Scandinavia Frozen Food Market Size by Type, Product, Distribution, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

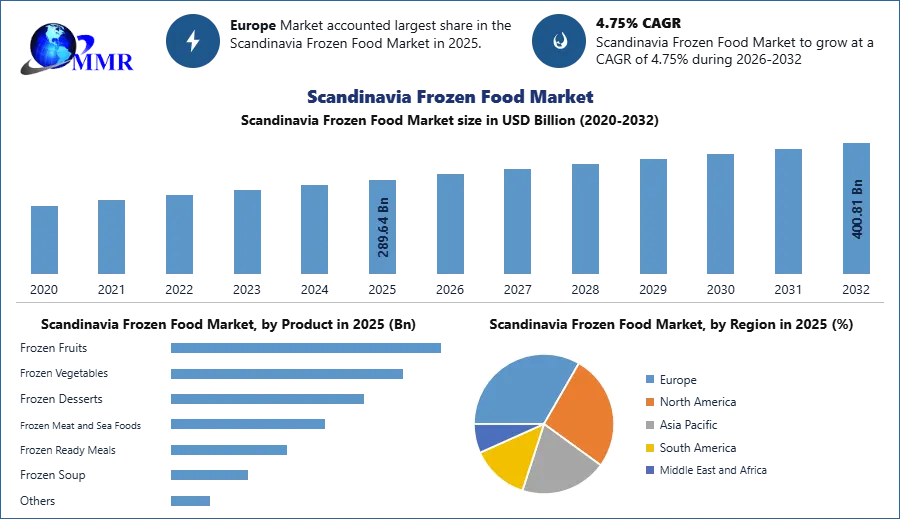

Scandinavia Frozen Food Market size was valued at USD 289.64 Billion in 2025 and is expected to grow at a CAGR of 4.75% from 2023 to 2029, reaching nearly USD 400.81 Billion.

Scandinavia frozen food market has witnessed substantial growth, driven by various factors. The market has benefited from the convenience offered by ready-to-cook and ready-to-eat frozen food options, saving consumers valuable time. Technological advancements in freezing techniques have improved the quality and preservation of flavor, texture, and nutrients in frozen food products. The market boasts a diverse range of products, including fruits, vegetables, meat, poultry, seafood, ready meals, bakery items, and desserts, catering to varied consumer preferences and dietary needs. Distribution channels such as supermarkets, hypermarkets, convenience stores, and online platforms play a significant role in the availability of frozen food products.

There is a growing demand for healthier frozen food alternatives, resulting in the introduction of organic, gluten-free, and low-calorie options to meet consumer expectations. Sustainability considerations have also become prominent, with consumers actively seeking eco-friendly products. Industry players are adopting sustainable practices and exploring packaging solutions that align with environmental concerns. Both domestic and international companies, such as Findus Group, Orkla ASA, Nestlé, Ardo NV, and McCain Foods, are actively participating in the market. However, it's important to note that market conditions can differ among the Scandinavian countries, necessitating thorough country-specific analyses to fully comprehend the nuances.

To know about the Research Methodology :- Request Free Sample Report

Scandinavia Frozen Food Market: Market Dynamics

Global Market Growth Drivers:

Scandinavia frozen food market is experiencing robust growth driven by various factors. The changing lifestyles and time constraints of consumers have resulted in a strong demand for convenient food options, making frozen food an increasingly popular choice. Manufacturers are responding to the growing health consciousness among consumers by offering nutritious frozen options that are free from additives. Technological advancements in freezing and packaging techniques have significantly improved the quality and shelf life of frozen food products.

The market offers a diverse range of products, including fruits, vegetables, seafood, meat, and ready-to-eat meals, catering to different dietary preferences. Sustainability concerns have also played a significant role in the market's growth, as frozen food helps reduce food waste and eliminate certain preservatives. Moreover, the cost-effectiveness of frozen food has made it an attractive choice for consumers, providing affordable options year-round. The availability of frozen food through various retail and e-commerce channels, including supermarkets, convenience stores, and online platforms, has further contributed to its widespread accessibility.

Scandinavia Frozen Food Market: Opportunities

Research on the Scandinavia frozen food market highlights numerous growth opportunities for manufacturers in the region. The report covers key findings such as the importance of product innovation in attracting consumers seeking unique and gourmet frozen options. Furthermore, it emphasizes the growing demand for health and wellness-oriented products, encouraging manufacturers to develop nutritious frozen options that align with specific dietary preferences, including natural, organic, low-sodium, gluten-free, and plant-based offerings. Convenience is identified as a crucial factor for on-the-go consumers, with a recommendation to create ready-to-eat, single-serve, and quick microwaveable frozen meals and snacks. The report also delves into the potential of the premium segment, suggesting the exploration of high-quality, artisanal frozen offerings such as specialty desserts, handcrafted pizzas, and premium seafood to cater to consumers seeking indulgent experiences at home.

Report explores the export potential of the Scandinavian market and suggests leveraging the region's reputation for safe and high-quality food products to tap into international markets. By capitalizing on these opportunities, manufacturers can drive growth, meet evolving consumer demands, and enhance their market position in the thriving Scandinavian frozen food industry.

Scandinavia Frozen Food Market: Restraints & Challenges

Scandinavia frozen food market, despite its remarkable growth, encounters various restraints and challenges. These include consumer perception and quality concerns, as well as price sensitivity, which hinder market players in effectively communicating the advantages of frozen food and striking a balance between affordability and product innovation. The complex supply chain involved in maintaining the cold chain, ensuring proper storage and transportation, presents logistical obstacles. Furthermore, compliance with stringent food safety and quality regulations necessitates ongoing investment and monitoring. Seasonality and ingredient sourcing pose challenges, particularly for products relying on seasonal ingredients.

The diverse consumer preferences and cultural differences across the Scandinavian countries require tailored market research and customized product offerings. The market also experiences intense competition, saturation in certain product categories, and a growing demand for eco-friendly packaging and sustainability practices, adding further complexity. To address these challenges, industry players must emphasize innovation, quality assurance, efficient supply chain management, consumer education, and sustainability initiatives. Successful adaptation to evolving consumer preferences and market dynamics is vital for achieving sustainable growth in the Scandinavia frozen food industry.

Scandinavia Frozen Food Market: Market Trends

The Scandinavian frozen food market report highlights key market trends that drive its growth and development. It covers the rising consumer demand for healthy and natural products, resulting in manufacturers offering a wider range of organic and additive-free frozen options. Convenience is a significant driver, with consumers seeking quick and ready-to-eat frozen meals. The market has expanded its product range to include international cuisines, specialty desserts, gourmet items, and plant-based alternatives. Sustainability and environmental responsibility are gaining importance, leading to an emphasis on eco-friendly packaging and transparent labeling. Technological advancements in freezing and packaging techniques have improved product quality and convenience. E-commerce has experienced growth, resulting in increased online sales of frozen food products. The preference for locally sourced ingredients and sustainable farming practices has prompted manufacturers to focus on transparent sourcing and production methods. These market trends reflect changing consumer preferences and behaviors, with manufacturers adapting their strategies accordingly.

Scandinavia Frozen Food Market: Market Segmentation

Scandinavia frozen food industry can be segmented based on product type, distribution channel, end user, country, consumer preferences, packaging type, and brand preference. These segments provide a detailed analysis of the market, allowing companies to identify and target specific customer groups effectively. The product type segment encompasses a wide range of categories, including frozen fruits and vegetables, meat and poultry, seafood, ready meals, bakery products, desserts, and others. Distribution channels vary from supermarkets and hypermarkets to convenience stores, online retailing, and others. The end-user segment covers residential consumers, food service establishments such as restaurants and hotels, and others. Geographically, the market is divided into Denmark, Norway, Sweden, Finland, and Iceland.

Consumer preferences, including organic, gluten-free, low-calorie frozen food products, and others, influence purchasing decisions. Packaging types such as bags and pouches, boxes and cartons, tubs and cups, and others play a role in product presentation. Brand preference can be categorized as domestic or international brands. Analyzing these segments provides valuable insights for companies, enabling them to tailor their strategies and effectively penetrate the market. It is important to note that the significance and scope of each segment may vary across the Scandinavian countries. Therefore, conducting comprehensive market research and understanding consumer preferences within each segment are essential for achieving successful market penetration.

Scandinavia Frozen Food Market: Regional Insights

Europe dominates the frozen food market during the 2026–2032 period, supported by strong consumption patterns, advanced cold chain infrastructure, and well-established retail networks.

Regional variations remain prominent in the Scandinavia frozen food market, with Denmark, Norway, Sweden, Finland, and Iceland continuing to exhibit distinct characteristics through the forecast period. Denmark maintains a strong position with a well-developed market driven by convenience-oriented consumers and an expanding portfolio of ready-to-eat and premium frozen offerings. Norway continues to emphasize high-quality, locally sourced frozen seafood, while demand for clean-label and health-focused products is steadily increasing. Sweden represents the most mature and innovation-driven market in the region, with strong consumer acceptance of organic, plant-based, and sustainably packaged frozen foods. Finland’s market is influenced by its traditional food culture, with sustained demand for high-quality frozen berries, vegetables, and forest-based products. Iceland, though smaller in scale, remains niche-focused, prioritizing locally sourced, environmentally sustainable frozen food products.

Within Scandinavia, evolving consumer preferences toward convenience, health, and sustainability are expected to drive innovation and competitive differentiation. Market players are increasingly focusing on product diversification, clean-label ingredients, and eco-friendly packaging to align with regional expectations and strengthen market positioning.

Scandinavia Frozen Food Market: Competitive Landscape

The industry is highly competitive, with both regional and international players striving to capture market share. Key players in the market include Findus Group, renowned for its wide range of frozen food products and focus on innovation and convenience. Orkla ASA, a prominent Nordic consumer goods company, offers a diverse portfolio of frozen food items and places a strong emphasis on sustainability. Nestlé, a food and beverage powerhouse, has established a significant presence in the Scandinavian market by prioritizing product quality, taste, and nutritional value. Ardo NV specializes in frozen vegetables, emphasizing sustainable practices and responsible sourcing. McCain Foods is a major player in frozen potato products, standing out with its commitment to quality, taste, and convenience.

Greenfood Group provides a varied selection of frozen fruits and vegetables, with an emphasis on organic and sustainable sourcing. Kronfågel AB, a leading poultry producer, is recognized for its top-notch frozen chicken products and dedication to animal welfare and sustainable farming methods. These companies exemplify the competitiveness of the market, where innovation, quality, convenience, and sustainability are vital factors for success. To thrive in this dynamic industry, companies must stay informed about market trends and consumer preferences.

Scandinavia Frozen Food Market Scope: Inquire before buying

| Scandinavia Frozen Food Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 289.64 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.75% | Market Size in 2032: | 400.81 USD Billion |

| Segments Covered: | by Packaging Type | Flexible Packaging Rigid Packaging Bulk Packaging Eco-Friendly Packaging |

|

| by Type | Ready-to-Eat Ready-to-Cook Ready-to-Drink Others |

||

| by Product | Frozen Fruits Frozen Vegetables Frozen Desserts Frozen Meat and Sea Foods Frozen Ready Meals Frozen Soup Others |

||

| by Distribution | Supermarkets & Hypermarkets Convenience Stores Online Retail Others |

||

Scandinavia Frozen Food Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Scandinavia Frozen Food Market Key Players:

1.Findus Group (Sweden)

2.Arla Foods (Denmark)

3. Orkla ASA (Norway)

4. Scandi Standard AB (Sweden)

5.ICA Gruppen AB (Sweden)

6. HKScan Corporation (Finland)

7. Lantmännen Unibake (Denmark)

8.Kavli Holding AS (Norway)

9. Axfood AB (Sweden)

10. Tulip Food Company (Denmark)

11.Apetit Oyj (Finland)

12. Kronfågel AB (Sweden)

13. Atria Plc (Finland)

14.Vaasan Group (Finland)

15. Polarica Group (Sweden)

16.Apetito AG (Sweden)

17.Felix AB (Sweden)

18. Frionor AS (Norway)

19.Lohilo Foods AB (Sweden)

20.Sunniva AS (Norway)

21.KLS Ugglarps AB (Sweden)

22. Scandza AS (Norway)

23.Paulig Group (Finland)

24. Picadeli AB (Sweden)

25. Netto Marken-Discount (Denmark)

26.Santa Maria AB (Sweden)

27.Coop Norge (Norway)