Paediatric Medical Device Market Size by Product, Type, End User and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

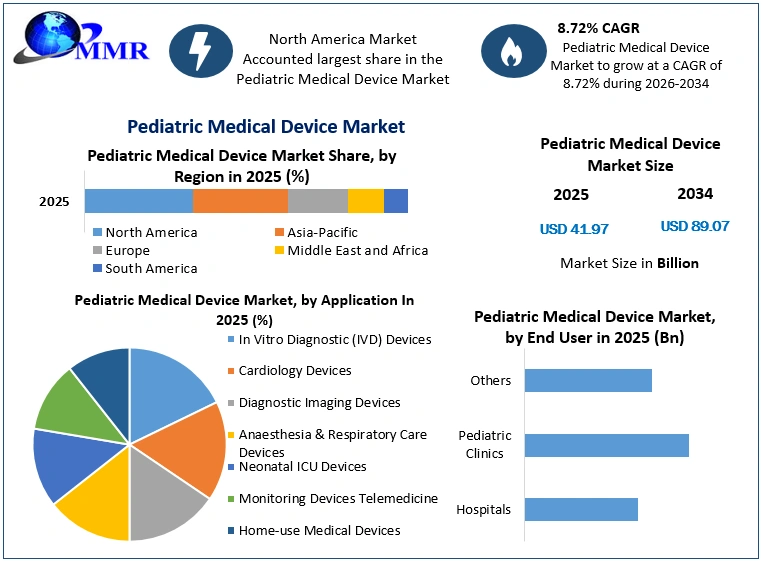

The Pediatric Medical Device Market size was valued at USD 41.97 Billion in 2025 and the total Pediatric Medical Device revenue is expected to grow at a CAGR of 8.72 % from 2026 to 2034, reaching nearly USD 89.07 Billion by 2034.

The Pediatric Medical Device Market refers to the sector dedicated to producing medical devices specifically designed for infants, children, and adolescents, addressing their unique healthcare needs. The Pediatric Medical Device Market is experiencing robust growth driven by various factors. Increasing incidences of pediatric diseases and disorders, coupled with advancements in healthcare technology, have boosted the demand for specialized medical devices catering to this demographic. Factors such as a greater emphasis on child healthcare, a surge in funding for research and development, and a growing focus on personalized medicine for children have significantly contributed to market expansion.

Key players in the Pediatric Medical Device industry, such as Medtronic, Philips Healthcare, Abbott Laboratories, Boston Scientific Corporation, and Johnson & Johnson, have been actively involved in the development of innovative pediatric medical devices. Recent developments include a shift toward minimally invasive procedures for children, the creation of wearable devices tailored for pediatric use, and advancements in imaging technologies specifically designed to address the unique needs of pediatric patients. There's an ongoing focus on enhancing the safety, efficacy, and usability of these devices to ensure better outcomes and improved quality of care for pediatric populations worldwide. The Pediatric Medical Device Market growth indicates sustainability, driven by continuous technological advancements, supportive regulatory environments, and a growing commitment to pediatric healthcare.

Pediatric Medical Device Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Pediatric Medical Device Market Dynamics:

Increasing Pediatric Health Conditions with Growing Emphasis on Personalized Medicine driving the growth of the Pediatric Medical Device Market

Rising incidences of chronic conditions such as diabetes and asthma among children fuel the demand for specialized devices such as Dexcom G6's continuous glucose monitoring system, enhancing disease management and reducing risks. Innovations in miniaturization and wireless connectivity, exemplified by the Owlet Smart Sock, provide real-time monitoring of vital signs for infants, empowering parents through smartphone apps. Tailoring devices to children's unique needs, such as Stryker Corporation's customizable orthopedic implants, improves functionality and fit, enhancing treatment outcomes. A shift towards less invasive treatments, facilitated by companies such as Olympus Corporation with pediatric endoscopes, reduces trauma during interventions.

Specialized imaging tools, such as GE Healthcare's pediatric MRI coils, enable high-resolution imaging, crucial for accurate diagnoses in children. Devices featuring intuitive interfaces, like the PARI Vios nebulizer, encourage compliance in pediatric respiratory care. Favorable regulations like the FDA's Pediatric Device Consortia program incentivize innovation and streamline approvals. Growing awareness among parents and healthcare providers, driven by educational campaigns, expands the market. Increased investments in pediatric healthcare infrastructure globally ensure accessibility and affordability of specialized devices. Dedicated R&D initiatives, like Children's Hospital of Philadelphia's Center for Applied Genomics, propel innovation catering specifically to pediatric healthcare needs, further driving Pediatric Medical Device market growth.

High Costs and Regulations Hamper Market Growth in Pediatric Medical Device

Stringent regulations pose a significant obstacle to the pediatric medical device market growth. Unlike devices for adults, those designed for children require specialized testing due to age-specific factors. For instance, the Berlin Heart, a pediatric ventricular assist device successful in Europe, faced delays in FDA approval due to the stringent safety and efficacy requirements. This prolonged the development process, increased costs, and limited market growth. These regulatory complexities create hurdles, complicating an already intricate development process.

The limited number of pediatric patients presents a challenge for manufacturers. The smaller market and conditions such as congenital heart defects, with low incidence rates, discourage investment in specialized pediatric devices. Companies often prioritize adult devices due to higher profitability, stalling innovation in pediatric medical technology. The economic viability of pediatric device development remains uncertain. The costs of creating specialized devices may not align with Pediatric Medical Device market demand, especially in cases such as respiratory support devices tailored for various pediatric age groups. Engineering challenges delay market introductions, further complicating matters.

Inadequate data and research in pediatric populations also impede device development. Limited clinical trials and data availability make it challenging to demonstrate safety and efficacy, leading to regulatory approval delays. This scarcity, particularly in rare pediatric diseases, creates barriers for developers, hindering progress and innovation. Reimbursement policies add to the problem. Unlike adult-focused devices with established reimbursement structures, pediatric devices face uncertainties, deterring healthcare providers from investing without clear reimbursement pathways. Ethical considerations in pediatric clinical trials and device use present further challenges. Balancing innovation with ethical guidelines, ensuring informed consent, and navigating ethical dilemmas regarding device usage in pediatric populations slow down research and development efforts.

The shortage of specialized pediatric expertise among healthcare professionals affects the adoption and proper utilization of pediatric devices. Training in using and maintaining these specialized devices is crucial, as a lack of expertise may lead to underutilization or improper usage. Pediatric device development involves prolonged research, clinical trials, and regulatory processes. For example, pediatric-specific robotic surgical instruments require extensive testing, delaying market entry and hindering growth. Rapid technological advancements also pose a risk, potentially rendering pediatric devices obsolete quickly. Continuous investment in research and development is essential to keep up with evolving technology.

Telemedicine and Remote Monitoring Solutions

The evolving landscape of healthcare technology presents numerous opportunities for growth in pediatric devices. Wearable tech advancements, exemplified by the Owlet Smart Sock, have redefined pediatric care by enabling real-time monitoring of vital signs for infants. This innovation not only diminishes hospital stays but also empowers parents to remotely monitor their baby's health, facilitating early intervention and granting invaluable peace of mind. Similarly, Gecko Health Innovations' smart inhalers have transformed asthma management in children, enhancing medication adherence through usage tracking and personalized data. Moreover, Nuubo's wearable ECG monitors have revolutionized pediatric cardiology by enabling continuous monitoring without impeding a child's mobility, thereby facilitating early diagnosis and timely interventions for heart conditions.

Telemedicine platforms such as TytoCare have emerged as a pivotal solution, offering virtual consultations that bridge the gap between parents and pediatricians, especially in remote regions. Alongside these technological advancements, 3D printing, as demonstrated by e-NABLE, provides cost-effective, personalized prosthetic limbs for children, significantly improving their quality of life. Plusoptix's handheld vision screeners and growth measurement tools like the Shapelog system contribute to early detection and monitoring of vision issues and growth-related concerns, respectively, streamlining screenings and healthcare provision.

Innovations such as Philips' child-friendly MRI designs and immersive experiences have mitigated children's anxiety during scans, improving overall experiences. Similarly, advanced hearing aid technologies, such as those offered by Phonak, cater specifically to children, optimizing auditory experiences in diverse environments. Furthermore, devices like the Bili-Hut have leveraged phototherapy to effectively manage neonatal jaundice, providing portable and user-friendly solutions that reduce the necessity for hospitalization, particularly in resource-limited settings.

Pediatric Medical Device Market Segment Analysis:

Based on Product, the Neonatal ICU Devices segment dominated the Pediatric Medical Device Market in 2025 and is expected to continue its dominance during the forecast period as it is important to the critical needs of premature infants and those requiring intensive care. The rising prevalence of preterm births, accounting for approximately 10% of births in the US according to the Centers for Disease Control and Prevention, necessitates advanced medical devices tailored for this segment. Disparities in preterm birth rates among different demographic groups, such as higher rates among African-American women compared to white or Hispanic women, indicate a continued demand for specialized NICU devices. The introduction of innovative products such as SAANS and SonarMed Airway Monitoring System addresses specific needs within the neonatal ICU segment, providing portable and improved respiratory support for critically ill newborns.

Based on the service type, The Pediatric Medical Device Market displays a diversified range of devices across various types, each serving unique applications and witnessing distinct levels of adoption. Infant Caps, Infant Incubators, and Infant Warmers stand as critical devices offering temperature regulation and support for premature or critically ill newborns, ensuring their well-being. Bili Lights, designed to treat jaundice in infants, hold substantial adoption due to the prevalence of neonatal jaundice. Devices such as New Born Hearing Screeners and Pulse Oximeters for Infants address early detection of hearing impairments and vital sign monitoring, respectively, enhancing timely interventions. Cranial Orthosis devices cater to correcting skull deformities in infants, while Automated External Defibrillators and Atrial Septal Defect Occluders focus on emergency cardiac care and congenital heart defect treatments. Cerebrospinal Fluid Shunts aid in managing conditions such as hydrocephalus. Other devices encompass a wide spectrum, contributing to specialized pediatric care. Adoption rates vary based on the criticality of conditions and technological advancements, with neonatal-centric devices witnessing higher demand owing to the vulnerability of newborns and premature infants.

Pediatric Medical Device Market Regional Insights:

North America dominated the Pediatric Medical Device Market and is expected to maintain its dominance due to several key factors. The region boasts significant production and utilization, underpinned by robust healthcare infrastructure and a flurry of innovative product launches. The prevalence of chronic pediatric conditions in the United States, affecting over 40% of school-aged children according to the CDC, drives the demand for advanced medical devices tailored to manage complex healthcare needs. Notable product introductions, such as Preceptis Medical's Hummingbird Tympanostomy Tube System and the Harmony Transcatheter Pulmonary Valve System FDA approval, showcase the region's focus on innovation and improved patient care. Furthermore, favorable government initiatives and collaborative research endeavors contribute to Pediatric Medical Device market growth.

Europe is a leading region with advanced manufacturing capabilities in countries such as Germany and the United Kingdom, contributing significantly to global exports while maintaining a strong domestic market. Meanwhile, the Asia-Pacific region, led by China and India, serves as a vital manufacturing hub, supplying a considerable volume of pediatric medical devices globally, thanks to cost-effective production processes and skilled labor. The Middle East and South America show promising growth prospects, reflecting a rising demand for pediatric medical devices and offering avenues for Pediatric Medical Device market growth.

Pediatric Medical Device Market Competitive Landscapes:

The Pediatric Medical Devices Market is highly competitive with leading key players such as Abbott Laboratories, Boston Scientific Corporation, Baxter International, Medtronic plc, Cardinal Health, F. Hoffmann-La Roche Ltd., GE Healthcare, Johnson & Johnson Services, Siemens Healthineers, and Koninklijke Philips. These Pediatric Medical Device industry giants continually innovate and strategize to maintain their dominance. Notably, Masimo secured FDA clearance for its SedLine monitoring and pediatric EEG sensor, enhancing neurophysiological monitoring in pediatric care, while Abbott's FDA-approved labeling update for HeartMate 3 heart pump expanded its application for pediatric patients with advanced refractory left ventricular heart failure, signifying a stride in pediatric cardiac care. The competitive landscape is not only shaped by established players but also by emerging ones. Merger and acquisition activities play a crucial role; for instance, Medtronic's acquisition of SonarMed Inc. in December 2020 aimed to introduce the SonarMed Airway Monitoring System for NICUs, elevating respiratory care for newborns. Such strategic moves expand product portfolios and market reach.

Partnerships and collaborations are prevalent, fostering innovation. These alliances facilitate technological advancements, like GE Healthcare's collaboration with Preceptis Medical, Inc., enhancing pediatric ear tube surgeries with the Hummingbird Tympanostomy Tube System. New product developments, such as Baxter International's advancements in neonatal care with its PrisMax System, demonstrate the industry's commitment to pediatric-specific innovations. The competitive landscape showcases a blend of established players' prowess, emerging players' disruptive innovations, merger and acquisition activities, and collaborative efforts, all aimed at advancing pediatric medical devices for better healthcare outcomes for children globally.

Pediatric Medical Device Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2025 | Medtronic | Secured FDA clearance for its next-generation pediatric insulin pump system featuring advanced automated insulin delivery algorithms. | Significantly enhances glycemic control and patient safety for young children managing Type 1 diabetes. |

| 12 May 2025 | GE HealthCare | Launched a specialized, low-dose pediatric CT imaging system designed to minimize radiation exposure while maintaining high-resolution image quality. | Improves diagnostic safety standards and reduces long-term radiation exposure risks for infants and young children. |

| 18 September 2025 | Philips Healthcare | Partnered with leading pediatric hospitals to commercialize its AI-powered pediatric patient monitoring platform. | Drives early detection of critical physiological changes, optimizing ICU workflow and clinical outcomes in neonatal care. |

| 10 February 2026 | Boston Scientific | Received regulatory clearance for its miniature pediatric interventional cardiology catheter tailored for structural heart defect repair. | Expands minimally invasive surgical options, dramatically lowering recovery times and surgical complications in infants. |

| 14 April 2026 | Masimo | Introduced a non-invasive continuous pediatric pulse oximetry sensor integrated with wearable remote monitoring technology. | Accelerates hospital-to-home transitions by offering reliable real-time vital signs tracking for pediatric home healthcare. |

Pediatric Medical Device Market Scope: Inquiry Before Buying

| Pediatric Medical Device Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 41.97 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 8.72% | Market Size in 2034: | US $ 89.07 Bn. |

| Segments Covered: | by Product | In Vitro Diagnostic (IVD) Devices Cardiology Devices Diagnostic Imaging Devices Anaesthesia & Respiratory Care Devices Neonatal ICU Devices Monitoring Devices Telemedicine Home-use Medical Devices |

|

| by Type | Infant Caps Infant Incubators Bili Lights New Born Hearing Screener Infant Warmer Cranial Orthosis Pulse Oximeter for Infants Automated External Defibrillator Atrial Septal Defect Occlude Cerebrospinal Fluid Shunt Others |

||

| by End User | Hospitals Pediatric Clinics Others |

||

Pediatric Medical Device Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Pediatric Medical Device Market Key Players:

Leading Players of Pediatric Medical Device Market in North America:

1. Abbott Laboratories

2. Boston Scientific Corporation

3. Medtronic plc

4. Cardinal Health, Inc.

5. Johnson & Johnson Services, Inc.

Major Companies of Pediatric Medical Device Market in Europe:

1. Siemens Healthineers

2. F. Hoffmann-La Roche Ltd.

3. Koninklijke Philips N.V.

4. Baxter International, Inc.

5. GE Healthcare

Leading Players of Pediatric Medical Device Market in Asia-Pacific:

1. Mindray Medical International Limited

2. Nipro Corporation

3. Terumo Corporation

4. Olympus Corporation

5. Asahi Kasei Corporation

Leading Players of Pediatric Medical Device Market in Middle East & Africa:

1. BD (Becton, Dickinson and Company)

2. Medtronic plc

3. GE Healthcare

4. Siemens Healthineers

5. Abbott Laboratories

Leading Players of Pediatric Medical Device Market in South America:

1. Drägerwerk AG & Co. KGaA

2. Dentsply Sirona

3. 3M Health Care

4. Mindray Medical International Limited

5. Terumo Corporation

Frequently Asked Questions:

1. What is the market size of the Global Pediatric Medical Device Market in 2025?

Ans. The market size Global Pediatric Medical Device Market in 2025 was US$ 41.97 Billion.

2. What are the different segments of the Global Pediatric Medical Device Market?

Ans. The Global Pediatric Medical Device Market is divided into Product, Type, and End User.

3. What is the study period of this market?

Ans. The Global Pediatric Medical Device Market will be studied from 2020 to 2034.

4. Which region is expected to hold the highest Global Pediatric Medical Device Market share?

Ans. The Asia Pacific dominates the market share in the market.

5. What is the Forecast Period of the Global Pediatric Medical Device Market?

Ans. The Forecast Period of the market is 2026-2034 in the market.