Shale Gas Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

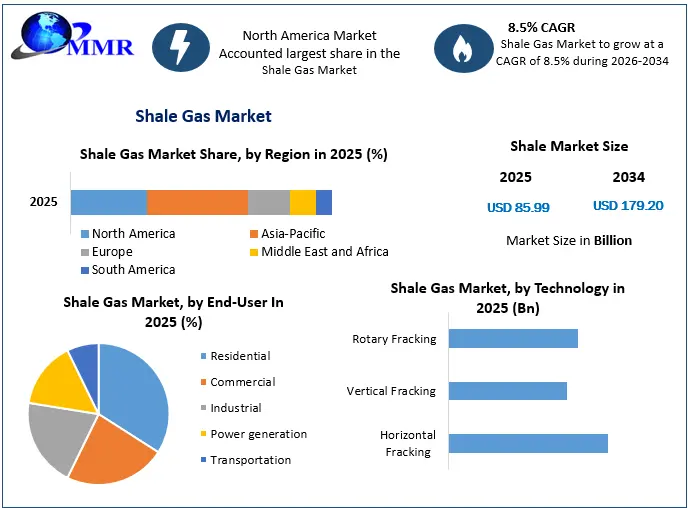

The Shale Gas Market size was valued at USD 85.99 Billion in 2025 and the total Shale Gas revenue is expected to grow at a CAGR of 8.5% from 2026 to 2034, reaching nearly USD 179.20 Billion.

Shale Gas Market Overview:

The Shale Gas Market is expected to reach US$ 179.20 Bn. by 2034. Natural gas, primarily methane, is found below in shale rock and is known as "shale gas." Because it is found in shale, a less permeable rock formation than the sandstone, siltstone, or limestone where "conventional" gas is found, and because it is typically dispersed over a considerably broader region, it is categorised as unconventional gas. This report focuses on the different segments of the Shale Gas market (Technology, End-user, Components and Region). In-depth analysis of the leading industry participants and regions is provided in this report (North America, Asia Pacific, Europe, Middle East & Africa, and South America).It provides a comprehensive analysis of the various sectors' tremendous modern-era growth. The key data analysis from 2020 to 2025 is highlighted through figures, images, and presentations. The market drivers, restraints, opportunities, and challenges for Shale Gas are examined in this report.The MMR report's investment suggestions are based on a thorough examination of the current competitive environment in the Shale Gas market.

Market Growth Outlook

To know about the Research Methodology:- Request Free Sample Report

Shale Gas Market Dynamics:

gas markets as of early June had either decreased demand or, at best, sluggish growth, as is the situation with the People's Republic of China (hence referred to as "China"). With a 7 percent year-over-year loss so far in 2025, Europe is the market that has been impacted the hardest. Major spot indices for natural gas are at record lows du

The use of unconventional natural gas reserves including shale gas, tight gas, and coal bed methane has increased due to the increase in global energy demand and the depletion of traditional gas reservoirs. The market is also expected to grow as a result of rising technological developments in shale drilling. Commercial amounts of shale gas that are trapped deep inside the shale source rock are obtained using hydraulic fracturing, combined with additional techniques of directional drilling and horizontal drilling.

The process of extracting shale gas produces hazardous pollutants and uses a lot of water. Environmental concerns have increased as a result, and activists have become more vocal in their opposition, which is expected to hamper market growth. The market demand is expected to be driven by technological developments for non-conventional gas drilling in deep water and ultra-deepwater.

Shale Gas Market Segment Analysis:

The Shale Gas Market is segmented by Technology, and End-user.

Based on the Technology, the market is segmented into Horizontal fracking, Vertical fracking, and Rotary fracking. Vertical fracking Technology segment is expected to hold the largest market share of xx% by 2034. This is due to its advantages over other fuels, which include low cost and little carbon breakdown as compared to other fuels.

Horizontal fracking Technology segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. In comparison to vertical drilling, directional or horizontal drilling gives producers more freedom and precision when reaching and extracting oil/gas. By drilling in many directions from one well pad, horizontal drilling also lessens the ecological impact of a drilling operation above ground.

Based on the End-user, the market is segmented into Residential, Commercial, Industrial, Power generation, and Transportation. Power generation End-user segment is expected to grow rapidly at a CAGR of 8.5% during the forecast period 2026-2034. It is expected that the rising trend of power plants converting from coal to gas will significantly impact market growth. Governments aim for a rising share of shale gas in the nation's energy mix. Due to its cleaner burning than other fossil fuels, power generation drives the majority of demand in international markets.

Industrial End-user segment is expected to grow rapidly at a CAGR of 8.5% during the forecast period 2026-2034. During the forecast period, the industrial segment is expected to be driven by the conversion of shale gas into value-added outputs. Opportunities to utilise this plentiful resource to increase industrial output would result in higher value-added goods that could subsequently be exported abroad more easily than the main energy source for practically any country rich in shale gas. For instance, natural gas is needed as a feedstock in the manufacturing of chemicals, fertilisers, and a number of other goods.

Residential End-user segment is expected to grow rapidly at a CAGR of 8.5% during the forecast period 2026-2034. The majority of the natural gas used in the residential sector is used for space and water heating. During the forecast period, it is expected that a rising network of natural gas pipelines with direct supply to households will significantly increase the shale gas market.

Shale Gas Market Regional Insights:

The North American region is expected to dominate the Shale Gas Market during the forecast period 2026-2034. The North American region is expected to hold the largest market share of 8.5% by 2034. Due to the use of horizontal drilling and hydraulic fracturing to extract ultra-hard shale from deep underground reserves spread across the nation, the U.S. is the main contributor to regional growth.

The International Trade Center states that due to increased exploration and production, the United States held the top spot in the global rankings of gas producers in 2025. Prior to the emergence of shale gas, the United States was a net importer of natural gas; now, it is an exporter. Major U.S. players are spending extensively in unconventional development since it is a dependable way to reduce carbon footprint.

Due to the advancement of drilling and well completion methods, including long-reach horizontal wellbores and multistage hydraulic fracturing, Canada offers long-term prospects for the delivery of natural gas across North America. In Canada, shale gas deposits can be discovered in a number of provinces and territories as well as British Columbia, Saskatchewan, Alberta, Ontario, New Brunswick, Manitoba, Quebec, and Nova Scotia.

Asia Pacific region is expected to grow rapidly at a CAGR of 8.5% during the forecast period 2026-2034. China is estimated to have the most technically recoverable resources in the entire globe. China's government has established large output goals. Large market participants have attractive opportunities to explore and produce unconventional gas in the nation due to these established targets, which also draw significant investments from around the globe.

The objective of the report is to present a comprehensive analysis of the Shale Gas Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Global Shale Gas Market dynamic and structure by analyzing the market segments and projecting the Global Shale Gas Market size. Clear representation of competitive analysis of key players by Distribution Channel, price, financial position, product portfolio, growth strategies, and regional presence in the Shale Gas Market make the report investor’s guide.

Shale Gas Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 31 January 2025 | Baker Hughes | Secured a major gas technology contract to supply six gas compression trains and six propane compressors for the third expansion phase of Aramco's Jafurah unconventional shale gas field. | Boosts processing capability at the largest unconventional field outside the US, accelerating infrastructure development for lower-emission shale gas utilization. |

| 23 December 2025 | Baker Hughes | Received a Full Notice to Proceed to supply six refrigerant turbo compressors powered by high-efficiency LM9000 turbines for the Commonwealth LNG export project in Louisiana. | Optimizes downstream infrastructure needed to convert regional US shale gas into exportable LNG at a large-scale 9.5 MTPA terminal. |

| 27 April 2026 | Shell plc | Signed a definitive agreement to acquire ARC Resources Ltd, a top-tier operator in the Montney shale formation, in an equity transaction valued at approximately US$13.6 billion. | Expands strategic exposure to low-cost, low carbon intensity shale gas fields in Canada while feeding downstream LNG production corridors. |

| 07 May 2026 | Devon Energy Corporation | Successfully completed its massive all-stock merger with Coterra Energy Inc., establishing a combined premier shale giant valued at approximately $58 billion. | Consolidates operations in the core of the Delaware Basin, targeting $1 billion in annual pre-tax synergies by the end of 2027 through optimized asset management and extraction efficiencies. |

Shale Gas Market Scope: Inquire before buying

| Global Shale Gas Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 85.99 Billion |

| Forecast Period 2026 to 2034 CAGR: | 8.5% | Market Size in 2034: | USD 179.20 Billion |

| Segments Covered: | by Technology | Horizontal fracking Vertical fracking Rotary fracking |

|

| by End-user | Residential Commercial Industrial Power generation Transportation |

||

| by Component | Compressors & Pumps Electrical Machinery, Heat Exchangers Internal Combustion Engines Measuring & Controlling Devices |

||

Shale Gas Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players

Royal Dutch Shell PLC

ConocoPhillips

PetroChina Company Limited

Exxon Mobil Corporation

Chevron Corporation

Chesapeake Energy Corporation

Reliance Industries Limited

SM Energy

Talisman Energy Inc.

BHP Billiton Limited

Anadarko Petroleum Corporation

Antero Resources

Cabot Oil & Gas

Devon Energy

Encana Corporation

Baker Hughes Incorporation

Frequently Asked Questions:

1] Which region is expected to hold the highest share in the Shale Gas Market?

Ans. The North American region is expected to hold the highest share in the Shale Gas Market.

2] Who are the top key players in the Shale Gas Market?

Ans. Royal Dutch Shell PLC, ConocoPhillips, PetroChina Company Limited, Exxon Mobil Corporation, and Chevron Corporation are the top key players in the Shale Gas Market.

3] Which segment is expected to hold the largest market share in the Shale Gas Market by 2034?

Ans. Vertical fracking Technology segment is expected to hold the largest market share in the Shale Gas Market by 2034.

4] What is the market size of the Shale Gas Market by 2034?

Ans. The market size of the Shale Gas Market is expected to reach USD 179.20 Billion. by 2034.

5. What was the Global Shale Gas Market size in 2025?

Ans: The Global Shale Gas Market size was USD 85.99 Billion in 2025.