North America Farm and Agro Equipment Market Size by Equipment Type, Technology, Power Source, Application and End User

Overview

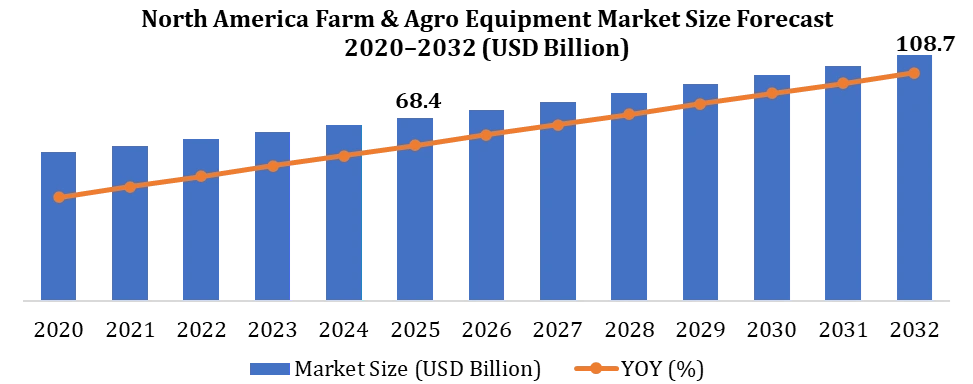

North America Farm and Agro Equipment Market was valued at USD 68.4 Billion in 2025 and is projected to reach around USD 108.7 Billion by 2032, growing at a CAGR of 6.8% during 2026–2032. Market growth is primarily driven by rising agricultural mechanization, increasing adoption of precision farming technologies, labor shortages in farming operations, and growing demand for high-efficiency agricultural equipment across the United States and Canada.

To know about the Research Methodology :- Request Free Sample Report

Agri-Tech Ecosystem Analysis – North America Farm and Agro Equipment Market

The North America Farm and Agro Equipment Market is increasingly supported by a rapidly evolving agri-tech ecosystem integrating advanced digital farming technologies, AI-driven analytics, IoT-enabled equipment, autonomous machinery, and precision agriculture platforms. The ecosystem includes agricultural equipment manufacturers, farm management software providers, precision agriculture technology companies, drone solution providers, GPS and satellite navigation firms, smart irrigation system developers, and agricultural data analytics platforms.

Companies such as Deere & Company, Trimble Inc., Raven Industries, Topcon Agriculture, AGCO Corporation, and CNH Industrial are actively integrating AI, IoT sensors, machine learning, autonomous navigation, and cloud-based farm management systems into agricultural equipment to improve operational efficiency, crop productivity, and resource optimization. In addition, growing adoption of agricultural drones, satellite-based field monitoring, variable rate technology (VRT), and real-time soil analytics is enabling farmers to make data-driven decisions and reduce input costs.

The expansion of connected farming infrastructure, 5G-enabled precision agriculture, and robotics-assisted farming operations is further accelerating agri-tech adoption across North America. Rising investments in sustainable farming technologies, smart irrigation systems, digital agriculture platforms, and autonomous tractors are strengthening the long-term transformation of the regional agricultural ecosystem. Furthermore, increasing collaboration between agri-equipment manufacturers, software developers, AI companies, and precision farming startups is expected to drive innovation and support the development of fully integrated smart farming environments across the region.

North America Farm and Agro Equipment Market Key Highlights

| Market Parameter | Value / Insight | Trend |

| Market Size (2025) | USD 68.4 Billion | Strong Growth |

| Forecast Size (2032) | USD 108.7 Billion | Rapid Expansion |

| CAGR (2026–2032) | 6.8% | Stable Growth |

| Dominant Segment | Tractors | Market Leader |

| Fastest Growing Segment | Precision Farming Equipment | Rapid Adoption |

| Leading Application | Crop Farming | High Demand |

| Emerging Trend | Autonomous & Smart Farming Equipment | Future Opportunity |

North America Farm and Agro Equipment Market Drivers

The North America Farm and Agro Equipment Market experienced significant growth in 2025, driven by increasing farm mechanization, rising labor shortages in agricultural activities, and growing demand for precision farming solutions. Tractors, harvesting machinery, and planting equipment collectively accounted for a major share of total equipment demand across the region.

Market Growth Restraints

High equipment costs, fluctuating raw material prices, elevated maintenance expenses, and limited affordability among small-scale farmers continued to restrict market growth, particularly in price-sensitive agricultural segments.

Market Growth Challenges

Supply chain disruptions, rising fuel prices, climate-related uncertainties, and integration complexities associated with advanced digital farming technologies remained key challenges for market participants across the region.

North America Farm and Agro Equipment Market Segment Analysis

Equipment Type, Tractors dominated the market in 2025 due to their extensive usage across farming operations including plowing, planting, hauling, and harvesting activities. Harvesters and planting equipment also witnessed strong demand supported by large-scale commercial farming operations. Precision farming equipment and irrigation systems experienced rapid growth owing to increasing adoption of smart agriculture technologies and water-efficient farming practices.

by Application, Crop Farming held a significant market share in 2025 owing to rising demand for mechanized farming operations and high agricultural output requirements. Livestock Farming and Horticulture segments also expanded steadily due to increasing investments in automated feeding systems, spraying equipment, and greenhouse farming technologies. Precision Agriculture applications gained strong traction as farmers focused on productivity optimization and cost reduction.

North America Farm and Agro Equipment Market Competitive Landscape

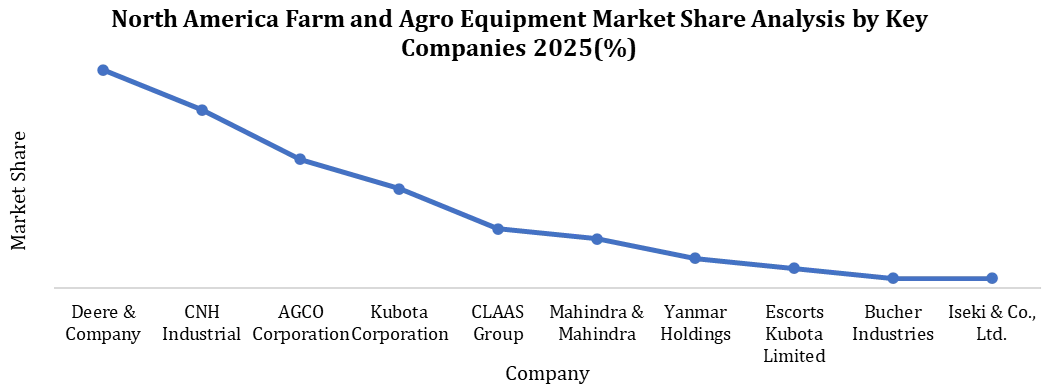

The North America Farm and Agro Equipment Market is highly competitive with the presence of agricultural machinery manufacturers, precision farming technology providers, and farm automation companies. Key players include Deere & Company, CNH Industrial, AGCO Corporation, Kubota Corporation, and CLAAS Group.

Competition is driven by autonomous farming technologies, GPS-enabled equipment, AI-based precision farming systems, strategic partnerships, and investments in sustainable agricultural solutions.

North America Farm and Agro Equipment Market Recent Developments

| Date | Company | Development | Impact |

| Apr-26 | Deere & Company | Expanded autonomous tractor solutions integrated with AI-driven precision farming capabilities. | Strengthened adoption of smart farming and automated agricultural operations across North America. |

| Jan-26 | AGCO Corporation | Introduced advanced precision agriculture platforms with real-time farm data analytics and smart connectivity features. | Accelerated digital transformation and operational efficiency in modern farming practices. |

North America Farm and Agro Equipment Market Country-Level Analysis (2025)

The United States dominated the North America Farm and Agro Equipment Market in 2025 due to high mechanization rates, large-scale commercial farming, and strong adoption of precision agriculture technologies including GPS-enabled tractors, autonomous farming equipment, and smart irrigation systems. The U.S. accounted for the largest regional market share driven by advanced farming infrastructure and increasing investments in AI-based agriculture solutions.

Canada witnessed steady growth supported by rising adoption of precision farming, sustainable agriculture practices, and automated irrigation systems across grain and oilseed farming operations.

Mexico emerged as the fastest-growing country due to increasing agricultural modernization, rising mechanization penetration, and growing demand for tractors, harvesting machinery, and irrigation equipment across commercial farming activities.

Growing labor shortages, rising demand for operational efficiency, increasing precision farming adoption, and expansion of autonomous agricultural equipment continue to drive market growth across North America.

North America Farm and Agro Equipment Market Scope: Inquire before buying

| North America Farm and Agro Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 68.4 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.8% | Market Size in 2032: | USD 108.7 Bn. |

| Segments Covered: | by Equipment Type | Tractors Harvesters Plowing & Cultivation Equipment Planting & Seeding Equipment Irrigation Equipment Spraying Equipment |

|

| by Technology | Conventional Equipment Semi-Autonomous Equipment Autonomous Equipment Precision Agriculture Technologies AI & GPS-Enabled Smart Farming Systems |

||

| by Power Source | Diesel Electric Hybrid |

||

| by Application | Land Development Sowing & Planting Harvesting & Threshing Irrigation Crop Protection Others |

||

| by End User | Small Farms Medium Farms Large Commercial Farms |

||

North America Farm and Agro Equipment Market Key Players

1. Deere & Company

2. CNH Industrial

3. AGCO Corporation

4. Kubota Corporation

5. CLAAS Group

6. Mahindra Agriculture North America

7. Yanmar Holdings

8. JCB Agriculture

9. Lindsay Corporation

10. Trimble Inc.

11. Raven Industries

12. Topcon Agriculture

13. Bourgault Industries

14. Great Plains Manufacturing

15. Buhler Industries

16. Vermeer Corporation

17. Kinze Manufacturing

18. Landoll Corporation

19. Alamo Group

20. Horsch Maschinen GmbH

FAQs- North America Farm and Agro Equipment Market

1. How is precision agriculture transforming the North America farm equipment market?

Precision agriculture is transforming the market through GPS-enabled tractors, AI-based crop monitoring, smart irrigation systems, and data-driven farming technologies that improve productivity, reduce input costs, and optimize farm operations.

2. Which country dominates the North America Farm and Agro Equipment Market?

The United States dominated the market in 2025 due to high agricultural mechanization, large-scale commercial farming operations, and strong adoption of autonomous and precision farming technologies.

3. Why is demand for autonomous farming equipment increasing?

Demand is increasing due to rising labor shortages, growing need for operational efficiency, reduced fuel consumption, and increasing adoption of AI-powered smart farming technologies across large agricultural operations.

4. How are smart farming technologies impacting agricultural productivity?

Smart farming technologies improve crop yield, irrigation efficiency, soil monitoring, fertilizer optimization, and real-time farm management through AI, IoT, machine learning, and precision agriculture systems.

5. Which equipment segment is witnessing the fastest growth?

Precision farming equipment is witnessing the fastest growth due to increasing adoption of GPS-guided machinery, automated irrigation systems, AI-powered analytics, and autonomous farming solutions.