PV Module Encapsulant Film Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

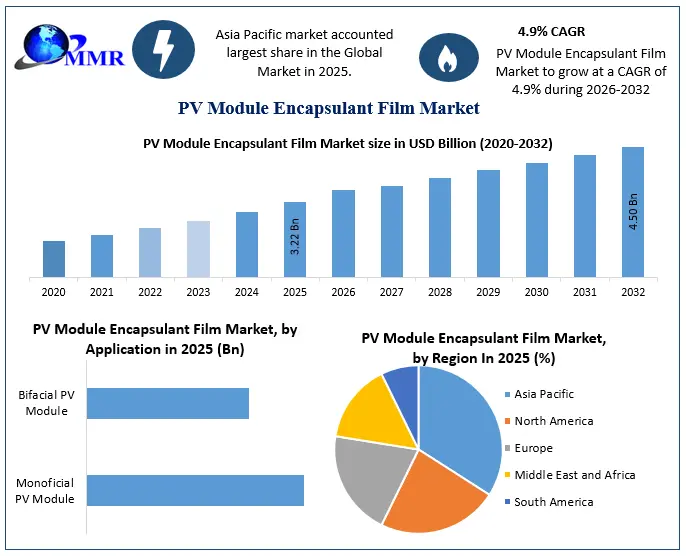

PV Module Encapsulant Film Market size was valued at USD 3.22 Billion in 2025 and the total PV Module Encapsulant Film revenue is expected to grow at a CAGR of 4.9% from 2026 to 2032, reaching nearly USD 4.50 Billion.

PV Module Encapsulant Film Market Overview

A photovoltaic (PV) module encapsulant film is an acute component used in the construction of solar panels. It acts as a protective layer that encapsulates and seals solar cells, ensuring their durability and longevity in several environmental conditions. The encapsulant film enhances the reliability, efficiency and overall performance of solar panels. The encapsulant film offers a barrier that shields the mild solar cells from environmental factors including moisture, dust, dirt and mechanical impacts. This protection supports to prevent damage to the solar cells and other internal components. Advancements in photovoltaic technologies, technological innovations in encapsulation materials and increasing awareness of climate change are the driving factors for the PV Module Encapsulant Film Market growth.

The report includes historical data, present and future trends, competitive environment of the PV Module Encapsulant Film industry. The bottom-up approach was used to estimate the market size. For a deeper knowledge of PV Module Encapsulant Film market penetration, competitive structure, pricing and demand analysis are included in the report. The qualitative and quantitative methods are included in the report for the analysis of the data of the PV Module Encapsulant Film industry. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

PV Module Encapsulant Film Market Dynamics

Drivers

Increasing demand for Solar Energy to boost PV Module Encapsulant Film Market growth

As more solar panels are expanded for commercial, residential and utility-scale projects, the requirement for encapsulant materials to keep and improve the performance of these panels also raises. Many countries are employing motivated renewable energy targets and policies to minimize greenhouse gas emissions and combat climate change. These policies encourage the solar energy industry growth, thereby enhancing the encapsulant film market. Solar energy is a hygienic and environmentally friendly source of electricity generation. Compared to conventional fossil fuels, solar energy provides substantial cost savings.

As the cost of solar installations becomes more individual, more competitive and businesses choose solar solutions which contribute PV Module encapsulant film market's growth. Increasing awareness of the advantages of solar energy such as its long-term economic benefits and favorable environmental impact, promotes more people to invest in solar panel installations, thereby raising the requirement for encapsulant materials. Ongoing advancements in solar technology including higher efficiency solar cells and improved panel durability, also boost greater adoption.

These advancements often need higher-performing encapsulant films to match the improved properties of solar panels. The growth of urban populations and increasing energy demand in rapid swift search for sustainable energy solutions. Solar energy, with its potential to be coupled within urban areas, experiences higher demand increasing the use of encapsulants. As China goals to increase its solar power capacity, there is a sophisticated demand for solar panel installations. This directly boosts the demand for PV module encapsulant films, which are crucial materials used to enhance the performance of solar panels and drive the PV Module Encapsulant Film Market growth. Goverment incentives and policies to fuel PV Module Encapsulant Film Market growth

Goverment incentives and policies to fuel PV Module Encapsulant Film Market growth

To encourage the use of renewable energy sources such as solar power, many governments provide subsidies and incentives. These incentives have involved tax credits grants and low-interest loans for solar installations. Such financial support minimizes the upfront costs for consumers and businesses, making solar energy more available and attractive. As a result, more solar panels are installed, leading to increased demand for encapsulant films. Governments establish feed-in tariff (FiT) programs, where energy producers for instance homeowners, businesses, or utility-scale projects are paid a fixed rate for the electricity they generate from solar panels and feed back into the grid.

FiTs offer a steady income stream and promote more people to invest in solar energy systems, thereby boosting the PV Module encapsulant film market growth. Many authorities set renewable energy targets or need utilities to produce a certain percentage of their electricity from renewable sources. To meet these targets, utilities and energy companies invest in solar energy projects, generating demand for solar panels and encapsulant films.Net metering policies allow solar energy system owners to receive credit for the additional electricity they generate and feed back into the grid. This promotes individuals and businesses to install larger solar systems, resulting in increased use of encapsulant films.

Governments have implemented green building codes that need or incentivize the use of renewable energy sources in new construction and renovations which fuel PV Module Encapsulant Film Market growth. Solar panels and by extension encapsulant films are components of these energy-efficient building needs.

PV Module Encapsulant Film Market Trend

Advancements in Materials and Formulations

New materials and formulations have led to encapsulant films that are more resistant to degradation from UV radiation, humidity, temperature fluctuations and other environmental stresses. Enhanced durability have been extend the lifespan of solar panels and minimized maintenance needs. UV resistance is essential to prevent the yellowing and degradation of encapsulant films over time. Advanced materials have been better UV protection, ensuring the long-term optical clarity and efficiency of solar panels. Solar panels have been experiencing temperature variations that impact their efficiency and performance.

Encapsulant films with enhanced thermal stability have been supporting panels to maintain their effectiveness under stimulating thermal conditions. Strong adhesion between encapsulant films and solar cell materials is crucial to prevent delamination and ensure the structural integrity of the panels. Advancements in adhesion technology have led to more reliable and long-lasting encapsulation which boost PV Module Encapsulant Film Market growth. Optimized materials have reduced the loss of solar energy due to light reflection and absorption within the encapsulant film itself. This has been resulting in higher energy conversion efficiency and improved overall panel performance.

Advanced materials have been offering encapsulant films with increased flexibility without sacrificing robustness. This flexibility is vital to accommodate the expansion and contraction of solar cells due to temperature changes without causing stress or damage to the panel.

PV Module Encapsulant Film Market Restraint

Volatility of raw material prices to hamper PV Module Encapsulant Film Market growth

Sharp and unpredictable fluctuations in the prices of raw materials including ethylene-vinyl acetate (EVA) or other polymer materials utilized in encapsulant films, have led to uncertainty in production costs. Manufacturers have struggled to accurately estimate their costs, affecting pricing strategies and profit margins. When raw material prices increase substantially, manufacturers face higher production costs without the capability to immediately pass those costs onto customers. This has consumed profit margins and impacted the financial health of companies in the encapsulant film market. If raw material prices increase for some manufacturers but not for others, those facing higher costs have become less competitive in the market. This has been resulting in market share shifts and potentially impedes the growth of some companies. As a result, the Volatility of raw material prices hamper PV Module Encapsulant Film Market growth.

PV Module Encapsulant Film Market Recent Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 28 April 2026 | Betterial Film Technologies | The company successfully maintained its top-three global shipment position and secured the second rank for non-China shipments amidst structural consolidation in the encapsulant industry. | This performance highlights structural supply chain stability and expands the availability of high-performance protective films for international solar module manufacturers. |

| 15 February 2026 | Hanwha Solutions | The company successfully commissioned a massive 140,000 metric ton annual capacity expansion for solar-grade copolymer materials at its Yeosu manufacturing facility. | The expansion scales total capacity to 520,000 metric tons per year, significantly securing raw material supply for advanced EVA encapsulant film production. |

| 05 January 2026 | Dow Inc. | The company introduced its next-generation bio-attributed solar encapsulant platform featuring 30% bio-based content and enhanced hydrolytic stability. | This material breakthrough addresses premium utility-scale requirements by delivering low-carbon compliance alongside strong protection against environmental degradation. |

| 18 December 2025 | LyondellBasell | The company finalized plans to invest USD 320 million in specialty polymer production at its Wesseling site in Germany to target high-value downstream sectors. | This capital injection establishes localized, reliable European production of premium resins vital for the production of next-generation PV module encapsulant films. |

| 02 October 2025 | Department of Commerce (India) | The Indian government officially initiated a comprehensive anti-dumping investigation on solar encapsulant film imports originating from South Korea, Vietnam, and Thailand. | This regulatory action protects domestic material suppliers and accelerates self-reliance initiatives across the regional solar module component ecosystem. |

PV Module Encapsulant Film Market Regional Insights

Asia Pacific held the largest PV Module Encapsulant Film Market share in 2024 and is expected to have the highest CAGR during the forecast period. The increasing energy demand, favorable government policies, and efforts to minimize carbon emissions are the boosting factors for the growth of solar energy installations in the Asia Pacific. The requirements for encapsulant films to secure and enhance the performance of solar panels has grown increasingly with this expansion. Developing economies in the Asia Pacific, especially China are global manufacturing cores for solar panels.

The high production volume of solar panels in this region directly translates to a significant demand for encapsulant films. Many countries have implemented supportive policies and incentives to encourage solar energy adoption. Feed-in tariffs, tax advantages and renewable energy goals create a conducive environment for solar installations, fuelling the encapsulant film market. The region has some of the world's most populous countries with growing energy requirements. Solar energy, maintained by encapsulant films, provides a clean and renewable solution to meet this demand.

Asia-Pacific countries have been enthusiastically involved in advancing solar technology. This involves developments in encapsulant film materials, enhancing the efficiency, durability and overall performance of solar panels. Rapid growth in urbanization and infrastructure development in the region creates a requirement for sustainable energy solutions which boosts the PV Module Encapsulant Film Market growth. Solar panels with encapsulant films have been incorporated into buildings, factories, and other structures to produce clean energy. Some Asia-Pacific countries are key exporters of solar panels and related products.

This export-oriented method contributes to the demand for encapsulant films to meet domestic as well as international market needs. Increasing awareness of environmental concerns and the need to minimize carbon emissions boost the adoption of renewable energy sources including solar power. Encapsulant films ensure the efficiency and reliability of solar installations. The region attracts significant investment in solar energy infrastructure. This investment helps the growth of the encapsulant film market as solar projects are developed and expanded.

PV Module Encapsulant Film Market Segment Analysis

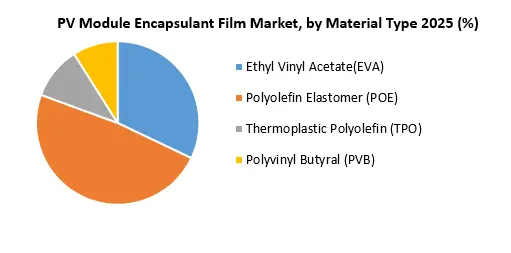

Based on Material Type, the market is segmented into Ethyl Vinyl Acetate (EVA), Polyolefin Elastomer (POE), Thermoplastic Polyolefin (TPO) and Polyvinyl Butyral (PVB). Ethyl Vinyl Acetate (EVA) dominated PV Module Encapsulant Film Market in 2024 and is expected to continue its dominance over the forecast period. EVA has admirable adhesion properties, allowing it to bond well with both solar cell materials and the back sheet. This strong adhesion supports protecting the solar cells from moisture, dust and other environmental factors. EVA is optically transparent, which means it allows sunlight to pass through with minimal reflection or absorption. This property supports maximizing the amount of sunlight that reaches the solar cells, improving energy conversion efficiency.

EVA is flexible and capable of accommodating solar panels' expansion and contraction as they heat up and cool down. This flexibility helps minimize stress on the solar cells and prevents delamination. EVA is easy to process and laminate, making it suitable for large-scale manufacturing of solar panels. Its relatively low processing temperature minimizes the risk of damaging elusive solar cell materials during encapsulation. They have historically been cost-effective compared to some other encapsulant materials. This has contributed to its adoption, especially in utility-scale solar installations where cost considerations are essential and drive PV Module Encapsulant Film Market growth. Due to its long history of utilization, EVA has a well-established supply chain, ensuring a reliable source of material for manufacturers.

By Application, the market is segmented into the Monoficial PV Module and Bifacial PV Module. Monoficial PV Module held the largest PV Module Encapsulant Film Market share in 2024 and is expected to have the highest growth rate over the forecast period. Monofacial PV modules are a well-established and extensively adopted technology in the solar industry. They have been in use for periods and are familiar to manufacturers, installers, and consumers.

Monofacial modules are typically more cost-effective to produce and install than bifacial modules. The simplicity of design and the absence of additional features such as rear-side transparent materials contribute to lower manufacturing costs. Monofacial modules are versatile and have been installed in a variety of locations and orientations. They do not need specific ground conditions or structures to capture rear-side sunlight, making them suitable for a wide range of applications. Manufacturers, engineers, and installers have extensive experience working with monofacial modules, which streamline design, installation, and maintenance processes.

Monofacial modules have well-established performance metrics and standards that make it easier to predict their energy output and integrate them into existing solar energy systems. Much of the solar energy infrastructure, such as mounting systems and tracking technologies, has been optimized for monofacial modules. This makes the transition to bifacial modules more multifaceted and potentially costly. Monofacial modules have a strong market presence and are widely adopted by consumers, investors, and regulatory bodies. This market adoption contributes to their dominance in installations and fuel PV Module Encapsulant Film Market growth.

PV Module Encapsulant Film Market Competitive Analysis

The Market's competitive analysis includes the PV Module Encapsulant Film Market size, growth rate and key trends. The report provides information about the Key companies, such as their size, PV Module Encapsulant Film market share, and geographic presence. The report provides such type of competitive landscape of all PV Module Encapsulant Film Key Players to assist new market entrants. Some of the key players are 3M(US), Borealis(Austria), Hangzhou Betterial Film Technologies Co., Ltd.(China), Jiangsu Sveck Photovoltaic New Material(China), Hangzhou First Applied Material(China), Shanghai HIUV New Materials Co(China), Mitsui Chemicals Company(Japan), Arkema(France), Cybrid Technology(Taiwan), Coveme(Italy), RenewSys (India), H.B. Fuller (US), Guangzhou Lushan New Materials Co., Ltd.(China), DuPont de Nemours, Inc.(US), First Solar, Inc(US) and Others.

Many companies conducted research and development activities to increase their product portfolio. For instance, in Changzhou Betterial Film Technologies Co., Ltd. (China) 2024, the company announced the development of a new PV module encapsulant film which is known as Billirial. It is a thermoplastic polyolefin (TPO) film that is designed to be more resistant to PID than traditional EVA films. Billirial is made from a new kind of TPO polymer that has been precisely designed for use in PV modules. Billirial is also easier to process than EVA films, which has been helping to minimize the cost of solar modules.

Global PV Module Encapsulant Film Market Scope: Inquire before buying

| Global PV Module Encapsulant Film Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 3.22 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.9% | Market Size in 2032: | USD 4.50 Bn. |

| Segments Covered: | by Material Type | Ethyl Vinyl Acetate(EVA) Transparent EVA White EVA Anti-PID EVA Polyolefin Elastomer (POE) Thermoplastic Polyolefin (TPO) Polyvinyl Butyral (PVB) |

|

| by Thickness | 0.20 -0.40mm 0.40-0.60 mm 0.60-0.80 mm |

||

| by Weight | Below 400 g/m2 400-475 g/m2 Above 475 g/m2 |

||

| by Application | Monoficial PV Module Bifacial PV Module |

||

| by End User | Commercial Industrial Residential |

||

PV Module Encapsulant Film Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

PV Module Encapsulant Film Key Player

1. 3M(US)

2. Borealis(Austria)

3. Changzhou Betterial Film Technologies Co., Ltd.(China)

4. Jiangsu Sveck Photovoltaic New Material(China)

5. Hangzhou First Applied Material(China)

6. Shanghai HIUV New Materials Co(China)

7. Mitsui Chemicals Company(Japan)

8. Arkema(France)

9. Cybrid Technology(Taiwan)

10. Coveme(Italy)

11. RenewSys (India)

12. H.B. Fuller (US)

13. Guangzhou Lushan New Materials Co., Ltd.(China)

14. DuPont de Nemours, Inc.(US)

15. First Solar, Inc(US)

16. STR Holdings, Inc.(US)

17. Bridgestone Corporation( Japan)

18. Mitsui Chemicals, Inc.( Japan)

19. Toyo Aluminium K.K. (Japan)

20. SKC Inc. (South Korea)

21. Kuraray Co., Ltd. ( Japan)

22. Hiuv New Materials Co., Ltd. ( China)

Frequently Asked Questions:

1] What is the growth rate of the Global PV Module Encapsulant Film Market?

Ans. The Global PV Module Encapsulant Film Market is growing at a significant rate of 4.9 % during the forecast period.

2] Which region is expected to dominate the Global PV Module Encapsulant Film Market?

Ans. Asia Pacific is expected to dominate the PV Module Encapsulant Film Market during the forecast period.

3] What is the expected Global PV Module Encapsulant Film Market size by 2032?

Ans. The PV Module Encapsulant Film Market size is expected to reach USD 4.50 Bn by 2032.

4] Which are the top players in the Global PV Module Encapsulant Film Market?

Ans. The major top players in the Global PV Module Encapsulant Film Market are 3M(US), Borealis(Austria), Hangzhou Betterial Film Technologies Co., Ltd.(China), Jiangsu Sveck Photovoltaic New Material(China), Hangzhou First Applied Material(China), Shanghai HIUV New Materials Co(China), Mitsui Chemicals Company(Japan), Arkema(France), Cybrid Technology(Taiwan), Coveme(Italy), RenewSys (India), H.B. Fuller (US), Guangzhou Lushan New Materials Co., Ltd.(China), DuPont de Nemours, Inc.(US), First Solar, Inc(US)and others.

5] What are the factors driving the Global PV Module Encapsulant Film Market growth?

Ans. Increasing demand for solar energy and government incentives and policies are expected to drive market growth during the forecast period.