Global Organic Chips Market Size by Product Type and Distribution Channel – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2034

Overview

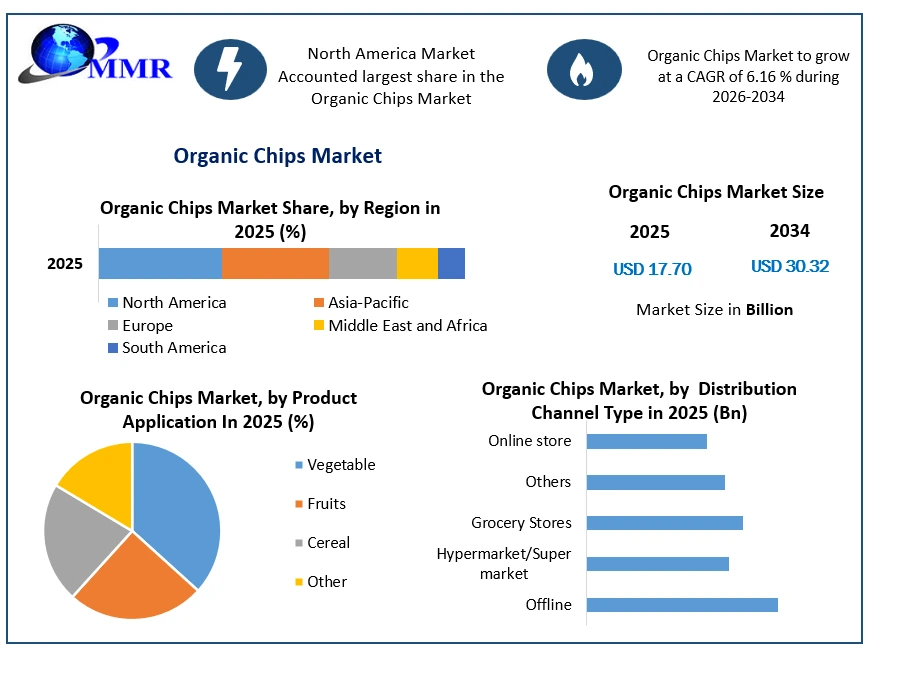

The Organic Chips Market size was valued at USD 17.70 Billion in 2025 and the total Organic Cheese revenue is expected to grow at a CAGR of 6.16% from 2026 to 2034, reaching nearly USD 30.32 Billion By 2034.

Organic chips are a type of snack food made from organic ingredients. They are typically made from vegetables such as potatoes, sweet potatoes, or kale. Organic chips are good source of fiber and vitamins, and they are a healthier alternative to conventional chips, which are often high in fat, sodium, and unhealthy additives.

Organic Chips Market Growth Outlook To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Key Findings Snapshot:

1. In 2025, According to the survey report, more than 52% of Americans followed a diet or eating pattern. The increased dieting has come mainly from consumers under age 50. The most common diets or eating patterns include clean eating (16%), mindful eating (14%), calorie counting (13%), and plant-based (12%). Growing demand for on-the-go snacking is driving growth of the organic chips market growth. According to the MMR analysis, 30% of Americans say it’s hard to prepare meals, given their busy schedules. Convenience and the nutritional value of organic chips are among the top reasons for the growing organic chips consumption.

2. Growing trend of clean label products is expected to uplift the market growth during the forecast. The number of vegans is on the rise globally, and this trend is particularly strong in North America. Vegans avoid all animal products, including meat, dairy, and eggs. Organic chips that are certified vegan are becoming increasingly popular among the growing population base across Europe and North America. In the US, the number of vegans went up 0.4 percent to almost 3.5 percent in the last two years or so. According to the ‘Vegetarianism in America’ study published by Vegetarian Times Magazine, the percentage of vegans in the US is rising fast. Right now, there are about 5%, equal to 15.5 million people in the US following a vegetarian-based diet. However, only 2 million of them that’s approximately 0.5 percent lead a purely vegan lifestyle. This reflects huge market opportunity and potential for Organic chips.

3. The Indian food industry is poised for huge growth, increasing its contribution to world food trade every year. In India, the food sector has emerged as a high-growth and high-profit sector due to its immense potential for value addition, particularly within the food processing industry. There has been a shift of customer preference of customers from snacks to healthy snacks. This has resulted in a creation of a new market for organic Chips. Salted Chips are a part of the snacks consumed by Indians. The unorganized market consists of homemade and loose salty snacks generally sold in small Kiranas. The branded or the organized Snacks segment in India is increasing virtually by the day. Some of the major players in the Indian organic chips market consist of Haldiram Foods, Frito-Lay, Balaji wafers. During fasting periods in India, such as Navratri and Lent, there is a surge in demand for organic chips as they are considered to be a healthier snack option.

4. Developing countries are expected to drive the global potato chips market in the coming years. Earlier, the consumption of potato chips was largely confined to the western countries. However, with the emerging trend of westernisation of food consumption patterns in addition to growing economy, rise in middle class population and increasing urbanisation, the consumption of potato chips in developing countries is expected to grow at a significant rate.

5. The growth of the organized retail sector is currently having a positive impact on the global potato chips market. Earlier, a number of global players were hesitant to sell their products in emerging regions because of lack of infrastructure, storage facilities, and appropriate knowledge about the developing markets. However, with an increase in the number of organised retail stores, many players are investing in organic chip markets.

Organic Chips Market Dynamics:

The “clean label” movement is a perceptible representation of consumer demand for less artificial ingredients

Food and beverage companies have embraced the movement by reintroducing both classic and new products with fewer ingredients. Consumers are increasingly becoming health-conscious and are seeking out products that are made with natural, recognizable ingredients and free from artificial additives and preservatives. Organic chips fit perfectly into this trend, as they are perceived as being healthier and more wholesome than conventional chips. Consumers are willing to pay more for products that they perceive as being healthier and more wholesome. The rising popularity of packaged food items and the increasing demand for healthier snack options are creating a strong growth opportunity for the organic chips market in North America and Europe. Organic chip manufacturers are constantly innovating to develop new flavors and varieties of chips in order to cater to the growing demand for organic snacks. Key players operating in the market are increasingly focusing on sustainability practices, such as using recyclable packaging and sourcing ingredients from sustainable farms.

Increasing sales of Organic Chips through online retailing

The online purchase of organic chips is increasing, from both pure-play online retailers and websites of traditional food retailers. The rising number of mobile users is crucial to the online sale of packaged nutritional foods, such as Organic Chips. Online shopping is convenient for consumers, who can browse and purchase organic chips from the comfort of their own homes. This is especially appealing to busy consumers who may not have time to shop at a brick-and-mortar store. Vendors are also providing their own online platform for reaching their end consumers. Such factors are expected to positively impact the organic market in focus during the forecast period. Online retailing allows organic chip manufacturers to sell directly to consumers, bypassing traditional distribution channels that give manufacturers more control over their brand and pricing. Online retailing is playing an increasingly important role in the growth of the organic chips market. The online sales of organic chips grew by 20% in 2025, while offline sales grew by 5%. More than 43% of consumers have purchased organic chips online in 2025.

Millennials and Gen Z consumers are more expected to purchase organic chips online than older generations.

Millennials and Gen Z consumers are playing a significant role in driving the growth of the organic chips market. These generations are more health-conscious and environmentally aware than previous generations, and they are willing to pay a premium for products that they perceive to be healthier and more sustainable. Organic chips fit this bill perfectly, as they are made without the use of synthetic pesticides, herbicides, and fertilizers. Millennials and Gen Z are more likely to prioritize healthy eating than previous generations. They are aware of the link between diet and health, and they are willing to make choices that they believe will benefit their long-term health. Organic chips are perceived to be a healthier option than traditional chips. Millennials and Gen Z are demanding more innovative and flavorful organic chips that is leading to the development of new products, such as organic chips made with vegetables, fruits, and whole grains. They are active on social media, and they are using these platforms to share their love of organic chips that is helping to raise awareness of organic chips and encourage others to try them.

Porter’s Five Forces Analysis for the Organic Chips Market

1.Bargaining Power of Suppliers: The product suppliers of organic chips market are high in number and are larger and more globalized. So, there will be less threat from the suppliers. Thus, the bargaining power of suppliers is low.

2.Bargaining Power of Buyers: Buyer’s demand cost effective Organic Chips that give instant energy. This has increased the pressure on the organic chips providers to offer the best organic chips in a cost-effective way. Thus, many suppliers are offering best yet cost –effective Organic Chips. This gives the buyers the option to freely choose organic chips that best fits their preference. Thus, the bargaining power of the buyers is high.

3.Threat of New Entrants: Companies entering the organic chips market are adopting various innovations such as developing organic chips that are available in different flavors and textures. Thus, the threat of the new entrants is moderate.

4. Threat of Substitutes: There are different types of food available for instant energy, but Organic Chips is the best choice because it is more effective as suggested by many studies. Thus, the threat of substitutes is low.

5. Competitive Rivalry in the Market: The competitive rivalry among industry leaders is rather intense, especially between the global players. Many companies are launching their value-added services in the international market and strengthening the footprint worldwide. Therefore, competitive rivalry in the market is high.

Organic Chips Market Segment Analysis:

Based on Product Type, Organic chips made from vegetables held the dominant position in the market and projected to continue its dominance during the forecast period. The growing snacking culture is driving the organic chips market growth. The demand for the plain or salted segment of the potato chips are expected to increase its adoption because of the high prevalence of various occasions, such as parties, gatherings, and sporting events. vegetable-based chips are gaining popularity as a healthier and more sustainable alternative to traditional potato chips organic potato chips currently represent one of the world’s most popular snack foods. Vegetable-based chip brands are constantly innovating and developing new flavors and varieties to meet the diverse preferences of consumers that helps to expand the appeal of vegetable-based chips and attract a wider range of consumers. Vegetable-based chip brands are actively marketing their products to consumers, emphasizing their health benefits, environmental advantages, and unique flavors. vegetable-based chips are becoming a popular snack choice among health-conscious and environmentally conscious consumers who are looking for healthier and more sustainable snack options. The growing demand for vegetable-based chips is likely to continue as consumers become more aware of the benefits of eating vegetables and as vegetable-based chip brands continue to innovate and expand their product offerings.

With the popularity of snack food through electronic and other media and rise in population and living standard the demand for snack foods in increasing rapidly including organic potato wafers. Consumers are increasingly aware of the health benefits of eating vegetables, and vegetable-based chips are a good way to incorporate more vegetables into their diets. They are lower in calories and fat than traditional potato chips, and they are a good source of fiber, vitamins, and minerals. Potato chips are consumed as a snack across the globe and are made by deep-frying or baking the potato slices. Market players offer potato chips as plain, salted, and flavored. Potato chips are one of the most convenient food options currently available for people to keep pace with their busy lifestyle. It shortens the meal preparation time and can be served in the form of a quick snack or part of the meal. The raw materials that are used in the manufacturing of potato chips are potatoes, oil and salt, which are widely available in every part of the world. The reliable supply of potatoes and other materials are ensured, thereby providing the potato chips market with a constant supply and efficient production planning.

The banana industry is an important part of the global industrial agro business. Most bananas go into export and international trade for consumption in Western countries. Banana is one of major and financially significant organic product yields of India. Generally, people consume banana wafers as a snack food. In India, Tamil Nadu, Maharashtra, Andhra Pradesh, Gujarat, Bihar, and Karnataka are the major banana producing states.

Organic Chips Market Regional Insights:

North America holds the largest market share for organic chips, accounting for nearly 48% of the global market in 2025. Europe follows with a 29% share. North American consumers are increasingly aware of the health benefits of eating organic food, and organic chips are perceived as a healthier alternative to traditional chips. Organic farming practices are considered more sustainable than conventional farming, as they reduce the use of chemicals that can harm the environment. This is appealing to environmentally conscious consumers in North America, who are looking for ways to reduce their carbon footprint. Organic chips are becoming increasingly available in a variety of retail channels in North America, including grocery stores, convenience stores, and online retailers that makes it easier for consumers to find and purchase organic chips.

Germans are among the most health-conscious consumers in Europe, and they are increasingly seeking out healthy snack options. Germany is the largest market for organic chips in Europe, followed by the United Kingdom, France, Italy, and Spain. Germany has a long history of organic farming, and the government provides substantial support to organic farmers. Organic potato chips are readily available in German supermarkets and convenience stores. The United Kingdom is the second-largest market for organic potato chips in Europe, with a demand share of 25%. Healthy snacks are becoming increasingly popular in the UK, as consumers are looking for healthier alternatives to traditional snacks

Indian consumers are willing to spend more on fitness classes and activities, consuming natural foods, health supplements, according to a survey by MMR. Indian consumers have opened their wallets towards fitness classes and activities, consuming natural foods, health supplements, and following specialized diets, which are driving the demand for organic Chips. According to the survey, 40 per cent of Indian respondents stated that they will pay a premium for products promoting health and wellness, which is higher than their global counterparts at 29 per cent.

Organic Chips Market Competitive Landscapes:

Key players operating in the market are continuously seek to understand their consumers and develop products that address their desire for organic chips products. The food production and marketing industry has to follow a variety of federal, state and local laws and regulations that includes food safety requirements related to the ingredients, manufacture, processing, packaging, storage, marketing, advertising, labeling quality and distribution of their products.

In the United States, the federal agencies governing the manufacture, marketing and distribution of products by the Federal Trade Commission (FTC), the United States Food & Drug Administration (FDA), the United States Environmental Protection Agency (EPA) and the Occupational Safety and Health Administration (OSHA). an evolving nature of compliance regulations and standards, and specific customer compliance requirements are expected to increase the complexity for the production of organic chips. The Hain Celestial Group (Boulder, CO) is a leading manufacturer of organic and natural foods, including chips under the brands Terra, Garden of Eatin', and SnackWell's. General Mills, Inc. (Golden Valley, MN) is an American multinational manufacturer and marketer of branded consumer foods, including organic chips under the brand Quinn Snacks.

Opportunities for Key Players Organic Chips Market to increase their revenue in the sales volume of Organic Chips

Product Diversification: Manufacturers are expected to have an opportunity to introduce the new and innovative flavors to cater to a wider range of consumer preferences. They can also utilize unconventional and nutrient-rich ingredients to differentiate products from competitors.

Expansion in New market: As the market continues to grow, key players are looking to expand into new markets to capitalize on this growth opportunity. The Organic Chips Market has potential to drive the growth across the emerging regions like APAC. The Hain Celestial Group is a leading manufacturer of organic and natural foods, including chips under the brands Terra, Garden of Eatin', and SnackWell's. The company is expanding into new markets in Asia Pacific and Latin America. Kellogg Company is a multinational food manufacturing company that produces a variety of organic chips under the brands Kashi, Bear Naked, and Kettle Foods. The company is expanding into new markets in Europe and the Middle East. Key players can partner with local distributors in new markets to gain access to local markets and distribution channels that help to overcome the challenges of entering a new market, such as understanding local regulations and consumer preferences. Key players should tailor their product offerings to suit the specific preferences and dietary habits of consumers in new markets.

Key players need to build brand awareness in new markets in order to attract consumers.

Online Retailing: Some of the online strategies include develop a user-friendly and visually appealing e-commerce platform that showcases the company's organic chips offerings, highlighting their unique qualities and benefits. Ensure the website is optimized for search engines to improve visibility and organic traffic. Utilize social media platforms like Instagram, Facebook, and Twitter to engage with potential customers, promote new products and flavors, and share engaging content related to organic food and healthy snacking. Run targeted social media ads to reach a wider audience and drive traffic to the e-commerce platform. Collaborate with established online grocery stores and e-commerce platforms like Amazon, Whole Foods Market, and Instacart to expand reach and visibility among a broader customer base and offer exclusive deals or promotions through these partnerships to attract new customers.

Marketing: Key players need to invest in research and development to develop new products and flavors that will appeal to consumers in new markets. Some of the marketing strategies, which helps to drive the market revenue are highlight the health advantages of organic chips, such as their use of natural ingredients, freedom from artificial additives, and potential benefits for heart health, digestion, and overall well-being. Educate consumers about the differences between organic and conventional chips. Collaborate with influential individuals in the health and wellness space, such as food bloggers, social media personalities, and fitness enthusiasts, to promote organic chips and reach a wider audience. Influencer endorsements can enhance brand credibility, drive sales, and generate positive buzz. Consumer advertising and promotion is used to build brand awareness and equity, drive trial to bring in new consumers and increase consumption. Paid social and digital advertising and public relations programs are the main drivers of brand awareness

Organic Chips Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 18 March 2026 | Mondelēz International | The company expanded its clean-label portfolio under the CLIF brand by launching organic, non-GMO Energy Bites and snack bars. | This move scales its better-for-you snack portfolio to capture multi-demographic demand for premium, organic bite-sized products. |

| 22 April 2026 | Simple Mills | Launched a new eco-forward product line utilizing ingredients sourced from regenerative agriculture farms. | The initiative strengthens biodiversity and soil health while meeting rising consumer demand for environmentally conscious snack options. |

| 04 May 2026 | The Hain Celestial Group | Implemented a major shift toward compostable packaging for its flagship organic chip and snack product lines. | Enhances the brand's sustainability profile, directly addressing the preference of 28% of consumers willing to switch brands for eco-friendly practices. |

| 15 January 2025 | Lay's | Expanded its North American distribution by officially introducing its All Dressed flavor profile to the U.S. organic and conventional market. | Broadens market penetration by leveraging global flavor trends to attract diverse, health-conscious consumer segments. |

Organic Chips Market Scope: Inquire Before Buying

| Global Organic Chips Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD17.70 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6.16% | Market Size in 2034: | USD 30.32Bn. |

| Segments Covered: | by Product Type | Vegetable Fruits Cereal Others |

|

| by Distribution Channel | Offline Hypermarket/Supermarket Grocery Stores Others Online store |

||

Organic Chips Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Organic Chips Market, Key Players are

1. Luke's Organic

2. Tyrrells Potato Crisps

3. Kettle Foods

4. The Hain Celestial Group

5. Popchips

6. Rhythm Superfoods

7. General Mills

8. Terra Chips

9. Garden of Eatin'

10. Barbara's Bakery

11. SnackNation

12. Enjoy Life Foods

13. Quinn Snacks

14. Angie's Boom Chicka Pop

15. Deep River Snacks

16. Sensible Portions

17. Simply 7

18. Lesser Evil

Frequently Asked Questions

1. What are the growth drivers for the Organic Chips Market?

Ans. Increasing Health Awareness, Shifting Consumer Preferences towards organic products are expected to be the major drivers for the Organic Chips Market.

2. What is the major restraint for the Organic Chips Market growth?

Ans. High price of organic Products is expected to be the major restraining factor for the Organic Chips Market growth.

3. Which region is expected to lead the global Organic Chips Market during the forecast period?

Ans. Europe is expected to lead the global Organic Chips Market during the forecast period.

4. What is the projected market size & and growth rate of the Organic Chips Market?

Ans. The Organic Chips Market size was valued at USD 17.7 Billion in 2025 and the organic chips market growth is expected to grow at a CAGR of 6.16% from 2026 to 2034.

5. What segments are covered in the Organic Chips Market report?

Ans. The segments covered in the Organic Chips Market report are Product Type, Distribution Channel, and Region.