Microproppant Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

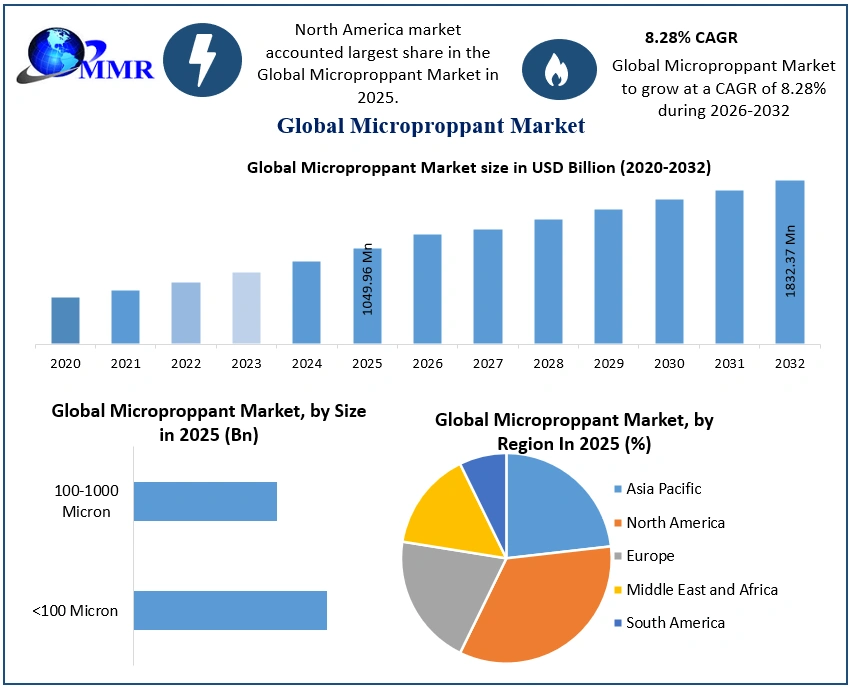

The Microproppant Market size was valued at USD 1049.96 Million in 2025 and the total Microproppant revenue is expected to grow at a CAGR of 8.28% from 2026 to 2032, reaching nearly USD 1832.37 Million by 2032.

Microproppant is an ultrafine mesh, high-quartz silica sand used to prop open induced or secondary fractures created around the main propped fracture in unconventional formations. The microproppant market is experiencing rapid growth driven by increasing global energy demand and the expansion of unconventional reservoir activities all across the world. As traditional oil and gas reserves are not sufficient for growing energy demand, there is a noticeable shift toward exploring unconventional sources such as shale gas and tight oil formations. Microproppants, which are particularly tiny particles used to perform hydraulic fracturing, play an important role in these operations because they prop open microfractures, which are required for optimal hydrocarbon extraction. This trend is especially prominent in the United States, where shale formations like the Permian Basin and Marcellus Shale have witnessed considerable increases in hydraulic fracturing activity enhanced by microproppants. Similarly, countries like Canada, China, and Argentina are adopting hydraulic fracturing techniques to tap into their unconventional reservoirs, further boosting the microproppant market growth on a global scale.

To know about the Research Methodology :- Request Free Sample Report

Microproppant Market Trends:

Increasing Adoption Of Advanced Coated Microproppants

The Microproppants Market is witnessing a significant trend towards the increasing adoption of advanced coated microproppants. Coatings are applied to microproppants to enhance their performance, improve proppant flowback control, and increase well productivity. These advanced coatings provide better adhesion, reduce proppant embedment, and prevent formation damage, resulting in improved fracture conductivity and overall reservoir performance. For examples,

In the Bakken Shale formation in North America, an operator utilized advanced resin-coated microproppants in their hydraulic fracturing operations. The microproppants were coated with a specialized resin that provided increased crush resistance and better proppant embedment control. The advanced coating technology ensured that the microproppants maintained their integrity under high closure stresses, leading to sustained fracture conductivity and improved hydrocarbon production. The successful implementation of coated microproppants in the Bakken Shale demonstrated their effectiveness in enhancing well performance and optimizing reservoir recovery.

In the Vaca Muerta shale play in Argentina, operators have been employing ceramic-coated microproppants in their stimulation treatments. The ceramic coating applied to the microproppants offers excellent resistance to chemical degradation, higher thermal stability, and improved proppant embedment control. The advanced coating technology has proven effective in maintaining long-term fracture conductivity and reducing proppant flowback, resulting in enhanced well productivity and extended production life. The adoption of coated microproppants in the Vaca Muerta formation has become a key factor in maximizing hydrocarbon recovery and optimizing the economic viability of the shale play. Thus, the increasing adoption of advanced coated microproppants highlights the industry's focus on improving microproppant performance and maximizing reservoir productivity, thereby supporting the microproppant market revenue growth.

Microproppant Market Dynamics:

Advanced Fracturing Technologies Drive Surge in Microproppants Demand

Technological advancements in hydraulic fracturing techniques have brought about a paradigm shift in the oil and gas industry, significantly enhancing production efficiency and opening up new avenues for resource extraction. Techniques such as horizontal drilling and multistage fracturing have gained widespread adoption, allowing operators to access previously inaccessible hydrocarbon reservoirs, particularly in unconventional formations like shale and tight sandstone. These advanced fracturing techniques require specialized proppants to effectively stimulate microfractures and optimize hydrocarbon recovery. Microproppants have emerged as a vital component in these processes, as their smaller size enables them to penetrate and prop open the intricate network of microfractures present in unconventional reservoirs. By providing enhanced fracture conductivity and creating pathways for fluid flow, microproppants contribute to maximizing the extraction potential of these reservoirs. Thus, the demand has witnessed a significant upsurge, driving the global microproppant market size.

For example, in the Barnett Shale in the United States, the application of advanced hydraulic fracturing technologies has led to remarkable production rates exceeding 7 billion cubic feet per day (Bcf/d). This achievement has unlocked vast reserves that were previously considered uneconomical to develop. The success in the Barnett Shale exemplifies the role of innovative fracturing techniques in driving the demand for microproppants, as they enable efficient extraction from challenging formations. As the industry continues to invest in research and development to further enhance hydraulic fracturing technologies, the demand for microproppants is expected to surge and boost the microproppant market. Ongoing advancements in proppant design and manufacturing processes, including the development of engineered microproppants with tailored properties, are further expected to propel the growth of the microproppant market.

Increasing Exploration and Production Activities in European Shale Basins Drive Microproppants Market Growth

Europe has witnessed a notable increase in exploration and production activities in its shale basins, driving the microproppant market growth in the European region. Several countries, including the United Kingdom, Poland, and Germany, have been actively exploring their shale reserves and deploying advanced stimulation techniques to tap into the vast hydrocarbon potential. This surge in shale exploration has created a significant opportunity for microproppants in Europe's oil and gas industry. The United Kingdom is home to the Bowland Shale, one of the largest shale formations in Europe. As exploration activities have gained momentum in recent years, operators have recognized the importance of using microproppants to unlock the shale's production potential.

For instance, Cuadrilla Resources, a leading exploration company in the United Kingdom, has utilized microproppants in their hydraulic fracturing operations in the Bowland Shale, contributing to improved well performance and enhanced hydrocarbon recovery. Poland possesses substantial shale gas resources, particularly in the Baltic Basin and the Lublin Basin. In recent years, the country has actively explored these reserves and undertaken hydraulic fracturing operations to assess their commercial viability. Microproppants have played a crucial role in these stimulation operations, allowing for the creation of fractures and the efficient flow of natural gas from the low-permeability shale formations. The use of microproppants has been instrumental in optimizing production rates and maximizing the recovery of natural gas reserves in Poland, thus the demand has witnessed a significant upsurge supporting the microproppants market growth.

Shale Gas Boom Fuels Demand for Microproppants in China's Energy Market

China has been actively exploring its shale gas reserves, particularly in the Sichuan Basin. Shale gas extraction involves the use of hydraulic fracturing, where microproppants are injected into shale formations to create fractures and allow for the release of trapped gas. The demand for microproppants is increasing in China to support the development of its shale gas resources, thereby the China microproppant market holds a significant amount of share. China's shale gas production has been steadily increasing in recent years. For example, in 2020, China's annual shale gas output reached over 20 billion cubic meters (BCM), marking a significant growth compared to previous years.

As China continues to tap into its shale gas potential, the demand for microproppants is expected to rise. Example: The Fuling shale gas field in the Sichuan Basin is one of the largest shale gas developments in China. Microproppants, such as those with a particle size of 325 mesh, are used extensively in hydraulic fracturing operations to prop open fractures and enhance gas flow from the shale formations. The successful application of microproppants in the ruling field has contributed to the growth of shale gas production in China and the subsequent demand for microproppants in the Asia-Pacific market.

Microproppant Market Segment Analysis:

Based on the end-use segment, the Oil and Gas segment dominated the global microproppant market with a significant revenue share of 83.51% in 2025 and is expected to grow at a CAGR of 7.02% during the forecast period. Growing shale gas and tight oil activities all across the world, increasing the demand for microproppants, thereby driving the segment growth. Microproppants are substantially used over traditional proppants in oil and gas extraction processes due to their finer size and enhanced properties. Unlike larger proppants, micro proppants penetrate deeper into tight formations, increasing the effective surface area and improving the conductivity of fractures. This allows for a better flow of oil and gas to the wellbore, enhancing overall production rates. Additionally, microproppants are effective in supporting the fracture walls, preventing closure, and maintaining the long-term productivity of the well.

Several countries, including the United States, are interested in extracting tight oil from shale formations because of the economic benefits, energy security, and enhanced global influence that come with increasing domestic energy production. More than half of the identified shale oil resources outside the United States are concentrated in four countries: Russia, China, Argentina, and Libya; more than half of the non-U.S. shale gas resources are concentrated in five countries: China, Argentina, Algeria, Canada, and Mexico. When compared to other countries, the United States comes in second after Russia for shale oil resources and fourth after Algeria for shale gas resources.

Economies such as the United States, Mexico, Canada, China, India, and Russia have seen increased demand for oil and gas throughout the previous decade. The scarcity of conventional oil and gas, along with their large carbon footprint, has led to an increase in the production of unconventional oil and gas such as shale oil and gas, tight oil and gas, and coalbed methane. Brazil, Algeria, South Africa, Argentina, Mexico, and Australia have considerable reserves of unconventional oil and gas, which is expected to boost the need for microproppants during the forecast period.

Microproppant Market Regional Insights:

North America led the global microproppant market with the highest revenue share of 42.65% in 2025 and is expected to maintain its dominance throughout the forecast period. The surge is attributable to considerable shale gas and tight oil activity, particularly in the United States and Canada, as well as the region's substantial presence of microproppant producers. The U.S. Energy Information Administration (EIA) estimates that about 3.04 million barrels, or 8.32 million barrels per day, of crude oil, are expected to be produced directly from tight oil deposits in the United States in 2023. This corresponded to around 64% of total US crude oil output in 2023. The United States' output of tight oil and shale gas has increased dramatically, thanks to technology advancements that have decreased drilling costs and improved drilling efficiency in key shale plays such as the Bakken, Marcellus, and Eagle Ford.

Leading microproppant market players are adopting various strategies to increase product sales, thereby company revenue. For instance, U.S. Silica Holdings, Inc., headquartered in Texas and a leading producer of commercial silica used in a wide range of industrial applications, has launched InnoProp Python RCS, a new high-performance resin-coated proppant designed to increase oil and gas well production economically and efficiently. InnoProp Python RCS is available in all mesh sizes used in modern frac designs and is approved for all formations with net closure stresses of up to 10,000 psi.

The United States is a leading country in the microproppant market in North America, thanks to the government which is actively exploring unconventional crude oil sources and using hydraulic fracturing techniques, thereby creating significant product demand. The amount of oil produced from hydraulically fractured wells is higher than that from conventionally fractured wells. With the country's developing hydraulic fracturing applications, particularly for shale gas and tight oil, demand for microproppants continues to rise, boosting the growth of the U.S. microproppant market. According to the MMR analysis, around 95% of new wells drilled in the United States are hydraulically fractured, accounting for two-thirds of total marketed natural gas output and approximately half of crude oil production.

Microproppant Market Scope:Inquire Before Buying

| Global Microproppant Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 1049.96 Million. |

| Forecast Period 2026 to 2032 CAGR: | 8.28% | Market Size in 2032: | USD 1832.37 Million. |

| Segments Covered: | by Size | <100 Micron 100-1000 Micron |

|

| by End Use | Oil and Gas Construction Healthcare Others |

||

Microproppant Market, by Region:

North America - United States, Canada, and Mexico

Europe - United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, and the Rest of Europe

Asia Pacific - China, South Korea, Japan, India, Australia, ASEAN, and the Rest of APAC

Middle East and Africa - South Africa, GCC, and the Rest of ME&A

South America - Brazil, Argentina Rest of South America

Leading Microproppant Market, Key Players:

1. Atlas Sand Company

2. Badger Mining Corporation (BMC)

3. CARBO Ceramics Inc.

4. Changqing Proppant Corporation

5. Covia Holdings LLC.

6. Fineway Inc

7. Hexion Inc.

8. MS industries

9. SEPPE Technologies Co., Ltd.

10. Sintex Minerals

11. Superior Silica Sands LLC

12. U.S. Silica Holdings, Inc.

13. US Ceramics, LLC

14. Vista Proppants and Logistics

15. Xinmi Wanli Industry Development Co., Ltd.

FAQs:

1. What are the growth drivers for the Microproppant market?

Ans. The increasing digitalization across industries, rising demand for text-to-speech technologies for accessibility, and integration of advanced AI capabilities. Key sectors like BFSI, logistics, and retail are adopting OCR solutions for enhanced data management and operational efficiency, despite challenges such as accuracy issues with handwritten documents and varying document qualities are expected to be the major drivers for the Microproppant market.

2. What are the factors restraining the global Microproppant market growth during the forecast period?

Ans. The Accuracy issues with handwritten text and limitations in technological infrastructure are expected to be the major factors restraining the global Microproppant market growth during the forecast period.

3. Which region is expected to lead the global Microproppant market during the forecast period?

Ans. North America is expected to lead the global Microproppant market during the forecast period.

4. What is the projected market size and growth rate of the Microproppant Market?

Ans. The Microproppant Market size was valued at USD 1049.96 Million in 2025 and the total Microproppant revenue is expected to grow at a CAGR of 8.28% from 2026 to 2032, reaching nearly USD 1832.37 Million by 2032.

5. What segments are covered in the Microproppant Market report?

Ans. The segments covered in the Microproppant market report are Size, End-Use, and Region.