Private Wireless Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

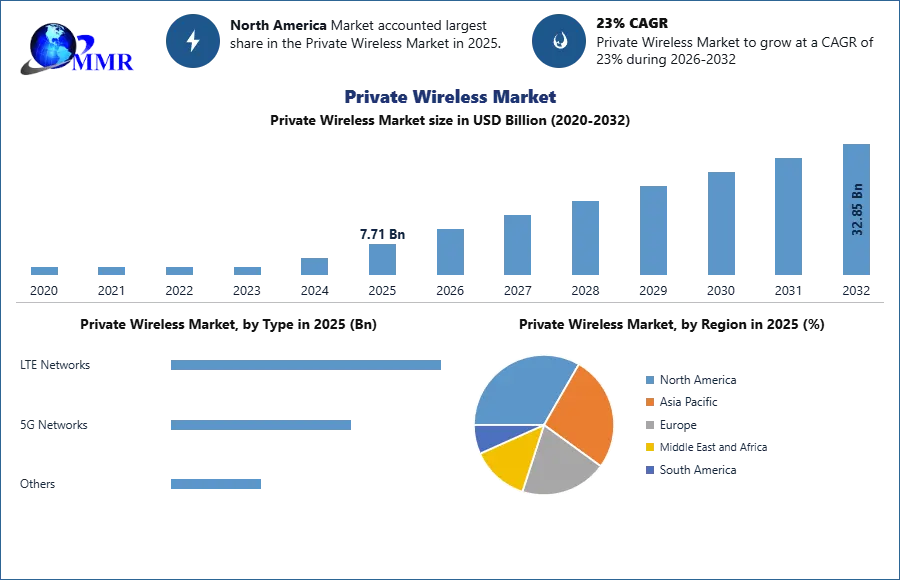

The Private Wireless Market size was valued at USD 7.71 Billion in 2025 and the total Private Wireless revenue is expected to grow at a CAGR of 23% from 2026 to 2032, reaching nearly USD 32.85 Billion.

The Global Private Wireless Market Overview

A private wireless network is communication network that is owned, operated, and used by specific organization or individual for their own use. It is not accessible to the general public. The private wireless network is limited to a particular company or area in the organization. The main goal of private wireless network is to provide a secure, dependable, and dedicated wireless communication service to satisfy the specific needs of the owner. Basically, it is a private phone network for business purpose, to maintain secure communication within organization. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The private wireless network market growth is driven by key industries like manufacturing, healthcare, transportation, and logistics. The private wireless network aligns with goal to optimize digital ecosystems and ensure robust wireless connectivity to specific operational demands. LTE (Long term evolution) and 5G technologies plays an important role in private wireless network across various industries. The application of these technologies goes beyond mobile connectivity. The mentioned technologies play an important role in EMBB (Enhanced Mobile Broadband), IoT (Internet of Things), (URLLC) ultra-reliable low latency communication and FWA (Fixed Wired Access).

North America dominates the Global private wireless market with the help of the advanced technological infrastructure and strategic investments. The dominance in both market share and growth is supported by US, Canada and Mexico, with US contributing to 22% of total revenue share. Companies such as AT&T Inc., Broadcom Inc., Cisco Systems Inc. and Huawei Technologies Co., Ltd. operating in the private 5G network market are contributing to the rapid growth of the private wireless network market in North America.

When it comes to Europe, Germany holds a significant market share in private wireless network with CAGR of 26%. Whereas UK follows Germany with CAGR of 25.5% in private wireless network market. APAC region is expected to grow considerably as countries such as China, Japan, South Korea, and Australia are actively engaged in substantial investments directed towards the establishment of automated factories and the acquisition of 5G spectrum.

Private Wireless Market Dynamics

The 5G Expansion

5G technology is expected to easily integrate or replace the existing wired connections. 5G technology provides faster speeds with lower latency, and also provide higher bandwidth. It provides seamless video streaming and lag-free video games but also to enable next-generation tools and platforms that draw on artificial intelligence, the Internet of Things. Reliance on autonomous guided vehicles (AGVs) is decreasing as 5G technology grow its use in broader public areas.

In 2025, there has been expansion in the deployment of private wireless networks. Count of private LTE/5G networks reached 2,900 globally in. It is expected that global count of private LTE and 5G networks set to grow more than 13,000 by . In 2025, the market of private network cellular equipment and services is expected to be worth tens of billions annually, highlighting significant economic impact and relevance in the business landscape. When it comes to investment, 500 Billion dollars is an expected investments globally from 2023 to 2025 in 5G infrastructure which boost the growth for private wireless market.

Asia-pacific is expected to dominate the 5G private wireless market with countries such as Japan, South Korea, China, and Australia contributing to the regional market growth. While North America dominates 30% of the global 5G private wireless market.

The private wireless market is impacted by the continuous growth of smart cities, the rising global use of connected devices, and the demand for Ultra-Reliable Low Latency Connectivity (URLLC). These factors are shaping the business landscape, reflecting a need for advanced and reliable network solutions to support the increasing connectivity demands and thus the growth of private wireless technology is inevitable. More than 5000 private 5G deployment was made in China, which maintains China’s dominance in APAC. Japan follows China in the development of private wireless network in APAC region.

Private wireless networks in IoT

Private wireless networks offer substantial enhancements in network performance, providing swift data transfer and minimizing latency. These networks bring about improved reliability, wider coverage, increased device connectivity, and consistent performance, ensuring the seamless operation of IoT devices. The security features of private wireless networks play a pivotal role in preserving the integrity and confidentiality of vital IoT processes and information. Wireless networks improves security features safeguarding the integrity and confidentiality of critical IoT processes. Private wireless networks allow organizations to tailor the network infrastructure to the specific needs of their IoT applications.

North America holds the largest market share of IoT. It is expected to maintain its dominance till 2025. The IoT market of North America was valued at $120 Billion in 2023 and is expected to grow with a healthy CAGR of 18%. With the help of private wireless network companies like Amazon Web Services, Cisco Systems, Google, Microsoft Corp are the key contributors to this large market share.

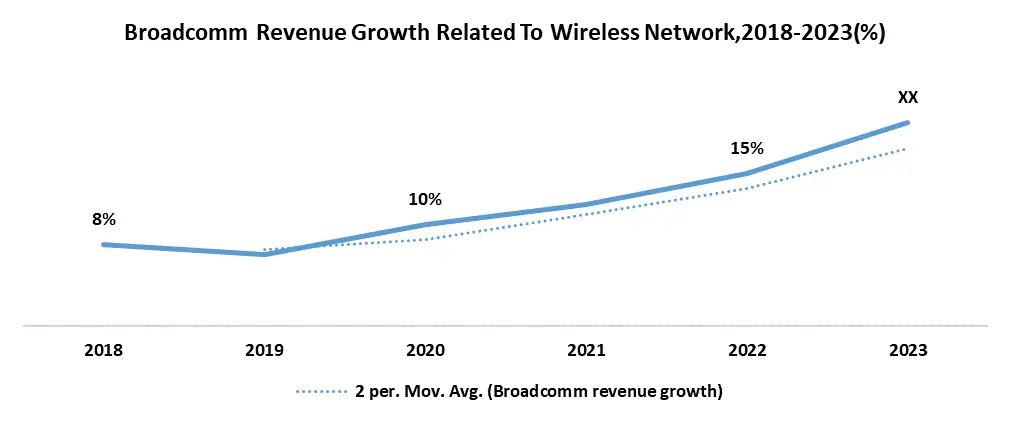

Companies like Broadcom, AT&T, Nokia, Qualcomm benefit from these development in IoT due to wireless network. The revenue share of Wireless networks for Broadcom in 2023 was 22%. Wi-Fi network market share of Broadcom in 2023 was 35% with Qualcomm gaining 25% market share.

The APAC region is expected to grow at highest CAGR with China expected to dominate the market of private network in 2028. Huawei holds the largest market share of network providers globally with around 25% market share. All these improvement in the IoT technology boost the demand for Private wireless network providers. Europe private wireless market in IoT services is expected to grow at 12% CAGR.

Regulation role in Private Wireless Market

The most important thing in private wireless market is to follow the complex regulatory frameworks set forth by respective governments. Regulatory challenges like obtaining licenses and permits slows down the deployment process and increase costs of the private wireless network market players. Spectrum is a crucial ingredient in the process of 5G deployment. As the allotment of 5G spectrum is in their initial stages, it acts as a resistance for the private wireless market companies’ growth.

United States has implemented regulations that restrict certain manufacturers from obtaining authorization and selling products. The Federal Communications Commission (FCC) has established guidelines to wireless carriers to follow cybersecurity standards. The FCC engages in the regulation of foreign investments in American telecom companies.

It is necessary for all telecom equipment and devices to obtain license to get approval from the Ministry of Industry and Information Technology (MIIT) in China.

Private Wireless Market segment analysis

By Type, LTE and 5G are the key types of wireless network. Long term evolution (LTE) networks are becoming popular for companies to establish their own cellular networks. The increasing demand for LTE in private wireless market is due to its enhanced security, control over coverage, and the ability to prioritize traffic. The global LTE private wireless market is expected to grow at a 10% CAGR. US and Canada significantly contribute to the LTE private wireless market in North America with an expected growth rate of 11%. UK and Germany significantly contribute to market revenue share of private LTE wireless network in Europe region.

The private LTE market shows robust segmentation based on key components, including infrastructure and services, as well as technology differentiators such as Frequency Division Duplex (FDD) and Time Division Duplex (TDD). The business impact of LTE and 5G is measured by company’s capacity to provide accelerated and dependable wireless connectivity. In Enhanced Mobile Broadband (EMBB) technologies equip users with high-speed internet access, seamless multimedia streaming, and video conferencing. AT&T, Deutsche Telekom AG, Ericsson are one of the key players in LTE Private Wireless market.

The expansion of the private 5G network market is driven by demand for seamless connectivity through private 5G services, catering to applications such as Ultra-HD cameras, extended reality headsets, and Automated Guided Vehicles (AGVs). The manufacturing sector has secured the predominant revenue share, surpassing 17.0%, and is expected to grow.

The Global adoption of 5G network is growing rapidly increasing the demand for private wireless network market. Spending on 5G private wireless network is expected to surpass USD 6 Billion by. Significant are being made in APAC region on 5G spectrum acquisition in countries like Japan, South Korea, China, and Australia. The expected CAGR of APAC region is 25% till.

Asia is the largest market share for 5G infrastructure. Samsung and ZTE are one of key players in private 5G wireless market in Asia. North America and Europe are second and third largest market globally in private 5G wireless market. Private 5G Radio Access Networks (RANs) enhance security measures by selectively permitting access to the network only for trusted devices. This controlled access contributes to the establishment of a secure and reliable communication environment.

By Application, The industry private wireless network market is experiencing rapid growth, fuelled by an increasing demand for secure, reliable, and high-speed connectivity solutions. Manufacturing is poised to represent 30% of the total expenditure on private networks, with a strategic emphasis on the implementation of smart factories and industrial facilities situated in rural areas. The adoption of private wireless network is increasing in transport and logistics which includes increasing infrastructure of airport, ports, warehouses used for on-site communications including staff, automation systems, vehicles, IoT sensors, cameras, and infrastructure. There is growing market of private wireless network in education.

Canadian government are increasing funding in private wireless network market as it offers encouragement to private investors to invest in wireless network technology. Private wireless networks offer a cost-effective alternative to public networks, essentially for government agencies looking for high-speed and low-latency connectivity. These networks make government entities to regulate internet access. The trend in government leans towards deploying private 5G networks. The focus centres on robust public-private partnerships, drawing inspiration from successful models like South Korea, characterized by extensive 5G coverage and a vibrant technology ecosystem.

Private Wireless market competitive landscape

Deutsche Telekom is making big investments to grow its fiber network, with plans to connect over 10-11million homes by 2025. In 2023, Deutsche Telekom connected 83% of 5G mobile sites with high-speed fiber, reaching 10,000 sites at 10 Gbps and have over 80,000 5G antennas. Cisco has strategically directed investments into its Quortus iNet private wireless network solution. The primary emphasis lies in delivering secure and reliable connectivity solutions tailored for both businesses and government organizations.

In May 2020, Huawei Tech came into partnership with 18 leading automakers to make a 5G automotive environment in the industry. In Dec 2023, Ericsson AB won a $14 billion contract to modernise AT&T wireless network, agreeing to build an open network that supplied by a number of vendors. In Feb 2022, Qualcomm Technologies, Inc. announced a strategic collaboration with Microsoft to unveil a groundbreaking chip-to-cloud solution for private enterprise networking. This innovative offering is designed to address the challenges surrounding technology adoption, providing enterprises with a scalable solution for the implementation of private 5G networks on a global scale.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 13 April 2026 | IPLOOK | Released its global research report detailing the transition to 5G Standalone (SA) as the uncompromising technical standard for industrial "digital sovereignty." | This shift marks the official end of the Non-Standalone (NSA) era, forcing vendors to upgrade legacy hybrid solutions to meet enterprise latency requirements. |

| 27 January 2026 | NTT Data Group | Finalized a $16 billion merger and restructuring move to transition from traditional outsourcing to full-stack digital ecosystem orchestration involving private networks. | The move consolidates cloud and 5G capabilities, accelerating the market shift toward managed services for complex industrial deployments. |

| 18 November 2025 | Celona | Collaborated with Sutherland to launch an AI-powered private 5G and autonomous network solution designed to simplify enterprise IT operations. | This partnership lowers the barrier to entry for non-technical enterprises by automating network management through integrated AI inference. |

| 22 October 2025 | Hughes Network Systems | Entered a strategic partnership with Celona to integrate private 5G LAN technology into its managed network services portfolio. | The agreement expands the reach of private wireless into rural and satellite-reliant sectors, providing fixed data connectivity in remote industrial sites. |

| 15 July 2025 | Nokia Corp | Partnered with Solis Tower Telecom to deploy flexible digital agriculture solutions across rural Brazil using private wireless infrastructure. | The project addresses the connectivity gap in global agribusiness, targeting the 81% of Brazilian agricultural land currently lacking cellular coverage. |

Private Wireless Market Scope: Inquire before buying

| Private Wireless Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 7.71 USD Billion |

| Forecast Period 2026-2032 CAGR: | 23% | Market Size in 2032: | 32.85 USD Billion |

| Segments Covered: | by Type | LTE Networks 5G Networks Others |

|

| by Application | Manufacturing Energy & Utilities Transportation & Logistics Healthcare Government / Public Safety Mining Others |

||

| by Component | Hardware Software Services |

||

Private Wireless Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Key Players / Competitors Profiles Covered in Brief in Global Private Wireless Market Report in Strategic Perspective:

- Telefonaktiebolaget LM Ericsson

- Nokia Corp

- Samsung

- ZTE Corp

- Deutsche Telekom

- Juniper Networks

- AT&T Inc

- Verizon Communications

- Cisco Systems

- Huawei Technologies Co., Ltd.

- Broadcom Inc

- Qualcomm Technologies, Inc.

- Vodafone Group Plc

- T-Systems International GmbH

- Celona

- Mavenir

- Airspan Networks

- Fujitsu

- NEC Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- Comba Telecom

- Affirmed Networks

- Altiostar

- Baicells Technologies