Quantum Dots Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

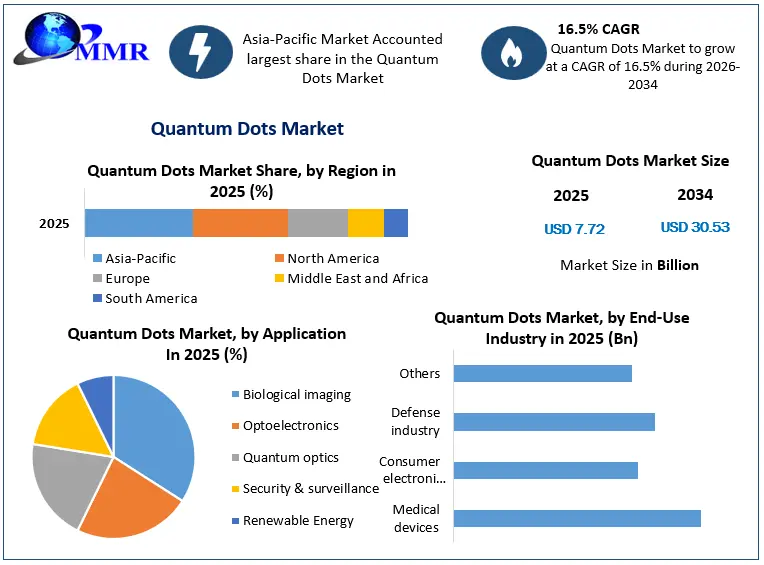

The Quantum Dots Market size was valued at USD 7.72 Billion in 2025 and the total Quantum Dots revenue is expected to grow at a CAGR of 16.5% from 2026 to 2034, reaching nearly USD 30.53 Billion.

Quantum Dots Market Overview:

Quantum dots (QDs) are tiny crystals that can transport electrons. When UV light strikes these semiconducting nanoparticles, they may emit a variety of colors. These synthetic semiconductor nanoparticles are used in composites, solar cells, and fluorescent biological markers.

Quantum dots are artificial nanostructures that can have a wide range of qualities based on their material and form, and as a result, demand for QD is significantly increasing. They can, for example, be utilized as active materials in single-electron transistors due to their unique electrical characteristics. A quantum dot's attributes are controlled not just by its size but also by its form, composition, and structure, such as whether it is solid or hollow. A dependable manufacturing technology that makes use of quantum dots' properties - for a wide range of applications such as catalysis, electronics, photonics, information storage, imaging, medicine, or sense - must be capable of producing large quantities of nanocrystals while adhering to the same parameters in each batch.

The growing need for optimized devices with improved performance and resolution quality is a primary driving force behind the adoption of this technology in a variety of application areas. Because quantum dots are employed in LEDs, the primary applications for quantum dots (QD) are display and monitoring. However, producing Blue quantum dots at sizes lower than average is more challenging than other hues of quantum dots, and this is a key limiting issue in the use of quantum dots in display and monitoring goods. Despite a few drawbacks, quantum dots would catch the attention of key players yet manufacturers would find it tough to investigate the possible use of quantum dots.

Quantum Dots Market Snapshot

To know about the Research Methodology:-Request Free Sample Report

Quantum Dots Market Dynamics:

Rising Popularity of quantum dot display devices among consumers

Modern screens not only have improved brightness and contrast ratios, but they also have higher resolutions and use less power than older displays. Display makers are designing screens with higher characteristics to increase their market position. Quantum dots are widely utilized in display systems because they provide richer color resolution, better color purity, a highly immersive high-dynamic-range (HDR) experience, and superior energy efficiency to traditional displays. Because quantum dots have narrow emission spectra and broad excitation profiles, they can more efficiently convert light into any hue in the visible spectrum. Quantum dots are often utilized by display makers due to their increased features.

Scarcity of rare earth materials

In the production of quantum dots, rare earth elements such as cadmium, selenium, zinc, and indium are utilized. Because of their scarcity and high demand, these materials are extremely costly. Quantum dots are created by a variety of processes that utilize materials with comparable characteristics. Materials appropriate for the formation of quantum dots are few; also, cadmium is a poisonous metal that is harmful to the environment. Cadmium, selenium, and indium are all being utilized more and more in the production of quantum dots. Due to their scarcity, these resources should be used as efficiently as possible.

Growing demand for large and high-resolution displays creates lucrative opportunities

In recent years, there has been a considerable increase in the demand for large-size and high-resolution display devices owing to the improved visual experience and the reduced prices of Lcd screens. Due to lower LCD pricing, large-screen displays have become more affordable. Due to the increased concentration of display manufacturers on the creation of 4K and 8K displays, there has been an increase in demand for quantum dots due to their capacity to enhance the display. The use of quantum dots in displays delivers benefits such as faster picture frame rates, better bit depth, and a broader color range.

Growing usage of toxic and heavy metals harms the environment and human health

Cadmium is the most effective raw material to manufacture of quantum dots. Heavy metal contamination, on the other hand, pollutes the environment and harms human health. The usage of heavy metals in home items might cause serious health concerns. However, numerous corporations and research organizations are developing cadmium-free quantum dots. Indium and zinc are acceptable cadmium alternatives for the creation of quantum dots. Cadmium-free quantum dots are predicted to be widely accessible soon and to dominate the market due to their safety, high performance, and environmental advantages.

Quantum Dots Market Segment Analysis:

By Material, the Cadmium Selenide segment dominated the market with the highest market share in 2025 and is expected to grow at a CAGR of 14.2% during the forecast period. Cadmium selenide (CdSe) quantum dots are distinguished by their monodisperse size distribution and adaptability. CdSe core quantum dots may be driven at a wide range of wavelengths and emit with a small peak, resulting in color-pure emission that spans almost the whole visible spectrum. CdSe core quantum dots are a low-cost option that is ideal for demonstrations and proof-of-concept work.

CdSe, the most common kind of QD, has become one of the most thoroughly investigated fluorescent semiconductor nanocrystal families due to its appropriate and controllable bandgap throughout the visible spectrum. Because hydrophobic CdSe QDs are insoluble in aqueous solutions, they cannot be used directly in biological applications. They must be water-soluble via surface modification with different bifunctional surface ligands or caps to increase aqueous solubility and biocompatibility. To be effective in biomedical applications, QDs must be conjugated with biological molecules without interfering with their biological function.

By manipulating nanocrystal size, photoluminescence (PL) and electroluminescence emission from colloidal cadmium selenide (CdSe) quantum dots (QDs) may be controlled within the visible spectrum from 450 nm to 650 nm. CdSe quantum dots' versatility allows them to be used in a wide range of photonic devices, including emitters for color displays, color modifiers for light emitting diodes (LEDs), optical fiber amplifiers, low threshold lasers, self-assembled photonic sphere arrays, polymer-based photovoltaic cells, optical temperature probes, chemical sensors, and high-speed signal-processing filters driving the segment growth.

CdSe quantum dots are also being utilized commercially to meet increasing demand in the field of biomedical imaging. In terms of biocompatibility, excitation and filtering simplicity, and photo-stability, QDs conjugated with antibodies generate biomarkers that compete with standard organic fluorescent tags.

By Application, the Biological Imaging segment is expected to maintain its dominance at the end of the forecast period. In terms of revenue, the biological imaging industry is the most mature, and it is expected to contribute to the growth of the Quantum Dots market. Semiconductor nanocrystals, also known as quantum dots (QDs), exhibit novels optical and electrical qualities such as size-tunable light emission, simultaneous stimulation of several fluorescence hues, high signal brightness, long-term photostability, and multiplex capabilities. Because of their photobleaching, low signal strength, and spectrum overlapping, such QDs have substantial benefits in chemical and biological research over standard fluorescent organic dyes and green fluorescent proteins. In recent years, these features of QDs have sparked a lot of interest in biology and medicine.

QDs are a type of semiconducting nanostructures with distinct optical and electrical features. In chemical and biological investigations, they have considerable benefits over typical fluorescent organic dyes in terms of adjustable emission spectra, signal brightness, photostability, and so on. The heavy metal-containing II-IV, IV-VI, or III-V QDs are now the most common form of QDs. To reduce the possible toxicity of fluorescent sensors for biological applications, silicon QDs, and conjugated polymer dots have also been produced. When used in biological research, such as in vitro and in vivo imaging, aqueous solubility is a common problem for all forms of QDs.

QDs are useful in imaging and as highly fluorescent probes for biological sensing because they have higher sensitivity, longer stability, good biocompatibility, and are less intrusive. The lengthy lifespan of 10-40 ns enhances the likelihood of absorption at shorter wavelengths and results in a wide absorption spectrum. The core-shell structure is of more interest in QDs than the core structure. The size of the core nanocrystal, regardless of core/shell configuration, controls the emission wavelength of QDs.CDs QDs, for example, are used to generate ultraviolet and blue emissions, CdSe is utilized to cover the majority of the visible spectrum, CdTe is ideally suited for the red and near-infrared regions, and PBS and PbSe have been used to construct cores that emit in the near-infrared area.

Quantum Dots Market Recent Industry Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 May 2025 | TCL Corporation | Launched the C6K QD-Mini LED TV series in the UAE market. | Expands consumer access to high-performance quantum dot display technology in the Middle East. |

| 22 January 2025 | UbiQD, Inc. | Completed the acquisition of BlueDot Photonics to integrate advanced intellectual property. | Strengthens R&D and production capacity for high-performance, cadmium-free quantum dot materials. |

Quantum Dots Market Regional Insights:

The Asia-Pacific quantum dots market dominated the Quantum Dots Market with the highest market share of about 15.5% in 2025 and is expected to maintain its dominance at the end of the forecast period. The Asia-Pacific region's market growth may be ascribed to customers' preference for technologically sophisticated goods, as well as the engagement of numerous colleges and organizations in the R&D of QD technology, especially in the display industry.

The rising demand for optoelectronic devices and solar energy applications is also a major driver of growth in this region's market. Quantum dots are the chosen material for display and lighting solutions because of their unique optical qualities such as high quantum yield, emission tenability, narrow emission band, and optical stability.

The demand for QD displays in Asia-Pacific, particularly in China, is expected to rise, driving the quantum dots market during the forecast period. The development of new products in the TV, monitor, and smartphone sectors is increasing the usage of QD displays, which may increase the growth of the quantum dots market. Japan and South Korea would dominate the market in terms of technology and innovation since they are technologically advanced in the field of electronics and semiconductor devices.

Quantum Dots demand fluctuates in response to variations in the semiconductor manufacturing sector. In , China witnessed a 39% increase in semiconductor equipment sales, reaching $1872 billion, up from $13.45 billion in . Global sales reached a new high of $71.2 billion in , up 19% from $59.75 billion in . Wafer processing, assembly and packaging, test, and other front-end equipment, such as mask/reticle production, wafer manufacture, and fab facilities, are all included in the equipment counts.

Taiwan ranked second with $17.15 billion in sales, up 0.2% from the previous year, after China took the top place in . Korea came in third with $16.08 billion, an increase of 61%, while Japan came in fourth with $7.58 billion, an increase of 21%, and barely ahead of North America. SEMI said that Europe sold $2.64 billion in , a 16% increase from the previous year's shrinkage.

North America is expected to grow considerably with the highest revenue share followed by Europe due to the early adoption of QD technology. Rising income, advancing technologies, and improved Internet connectivity are the factors driving the increased penetration of electronic devices in the industry, resulting in increased demand for Quantum Dots. This rising demand would undoubtedly have a beneficial influence on market size.

Consumer electronics are widely used in a wide range of areas, ranging from computers, mobile phones, ear pods, smartwatches, and smartphones to smart household gadgets such as washing machines, air conditioners, and others. According to a Pew Research Centre poll done in , one in every five Americans possesses a wearable fitness tracker or a smartwatch, while 85% own a smartphone device.

Quantum Dots Industry Ecosystem:

Quantum Dots Market Scope: Inquire before buying

| Quantum Dots Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 7.72 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 16.5% | Market Size in 2034: | USD 30.53 Bn. |

| Segments Covered: | by Material | Cadmium Selenide Cadmium Sulphide Cadmium Telluride Indium Arsenide Silicon |

|

| by Technology | Colloidal synthesis Fabrication Viral assembly Electrochemical assembly Bulk manufacturing Cadmium-free QD technology |

||

| by Application | Biological imaging Optoelectronics Quantum optics Security & surveillance Renewable Energy |

||

| by End-Use Industry | Medical devices Consumer electronic devices Defense industry Others |

||

Quantum Dots Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Switzerland, Austria and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina and Rest of South America)

Quantum Dots Market, Key Players are:

1. NANOSYS INC (US)

2. Sigma-Aldrich Co. (US)

3. Thermo Fisher Scientific Inc. (US)

4. The Dow Chemical Company (US)

5. Ocean NanoTech (US)

6. Altair Nanotechnology, Inc. (US)

7. Life Technologies Corporation (US)

8. Microvision Inc. (US)

9. Quantum Material Corporation (US)

10. NNCrystal (US)

11. Apple Inc. (US)

12. American Elements (US)

13. Nanoco Technologies Limited (UK)

14. OSRAM GmbH. (Germany)

15. Innolume GmbH (Germany)

16. Merck Group (Germany)

17. Applied Quantum (Canada)

18. Cytodiagnostics Inc. (Canada)

19. Attonuclei (France)

20. Sony Corporation (Japan)

11. QD Laser, Inc. (Japan)

12. LG Display (South Korea)

13. Samsung Electronics Co. Ltd (South Korea)

14. Avantama AG (Switzerland)

15. Metrohm AG (Switzerland)

FAQs:

1. Which is the potential market for the Quantum Dots (QD) in terms of the region?

Ans. APAC is the potential market for Quantum Dots (QD) in terms of the region.

2. What are the opportunities for new market entrants?

Ans. The Growing demand for large and high-resolution displays creates lucrative opportunities.

3. What is expected to drive the growth of the Quantum Dots Market in the forecast period?

Ans. A major driver in the Quantum Dots Market is the Rising Popularity of quantum dots display devices among consumers.

4. What was the Global Quantum Dots Market size in 2025?

Ans: The Global Quantum Dots Market size was USD 7.72 Billion in 2025.

5. What segments are covered in the Quantum Dots Market report?

Ans. The segments covered are Material, Technology, Application, End-Use Industry, and Region.