Data Center Chip Market Size by Chip Type, Data Center, Industry, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

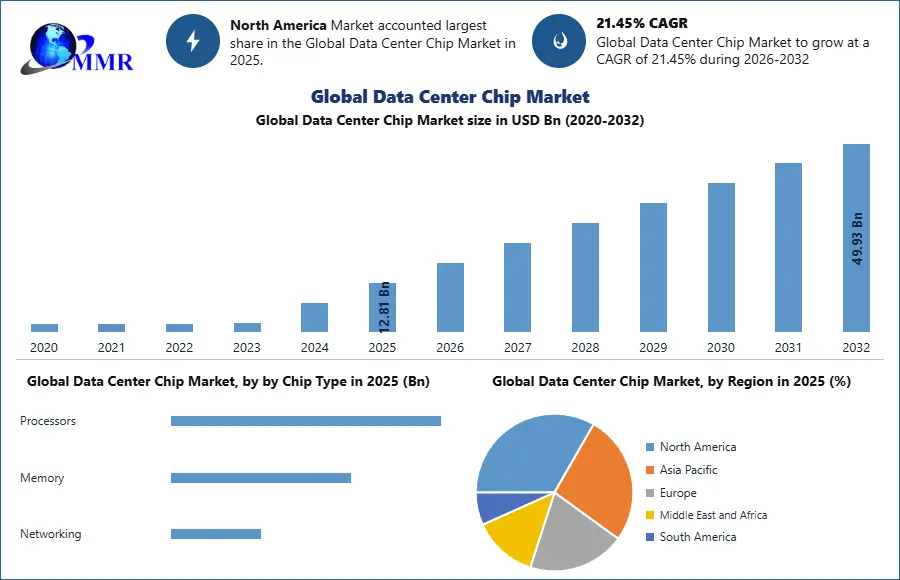

The Data Center Chip Market size was valued at USD 12.81 Billion in 2025 and the total Data Center Chip revenue is expected to grow at a CAGR of 21.45% from 2026to 2032, reaching nearly USD 49.94 Billion.

Global Data Center Chip Market Definition

Data center chips are the type of processor chips which are widely used for cloud computing, artificial intelligence applications and are also used to run various programs on a single chip.

To know about the Research Methodology :- Request Free Sample Report

Global data center chip market Dynamics

A growing adoption of data center chips from cloud computing companies and ongoing advancements in chip technology are the major driving factors behind the growth of the market. Increasing number of data centers across the globe, rising adoption of government regulations concerning localization of data centers, growing adoption of various smart computing devices, rising technological advancements in cloud computing, artificial intelligence based computing and escalating market for FPGA-based accelerators are expected to witness fast growth during the forecast period.

However, increased costs and ever-changing data center operations are the major restraining factors that cloud hamper the growth of the market.

Global Data Center Chip Market: Segmentation Analysis :

In 2025, the Chip Type segment is dominated by Central Processing Units (CPUs) and Graphics Processing Units (GPUs) due to their critical role in handling compute-intensive workloads across data centers. CPUs remain the backbone for general-purpose computing and server operations, while GPUs are witnessing the highest demand growth driven by artificial intelligence (AI), machine learning, and high-performance computing workloads. Field-Programmable Gate Arrays (FPGAs) are gaining traction for their flexibility and low-latency processing in specialized workloads, particularly in edge and networking applications. Application-Specific Integrated Circuits (ASICs) are increasingly adopted for custom, high-efficiency processing in AI and hyperscale environments. The “Others” category, including emerging chip architectures, shows steady but niche adoption.

Based on Memory, Double Data Rate (DDR) memory holds the largest share in 2025 due to its widespread use in standard server architectures and cost-effectiveness. However, High Bandwidth Memory (HBM) is the fastest-growing segment, driven by rising demand for high-speed data processing in AI workloads, GPUs, and advanced analytics. HBM offers superior bandwidth and performance, making it ideal for next-generation data centers. As data-intensive applications expand, the transition toward high-performance memory solutions continues to accelerate.

In the Networking segment, Network Interface Cards (NICs)/Network Adapters dominate in 2025 as they are essential for enabling communication between servers and external networks. Interconnects are experiencing strong growth due to increasing demand for low-latency, high-speed data transfer within hyperscale and cloud data centers. The “Others” segment, including switches and routers, continues to support overall infrastructure but grows at a moderate pace compared to advanced interconnect technologies. The overall trend is toward faster, more efficient networking solutions to support massive data flows.

| Global Data Center Chip Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 12.81 USD Bn |

| Forecast Period 2026-2032 CAGR: | 21.45% | Market Size in 2032: | 49.93 USD Bn |

| Segments Covered: | by Chip Type | Processors Central Processing Units (CPUs) Graphics Processing Units (GPUs) Field-Programmable Gate Arrays (FPGAs) Application-Specific Integrated Circuits (ASICs) Others Memory High Bandwidth Memory (HBM) Double Data Rate (DDR) Networking Network Interface Cards (NICs)/Network Adapters Interconnects Others |

|

| by Data Center Type | Small and Medium-Sized Data Centers Large Data Centers |

||

| by Application | Artificial Intelligence (AI) Cloud Computing Big Data Analytics |

||

| by End-use | IT Telecom Healthcare BFSI Retail & E-commerce Entertainment & Media Energy Others |

||

Global Data Center Chip Market: Regional Analysis

Based on Region, North America leads the Global Data Center Chip Market in 2025, supported by the presence of major cloud providers, advanced semiconductor companies, and strong AI adoption. The region benefits from significant investments in hyperscale data centers and cutting-edge technologies. Asia Pacific is the fastest-growing region, driven by rapid digitalization, expansion of cloud services, and increasing data consumption in countries like China and India. Western Europe shows steady growth with strong regulatory frameworks and digital infrastructure investments. Eastern Europe, MEA, and South America exhibit moderate growth, influenced by gradual technology adoption and expanding data center ecosystems.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 19 March 2026 | AMD | Expanded its strategic partnership with Samsung to secure HBM4 and DDR5 memory supply for future AI silicon. | Secures a critical supply chain advantage for next-generation MI455X accelerators amidst global memory allocation constraints. |

| 16 March 2026 | Intel | Confirmed Intel Xeon processors will serve as the host CPUs for NVIDIA DGX Rubin NVL8 systems. | Reinforces Intel’s dominance in CPU orchestration for high-end AI infrastructure despite intense competition in GPU accelerators. |

| 24 February 2026 | Meta Platforms | Entered a major agreement to purchase up to $60 billion worth of AI chips from AMD over five years. | Signals a major shift toward multi-vendor AI hardware strategies, reducing reliance on a single primary chip supplier. |

| 22 September 2025 | NVIDIA | Announced a strategic partnership with OpenAI to deploy 10 gigawatts of AI infrastructure using the Vera Rubin platform. | Establishes a landmark scale for AI deployment, effectively setting the performance benchmark for superintelligence training. |

The objective of the report is to present a comprehensive analysis of the Global Data Center Chip Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language.

The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers, and new entrants. PORTER, SWOT, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding Global Market dynamics, structure by analyzing the market segments and projects the Global Market. Clear representation of competitive analysis of key players by Application, price, financial position, Product portfolio, growth strategies, and regional presence in the Global Market make the report investor’s guide.

The Scope of Global Data Center Chip Market: Inquire before buying

Global Data Center Chip Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Data Center Chip Market Report in Strategic Perspective:

- Intel Corporation

- GlobalFoundries

- Advanced Micro Devices Inc

- Taiwan Semiconductor Manufacturing Co. Ltd

- Samsung Electronics Co. Ltd

- Arm Limited

- Broadcom

- Xilinx, Inc

- Huawei Technologies Co. Ltd

- Nvidia Corporation

- IBM Corporation

- Google LLC

- Amazon.com Inc

- Qualcomm Inc

- Microsoft Corporation

- Meta Platforms, Inc

- Marvell Technology, Inc

- SK Hynix Inc

- Micron Technology, Inc

- Achronix Semiconductor Corporation

- Fujitsu Limited

- Cerebras Systems

- Graphcore

- Ampere Computing

- Groq, Inc