Seafood Market by Product Type, Form, Distribution Channel, End User and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

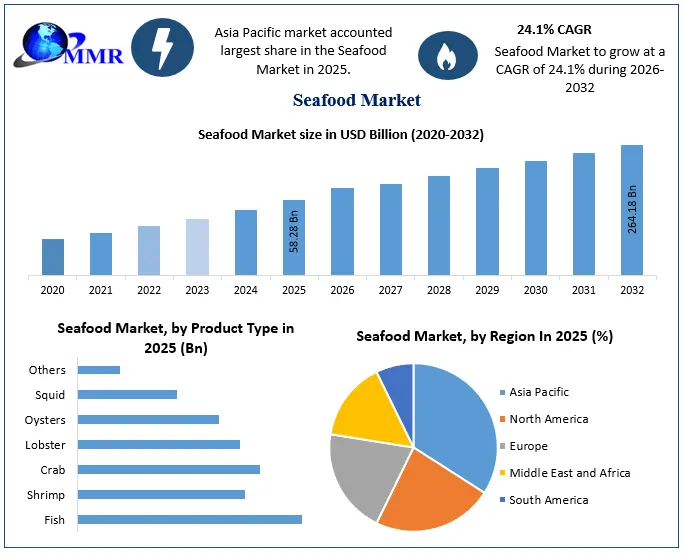

The Seafood market size was valued at USD 58.28 Billion in 2025 and the total Seafood market size is expected to grow at a CAGR of 24.1% from 2026 to 2032, reaching nearly USD 264.18 Billion by 2032.

Seafood market Overview:

The seafood market growth is fueled by its exceptional health properties, including healing cardiovascular health through the intake of omega-3 fatty acids. These are essential nutrients, which greatly assist in the stabilization of blood pressure, reduction of triglycerides, and prevention of blood clots. This makes seafood first choice for heart health. The trend of sustainability is one the rise as the principal influence on how the seafood market operates. Responsible fishing and concerns over overfishing and environmental damage has led to a market demand for well sourced seafood. Those producers, who prioritize sustainable fish farming like Cermaq Group AS, are rising and positioning themselves as flagships of consumer values. The big ones like Thai Union Group PCL., Maruha Nichiro Corporation, Mowi, and Nissui are essentially engaged in sustainable initiatives and thus pushing towards a greenish industry.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The seafood market, on the other hand, encounters challenges, that is the development of online seafood market and e-commerce. While these platforms expand the range of access and choices for consumers, perishable goods face the problem of delivery. Companies will need to devise robust supply chain models which provide the customer with the freshest seafood, maximizing convenience while providing quality. Environmental factors exert a huge influence on the market and affect how species are available depending on temperature changes, shifts in ocean currents, or marine ecosystems. Being up to the task of accommodating these changes is fundamental for the uninterrupted supply and sustainability of these services.

The health benefits and eco-friendly efforts make seafood the leader in the growth of industry due to the global efforts of wellness. In spite of these problems like overfishing, climate change, and growth of plant based substitutes, the strategic criteria are still helpful for steady development and adaptation. In addition, the location-specific analysis illustrates the various trends, specifically, with health consciousness leading in North America, and with sustainability taking center stage in Europe, and Asia Pacific region dominating the global seafood industry. Despite the challenges, the seafood market's growth prospects are still quite promising, provided the businesses have the appropriate strategic reaction to the new trends and challenges.

Seafood Market Dynamics

Seafood's health benefits have been a major driver in the seafood market's growth. The contribution of omega-3 fatty acids in cardiovascular health constitutes a powerful factor determining the buyer’s opinion. Omega-3 fatty acids, the main component of seafood lowers the risk of cardiovascular diseases by stabilizing blood pressure, decreasing triglycerides and preventing blood clots, gives an. extremely valuable role of seafood as a perfect complement to heart health. With the increasing awareness of cardiovascular diseases across the globe is resulting in people incorporating seafood into their food regimen and thereby making progress towards a healthier lifestyle. Additionally, fish nutrition for brain function makes it a palatable food choice, among other things, due to the influence of seafood on cognitive function.

The increasing trend of sustainability in seafood is another factor impacting the seafood market dynamics. Consumers concerns linked to overfishing, impact not only the seafood production but also the businesses that are not adhering to responsible sourcing and sustainable fishing practices. Such companies are likely to get outpaced as opposed to companies who are following the visionary goal of preserving the environment such as Cermaq Group AS, who assumes the responsibility of sustainable fishing. Their goal is to not just profitable business but also meeting ambitious climate change targets and local sustainability requirements. Other major players taking part in the sustainability drive include Thai Union Group PCL., Cooke Aquaculture, Tri Marine and Nissui to name a few.

While the market demonstrates optimism given the outlined trends in the Seafood Market, it still experiences inevitable challenges that call for smart considerations. The development of e-commerce and the growing number of online seafood platforms is one of them. While such platforms lead to improved accessibility and selection for consumers, it also poses challenges with regards to the distribution of the perishable goods. Companies have to design their business models such that there is a robust supply chain ensuring the freshest fish to their consumers. The environment where fish live has more impact on the way of Seafood Market conduct. The rising of sea temperatures and changes in ocean currents and marine ecosystem components results in shortages in the wild-caught and farmed populations of various species. Modifying the current situation, which keeps on the impact of environmental change is a key activity in ensuring the continuous availability and sustainability of seafood products.

The environment where fish live has more impact on the way of Seafood Market conduct. The rising of sea temperatures and changes in ocean currents and marine ecosystem components results in shortages in the wild-caught and farmed populations of various species. Modifying the current situation, which keeps on the impact of environmental change is a key activity in ensuring the continuous availability and sustainability of seafood products.

Developments as such take us to safety and health issue which are becoming the impediment of continued market growth. Issues like poisoning, contamination of mercury and microplastics in some seafood varieties are surfacing which is expected to affect consumer preferences in the Seafood Market. Safety of seafood products must be guaranteed and communicated to consumers which require labels to be transparent, quality food control to be rigorous and the standards of food safety to be met.

The health advantages of seafood stand out as a strong boost for seafood market growth thanks to its omega-3 fatty acid, rich nutrient and harmonizing trends in global wellness. With a rise in the number of consumers, who put holistic wellbeing and healthy dietary options at a center of their eating habits, demand for seafood as a natural and nutritious source is bound to result in the rapid growth of the Seafood Industry.

All in all, the seafood is being positively influenced by health and wellness trends, but there are obstacles such as overfishing, climate change, and becoming of plant-based alternatives; therefore, the growth and adaptation inside the industry demand cautious strategies. The ever-changing environment demands a multi-faceted strategy to maintain food supply market stability and adaptation to challenges and resources emerging at the same time in competitive and adventurous conditions.

Seafood market Segment Analysis

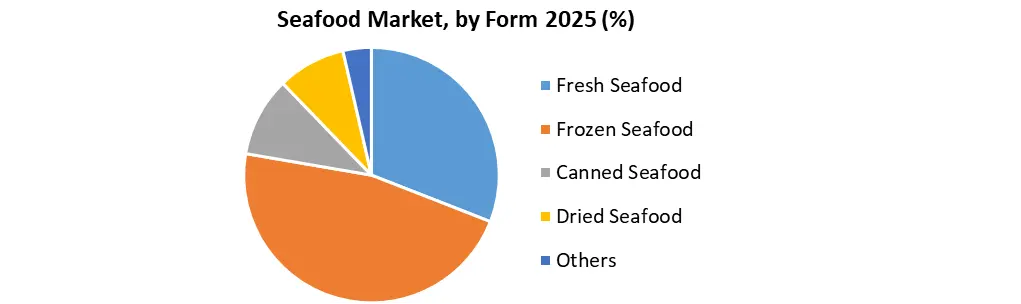

By Form, The seafood market by form is led by frozen seafood, which accounts for over 35% of the market share. Its dominance is driven by extended shelf life, global export feasibility, and widespread use in retail and foodservice sectors. Advanced freezing technologies and improved cold chain infrastructure have further boosted consumer trust in frozen options, particularly in urban and inland areas. Fresh seafood ranks second, largely popular in coastal regions with direct access to fisheries and efficient logistics. The segment benefits from growing consumer preference for minimally processed, locally sourced products.

Canned seafood remains resilient due to its affordability, long storage capability, and convenience, especially in developing markets. Dried seafood holds niche appeal in traditional Asian cuisines and health-focused consumer groups seeking high-protein, low-fat snacks. Other forms, including marinated or precooked options, are slowly growing, aligned with ready-to-eat trends. Overall, form selection is influenced by lifestyle changes, perishability management, and evolving dietary patterns.

By Product Type, Among seafood product types, fish dominates with more than 50% market share, led by high consumption of salmon, tuna, cod, and tilapia. This is supported by both wild capture fisheries and aquaculture growth, particularly in Asia-Pacific and Europe. Shrimp follows as a high-value commodity, benefiting from intensive farming practices, especially in India, Vietnam, and Ecuador, and strong export demand from the U.S. and China. Crabs and lobsters cater to the premium and festive food segments, exhibiting seasonal consumption peaks and strong performance in hotel and fine dining sectors. Oysters and squid show moderate growth, driven by health trends and culinary diversification.

Innovations in sustainable harvesting, traceability, and eco-labeling are shaping product preference among eco-conscious consumers. Diversification in species availability and culinary formats is also expanding the Other Product Types, with new entries such as sea urchin and cuttlefish gaining niche popularity.

By Distribution Channel, Supermarkets and hypermarkets are the primary distribution channels, accounting for nearly 40% of seafood sales, due to their wide assortment, competitive pricing, and established supply networks. Their growth is bolstered by in-store seafood counters, value-added offerings, and robust inventory management. Specialty stores and fishmongers come next, offering curated selections and fresher stock, which appeals to discerning buyers focused on quality and sustainability. These stores often emphasize local sourcing, seasonal availability, and expert recommendations, making them influential in premium segments. Online retail is the fastest-growing channel, supported by rising digital adoption, cold-chain-enabled e-commerce, and contactless delivery models. Consumers value the convenience, variety, and access to origin information provided by online platforms. Convenience stores and other smaller outlets cater to quick-purchase needs but hold a relatively modest share. Across all channels, consumer awareness of eco-certification, packaging innovation, and traceable sourcing is increasingly shaping buying decisions.

Seafood Market Recent Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2026 | SalMar ASA | The company agreed to acquire the remaining 49% stake in Norwegian salmon-farming company Oylaks for NOK 137.2 million via share issuance. | This transaction grants SalMar 100% full control over Oylaks, advancing its strategy to consolidate the aquaculture sector and bolster its position as a global leader in salmon production volume. |

| 30 June 2025 | High Liner Foods Incorporated | The company successfully finalized the acquisition of the iconic premium U.S. frozen seafood brands Mrs. Paul’s and Van de Kamp’s from Conagra Brands, Inc. for an adjusted purchase price of USD 42.4 million. | This acquisition expands High Liner Foods' direct brand portfolio in the U.S. retail market, driving incremental commercial volume, vertical integration margins, and cross-selling scale. |

| 17 June 2025 | Yumbah Aquaculture Ltd | The company amended its Scheme Implementation Deed to acquire all outstanding ordinary shares on issue of Australian premium finfish producer Clean Seas Seafood Limited. | This consolidation builds an extensive diversified aquaculture network, strengthening market capability for high-quality, traceable marine proteins in global export markets. |

| 18 March 2025 | Silver Bay Seafoods | The company formed a joint venture partnership with the Bristol Bay Economic Development Corporation to acquire a controlling equity interest in OBI Seafoods. | This acquisition transfers management of multiple processing facilities, thereby enhancing economic stability for wild-caught salmon, whitefish, and crab processing across Alaska. |

Seafood market Regional Analysis:

The Asia-Pacific region continues to dominate the global seafood market, driven by robust aquaculture practices, rising per capita seafood consumption, and the integral role of seafood in regional cuisines. Countries such as Japan, Thailand, and China showcase the diversity of seafood through vibrant wholesale fish markets, street food culture, and extensive marine biodiversity. The region has seen surging demand for shellfish, including shrimp, prawns, and crabs, propelled by culinary versatility and increasing preference for high-protein diets.

Notably, innovative aquaculture systems like integrated multi-trophic aquaculture (IMTA) and recirculating aquaculture systems (RAS) are gaining traction to ensure sustainable fish farming. Consumer preference for live and freshly prepared seafood, along with the expansion of immersive seafood dining experiences, underscores a regional emphasis on freshness and quality. Technological integration in seafood processing and sustainable harvesting methods strengthens Asia-Pacific’s position as a trendsetter in the global seafood industry.

In Europe, the seafood market is shaped by a deep cultural heritage and emphasis on sustainable fisheries management. European consumers are increasingly demanding eco-labeled seafood certified by standards such as Marine Stewardship Council (MSC) and Aquaculture Stewardship Council (ASC). Mediterranean and Nordic seafood traditions, including Scandinavian pickled herring and Mediterranean anchovies, are seeing renewed popularity due to social media influence and rising interest in health-conscious diets. The region also witnesses growth in value-added seafood products and ready-to-eat formats, supported by technological advancements in processing and packaging.

The North American seafood market is characterized by high demand for premium, sustainably-sourced seafood, driven by consumer focus on nutrition, transparency, and traceability. Salmon, especially omega-3 rich varieties, remains a staple, while demand for locally-sourced crab and shrimp continues to rise. The market is also benefitting from the expansion of convenient seafood offerings, including frozen, pre-cooked, and ready-to-eat meals, aligning with busy urban lifestyles. There's also growing interest in aquaponics and traceable seafood supply chains to ensure product authenticity and environmental responsibility.

In conclusion, the seafood market is undergoing significant transformation. A data-driven approach to consumer demographics, sustainability credentials, and regional market dynamics is essential for businesses aiming to stay competitive. Understanding evolving trends such as blue economy initiatives, smart fisheries, and alternative seafood proteins will enable companies to innovate and capture untapped market potential. The interplay between tradition and technology is shaping a modern, sustainable, and globally interconnected seafood ecosystem.

Seafood market Competitive Landscape

The market is a highly competitive global sector with many participants striving to be leaders. In the global seafood market, Maruha Nichiro Corporation is among the major companies known for its wide variety of products and strong distribution system. The company's dedication to quality control, fresh ideas in new products and concern about sustainability are all elements that emphasize it as an important player in Seafood Market. This company pays attention to quality control procedures along its supply chain, as well as creating new products that match with changes in tastes and preferences among consumers globally. They also recognize the importance of sustainability issues are in this sector. The concept of cell-cultivated seafood is a very promising field in the future food industry, showing great potential for growth. This method offers an environmentally friendly answer to lessen pressure on wild fish stocks while still satisfying the rising need from customers who are mindful about their health and seek options other than regular protein providers such as meat or fish caught in oceans (UMAMI Bioworks Teams Up With Maruha Nichiro For Cell-Cultivated Seafood).

Moreover, Mowi is a well-known seafood company with its main office in Bergen, Norway. It exhibits commitment towards sustainability by adhering to particular strategic measures highlighted within the biodiversity framework. The sustainability programs of Mowi encompass various aspects such as climate, pollution and fresh water care among others. They also involve actions for social responsibility that resemble international norms such as Global Reporting Initiative (GRI) and Taskforce on Climate-related Financial Disclosures (TCFD) framework. By using this way of tracking progress along with revealing risks and opportunities linked to climate changes, Mowi keeps displaying dedication to transparently accountable business methods.

The seafood market competition demonstrates a dynamic blend of innovative ideas, collaborative groupings and sustainability actions from key participants worldwide. People are getting more aware about sustainability and fair sourcing, so companies must be adaptive and quick to respond in order to maintain their edge within this fast-changing industry.

Seafood Market Scope: Inquire Before Buying

| Global Seafood Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 58.28 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 24.1% | Market Size in 2032: | USD 264.18 Bn. |

| Segments Covered: | by Product Type | Fish Shrimp Crab Lobster Oysters Squid Others |

|

| by Form | Fresh Seafood Frozen Seafood Canned Seafood Dried Seafood Others |

||

| by Distribution Channel | Supermarkets/Hypermarkets Specialty Stores/Fishmongers Online Retail Convenience Stores Others |

||

| by End-User | Household Consumption Foodservice Industry Industrial |

||

Seafood Market, by Regions

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players in the Seafood Market are:

1. Thai Union roup

2. Mowi ASA

3. Charoen Pokphand Foods (CPF)

4. Maruha Nichiro Corporation

5. Dongwon Industries

6. Lerøy Seafood Group

7. Austevoll Seafood ASA

8. Royal Greenland A/S

9. Cooke Inc.

10. Trident Seafoods

11. High Liner Foods

12. Nueva Pescanova Group

13. Grupo Profand

14. Kyokuyo Co., Ltd.

15. Tassal Group

16. Sea Harvest Group

17. Australis Seafoods

18. Camanchaca

19. Ocean Beauty Seafoods

20. Pacific Seafood Group

21. Labeyrie Fine Foods

22. Young’s Seafood

23. Clearwater Seafoods

24. American Seafoods Group

25. Slade Gorton & Co.

26. Lund's Fisheries

27. Pesquera Diamante

28. SeaPak Shrimp & Seafood Co.

29. Oceanus Group

30. MMP International

Frequently Asked Questions:

1. Which species are most consumed?

Ans. Salmon represents the largest single fish commodity in the global seafood market, driven by its high consumer demand.

2. Which country has most Exports of dry Fish?

Ans. United States , Ivory Coast , and Sri Lanka has the most imports of Dry fish.

3. What is the expected Global Seafood market size by 2032?

Ans. The expected Global Seafood market size is US$ 264.18 Bn by 2032.

4. Which region held the largest Seafood Market share in 2025?

Ans. Asia-Pacific is recorded to hold the largest market share for Seafood in 2025.