Global Surrogacy Market Size by Type, Technology, Age Group, and Service Provider – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

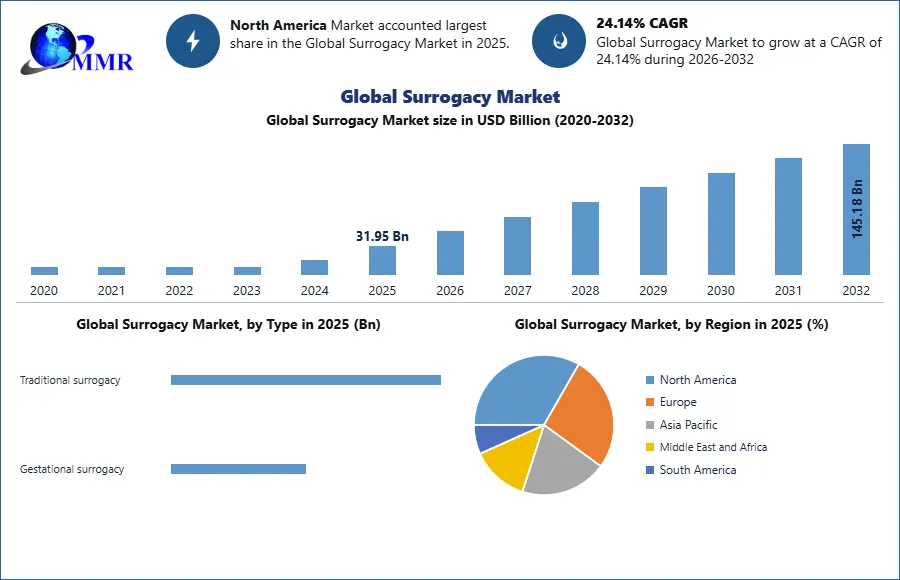

The Surrogacy Market size was valued at USD 31.95 Billion in 2025 and the total Surrogacy revenue is expected to grow at a CAGR of 24.14% from 2026 to 2032, reaching nearly USD 145.18 Billion.

Surrogacy Market Overview

Surrogacy is a reproductive arrangement in which a woman (the surrogate) carries and delivers a child on behalf of another person or couple, known as the intended parents. Surrogacy is typically used when the intended parents are unable to conceive or carry a pregnancy to term owing to various reasons, such as infertility, medical conditions, or other circumstances.

The surrogacy market has seen remarkable growth, driven by factors such as rising infertility rates, delayed pregnancies, and increasing acceptance of alternative reproductive technologies. The surrogacy market is particularly strong in countries with well-established fertility treatment industries, including the United States, India, and Canada. For instance, the U.S. surrogacy market is regulated at the state level, with California emerging as a leading hub, attracting both domestic and international clients due to its favorable legal framework. The rising accessibility of fertility treatments has led to more individuals, including same-sex couples and single parents, opting for surrogacy to build families, further boosting the surrogacy market.

Advancements in IVF technology and improved success rates have also enhanced the attractiveness of surrogacy as a viable option. Countries like India have become prominent global surrogacy destinations, offering cost-effective services. The surrogacy market faces ethical and legal challenges, including concerns about surrogate exploitation, which have created barriers in certain regions. In spite of these hurdles, the surrogacy market is poised for continued growth as demand rises globally and more countries introduce supportive regulations. As societal attitudes shift, surrogacy is expected to become an increasingly accepted and accessible method for family building, cementing its role in the reproductive healthcare sector.

• In the US, surrogacy success rates are roughly 75%. If the surrogate becomes pregnant, the success rate for having a healthy birth increases to as much as 95%. Medically speaking, those numbers are very similar around the world especially in developed countries like the UK.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Surrogacy Market Dynamics

Breaking Barriers in Parenthood: The Rise of Surrogacy and Its Global Impact

The surrogacy market has experienced significant growth, driven by rising infertility rates, changing societal norms, and increasing acceptance of diverse family structures. The demand from LGBTQ+ couples and single parents has surged, especially as global recognition of same-sex marriage grows. With infertility affecting an estimated 15% of couples worldwide, the surrogacy market has become a vital pathway for many seeking parenthood. Countries like the USA, Georgia, and Ukraine have become key players in the surrogacy market, offering structured programs with robust legal frameworks that attract international intended parents.

Meanwhile, more affordable options in Mexico and Colombia provide alternative solutions for those looking to manage costs. As major players like Circle Surrogacy, World Center of Baby, and Egg Donors Miracles expand their operations globally, they cater to the rising demand, particularly in light of regulatory shifts in markets like India and Ukraine. The growing awareness and acceptance of assisted reproductive technologies (ART) continue to propel the surrogacy market, shaping its role in global fertility solutions through a complex interplay of legal, ethical, and cost factors.

The Surrogacy Boom: Global Shift in Family Creation

Legal Status of Surrogacy by Country: Impact on Global Market Trends

The legal framework for surrogacy varies widely across countries, significantly influencing the surrogacy market dynamics. In regions like Australia, Canada, and the UK, only altruistic surrogacy is permitted, where compensation is limited to covering the surrogate's expenses. The restrictive approach contrasts with the surrogacy market in Ukraine and certain U.S. states, where both commercial and altruistic surrogacy are legally supported, making these areas prominent destinations for intended parents. India, Greece, and Israel allow surrogacy but impose strict medical and eligibility criteria, which limit access. In contrast, countries like Colombia and Kenya have minimal regulation, leading to uncertainty and a less formalized surrogacy market.

Mexico, having legalized surrogacy in 1992, has become a key destination for cross-border reproductive care, attracting international clients seeking more accessible options. Meanwhile, nations like Thailand have criminalized commercial surrogacy due to ethical and legal concerns, impacting the surrogacy market's appeal. The diversity in legal stances affects market growth, with more liberal regulations fostering international surrogacy tourism and drawing intended parents from countries with restrictive policies, thereby shaping global market trends.

Commercial and Altruistic Surrogacy: Legal Status in Major Countries

| Country | Commercial Surrogacy | Altruistic Surrogacy | Surrogacy Status |

| Australia | Prohibited | Allowed | Altruistic surrogacy is legal in all jurisdictions. Commercial surrogacy is a criminal offense. |

| Canada | Banned | Allowed | Only altruistic surrogacy is permitted. Compensation for gestational carriers is limited to approved expenses. |

| Colombia | Uncertain | Allowed | There are no clear rules, but altruistic surrogacy is performed and well tolerated. |

| Greece | Banned | Allowed | Heterosexual couples, single females allowed. |

| India | Prohibited | Allowed | Altruistic surrogacy is permitted for certain couples based on medical and age criteria. |

| Israel | Allowed | Allowed | Gestational surrogacy is legal under the Embryo Carrying Agreements Law |

| Kenya | N/A | N/A | No legal regulations/laws for surrogacy in Kenya. |

The Struggle for Global Market Growth Amidst Rising Regulations

The surrogacy market has been grappling with numerous challenges that have significantly impacted its growth. One of the major hurdles is the tightening of legal restrictions across various countries. Nations like India, Thailand, and Cambodia, which were once leading hubs for the surrogacy market due to their affordable services, have imposed bans or stringent regulations following media exposure of unethical practices and concerns about human trafficking. For instance, India's ban on foreign surrogacy, coupled with new restrictions on domestic surrogacy, has drastically limited access for international clients, resulting in a notable decline in market demand within the region.

Similarly, Italy’s recent legislation criminalizing international surrogacy for its citizens exemplifies the increasing regulatory pushback against the surrogacy market abroad. This shift not only discourages Italian citizens from seeking surrogacy services internationally but also forces agencies and clinics to navigate more complex legal environments. The fear of legal repercussions and the ambiguous legal status of surrogacy in various countries prompt intended parents to explore less regulated markets, which can reduce consumer confidence in the surrogacy market. The absence of uniform regulations and varying legal stances across countries have led to a fragmented surrogacy market, creating uncertainties that hinder expansion. These regulatory and ethical concerns directly impact market growth opportunities, increasing operational costs as clinics and agencies must adapt to evolving laws and mitigate legal risks.

Surrogacy Market Segment Analysis

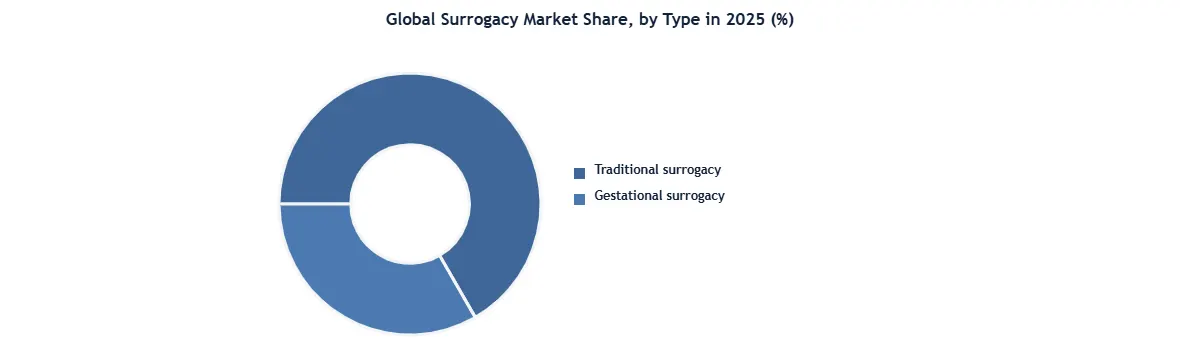

Based on Type, Surrogacy is available in two types, mainly gestational and traditional. Traditional surrogacy comprises the insemination of the surrogate naturally or artificially with the semen of the male partner of the childless couple. It has several ethical, social, and legal implications. On the other hand, in the case of gestational surrogacy, artificial reproduction techniques (ART) and an embryo from the eggs of the intended couple are formed in the test tube and transferred to the womb of the surrogate. The technological advancement in Artificial Reproductive Techniques (ART) is expected to boom in the field of surrogacy. Surrogacy is becoming a popular way for many couples in the limelight to have children.

Fertility clinics are increasingly adopting strategies like digital marketing to raise awareness about available infertility treatments, aiming to expand their customer base. The growing number of infertility cases has led to a surge in the establishment of fertility clinics and the demand for specialists, which in turn is fueling the growth of the surrogacy market. Many global surrogacy agencies have introduced measures such as requiring surrogate mothers to reside in dormitory-style housing throughout pregnancy. This approach ensures access to nutritious foods, clean drinking water, and high-quality antenatal care, ultimately improving the health outcomes for both the surrogate and the baby, thereby enhancing the overall success rates in the surrogacy market.

Based on Technology, the In-vitro Fertilization (IVF) segment dominated the Surrogacy market in the year 2025 and is expected to dominate the market during the forecast period. This dominance is underscored by comprehensive market segment analysis, revealing IVF as the preferred and prevailing technology for surrogacy services. The industry segmentation distinctly positions IVF as a cornerstone, reflecting the targeted market analysis that acknowledges its central role in addressing diverse consumer demographics. Intricately woven into the product segmentation, IVF stands out among other technologies such as Intrauterine Insemination (IUI), Classical/Standard IVF, Intracytoplasmic Sperm Injection (ICSI), and other alternatives. The geographic segmentation further accentuates the widespread adoption of IVF across various regions, reflecting its prevalence in market subsegments and niche markets.

The customer profiling within the Surrogacy Market is significantly influenced by the prominence of IVF, as it captures a substantial market share by segment. The segment growth analysis underscores the continuous expansion of IVF services, making it a driving force in the competitive segment landscape. Additionally, the attractiveness of IVF as a technology choice is evident in its behavioral segmentation impact, resonating with the preferences and choices of those seeking surrogacy services.

Surrogacy Market Region Analysis

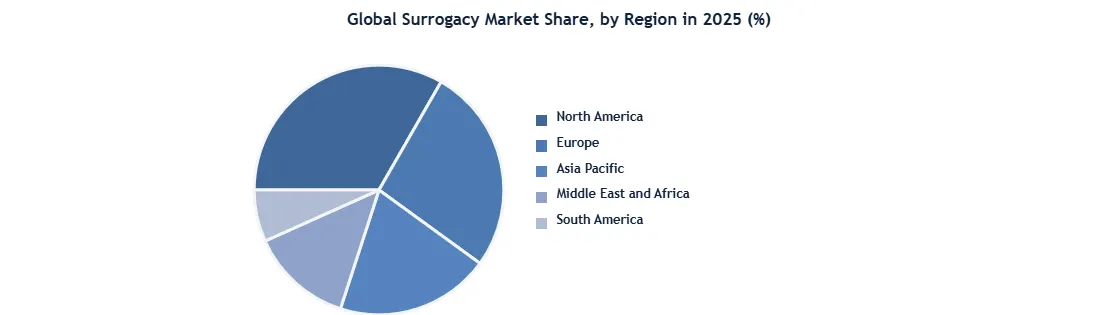

North America emerged as the dominant region in 2025 owing to its well-established legal frameworks, advanced medical infrastructure, and high demand for surrogacy services. The region's robust legal protections ensure a secure environment for intended parents and surrogate mothers, with clear contracts, medical insurance, and ethical guidelines.

The United States, emerges as the dominant region in the global surrogacy market, commanding the highest share as of 2025. This dominance is driven by a combination of favorable regulations, high demand, and a wealthy clientele. States like California, Illinois, and Nevada are at the forefront, offering well-regulated surrogacy arrangements with legal protections that attract both domestic and international intended parents. Leading surrogacy agencies such as Circle Surrogacy and Growing Generations have established strong reputations for providing comprehensive, ethically sound services, further cementing North America's position as a market leader.

Canada, while less commercially driven, also contributes to regional dominance with a focus on altruistic surrogacy. Most provinces have legal frameworks in place for surrogacy, although commercial arrangements are prohibited. This creates a niche for agencies that cater to domestic and international clients seeking ethical, non-commercial surrogacy options, often at a lower cost compared to the U.S.

The surrogacy markets in Europe and parts of Asia face significant regulatory restrictions, limiting their growth potential. For instance, countries like Italy have passed laws prohibiting citizens from seeking surrogacy abroad, further reducing the European market’s prominence. These regulatory barriers strengthen North America's leadership, as legal protections and infrastructure continue to shape the region's surrogacy market growth.

Surrogacy Market Competitive Analysis

The surrogacy market features key players like Ovation Fertility, US Fertility, and Circle Surrogacy, each offering distinct services to meet growing demand. Ovation Fertility stands out with its advanced IVF and genetic testing services, focusing on high-quality reproductive care. US Fertility, backed by Amulet Capital, leads with its extensive network of fertility centers and administrative support. Circle Surrogacy, known for its personalized services, offers international surrogacy options, setting itself apart in global markets. These industry leaders contribute to the surrogacy market’s expansion by improving patient access, clinical outcomes, and regulatory compliance, ensuring continued growth in reproductive healthcare.

• On April 3, 2023, Morgan Stanley Capital Partners (MSCP) announced the sale of Ovation Fertility to US Fertility (USF), with financial details undisclosed. Ovation, based in Nashville, Tennessee, offers IVF, genetic testing, and embryo storage, while USF, headquartered in Maryland, provides administrative and technical platforms to enhance fertility practices across the U.S. and internationally. The acquisition combines two complementary providers, aiming to improve clinical outcomes and expand patient access. This move reflects the ongoing consolidation trend in the fertility sector, positioning the combined entity as a leader in the U.S. market with enhanced patient care capabilities.

• On April 3, 2023, US Fertility (USF) and Ovation Fertility announced a definitive agreement to merge operations, creating a leading national fertility platform. USF, supported by Amulet Capital, manages over 120 physicians and performs more than 30,000 IVF cycles annually. Ovation, backed by Morgan Stanley Capital Partners since 2019, specializes in IVF and ancillary services like genetic testing and surrogacy. The merger combines complementary strengths, aiming to enhance patient outcomes, increase access, and drive innovation in fertility care.

Surrogacy Market Recent Development

Surrogacy Market Scope: Inquire before buying

| Global Surrogacy Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 31.95 USD Billion |

| Forecast Period 2026-2032 CAGR: | 24.14% | Market Size in 2032: | 145.18 USD Billion |

| Segments Covered: | by Type | Traditional surrogacy Gestational surrogacy |

|

| By Technology | Intrauterine insemination (IUI) In-vitro fertilization (IVF) Classical/standard IVF Intracytoplasmic sperm injection (ICSI) Others |

||

| By Age Group | Below 35 years 35-37 years 38 - 39 years 40-42 years 43-44 years Over 44 years |

||

| By Service Provider | Hospitals Fertility clinics Others |

||

Surrogacy Market, by Region

North America (United States, Canada, Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (India, China, Japan, South Korea, Australia, ASEAN, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME & A)

South America (Brazil, Argentina, Columbia, and Rest of South America)

Surrogacy Market, Key Players are:

1. New Hope Fertility Center

2. IVI-RMA Global

3. Ovation Fertility

4. Growing Generations, LLC

5. Bourn Hall Fertility Clinic

6. Merck KGaA

7. Morpheus Life Sciences Pvt. Ltd.

8. American Surrogacy.

9. United Fertility.

10. Growing Generations.

11. Circle Surrogacy.

12. Surrogate Solutions.

13. ConceiveAbilities.

14. SurroGenesis.

15. Extraordinary Conceptions

16. Fertility Connections

17. World Center of Baby

18. Global Surrogacy Services

19. Simple Surrogacy

20. Creative Family Connections

21. The Surrogacy Group

22. Canadian Surrogacy Options

23. New Life Global Network

24. Elite IVF

Others