Sleep Apnea Implants Market Size by Product, Indication Based, End User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

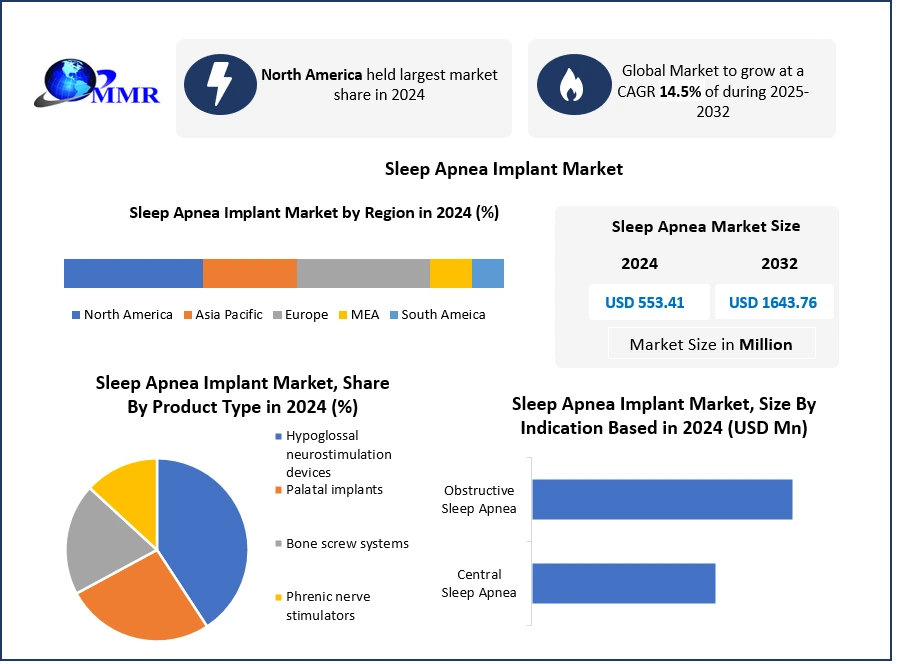

Global Sleep Apnea Implants Market size was valued at USD 556.41 Million in 2024, and the total Sleep Apnea Implants Market revenue is expected to grow by 14.5 % from 2025 to 2032, reaching nearly USD 1643.76 Million

Sleep Apnea Implants Market Overview

Sleep apnea implants are advanced medical devices designed to treat obstructive sleep apnea (OSA) by maintaining an open airway during sleep, offering an effective alternative for patients who cannot tolerate conventional therapies such as CPAP machines. These implants, including hypoglossal nerve stimulators (HGNS), deliver targeted stimulation to the airway muscles, reducing apnea events and improving sleep quality through minimally invasive procedures. The Sleep Apnea Implants Market presents significant growth opportunities, driven by the increasing number of patients seeking alternatives to CPAP therapy. For example, Nyxoah’s Genio system, a leadless and wearable HGNS device, demonstrated statistically significant improvements in the DREAM pivotal study, highlighting strong patient acceptance in the U.S. Similarly, Inspire Medical Systems’ next-generation Inspire V therapy, featuring a Bluetooth-enabled neurostimulator and remote-controlled app, is set for a full launch in 2025, reinforcing commercial potential. Rising OSA prevalence due to aging populations, obesity, and lifestyle factors boosts demand. Technological innovations, including fully upgradable wearable components and MRI-compatible devices, enhance patient comfort and therapy personalization. Regulatory approvals in North America and Europe, combined with increasing awareness among patients and healthcare providers about CPAP limitations, are supporting widespread adoption, driving global Sleep Apnea Implants Market growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Sleep Apnea Implants Market Dynamics

Rising Prevalence of Sleep Apnea to drive the growth of Sleep Apnea Implants Market

The global burden of sleep apnea is expanding at an alarming rate, creating significant demand for effective treatment solutions. Nearly 1 billion people worldwide are estimated to suffer from sleep apnea, with both diagnosed and undiagnosed cases contributing to a large patient pool. In the United States, up to one-third of adults are affected by Obstructive Sleep Apnea (OSA), while in India, more than 100 million working-age adults are believed to live with the condition. This growing prevalence is boosting the need for advanced therapies. Current treatment largely depends on Continuous Positive Airway Pressure (CPAP) devices; however, low adherence rates limit their effectiveness. More than half of patients discontinue CPAP use due to discomfort, noise, or inconvenience, leaving millions inadequately treated. This unmet need is encouraging the adoption of alternative solutions such as implant-based therapies, which offer greater convenience and long-term efficacy. The rising health and socioeconomic risks of untreated OSA further strengthen market growth. Untreated patients face higher risks of cardiovascular disease, diabetes, accidents, and reduced productivity, making effective interventions a priority for both individuals and healthcare systems. With growing awareness, improved screening, and continuous advancements in implant technology, the market is witnessing rapid adoption of innovative implantable devices, establishing sleep Apnea implants Market as a vital growth driver.

High Upfront Device and Procedure Costs Limit Market Growth

The high initial cost of devices and surgical procedures compared to traditional therapies such as CPAP machines and oral appliances limits the growth of Sleep Apnea Implants Market. A CPAP device typically costs between USD 500 and 1,000, while oral appliances may cost USD 1,800 to 2,000. In contrast, implant-based therapies, such as hypoglossal nerve stimulation implants, cost USD 20,000 to 40,000 per procedure, including device and surgical expenses. This sharp cost difference creates a barrier to accessibility, particularly in cost-sensitive regions. Insurance coverage also remains inconsistent. While some private insurers and Medicare in the U.S. cover part of the implant cost, out-of-pocket expenses still remain high for patients. In emerging markets such as India and China, where healthcare reimbursement systems are less comprehensive, affordability becomes a major limiting factor despite rising prevalence.

In the U.S., while over 17 million patients are diagnosed with OSA, only a fraction qualifies or opt for implants due to financial burden, leaving CPAP as the most widely used therapy. Similarly, in Europe, adoption is concentrated in wealthier nations such as Germany and the U.K., where reimbursement frameworks are more supportive. Thus, although implants offer superior long-term outcomes, their high cost compared to conventional therapies slows widespread adoption, limiting Sleep Apnea Implants Market.

Rising Demand for Hypoglossal Nerve Stimulation (HGNS) Devices Creates a Strong Market Opportunity

The limitations of Continuous Positive Airway Pressure (CPAP) therapy have created a significant opportunity for implantable solutions, particularly Hypoglossal Nerve Stimulation (HGNS) devices. CPAP remains the first-line treatment for Obstructive Sleep Apnea (OSA), yet adherence is low, with more than 50% of patients discontinuing use due to discomfort, inconvenience, or noise. This leaves millions of patients inadequately treated, opening a strong demand for alternative therapies’ devices address this gap by providing a minimally invasive and highly effective solution that directly stimulates airway muscles to prevent obstruction during sleep. Clinical studies have shown that HGNS significantly reduces apnea episodes, improves sleep quality, and enhances patient compliance compared to CPAP. This proven clinical effectiveness makes HGNS an attractive alternative for patients struggling with conventional therapies.

Real-time market adoption highlights this opportunity. In the United States, companies such as Inspire Medical Systems have reported consistent revenue growth as hospitals increasingly adopt neurostimulation implants for CPAP-intolerant patients. In Europe, Germany has emerged as a key hub for HGNS adoption due to strong reimbursement policies. Meanwhile, in China, rising awareness of OSA and limited CPAP acceptance are accelerating interest in advanced implantable therapies.Thus, the combination of unmet patient need, proven clinical outcomes, and expanding healthcare acceptance positions HGNS devices as one of the most promising growth opportunities in the sleep apnea implants market.

Next-Gen Sleep Apnea Implants: Hypoglossal Reliability Meets Trigeminal Innovation

In 2024, the market share for Sleep Apnea Implant Market dominated by hypoglossal neuro stimulation. Over 90,000 patients in total exhibit significant reductions in apnea-hypopnea index rates, cessation of loud snoring, and enhanced sleep quality. The latest pulse generator from Inspire Medical Systems reduces the risk of lifetime revision by extending battery life to 10 years. The market for trigeminal stimulators is expected to expand. Patients who are concerned about appearance find submental placement appealing because it avoids a chest pocket. Venture capital is drawn to this category because of the high safety margins and selective modulation of sleep architecture suggested by early clinical work. Miniaturization, user-friendly app interfaces, and MRI safety features are key components of competitive dynamics. Trigeminal devices are expected to take a sizable portion of the Sleep Apnea Implant Market by the end of the decade, according to strong momentum.

Sleep Apnea Implants Market Segment Analysis

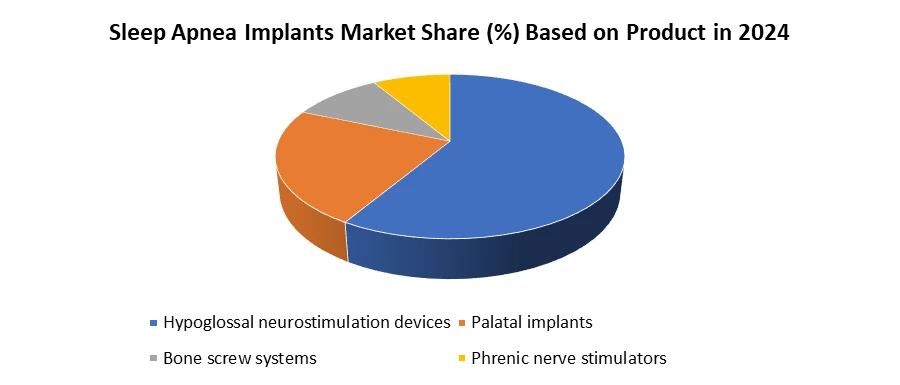

Based on Product, Sleep Apnea Implants Market the market is segmented into Hypoglossal neurostimulation devices, Palatal implants, Bone screw systems, Phrenic nerve stimulators. The Hypoglossal neurostimulation devices market dominated the Sleep Apnea Implants Market in 2024. Due to their superior clinical efficacy and growing adoption among patient’s intolerant to traditional CPAP therapy. HGNS devices work by stimulating the hypoglossal nerve to maintain airway patency during sleep, addressing the root cause of obstructive sleep apnea (OSA). This mechanism provides consistent outcomes compared to palatal implants or bone screw systems, which offer limited effectiveness in moderate to severe cases. Increasing clinical evidence, such as FDA-approved Inspire therapy, has boosted physician confidence and patient acceptance. Also, rising awareness through clinical trials and reimbursement approvals in key markets like the U.S. and Europe have accelerated adoption. Real-world examples, including the growing number of Inspire implants performed in U.S. hospitals, highlight the segment’s dominance.

Based on End User Sleep Apnea Implants Market the market is segmented into Hospitals, Ambulatory surgical Centers, Other. The Hospitals segment dominated the Sleep Apnea Implants Market End User Segment in 2024. Due to their advanced infrastructure, availability of specialized surgeons, and ability to manage complex cases. Sleep Apnea implant procedures, particularly hypoglossal neurostimulation, require advanced diagnostic facilities, skilled surgical expertise, and post-operative monitoring, which are more widely available in hospitals compared to ambulatory surgical centers (ASCs) or smaller clinics. Hospitals also provide access to multidisciplinary care, including pulmonologists, neurologists, and ENT specialists, ensuring comprehensive management of sleep apnea patients. Hospitals are often the preferred choice for patients with moderate to severe obstructive sleep apnea who require close monitoring during and after surgery due to associated comorbidities such as obesity, cardiovascular disorders, or diabetes. Reimbursement policies in several countries also favor procedures performed in hospital settings, driving patient inflow. In contrast, ASCs primarily handle less complex cases and face limitations in critical care infrastructure, which restricts their share. This makes hospitals the dominant end-user segment in 2024.

Sleep Apnea Implant Market Regional Analysis:

North America Dominated the Sleep Apnea Implants Market in 2024 due to excellent healthcare system and high rate of implant and medical device acceptance. The US and Canada lead the North American sleep apnea implant market due to their cutting-edge therapies. Advanced healthcare infrastructure, favorable reimbursement frameworks, and early adoption of innovative therapies. The region has a high prevalence of obstructive sleep apnea (OSA), with the American Academy of Sleep Medicine estimating that nearly 30 million adults in the U.S. suffer from this condition, creating a strong demand base for effective treatment solutions. Hypoglossal neurostimulation devices, particularly Inspire therapy, have gained significant traction across U.S. hospitals and specialized clinics as a proven alternative for patients who cannot tolerate CPAP therapy. Real-world adoption is evident as Inspire Medical Systems reported double-digit growth in implant procedures across leading healthcare centers such as Mayo Clinic and Cleveland Clinic.

Reimbursement coverage by Medicare and private insurers has boost accelerated patient acceptance, reducing the financial burden of implantation procedures. Additionally, increasing awareness campaigns and sleep disorder diagnosis programs in the U.S. and Canada have led to higher patient identification and treatment initiation. Hospitals in North America are well-equipped with skilled ENT surgeons and advanced diagnostic technologies, ensuring safe and efficient implant procedures. Furthermore, ongoing clinical trials and FDA approvals of new devices continue to strengthen the regional market. Compared to Europe or Asia-Pacific, the combination of strong clinical adoption, supportive healthcare policies, and patient preference positions North America as the leading hub for Sleep Apnea Implant demand in 2024.

Sleep Apnea Implants Market Competitive Analysis:

Sleep Apnea Implants Market is Competitive. Hypoglossal Nerve Stimulation (HGNS) continues to attract significant attention from medical device companies aiming to address obstructive Sleep Apnea (OSA). Nyxoah has reported promising results from its DREAM pivotal study in the United States, evaluating the Genio system a next-generation HGNS device that delivers bilateral stimulation and is powered by a wearable, non-implanted battery. The study demonstrated strong efficacy, particularly for patients who had not benefited from conventional therapies such as CPAP. LivaNova plc achieved a major milestone with its OSPREY clinical trial of the aura6000 HGNS system. The trial, targeting patients with moderate to severe OSA unable or unwilling to use positive airway pressure therapy, was concluded early due to a greater than 97.5% probability of meeting its primary endpoint, underscoring the system’s potential. Adding to market innovation, startup LunOSA, founded by former executives of Micro-Leads and StimWave, is developing a novel injectable HGNS device. Leveraging Micro-Leads’ paddle-lead technology, LunOSA plans to offer both battery-powered and batteryless options delivered via a 14-gauge percutaneous injector. These advancements illustrate a growing trend of innovation and diversification within the HGNS segment, highlighting opportunities for improved patient outcomes and expanding therapeutic options in the OSA treatment landscape.

Sleep Apnea Implant Market Key Trends:

1. Rising Adoption of Hypoglossal Nerve Stimulation (HGNS) Devices:

HGNS implants are gaining traction as an alternative for patients who struggle with Continuous Positive Airway Pressure (CPAP) therapy, which many find uncomfortable or inconvenient. These devices stimulate the hypoglossal nerve to maintain airway patency during sleep, reducing Apnea events. Clinical studies, such as the DREAM trial by Nyxoah, have demonstrated significant improvements in sleep quality and reduction in daytime sleepiness. Hospitals and sleep clinics increasingly recommend HGNS for moderate-to-severe obstructive sleep apnea (OSA), contributing to higher adoption rates. Market growth is further supported by patient preference for minimally invasive, implantable solutions over long-term CPAP use.

2. Integration of Advanced Wireless and Wearable Technologies:

Next-generation sleep apnea implants increasingly incorporate wireless and wearable technologies, allowing for real-time monitoring and remote therapy adjustments. Some systems eliminate the need for implanted batteries, using external wearable units instead. These innovations improve patient compliance by reducing discomfort, simplifying device management, and enabling healthcare providers to track treatment effectiveness continuously. Wearable integration also supports personalized therapy, as stimulation can be fine-tuned based on patient-specific sleep patterns. The convergence of implantable devices with digital health technologies is driving market growth, offering improved outcomes and convenience, particularly in technologically advanced regions such as North America and Europe.

Sleep Apnea Implant Market Key Development:

On August 2, 2024, Inspire Medical Systems received FDA approval for its next-generation Inspire V therapy system, designed for moderate to severe OSA patients intolerant to PAP therapy. The system features an updated neurostimulator, Bluetooth-enabled patient remote, and physician programmer. Inspire therapy, a surgical implant, keeps airways open, tracks sleep data via an app, and is slated for full launch in 2025.

On April 12, 2021, ZOLL Medical Corporation, an Asahi Kasei company, has acquired Respicardia, Inc., the developer of the remedē System, the only FDA-approved implantable neurostimulator for moderate to severe Central Sleep Apnea (CSA) in adults with reduced cardiac function. The system, implanted via a minimally invasive outpatient procedure, stimulates the phrenic nerve to normalize breathing patterns, improving sleep and overall health. The acquisition combines ZOLL’s cardiac and respiratory expertise with Respicardia’s innovative technology to enhance patient outcomes, with all Respicardia employees joining ZOLL while maintaining its Minnetonka, Minnesota headquarters. This moves targets over one million potential CSA patients in the U.S. alone.

On November 11, 2024, LivaNova announced that its OSPREY clinical trial for the aura6000 implantable hypoglossal neurostimulator met primary safety and efficacy endpoints in treating moderate to severe obstructive sleep apnea. At six months, median apnea-hypopnea index dropped 66.2% and oxygen desaturation index 63.3%. No serious device- or procedure-related adverse events were reported. The company plans to submit the data to the FDA and continue collecting 12-month long-term outcomes.

On July 2, 2024 Nyxoah submitted the fourth and final module of its Premarket Approval (PMA) application for the Genio system to the US FDA. Genio, a leadless, fully MRI-compatible HGNS device, uses a wearable, non-implanted battery that allows technology upgrades without surgery. Following positive DREAM US pivotal study results showing significant 12-month reductions in AHI and ODI, Nyxoah aims for a US launch by year-end 2024, with full data presentation planned at the International Surgical Sleep Society meeting.

Sleep Apnea Implants Market Scope: Inquire before buying

| Sleep Apnea Implants Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 553.41 Mn. |

| Forecast Period 2025 to 2032 CAGR: | 14.5% | Market Size in 2032: | USD 1643.76 Mn. |

| Segments Covered: | by Product | Hypoglossal neurostimulation devices Palatal implants Bone screw systems Phrenic nerve stimulators |

|

| by Indication Based | Central Sleep Apnea Obstructive Sleep Apnea |

||

| by End User | Hospitals Ambulatory surgical Centers Other end-users |

||

Sleep Apnea Implants Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Sleep Apnea Implants Market,Key Players are

North America

1. Inspire Medical Systems (USA)

2. Pillar Palatal LLC (USA)

3. Avery Biomedical Devices (USA)

4. Synapse Biomedical (USA)

5. Medtronic plc (USA)

6. LinguaFlex (USA)

7. Siesta Medical (USA)

8. Respicardia (Acquired by ZOLL Medical, USA)

9. Apnex Medical, Inc. (USA)

10. ReVENT Medical Inc. (USA)

11. Eunoia Medical (USA)

12. Boston Scientific Corporation (USA)

13. Asahi Kasei Corporation (USA)

Europe

14. LivaNova (UK/USA)

15. ImThera Medical (UK)

16. Koninklijke Philips N.V. (Netherlands)

17. Nyxoah (Belgium)

18. Aura MEDICAL (Aura6000) (UK)

Asia Pacific

19. SomnoMed Ltd. (Australia)

20. Invicta Medical, Inc. (Australia)

Sleep Apnea Implant Market Frequently Asked Questions

1. The End User of the Sleep Apnea Implant Market?

Ans: Hospitals, Ambulatory Surgical Centers and Office-Based Clinics are the End User of Sleep Apnea Implant Market.

2. What is the study period of this market?

Ans: The Global Market is studied from 2024 to 2032.

3.Sleep Apnea Implant Market Size?

Ans: The Global Sleep Apnea Implant Market size reached USD 553.41 Mn in 2024 and is expected to reach USD 1643.76 Mn by 2032, growing at a CAGR of 14.5% during the forecast period.

4. Which key trends are observed in the Sleep Apnea Market?

Ans: Advancements in Implant Technology, Function of AI in Sleep Apnea Management, Growing Need for Long-Term Remedies are the key trends observed in the Sleep Market.