Space Food Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

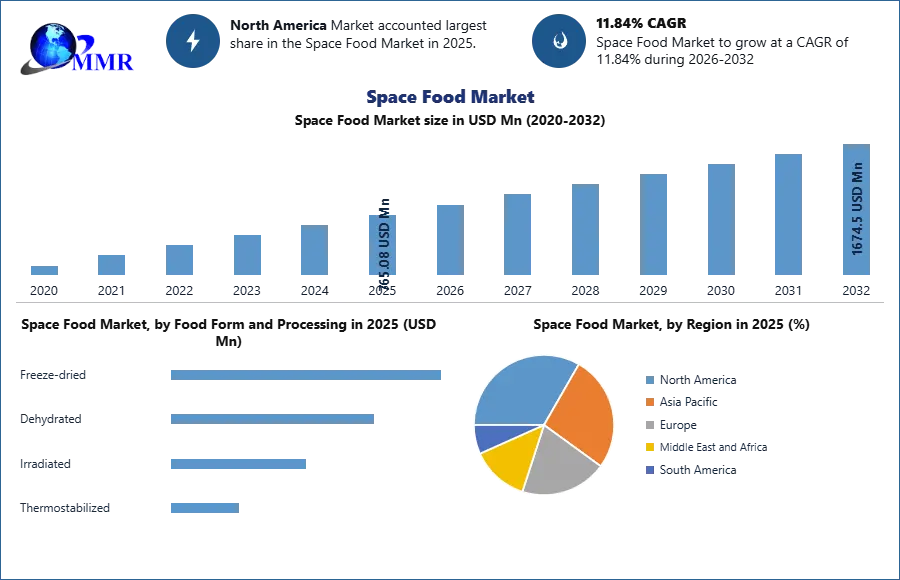

The Space Food Market size was valued at USD 765.08 Million in 2025 and the total Space Food revenue is expected to grow at a CAGR of 11.84% from 2026 to 2032, reaching nearly USD 1674.50 Million.

Space Food Market Overview:

The Space Food Market pertains to the specialized sector of the food industry that focuses on the research, development, production, and supply of consumable products intended for consumption by astronauts during space missions. Space food products are meticulously designed to meet the unique challenges of space travel, including microgravity conditions, limited storage capacity, prolonged shelf life requirements, and nutritional needs to sustain the health and performance of astronauts during their missions. The concept of personalized space nutrition is gaining traction, and by , investments in this niche are expected to reach 10 million. This approach not only aligns with broader trends in personalized nutrition on Earth but also presents a unique avenue for innovation in the context of space exploration. In mission Endeavor I NASA invested approximately $65 million in contracts for the development of Space Food technologies. This investment reflects the growing importance of enhancing the quality, variety, and sustainability of space food options to support longer-duration missions.

The Space Food Market is undergoing a structural transformation as the 2026 Middle East crisis destabilizes global supply chains. With the Hormuz blockade driving crude to $120/bbl, energy-intensive freeze-drying overheads have spiked 30%, while 400% maritime freight surcharges disrupt specialized packaging logistics. Industry leaders are prioritizing near-shored "Closed-Loop" production and circular bio-regenerative models to bypass volatile corridors. This strategic shift is essential for maintaining the 11.84% CAGR, ensuring mission readiness and sustainable nutrition for the expanding orbital and lunar sectors.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Space Food Market Dynamics:

Prolonged Space Missions to Boost the Space Food Market Growth

The expansion of space missions beyond the International Space Station (ISS) to destinations such as the Moon, Mars, and potentially even farther, demands that astronauts have access to sustenance for extended periods. Traditional space food technologies, designed for shorter missions, are insufficient for journeys that span months or years. As a result, there is a critical need for food products that offer extended shelf life while retaining their nutritional value and palatability. Astronauts' health and performance are reliant on receiving proper nutrition. Space Food market focuses not only on extending shelf life but also on maximizing nutrient retention.

The development of space food that maintains its vitamins, minerals, and macronutrients over extended periods addresses the nutritional requirements of astronauts, ensuring they remain in optimal health throughout their missions. Weight and volume limitations on spacecraft pose significant challenges for provisioning missions. Space Food technologies aim to minimize the weight and volume of food items without compromising their nutritional content. This resource efficiency is crucial for conserving limited cargo space, reducing launch costs, and accommodating other essential equipment and supplies.

Long-duration space missions can lead to sensory monotony, impacting astronauts' mental well-being and causing decreased appetite. Developing Space Food that retains its taste, texture, and variety can contribute to astronauts' psychological comfort and overall satisfaction. Such food not only provides essential nourishment but also contributes to maintaining positive morale during isolation in space. Innovations in food processing techniques, such as high-pressure processing, controlled fermentation, and regenerative systems, offer the potential to create space food that is both safe and nutritious. These methods can enhance the preservation of food without relying heavily on traditional methods that might compromise quality.

Space Food technologies allow for a level of customization in astronauts' diets based on individual nutritional needs and preferences. This capability ensures that each astronaut's dietary requirements are met, optimizing their performance and health. Developing space food that relies on closed-loop systems, such as cultivating crops or producing protein-rich foods in space, reduces the need to transport all provisions from Earth. This enhances the sustainability of missions, reduces dependency on resupply missions, and positions astronauts for future deep space exploration. The development of Space Food is not limited to food science; it involves collaborations across various disciplines such as nutrition, materials science, packaging engineering, and even psychology. This convergence of expertise accelerates the innovation process, resulting in holistic solutions that address the multifaceted challenges of space food provision.

The complexity of Nutritional Requirements to Restraint the Space Food Market Growth

One significant restraint in the development of Space Food is the complexity of meeting astronauts' precise nutritional needs. Space missions demand nutritionally balanced diets that support optimal physical and cognitive performance. Achieving this balance while factoring in individual dietary preferences, cultural considerations, and the potential physiological impacts of extended space travel presents a multifaceted challenge and is expected to hamper the Space Food market growth. Space Food must not only deliver essential nutrients but also cater to specific requirements unique to space conditions, such as mitigating bone density loss and muscle degradation due to microgravity. Spacecraft have stringent limitations on available resources, including space, weight, and power. These constraints impact the design, production, and packaging of Space Food. Innovations that add significant weight or require extensive storage space can strain already limited resources and potentially compromise mission objectives. Developing food products that efficiently utilize available resources while meeting nutritional and sensory criteria is a restraint that demands careful consideration of every aspect of food technology.

The psychological well-being of astronauts is crucial for mission success. In the confined and isolated environment of space, the appeal, taste, and variety of food become essential factors in maintaining morale and mental health. Space Food technology, while focusing on nutritional optimization, must also ensure that meals remain appealing and satisfying. Failure to meet astronauts' sensory expectations can lead to decreased appetite, potential nutritional deficiencies, and a negative impact on overall mental health and mission effectiveness. Ensuring the safety and compliance of Space Food with stringent regulations is a significant restraint expected to restrain the Space Food market growth over the forecast period. The introduction of new ingredients, processing methods, or packaging technologies requires thorough testing and approval. The unique challenges posed by the space environment, such as altered metabolism and potential interactions with medications, necessitate rigorous assessment. Navigating the complex regulatory landscape while adhering to high safety standards is a constraint that demands meticulous attention and collaboration between food scientists, regulatory bodies, and space agencies.

The reliability of Space Food technology is paramount to astronauts' safety and mission success. Space missions are characterized by high stakes, and any failure in food production, packaging, or preservation can have severe consequences. Ensuring the consistent functionality of food technology under varying conditions, such as temperature fluctuations and microgravity, is a significant challenge. Redundancy, fail-safe mechanisms, and rigorous testing protocols are required to mitigate the risk of technology failure in space. Developing Space Food requires collaboration across multiple disciplines, including food science, engineering, materials science, and nutrition. Coordinating efforts and ensuring effective communication among experts from diverse fields can be challenging, particularly when addressing the intricate interplay between nutritional content, sensory attributes, and technological feasibility. Effective interdisciplinary integration is essential to create cohesive solutions that meet the demands of space food while also considering practical constraints and scientific requirements.

Space Food Market Segment Analysis:

Based on the Food Form and Processing Segment, this segment classifies space food based on its form and processing methods. It encompasses freeze-dried, dehydrated, irradiated, thermostabilized, and bioregenerative foods. Freeze-dried foods are popular due to their lightweight nature and long shelf life, making them suitable for extended missions. Thermostabilized foods are heat-treated for preservation, while irradiated foods undergo radiation treatment to prevent microbial growth. Bioregenerative foods involve growing crops in space for fresh produce. Analyzing the pros and cons of each form guides menu planning and storage strategies.

Based on the Packaging and Preservation, the market is segmented into vacuum-sealing

Modified atmosphere packaging controlled temperature storage. Packaging and preservation techniques segment addresses the methods used to maintain space food quality and safety. Packaging must prevent moisture ingress, oxidation, and microbial contamination while remaining compact and lightweight. Preservation methods such as vacuum sealing, modified atmosphere packaging, and controlled temperature storage are crucial to extending shelf life and preventing nutrient degradation. Innovations in packaging materials and techniques are vital to ensuring food safety and quality throughout the mission

Space Food Market Regional Insights:

North America, home to leading space agencies such as NASA and private space companies, is at the forefront of space food research and innovation. The United States, with its robust space exploration endeavors, has pioneering advancements in space food technology. NASA's Johnson Space Center has been a key player in developing and testing space food to meet the nutritional requirements of astronauts. Collaborations between government agencies and private sector entities drive the innovation of advanced packaging, preservation methods, and sensory enhancements. The region's research institutions and technological expertise enable it to remain a leader in space food technology within the forecast period.

Europe, with its collaborative approach to space exploration through the European Space Agency (ESA), contributes significantly to the space food market. Countries such as France, Germany, and Italy are engaged in research to develop nutritious and palatable space food solutions. European food technology companies work closely with space agencies to create meals that cater to the preferences and dietary needs of European astronauts. The region's emphasis on sustainability and environmental consciousness extends to space food, with efforts to minimize packaging waste and develop efficient production processes.

The Asia-Pacific region, driven by space agencies in countries such as China and Japan, is increasingly asserting its presence in the space food market. China's notable advancements in space exploration have spurred research into space food technology to support its ambitious missions, including lunar exploration. Japan's space agency, JAXA, collaborates with food companies to develop nutritious and culturally appropriate meals for its astronauts. The region's focus on innovation and collaboration positions it as an emerging player in the global space food market.

Space Food Market Competitive Landscape:

NASA, the premier space agency of the United States, assumes a pioneering role within the space food market. Over several decades, NASA has cultivated an extensive portfolio of space food solutions, spanning from freeze-dried repasts to sophisticated nutrient-enhanced products. The agency's unwavering commitment to research, synergistic collaborations with food scientists, and a culture of innovation have established a definitive benchmark for space food technology. NASA's unceasing dedication to refining taste, nutritional profiles, and packaging has culminated in the formulation of nourishing meals impeccably tailored to address astronauts' requisites throughout protracted space missions.

In a parallel vein, the European Space Agency (ESA) emerges as a formidable contender in the space food market. Comprising member states across Europe, ESA engenders synergies with food technology enterprises to engineer culinary offerings harmonizing with the distinct inclinations and nutritional necessities of European astronauts. The agency's pronounced emphasis on sustainability, exemplified by its endeavors in waste minimization and resource optimization, permeates its methodology in space food production.

Simultaneously, private space enterprises are progressively asserting greater influence within the space food market. Companies such as SpaceX, Blue Origin, and Boeing are venturing beyond the ambit of spacecraft development to embrace the frontiers of space food technology. An orientation towards commercial space travel has impelled these companies to pioneer innovative methodologies in the sphere of space food production. Groundbreaking approaches such as 3D printing and streamlined packaging solutions are emblematic of their entrepreneurial zeal and competitive spirit, potentially hastening the trajectory of technological progress within the market.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 19 January 2026 | Seraphim Space | The firm reported that private investment in SpaceTech grew 48% to $12.4 billion in 2025, signaling a full recovery from previous downturns. | Increased capital availability accelerates the commercialization of deep-space provisioning and life-support infrastructure. |

| 25 June 2025 | Charoen Pokphand Foods (CPF) | CPF’s Thai chicken dishes officially arrived at the ISS via Axiom Mission 4, marking the first time Thai cuisine met NASA’s safety standards. | This mission validates commercial food certification processes and expands the variety of palatable meals available for international crews. |

| 15 March 2026 | SpaceX | SpaceX led the competitive landscape by vertically integrating crew mission provisioning, significantly reducing launch-to-table costs. | Vertical integration disrupts traditional suppliers by allowing launch providers to control the entire food supply chain for space tourism. |

| 30 September 2025 | mu Space | The company signed a Memorandum of Understanding with DigitalBlast to collaborate on advancing lunar exploration and habitability technologies. | The partnership focuses on bioregenerative systems essential for long-term food sustainability on the Moon's surface. |

| 13 March 2026 | SP Scientific | The company scaled its VirTis Advantage Pro lyophilizer production to meet a 30% surge in demand for freeze-dried space ingredients. | Improved lyophilization efficiency reduces the energy footprint of space food processing, making it more viable for large-scale production. |

| 02 March 2026 | NASA | NASA released its FY 2026 budget request, which includes ring-fenced funding for the development of advanced food preservation for Mars missions. | Government funding guarantees R&D stability for technologies aimed at extending food shelf-life to the required five-year window. |

Space Food Market Scope: Inquire before buying

| Space Food Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 765.08 USD Mn |

| Forecast Period 2026-2032 CAGR: | 11.84% | Market Size in 2032: | 1674.5 USD Mn |

| Segments Covered: | by Food Form and Processing | Freeze-dried Dehydrated Irradiated Thermostabilized |

|

| by Packaging Type | Pouches Cans Tubes Others |

||

| by End User | Astronauts Space Tourists |

||

Space Food Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Space Food Market Report in Strategic Perspective:

- NASA (United States)

- European Space Agency (ESA) (France)

- Roscosmos (Russia)

- SpaceX (United States)

- Blue Origin (United States)

- Boeing (United States)

- Lockheed Martin (United States)

- Northrop Grumman Corporation (United States)

- Orbital ATK (United States)

- ISSpresso (Italy)

- Sierra Nevada Corporation (United States)

- Thales Alenia Space (France)

- Airbus Defence and Space (Germany)

- Made In Space (United States)

- NanoRacks (United States)

- Space Tango (United States)

- Bigelow Aerospace (United States)

- Space Adventures (United States)

- Zero Gravity Solutions (United States)

- Honeywell Aerospace (United States)

- Paragon Space Development (United States)

- JAXA (Japan)

- Charoen Pokphand Foods (Thailand)

- BeeHex (United States)

- Astroscale (Japan)

Frequently Asked Questions

1.What is the current Space Food Market size and the projected growth rate through 2032?

Ans. The market was valued at USD 765.08 million in 2025, expecting an 11.84% CAGR to reach USD 1674.50 million by 2032, driven by deep-space exploration.

2. Which region leads the Space Food Market share analysis and what factors drive its dominance?

Ans. North America dominates due to NASA's leadership and private investments. The region spearheads Space Food Market Trends 2026 through advanced R&D and specialized packaging innovation.

3. How is the shift toward long-duration missions acting as one of the primary industry growth drivers?

Ans. Extended missions to Mars demand advanced food preservation. This necessity fuels Space Food Market Trends 2026, focusing on five-year shelf lives and nutrient-dense, lightweight processing.

4. What role do private companies like SpaceX play in the Space Food Market competitive landscape?

Ans. Private firms accelerate commercialization through vertical integration. Their entry reduces launch-to-table costs, disrupting traditional supply chains and introducing 3D printing and innovative bioregenerative food systems.

5. How does personalized nutrition impact the Space Food Market revenue and astronaut health optimization?

Ans. Investments in personalized space nutrition enhance performance. Customizing diets to mitigate microgravity-induced bone loss represents a high-growth niche, attracting significant capital for individualized astronaut wellness solutions.

6. What are the primary technological challenges hindering the Space Food Market growth through 2032?

Ans. Strict safety regulations and microgravity's impact on metabolism restrain expansion. Balancing nutritional density with stringent weight, volume, and power constraints remains a complex engineering hurdle.

7. How are sustainability and closed-loop systems shaping the future of Space Food Market innovation?

Ans. Bioregenerative systems and waste minimization are critical for lunar habitability. Partnerships focusing on cultivating crops in space reduce Earth-dependency, ensuring long-term sustainability for future colonization.