occur at the site of the anchor insertion or in the surrounding tissues. Suture anchors experience failure or loosening, leading to inadequate tissue fixation or instability. In addition, improper placement or excessive tension on the sutures causes tissue damage, including tearing or fraying of the repaired structures. Thus, these high risks of complications associated with suture anchors are expected to restrain the suture anchors market growth during the forecast period.

Suture Anchors Market Segment Analysis:

By tying type, the knotless segment dominated the global suture anchors market with the highest market share of over 60% in 2025. The segment is expected to grow at a CAGR of 5.3% and maintain its dominance by 2032. A knotless suture anchor is a type of medical device that is used in orthopedic treatments/ surgeries to attach soft tissues to the bone without the use of conventional knots. These anchors provide simplified surgical technique, stronger fixation, reduced implant profile, time-saving benefits, and versatility in various orthopedic procedures. Thus, thanks to its benefits, these types of anchors are widely used in orthopedic surgeries over other tying types, thereby supporting segment growth.

Knotless suture anchors have the advantage of being easier to operate with cutting-edge technology and less likely to damage cartilage while still providing adequate knot security and tension, as mentioned in the research article "Knot-Tying versus Knotless Suture Anchors for Arthroscopic Bankart Repair: A Comparative Study" published in July . Likewise, knotless suture anchors have reduced the time required to complete the process and increased adaptability. As a result of the shift in demand towards high-quality joint surgeries, the knotless suture anchor segment is expected to increase during the forecast period. In addition, increasing investment in research and development activities to enhance the performance and durability of knotless suture anchors, is expected to further increase the attractiveness of these types of anchors in surgeons and healthcare professionals. Key suture anchors vendors are focusing on creating new products to diversify their product portfolios and drive market growth. For example,

In addition, increasing investment in research and development activities to enhance the performance and durability of knotless suture anchors, is expected to further increase the attractiveness of these types of anchors in surgeons and healthcare professionals. Key suture anchors vendors are focusing on creating new products to diversify their product portfolios and drive market growth. For example,

3. Acuitive Technologies gained approval from the US Food and Drug Administration (FDA) in February to commercialize the CITREFIX Knotless Suture Anchor System using CITREGEN material technology, a new-generation bioresorbable synthetic polymer.

4. In2Bones Global Inc. released the "Hercules Suture Anchor System" in February , including a revolutionary knotless suture anchor and radiolucent PEEK material.

Besides that, suture anchor suppliers use significant growth strategies such as mergers and acquisitions, joint ventures, collaboration, etc. to retain their global market share. As an example,

5. Smith+Nephew formed a marketing agreement with Movendo Technology (Genoa, Italy) in March , which is expected to offer personalized robotic rehabilitation capacity to the company's technology solutions. This partnership is expected to result in a fully digitized pathway for patients from the beginning to the end. The system is planned to operate on 130 distinct factors and provide a personalized patient rehabilitation program to enhance the articulation of the joint. Such advancements are expected to boost the segment growth during the forecast period.

Knotted suture anchors segment is expected to grow at a CAGR of 5.6% during the forecast period and provides significant growth potential during the forecast period. Knotted suture anchors are used in orthopedic surgeries to secure soft tissues, such as tendons or ligaments, to the bone using traditional knot-tying techniques. These types of anchors can be adjusted to achieve the desired tension in the repaired tissue. This adjustability allows the surgeon to fine-tune the tension during the procedure. Thus, this advantage is expected to increase the demand for these types of suture anchors and thereby supporting the segment growth. However, the knots are expected to create a bulkier profile compared to knotless anchors. This bulkiness increases the risk of soft tissue irritation or impingement. Additionally, the knot-tying process is time-consuming and expected to add complexity to the surgical procedure. Thus, these factors are expected to limit the segment growth.

Suture Anchors Market Regional Insights:

North America led the global suture anchors market with the highest revenue share of 42.5% in 2025. The region is expected to grow at a CAGR of 5.7% during the forecast period and maintain its dominance by 2032. Increasing Musculoskeletal disorders among North American individuals, rising incidence of sports-related injuries, and bariatric surgeries, and increasing chronic disorders in the region are expected to be the major growth factors driving the regional market growth.

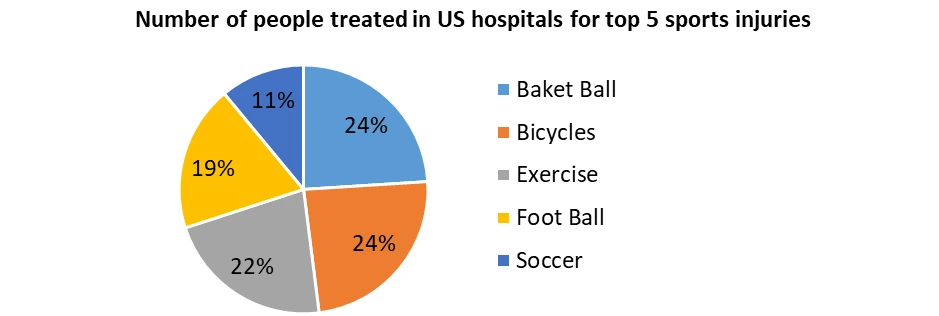

North America has a high incidence of sports-related injuries, such as shoulder and knee injuries, which often require suture anchor-based surgical interventions. According to the MMR analysis, approximately 6 million individuals in the United States break a bone each year. Hip fractures are the most common fractured bone in persons over the age of 75. Every year, fractures account for 16% of all musculoskeletal injuries in the United States. At home, more than 40% of fractures occur. Musculoskeletal difficulties among elderly people are another factor driving the growth of the suture anchor device market, as they raise demand for suture anchor devices, which is expected to support growth in the region. Sports-related injuries are expected to be another major factor boosting the suture anchors market growth. Approximately, 260,000 players were treated for injuries caused by basketball in the United States in . In , more than 220,000 Americans were treated for injuries related to football. In addition, More than 140,000 people show up in U.S. emergency departments because of soccer injuries each year.

Sports-related injuries are expected to be another major factor boosting the suture anchors market growth. Approximately, 260,000 players were treated for injuries caused by basketball in the United States in . In , more than 220,000 Americans were treated for injuries related to football. In addition, More than 140,000 people show up in U.S. emergency departments because of soccer injuries each year.

Furthermore, according to Centres for Disease Control and Prevention (CDC) data revised in March , the number of emergency department visits in the United States in was 130 million, and the number of injury-related visits was 35 million. This rise in emergency visits, along with an increase in injuries, is expected to result in a higher proportion of suture anchor implants used for treatment in the United States, driving the suture anchors market growth. Besides that, increasing chronic disorders such as osteoarthritis or tendinopathy, are more prevalent among the elderly population. Thus, an increase in the number of people requiring orthopedic interventions is expected to increase the demand for suture anchors, thereby driving the suture anchors market growth.

Asia Pacific region is expected to grow at a significant CAGR and offer lucrative growth opportunities for suture anchors manufacturers during the forecast period. The increasing prevalence of osteoarthritis among individuals in the APAC region is expected to be the primary growth factor driving the suture anchors market growth. According to the MMR studies, the highest number of osteoarthritis cases in were found in China (132.81 million), and India (62.36 million). When conservative therapies such as medicine and physical therapy fail to give adequate relief in advanced incidents of osteoarthritis, surgical intervention is required. Suture anchors are frequently used to fix and heal injured soft tissues, ligaments, or tendons during joint procedures such as arthroscopic debridement, osteotomy, or joint replacement. Thus, the growing number of osteoarthritis cases is expected to increase the demand for these orthopedic procedures and associated suture anchors, thereby driving Suture Anchors Market growth.

In addition, sports-related activities have increased rapidly in recent years in the Asia Pacific region. Asia has emerged as a significant location for global athletic events, and Asian home-grown professional sports leagues are gaining attraction and significance in the international arena. Cricket in India represents Asia's enormous contribution potential to the global sports ecosystem. The Indian Premier League (IPL) is presently one of the world's most valuable sports leagues.

The ordinary Indian's profound affinity to sports has resulted in the formation and investment of sports-related companies and other parts of the sports sector, particularly fantasy sports. As a result, participation in sports, both amateur and professional, is expected to lead to a higher incidence of sports-related injuries. These injuries often involve damage to ligaments, tendons, and other soft tissues that are expected to require surgical repair, eventually increasing the demand for suture anchors devices and driving the suture anchors market growth.

Suture Anchors Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 18 July 2025 | Smith+Nephew | Launched the Q-FIX KNOTLESS All-Suture Anchor for soft tissue-to-bone fixation. | Enhances fixation strength and efficiency in shoulder, hip, and foot/ankle arthroscopic procedures. |

| 10 July 2025 | OSSIO | Introduced the OSSIOfiber 2.5 mm Suture Anchor for specialized orthopedic repairs. | Provides a bio-integrative solution for Brostrom repairs, eliminating permanent implant risks in lateral ankle instability. |

| 12 February 2026 | Acuitive Technologies | Received regulatory clearance for the CITREFIX Knotless Suture Anchor System. | Utilizes CITREGEN material technology to offer a next-generation bioresorbable alternative to traditional PEEK anchors. |

| 05 January 2026 | Stryker Corporation | Updated its sports medicine portfolio with the integration of advanced all-suture technology. | Strengthens market position in minimally invasive surgery by reducing subacromial irritation through knotless designs. |

| 20 March 2026 | Arthrex | Expanded the SwiveLock anchor line to include high-tensile FiberTape options. | Increases the contact area at the tendon-bone interface, improving biological healing in rotator cuff repairs. |

Suture Anchors Market Scope: Inquire before buying

| Suture Anchors Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 744.33 USD Mn |

| Forecast Period 2026-2032 CAGR: | 5.4% | Market Size in 2032: | 1075.6 USD Mn |

| Segments Covered: | by Product Type | Absorbable Non-Absorbable |

|

| by Tying Type | Knotless Knotted |

||

| by Material Type | Metallic Suture Anchor Bio-absorbable Suture Anchor PEEK Suture Anchor Bio-composite Suture Anchor Others |

||

| by End-User | Hospitals and Clinics Ambulatory Surgical Centers Others |

||

Suture Anchors Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Suture Anchors Manufacturers, Key Players:

1.Arthrex (United States)

2. Smith & Nephew (United Kingdom)

3.Medtronic (Ireland)

4. DePuy Synthes (Johnson & Johnson) (United States)

5.CONMED Corporation (United States)

6.Zimmer Biomet (United States)

7.Stryker Corporation (United States)

8.Biomet (part of Zimmer Biomet) (United States)

9. B. Braun Melsungen AG (Germany)

10.Ethicon (Johnson & Johnson) (United States)

11.Mitek Sports Medicine (Johnson & Johnson) (United States)

12. CONMED Linvatec (United States)

13.Wright Medical Group N.V. (United States)

14.Karl Storz GmbH & Co. KG (Germany)

15.ArthroCare Corporation (Smith & Nephew) (United States)

16.DJO Global (United States)

17.Bioretec Ltd. (Finland)

18.Teknimed (France)

19. Merete Medical GmbH (Germany)

20.Ortosintese (Brazil)

21.Innomed, Inc. (United States)

22. Shanghai Kinetic Medical Co., Ltd. (China)

23. Tianjin Walkman Biomaterial Co., Ltd.(China)

24.ConMed Corporation (United States)

25. Surgicraft Ltd. (United Kingdom)

26.Teknimed (France)

27. FX Solutions (United States)

28. Arthro Surface (United States)

29. Tenex Health (United States)

30.Stars Medical Devices (France)