Semiconductor Glass Market Size by Type, Application, Category, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2030

Overview

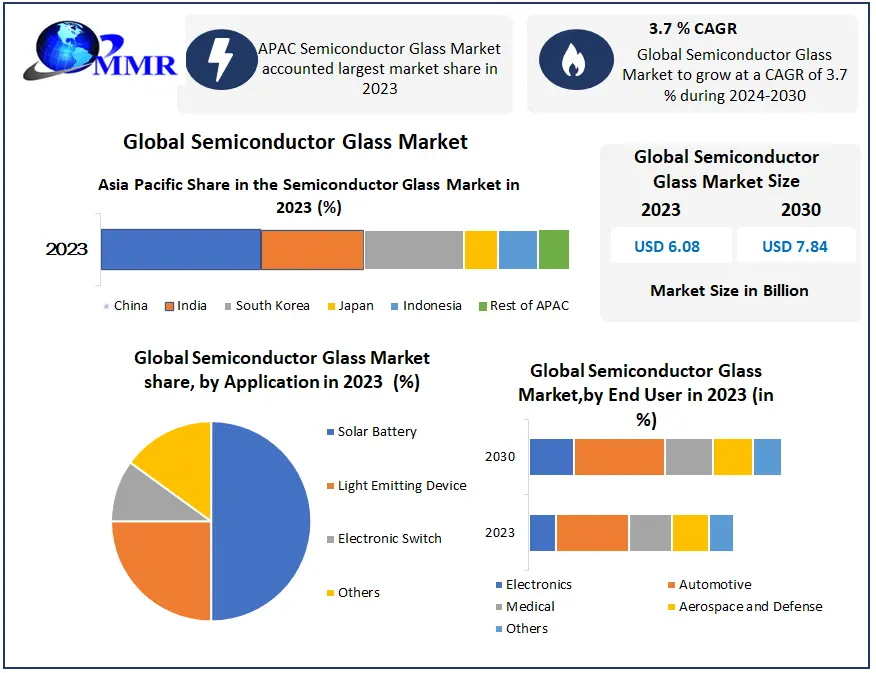

Global Semiconductor Glass Market size was valued at USD 6.08 Bn in 2023 and is expected to reach USD 7.84 Bn by 2030, at a CAGR of 3.7 %.

Overview

Semiconductors, solid chemical substances capable of both absorbing light and conducting electricity under specific conditions, serve as vital regulators of electronic signals. The movement of electrons and the molecules within semiconductors exhibit reverse directionality. Semiconductor glass, characterized by its low electrical consumption and extended lifespan, occupies a niche between conductors and insulators due to its moderate conductivity. The semiconductor glass has remarkable flexibility and maintains high thermoelectric efficiency at room temperature. The market for semiconductor glass has increased due to the growth of the electronics sector. An increase in the manufacture of semiconductors, display devices and electronic components, is expected to drive growth in the semiconductor glass market for the electronics industry.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Semiconductor Glass Market Dynamics: Drivers, Restraints, Opportunities and Trends

Technological Advancements in Semiconductor Glass to Drive the Market Growth

Semiconductors have become an indispensable feature of comfortable daily life. Semiconductor Glass manufacturers face several issues as circuit patterns have become increasingly miniaturized as semiconductor device performance continues to advance. These trends have presented the opportunity for Central Glass to combine its long-cultivated technologies in glassmaking and chemical production to deal with the problem of circuit pattern collapse in the drying process after deionized water rinsing of the wafer.

Continuous advancements in semiconductor manufacturing processes require high-quality glass materials for various applications such as photomasks, wafer carriers, and substrates. The development of advanced glass compositions with superior optical and thermal properties, along with precise dimensional control, enables semiconductor manufacturers to achieve higher yields and performance in their devices. innovations in glass fabrication techniques, such as precision machining and chemical strengthening, further enhance the suitability of glass for demanding semiconductor applications are drive the Semiconductor Glass Market growth.

For instance, AGC Asahi Glass (AGC) has developed a diverse line of glass substrates specifically designed for semiconductor packaging applications and semiconductor manufacturing process support. The company is demonstrating the new substrates at NEPCON JAPAN 2017, opening today in Tokyo. AGC's exhibit can be found at booth W3-6 in the West Hall (1F). Key advanced packaging technologies are poised to benefit from AGC products. Wafer-level packaging (WLP) technology – in which the IC is packaged while still part of the wafer – has made remarkable progress with next-generation semiconductor and MEMS devices. This has resulted in a growing need for glass wafers – in particular, those that match silicon's coefficient of thermal expansion (CTE), thus eliminating the warping that occurs when attempting to directly laminate silicon and glass wafers whose CTE values differ. Another target technology for the new substrates is fan-out wafer-level packaging (FOWLP), which enhances standard WLP technology to provide a smaller package footprint with improved thermal and electrical performance. It involves joining materials with different CTEs, including silicon wafers, rewiring layers and resin. Such innovation by semiconductor glass companies is driving market growth.

As consumer demand for high-resolution displays, flexible screens, and augmented reality experiences escalates, the need for advanced semiconductor glass materials intensifies. This presents a ripe opportunity for market players to invest in research and development, creating novel glass compositions tailored to the specific requirements of emerging display technologies. For instance, the demand for bendable displays in smartphones and wearable devices necessitates the development of flexible and durable semiconductor glass formulations. Additionally, the proliferation of augmented reality (AR) and virtual reality (VR) applications demands high-transparency glass with exceptional optical properties to deliver immersive user experiences. Capitalizing on these evolving demands by offering innovative semiconductor glass solutions positions companies at the forefront of this burgeoning Semiconductor Glass Market.

Increasing Demand for Consumer Electronics to Influence the Market

Consumer electronics sales: During the pandemic, computer and TV sets outgrew smartphones Across the consumer electronics sales categories, computers (+34%) and TV sets (+12%) have grown much faster than smartphones (+1%) in the past three years globally, likely due to COVID-19 restrictions and more time spent working and learning from home. As a result, smartphones’ share of combined sales dollars for the three device categories has fallen from 65% to 60%. The proliferation of smartphones, tablets, laptops, and other electronic devices fuels the demand for semiconductor components, driving the semiconductor glass market. Glass substrates are essential for manufacturing integrated circuits (ICs), flat panel displays, and optoelectronic devices used in these electronics. As consumer preferences shift towards sleeker designs and higher display resolutions, the demand for specialty glass with exceptional clarity, flatness, and durability continues to rise, further boosting the semiconductor glass Industry.

Table: Active Smartphone Users by Countries in 2022-23

| Country | Smartphone Users | Smartphone Penetration |

| China | 974.69 million | 68.4% |

| India | 659 million | 46.5% |

| United States | 276.14 million | 81.6% |

| Indonesia | 187.7 million | 68.1% |

| Brazil | 143.43 million | 66.6% |

| Russia | 106.44 million | 73.6% |

| Japan | 97.44 million | 78.6% |

| Nigeria | 83.34 million | 38.1% |

| Mexico | 78.37 million | 61.5% |

| Pakistan | 72.99 million | 31% |

Growing Demand for Electric Vehicles to Create Lucrative Opportunity for Market Growth

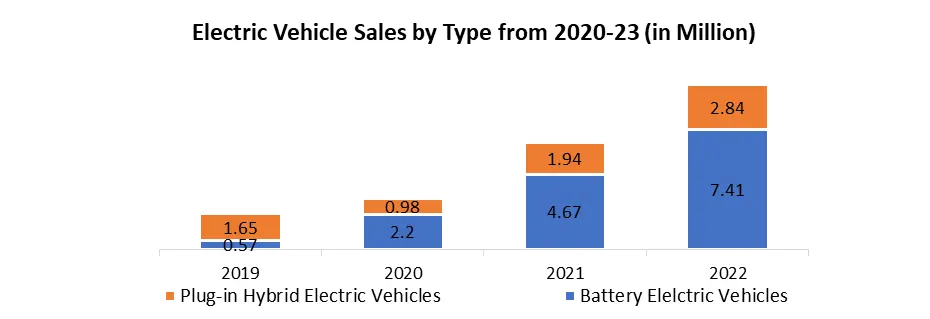

The surge in electric vehicle (EV) adoption globally presents a lucrative opportunity for the Semiconductor Glass Market. As automotive manufacturers transition from internal combustion engines to electric powertrains, the demand for semiconductor components such as power electronics and sensors is poised to escalate. Semiconductor glass, known for its thermal and electrical properties, plays a crucial role in encapsulating and protecting these sensitive electronic components in automotive applications. Also, the trend towards autonomous driving and connected vehicles further amplifies the need for advanced semiconductor glass solutions to ensure the reliability and performance of onboard electronics. By catering to the burgeoning EV market with specialized glass formulations optimized for automotive applications, companies can capitalize on this growing opportunity and establish a strong foothold in the automotive semiconductor sector.

The manufacture of hybrid and electric vehicles is advancing due to a focus on pollution control and strict environmental restrictions, which is encouraging the Semiconductor Glass Market growth in the Automotive sector. To comply with government regulations, consumers and manufacturers are forecasted to seek more environmentally friendly automobiles, putting a value on hybrid and electric vehicles, which are driving the market. In US the EV sales skyrocketed 81% in the latest month, while hybrid sales were up 32%. However, the vast majority of Ford's sales nearly 90% continued to be from traditional internal combustion engine vehicles. Hybrid vehicles continue to be a growth segment for Ford and sales have grown at a faster rate than the overall U.S. industry for much of the last year.

Global EV sales continued as expected by us at the beginning of 2023. A total of 14,2 million new Battery Electric Vehicles (BEV) and Plug-in Hybrids (PHEV) were delivered during 2023, an increase of +35 %. 10 million were pure electric BEVs and 4,2 million were Plug-in Hybrids (PHEV) and Range Extender EVs (EREV). China is, by far, the largest EV market with 8,4 million units in 2023 and 59 % of global EV sales. With 9,3 million EVs made, China's role as the largest EV production base is even stronger: 65 % of global EV sales in 2023 came out of China. 900 000 EVs were exported from China, most of them (530k) by Western brands. The largest exporters were Tesla, SAIC (MG, Maxus), Geely (Volvo, Polestar, Lynk, Smart) BYD, Renault (Dacia), BMW and Great Wall. As a result, these factors are expected to boost the Semiconductor Glass Market growth.

Glass offers numerous advantages in semiconductor applications due to its transparency, thermal stability, and low electrical loss. Borosilicate, Corning Eagle XG, Schott BOROFLOAT, and quartz/fused silica are commonly used materials. Borosilicate provides exceptional thermal stability, while Corning Eagle XG offers a coefficient of expansion similar to silicon. Schott BOROFLOAT combines toughness and chemical resistance, while quartz/fused silica withstands high temperatures and pressure.

For instance, Swift Glass specializes in the custom fabrication of precision glass wafers tailored to semiconductor industry requirements. These wafers, crafted from fused silica, quartz, or borosilicate glass, serve as carriers for MEMs substrates like silicon, offering versatility for temporary or permanent semiconductor applications. Their prototype and production shop ensure scalability from small to large runs, utilizing advanced cutting systems to achieve thicknesses as low as 0.3 mm.

Supply Chain Distribution to Restrain the Market

The semiconductor glass market faces restraining factors due to its dependence on complex and fragile supply chains. These supply chains involve intricate processes for sourcing raw materials, manufacturing, and distribution, often spanning multiple countries. Any disruption in these supply chains, such as natural disasters, geopolitical tensions, or pandemics, can significantly impact the availability and cost of semiconductor glass.

For instance, a shortage of critical raw materials or disruptions in manufacturing facilities can lead to delays in production and increased costs for semiconductor glass manufacturers. Moreover, the reliance on international trade exposes the market to risks associated with tariffs, trade disputes, and logistic challenges, further exacerbating supply chain vulnerabilities. The semiconductor glass companies must invest in diversifying their supply chains, enhancing resilience, and developing contingency plans to mitigate these risks and ensure stable operations in the face of external disruptions. The COVID-19 pandemic has exacerbated this problem, leading to disruptions in the supply of raw materials for industries. Such shortages significantly impact production processes, causing delays, increased costs, and ultimately affecting firms' operating performance.

Semiconductor Glass Market Segment Analysis

By Application

Based on application, the Semiconductor Glass Market is segmented into solar batteries, light-emitting devices, electronic switches, and other uses. In 2023, the solar batteries semiconductor glass segment dominated the largest market share. Semi-transparent solar panels are a specific type of transparent solar panels that have a light transmittance below 100%. The main goal of Solar Cell Cover Glasses in solar batteries is to offer effective protection for space and terrestrial photovoltaics. As the world increases its reliance on solar power to generate electricity, the use of photovoltaics is becoming more widespread not only on Earth but in space. The prevalence of silicon solar panels has led to the emergence of affordable energy generators with the ability to convert more than 20% of the sunlight into electricity for different purposes. Also, the semiconductor materials such as glass have been shown to function efficiently and are considered stable, they are regarded as costly and, not economical which is a critical factor in the solar panel design industry. This disadvantage causes the recently designed solar panel to be composed entirely of the combination of these two materials which is particularly not reasonable for mass production at the moment. All factors are driving the segment growth over the forecast period.

By End User

Based on end users, the automotive segment held the largest Semiconductor Glass Market share in 2023. In the automotive industry, glass applications are diverse. Headlights utilize krypton, xenon, and neon for high-performance lighting, while taillights incorporate similar gases. Windows benefit from nitrogen and hydrogen during manufacturing, ensuring clarity and strength. Windshields, made of safety glass with a plastic layer, use nitrogen to bond layers securely, preventing sharp glass shards in accidents. This industry relies on inert gases for safety and efficiency in various production processes. Semiconductor glass is integral to automotive electronics, powering engine control units, safety systems like ADAS, and infotainment displays. These glass components enhance vehicle safety, efficiency, and performance, enabling features such as collision avoidance and advanced driver assistance. They also facilitate precise control of engine parameters for optimized fuel economy and emissions. Semiconductor glass technology continues to drive innovation in the automotive industry, shaping the future of vehicle design and functionality. However, the Electronics Semiconductor Glass segment is expected to grow at a significant CAGR over the forecast period. This is due to the increasing adoption of consumer electronics across the world is the primary factor that boosts Market growth.

Semiconductor Glass Market Regional Analysis

Asia Pacific held the largest Semiconductor Glass Market share in 2023 in terms of Semiconductor Glass production and consumption. The market growth is primarily driven by this region is a big gateway for multiple manufacturers of OEMs and the presence of a prospective economy such as China, South Korea, Japan, and India. China is the largest semiconductor market, accounting for 25% of global consumption and this is the key factor behind the Semiconductor Glass Industry growth. government rules and regulations support regional market growth. for example, Development of “game-changing” future semiconductor technologies. For this purpose, Japan is establishing the LSTC, a government-supported R&D center for advanced chip research. The idea for the LSTC reportedly arose out of the U.S.-Japan discussions that led to the adoption of the Basic Principles. IBM will support the establishment and work of the LSTC. The world imports most of its semiconductors from China, Vietnam and Germany. The top 3 Semiconductor Glass importers are Vietnam with 669,070 shipments followed by India with 128,323 and Germany at the 3rd spot with 105,151 shipments. Top or leading players in Asia Pacific's semiconductor glass industry include AGC Inc., Corning Incorporated, Samsung Corning Precision Materials Co., Ltd., Shin-Etsu Chemical Co., Ltd., Hoya Corporation, and Ohara Corporation. AGC and Corning lead with diverse glass technologies. Samsung Corning is a joint venture specializing in glass substrates. Shin-Etsu and Hoya provide specialty glass, while Ohara focuses on optical glass. These companies collectively drive innovation and supply essential materials for semiconductor manufacturing.

With second largest Semiconductor Glass Market share, North America is expected to become the most competitive market. As a result, demand for semiconductor glass in North America is projected to experience solid microchip consumption of different smart electronics applications, thus generating better prospects for glass manufacturers over the forecast period.

Europe holds a prominent market share due to increasing demand for renewable energy sources like wind, hydroelectricity, and solar power, requiring semiconductor chips that push consumer demand. It is expected that Brazil and Mexico will continue to expand due to growing demand and technology growth for advanced electronics, which in turn boosts the market growth in Latin America. Middle East and Africa are witnessing relatively slow growth as a result of the impact of tight regulations by the governments slowing down Semiconductor Glass Market growth

Semiconductor Glass Market Scope: Inquire Before Buying

| Global Semiconductor Glass Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 6.08 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 3.7% | Market Size in 2030: | US $ 7.84 Bn. |

| Segments Covered: | by Type | Borosilicate Based Silicon Based Ceramic Based Silica/Quartz Based Others |

|

| by Application | Solar Battery Light Emitting Device Electronic Switch Others |

||

| by Category | Electronics Automotive Medical Aerospace and Defense Others |

||

Semiconductor Glass Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Semiconductor Glass Key players

North America Semiconductor Glass Leading Players

1. Corning Incorporated (USA)

2. Rubicon Technology, Inc. (USA)

3. Wafer World, Inc. (USA)

4. II-VI Optical Systems (USA)

5. IDEX Health & Science LLC (USA)

6. Dynasil Corporation of America (USA)

7. GT Advanced Technologies (USA)

8. Edmund Optics (USA)

Europe Semiconductor Glass Manufacturers

9. SCHOTT AG (Germany)

10. Plan Optik AG (Germany)

11. SwissOptic AG (Switzerland)

12. Saint-Gobain (France)

13. Heraeus Holding GmbH (Germany)

14. Others

APAC Semiconductor Glass Companies

15. Shin-Etsu Chemical Co., Ltd. (Japan)

16. AGC Inc. (formerly known as Asahi Glass Co., Ltd.) (Japan)

17. Nippon Electric Glass Co., Ltd. (NEG) (Japan)

18. OHARA Inc. (Japan)

19. Tosoh Corporation (Japan)

20. Silitech Technology Corporation (Taiwan)

Frequently Asked Questions:

1] What is the growth rate of the Global Semiconductor Glass Market?

Ans. The Global Semiconductor Glass Market is growing at a significant rate of 3.7 % during the forecast period.

2] Which region is expected to dominate the Global Semiconductor Glass Market?

Ans. APAC is expected to dominate the Semiconductor Glass Market during the forecast period.

3] What is the expected Global Semiconductor Glass Market size by 2030?

Ans. The Semiconductor Glass Market size is expected to reach USD 7.84 Bn by 2030.

4] What are the Opportunities in the Global Semiconductor Glass Market?

Ans. With the proliferation of smartphones, tablets, wearables, and other electronic devices, there's a growing need for high-performance semiconductor components. Semiconductor glass is used in various electronic applications such as displays, sensors, and optoelectronic devices, thus fueling market growth.

5] What are the factors driving the Global Semiconductor Glass Market growth?

Ans. With the rise in consumer electronics such as smartphones, tablets, laptops, and wearables, there's a growing demand for semiconductors, which in turn boosts the demand for semiconductor glass used in their manufacturing.

6] What are the factors restraining factors the Global Semiconductor Glass Market growth?

Ans. The semiconductor industry heavily relies on complex supply chains. Disruptions in the supply chain, such as shortages of raw materials or components, can hinder production and limit market growth.