Surety Market by Bond Type, End User, Industry and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

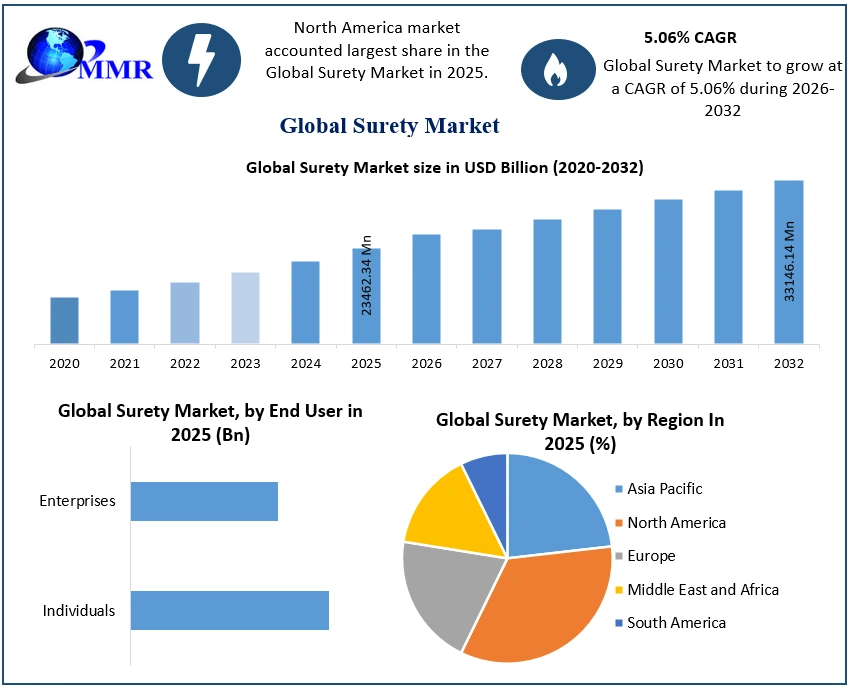

The Surety Market size was valued at USD 23462.34 Million in 2025 and the total Surety revenue is expected to grow at a CAGR of 5.06% from 2025 to 2032, reaching nearly USD 33146.14 Million by 2032.

The MMR report provides an in-depth examination of the macroeconomic and regulatory forces shaping the Surety Market in 2025 and beyond. It analyzes the impact of interest rate fluctuations, inflationary pressures, global conflicts, and the ongoing shift from bank guarantees to surety bonds, highlighting how these dynamics affect premium pricing, underwriting capacity, and risk appetite. The report also explores interest cost savings through bond insurance, repricing risks, and the growing involvement of reinsurers in managing large bond exposures. Additionally, it covers evolving claims trends and loss ratios, while offering a detailed assessment of regulatory and legal frameworks, including U.S.-specific surety laws, international compliance standards like FIDIC and EU bonding laws, licensing and solvency requirements, and cross-border regulatory developments, providing a comprehensive view of the global surety landscape.

To know about the Research Methodology :- Request Free Sample Report

Surety is a financial arrangement where one party, the surety, guarantees the performance, obligations, or debts of another party, the principal, to a third party, obligee. This ensures that the principal fulfils their contractual obligations, and if they fail, the surety compensates oblige for any losses incurred. The Surety Market growth is influenced by the need for financial guarantees on large infrastructure projects, allowing contractors meet their obligations. North America holds a dominant position, followed by Europe and Asia-Pacific region, reflecting the construction industry health and regulatory frameworks in this region.

Economic growth fuels the surety market's growth. The need for infrastructure development, driving demand for surety bonds. For instance, in India, recent launch of Surety Insurance Bonds supports the government's infrastructure agenda, unlocking capital for contractors and enhancing their bidding capacity. This initiative is crucial as India aims to become a USD 5 trillion economy. Regulatory changes, such as U.S. Small Business Administration increasing statutory contract limits for the Surety Bond Guarantee Program, further boost small business’s ability to secure larger projects, promoting economic growth and job creation.

Technological advancements and strategic partnerships also play a critical role in the Surety Market evolution. Bond-Pro, a leading collateral software platform, is partnering with Surety2000 and Xenex Enterprises to automate collateral bond services, simplify issuance and increase efficiency. This collaboration solves industry challenges by integrating electronic signature verification technology, streamlining the traditionally complex mortgage issuance process. The Bond-Pro Bond Expedite service further simplifies the purchase of bail bonds, improving the experience of insurance companies, agents and customers

Recent developments by key players highlight the dynamic nature of the surety market. For example, TATA AIG's Surety Insurance Bonds cater to both government and private sector projects, offering coverage against contractor non-performance and facilitating smooth project execution. This product suite includes various contract bonds, such as bid bonds and performance bonds, in line with IRDAI guidelines. The National Highways Authority of India (NHAI) has accepted insurance surety bonds for bid security, enhancing liquidity for highway projects and setting a new benchmark in the road infrastructure sector.

Market Dynamics:

Infrastructure Development and Government Spending drive the market growth:

The rise in government infrastructure spending, particularly grow by initiatives like the $1.2 trillion infrastructure bill in United States, serves as significant driver for the surety market. This increased investment fuels demand for surety bonds to guarantee the completion of various projects, ranging from bridges and airports to public transit systems. For instance, allocation of $550 billion in US infrastructure bill for projects such as grid modernization and broadband growth has led to substantial uptick in surety bond requirements. India's focus on infrastructure development, as evidenced by announcements in Union Budget 2024 and the hosting of the G20 summit, underscores the trend of governments prioritizing infrastructure investment, driving demand for surety bonds to secure these projects.

Technological advancements and digitization are transforming surety bond industry, streamlining processes, reducing costs, and enhancing efficiency. Innovations such as blockchain and artificial intelligence are revolutionizing how surety bonds are issued, managed, and serviced. For instance, use of blockchain enhances security and transparency, eliminating traditional paperwork and reducing fraud risks. AI improves risk assessment and fraud detection, providing more accurate underwriting. Companies like Xenex are at the forefront of this transformation, offering solutions like Signature Master and Surety Master Bonds. These technological improvements make surety bonds more accessible and reliable, driving Surety Market growth by attracting more businesses to use these advanced financial instruments.

Growing emphasis on Environmental, Social, and Governance (ESG) factors is another driver of the surety market. Stakeholders, including surety providers, are increasingly considering companies' commitment to sustainability, safety, and ethical practices. This shift is evident in the construction industry, where firms integrating ESG principles into their operations improve their bonding capacity and Surety Market reputation. For instance, leading construction company in Brazil has initiated a sustainability program to reduce carbon emissions, which has enhanced its competitiveness and attractiveness to environmentally-conscious clients and investors. The emphasis on ESG factors aligns with broader societal and regulatory trends, encouraging more companies to adopt surety bonds that support sustainable and ethical business practices.

Growing Technological Advancements and Digitization in the market:

The integration of advanced technologies like blockchain and AI into the surety industry is transforming the Surety Market. Partnerships such as that between Bond-Pro, Surety2000, and Xenex Enterprises streamline surety bond processing, making it more efficient and secure. For example, Bond-Pro’s Bond Expedite simplifies the purchase process by enabling online applications and instant decisions, reducing cumbersome traditional methods. This technological shift not only enhances efficiency but also attracts more users to the surety market, driving its growth.

The growth in infrastructure projects and government spending significantly drives growth of the surety market. For instance, India's allocation of 3.3% of GDP for infrastructure development in 2025 aims to support its journey to becoming a USD 5 trillion economy. Surety bonds, like those introduced by TATA AIG, provide contractors with alternatives to traditional bank guarantees, enhancing their bidding capacity and overcoming liquidity constraints. This increased use of surety bonds facilitates the smooth execution of infrastructure projects and commercial contracts, thereby boosting Surety Market demand.

Regulatory changes, such as the U.S. Small Business Administration increasing statutory contract limits for the Surety Bond Guarantee Program, create significant growth opportunities. By raising the guaranteed limits to $9 million for general projects and $14 million for federal contracts, the SBA is enabling small businesses to access larger projects and federal contracts. This support helps small businesses win more contracts, fostering economic growth and increasing the demand for surety bonds, thereby expanding the Surety Market.

Surety Market Segment Analysis:

Based on Bond Type, the Surety Market is segmented into Contract Surety Bonds, Fidelity Surety Bonds, Court Surety Bonds, and Commercial Surety Bonds. Contract Surety Bonds dominated the Surety Market with a 58.24% share in 2025 due to their crucial role in construction and infrastructure projects globally. These bonds guarantee that contractors fulfill their contractual obligations, including timely and budget-compliant project completion. This includes bid bonds, performance bonds, and payment bonds. Bid bonds ensure contractors have the financial capacity to undertake projects, performance bonds provide financial protection if contractors fail to complete projects, and payment bonds ensure subcontractors and suppliers are paid.

For example, in a municipal building project, a performance bond is required from the contractor. If the contractor fails to meet obligations, the surety company remedies the situation, potentially hiring a new contractor or compensating the project owner for losses. While Contract Surety Bonds are in high demand, other segments like Commercial Surety Bonds, Fidelity Surety Bonds, and Court Surety Bonds are also important. Commercial Surety Bonds guarantee non-construction-related contracts such as licenses and leases, Fidelity Surety Bonds protect against employee dishonesty, and Court Surety Bonds ensure compliance with legal obligations, including bail and appeal bonds.

Based on End User, in 2025, the Construction segment leads the Surety Market, capturing the largest share thanks to its reliance on contract bonds for infrastructure and public works projects, fueled by strong infrastructure investments and legislation like the U.S. Infrastructure Investment and Jobs Act. Automotive & Transport and Machinery & Equipment Manufacturers follow, driven by performance and supply guarantees in manufacturing and logistics. The IT & Telecommunications and Electronics sectors are growing due to increasing project-based contracts requiring commercial surety. Chemical, Metal & Mining, and Food Industry industries contribute moderately through compliance and license bonding needs, while Others—including healthcare, hospitality, and SME sectors—round out the market with smaller but steady demand.

Surety Market Regional Insights:

North America holds largest market share of the surety market, accounting for 50.44% of the market, is driven by a robust construction industry, and stringent regulatory frameworks. The region's thriving construction sector features significant infrastructure development projects, ranging from commercial buildings and residential complexes to large-scale public infrastructure initiatives. These projects often mandate surety bonds to guarantee performance, payment, and adherence to contractual obligations. Well-established surety market players, including insurance companies, surety bond producers, and bonding agent, contribute to the market accessibility. Regulatory requirements and licensing mandates in North America drive sustained demand for surety bonds across various sectors, with businesses relying on these bonds to demonstrate financial responsibility and compliance with regulatory standards.

Europe is the 2nd largest market, accounting for 21.93 percent of the surety market. Europe benefits from a mature construction industry and stringent regulatory frameworks. The EU regulations also promote the use of surety bonds for various commercial activities, allowing financial security and compliance with contractual obligations. APAC holds 13.80 percent and is expected to experience significant growth. The region growing construction industry, driven by rapid infrastructure development contributes to this growth. Governments in these countries are increasingly adopting surety bonds to ensure project completion and mitigate financial risks.

Competitive Landscape

Recent developments in the surety bond market are poised to drive significant growth. Key acquisitions, such as Marsh McLennan Agency's purchase of HMS Insurance Associates and Talanx Group's acquisition of Liberty Seguros' operations in Latin America, have expanded their expertise and Surety Market reach. Additionally, TATA AIG General Insurance's launch of Surety Insurance Bonds in India introduces innovative alternatives to traditional bank guarantees, boosting contractors' financial capacity. Furthermore, Bond-Pro's partnership with Surety2000 and Xenex Enterprises to automate surety bond processing addresses industry challenges with digital solutions, enhancing efficiency and adoption. These strategic moves collectively strengthen the Surety Market, ensuring robust growth and improved service offerings.

On January 4, 2023, Marsh McLennan Agency (MMA) announced the acquisition of HMS Insurance Associates, a strategic move aimed at enhancing MMA's growth, service offerings, and talent retention. This acquisition allows MMA to expand its expertise in the specialized area of surety bonds, which are essential for guaranteeing the performance and fulfillment of contractual obligations. By integrating HMS' strengths in this niche market, MMA better serve clients with surety bond needs, aligning with its long-term goals and competitiveness in the insurance industry.

On May 27, 2023, Talanx Group's Retail International division acquired Liberty Seguros' personal and small commercial businesses in Brazil, Chile, Colombia, and Ecuador. This strategic move elevated Talanx to the third-largest property and casualty insurer in Latin America, with an anticipated increase in gross written premiums of approximately EUR 1.7 billion. Post-acquisition, Talanx's HDI division ranked second in Brazil, first in Chile, and seventh in Colombia. This acquisition supports Talanx's goal of securing top market positions and enhancing technical excellence and portfolio diversification by 2025.

On May 29, 2024, TATA AIG General Insurance launched Surety Insurance Bonds to bolster India's infrastructure development, which accounts for 3.3% of GDP in FY 2024. These bonds offer an alternative to traditional bank guarantees, enhancing contractors' capital and bidding capacity. They cover losses from contractors' non-performance, non-fulfillment, or breach of contractual obligations. TATA AIG’s bonds, available in conditional and unconditional formats, include bid, performance, advance payment, and retention money bonds, facilitating smoother project execution in both the government and private sectors.

On April 10, 2024, Bond-Pro announced a partnership with Surety2000 and Xenex Enterprises to fully automate surety bond processing. This collaboration aims to streamline surety bond issuance from start to finish by integrating leading surety bond electronic signature and authentication technologies from the U.S. and Canada. Surety bonds, which require multiple approvals, have traditionally relied on raised seals and wet signatures. Transitioning to electronic methods has been challenging due to the need for legislative acceptance and proof of authenticity. This partnership addresses these issues, facilitating the adoption of digital surety bonds and improving efficiency in the industry.

Surety Market Scope: Inquiry Before Buying

| Surety Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 23462.34 Million |

| Forecast Period 2026 to 2032 CAGR: | 5.06 % | Market Size in 2032: | USD 33146.14 Million |

| Segments Covered: | by Bond Type | Contract Surety Bond Commercial Surety Bond Fidelity Surety Bond Court Surety Bond Others |

|

| by End User | Individuals Enterprises |

||

| by Industry | IT & Telecommunications Construction Machinery & Equipment Manufacturers Chemical Electronics Food Industry Metal & Mining Automotive & Transport Others |

||

Surety Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Surety Market, Key Players

1. The Travelers Indemnity Company.

2. Liberty Mutual Insurance Group

3. Chubb Limited

4. CNA Financial Corporation

5. The Hartford Financial Services Group, Inc.

6. The Hanover Insurance Group

7. Old Republic Surety Company

8. RLI Corp

9. Great American Insurance Company

10. AmTrust Financial

11. Markel Corporation

12. Hudson Insurance Group

13. Merchants Bonding Company

14. Westfield

15. IAT Insurance Group

16. CapSpecialty, Inc.

17. United Fire & Casualty Company (UFG Insurance)

18. FCCI Insurance Group

19. Everest Re Group, Ltd.

20. Arch Insurance Group

21. Coface

22. Swiss Re

23. AoN

24. Zurich Insurance Group

25. Tokio Marine HCC

26. AXA XL

27. QBE Insurance Group Limited

28. Intact US Insurance

29. Berkshire Hathaway Specialty Insurance

30. Marsh McLennan

31. Others

FAQs:

1] What segments are covered in the Surety Market report?

Ans. The segments covered in the Surety Market report are based on Bond Type, End User, Industry, and region

2] Which region is expected to hold the highest share of the Surety Market?

Ans. The North America region is expected to hold the highest share of the Surety Market.

3] What is the market size of the Surety Market by 2032?

Ans. The market size of the Surety Market by 2032 is USD 33146.14 Mn.

4] What is the growth rate of the Surety Market?

Ans. The Global Surety Market is growing at a CAGR of 5.06 % during the forecasting period 2026-2032.

5] What was the market size of the Surety Market in 2025?

Ans. The market size of the Surety Market in 2025 was USD 23462.34 Mn.