Global Legumes Market Size by Type, Category, End-User, and Distribution Channel – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

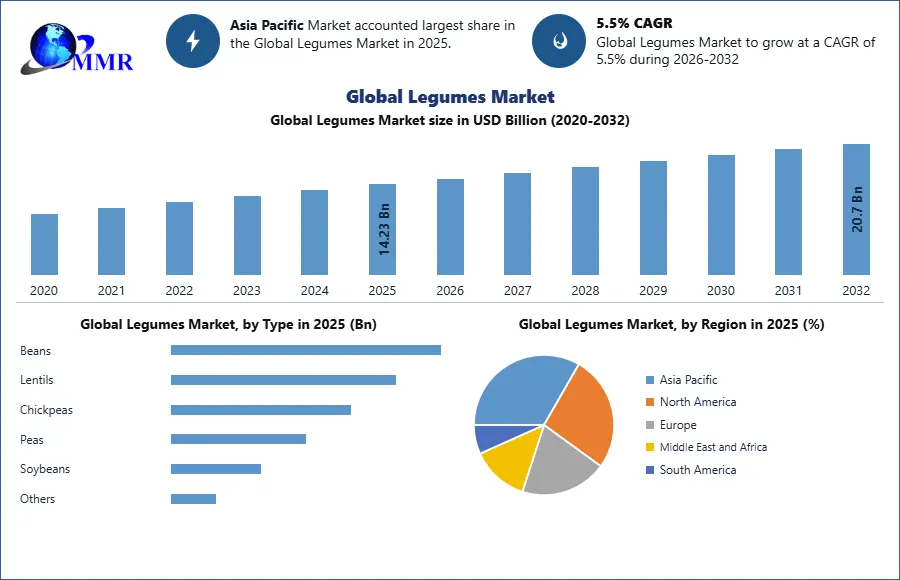

The Legumes Market size was valued at USD 14.23Billion in 2025 and the total Legumes revenue is expected to grow at a CAGR of 5.5% from 2026 to 2032, reaching nearly USD 20.7 Billion.

Legumes Market Overview

Legumes, encompassing various species within the Fabaceae family, offer a diverse range of nutritionally rich seeds in dehiscent and indehiscent fruits. These legume variants vary in shape and size, from elongated pods to massive 2-meter-long fruits like those found in the monkey ladder plant. In the Legumes Market, these diverse offerings contribute to an extensive range of protein-rich seeds and essential amino acids, catering to various consumer needs and preferences. Amongst these, peanuts and carobs stand distinct, choosing not to naturally open upon maturation, yet holding a treasure trove of nourishment within. Legumes, including the likes of snow peas, edamame, and green beans, present a spectrum of culinary possibilities, often harvested while still succulent to grace our tables with their vibrant flavors. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

In their culinary charm, legumes serve as a beacon of sustenance, offering not only food for both humans and animals but also yielding oils, fibers, and raw materials vital for various industries. Their unparalleled nutritional richness high protein content and housing of essential amino acids make them a beacon in plant-based diets, presenting a versatile, affordable, and widely available alternative to meat. Beyond their dietary significance, legumes, through their unique ability to fix nitrogen in association with friendly soil bacteria, confer environmental benefits. This symbiotic relationship Categories nodules within their roots, acting as miniature nitrogen factories, enriching the soil and reducing the reliance on commercial nitrogen applications, thereby mitigating the ecological footprint in agriculture. As crops such as lentils, chickpeas, and peas intertwine with grain rotations, they offer a suite of advantages disease control, pest management, and enhanced nutrient values benefiting not only themselves but also the companion crops, exemplifying the interwoven harmony within ecosystems.

The life cycle of legumes, from precise harvesting methods ensuring ideal moisture content for storage to post-harvest care, reflects a story of preservation and precision. Harvest timing, crucial in the Legumes Market, is an art, balancing the risk of premature harvesting with underdeveloped crops against potential losses due to excessive dryness from delayed harvesting. This meticulous process highlights the importance of preserving quality in the legume supply chain. The storage facilities, a sanctuary for these precious yields, demand careful maintenance of moisture levels and temperatures to thwart spoilage and maintain quality. Be it the vigilant monitoring of moisture content in pulses like peas, chickpeas, and lentils or the strategic use of aeration to cool and dry the seeds, the narrative of preservation extends far beyond the harvest, portraying a saga of safeguarding End User's bounty for sustained nourishment and longevity.

Legumes Market Trend

Growing Embrace of Regenerative Farming and Sustainable Practices Elevates Legumes' Role in Reducing Carbon Footprint in Agriculture

The rising adoption of regenerative farming and sustainable practices marks a significant trend in the Legumes market. This movement stems from a collective awareness of the environmental impact of conventional agriculture and a pursuit of more eco-friendly farming methods. Legumes play a pivotal role in this shift due to their inherent capacity for nitrogen fixation. Through a symbiotic relationship with specific bacteria in their roots, legumes convert atmospheric nitrogen into a usable Category, enriching the soil with this essential nutrient. This natural process not only enhances soil fertility but also diminishes the dependence on synthetic nitrogen-based fertilizers, pivotal in reducing greenhouse gas emissions during production. Legumes serve as a sustainable crop option within crop rotation systems, a vital aspect in the Legumes Market promoting soil health and ecological sustainability. Legumes' nitrogen-fixing capacity enhances soil health, curbing reliance on chemicals and lowering farming's environmental impact. When integrated into crop rotations, they bolster soil structure, prevent erosion, and sustain soil moisture, fostering lasting agricultural sustainability. Legumes, with their deep root systems, aid in carbon sequestration by trapping and storing atmospheric carbon in the soil. This process helps in offsetting carbon emissions, contributing to efforts aimed at mitigating climate change. The current trend in the Legumes Market involves a growing emphasis on sustainable and regenerative agriculture. Legumes stand out as a key component in this movement due to their ability to enhance soil health, reduce reliance on synthetic inputs, aid in carbon sequestration, and play a crucial role in reducing the carbon footprint associated with agriculture.

Legumes Market Dynamics

Driver

Increasing Demand for Plant-Based Protein to boost Legumes Market growth

The burgeoning global appetite for plant-based proteins stands as a paramount catalyst propelling the growth trajectory of the Legumes Market. This shift in dietary preferences mirrors a collective consciousness toward health, sustainability, and environmental stewardship. Traditional reliance on animal proteins for essential amino acids is evolving. Diverse plant-based sources, notably legumes like lentils, chickpeas, beans, and peas, rival this belief. These powerhouses offer a nutrient-packed profile, abundant in protein, fiber, vitamins, minerals, and phytonutrients, reshaping nutritional norms. Their potential in fostering weight loss, particularly among individuals grappling with conditions like type 2 diabetes or cardiovascular disease, showcases the efficacy of plant-centric diets in promoting healthier lifestyles. The merits of embracing plant proteins extend beyond personal health to environmental conservation. The adverse health implications linked with red meat consumption, specifically its contribution to heart disease and type 2 diabetes due to saturated fat content. Conversely, plant-based diets showcase an impressive ability to positively impact cholesterol levels. This is evidenced by indicating that plant-based diets, among diets with red or white meat, exhibit the most beneficial effects on LDL or bad cholesterol. Embracing legumes and plant-based diets over red meat has been associated with improved blood pressure, a crucial aspect in reducing the risk of heart disease, a focus highlighted by the Centers for Disease Control and Prevention (CDC). This dietary shift holds significance within the Legumes Market, emphasizing health benefits and altering consumption patterns.

In tandem with health and sustainability benefits, legumes and plant-based proteins signify a paradigm shift in the nutritional landscape, steering away from traditional beliefs centered on animal protein as the dietary centerpiece. Aligning with recommended daily protein allowances, these plant-based sources offer an array of culinary possibilities, enriching meals with high-quality proteins, whether through lentils as the star of a veggie burger or chickpeas elevating the allure of hummus.

The integration of legumes into daily meals signifies a holistic nutrition approach, featuring plant proteins in diverse snacks and meals. In the Legumes Market, this shift emphasizes balanced nutrition, promoting nutrient-rich vegetables, fruits, and whole grains alongside protein intake. It challenges the notion that meal satisfaction relies solely on substantial meat portions, focusing on diverse and nutrient-dense food choices. As perceptions evolve, the culinary landscape diversifies, offering abundant opportunities to seamlessly incorporate high-quality plant proteins into everyday diets, reshaping not just individual health but also the broader narrative of sustainable living and conscious consumption. The increasing demand for plant-based proteins serves as a pivotal growth driver for the legumes market, sparking a paradigm shift in dietary choices that converge health, sustainability, and culinary innovation. This trajectory not only promotes individual well-being but also addresses environmental concerns, ushering in an era where legumes and plant proteins emerge as the cornerstone of a more nourished, balanced, and eco-conscious world.

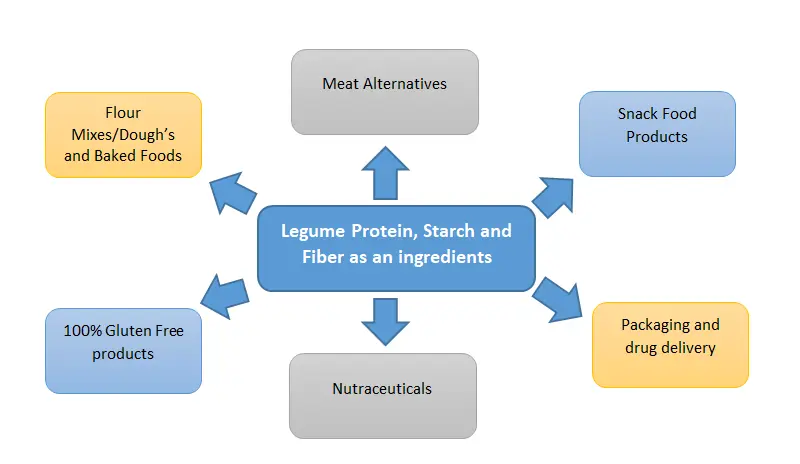

Legumes, rich in protein, starch, and fiber, witness escalating demand as key ingredients. This surge stems from the preference for plant-based protein sources, driving the legume market. Flour mixes, meat alternatives, gluten-free products, and nutraceuticals, among others, benefit from legume inclusion, catering to diverse segments including baked goods, snack items, packaging for drug delivery and others.

Opportunity

Technological advancements and innovations in processing and value addition

Technological advancements and innovations in processing and value addition stand as the cornerstone of the burgeoning opportunity within the legumes market. These advancements are revolutionizing the landscape by addressing critical limitations faced in regions like Zambia, where crop productivity suffers due to diseases, insects, soil quality, and drought. Pioneered by initiatives like the Michigan State University-led project, novel tools and platCategorys are redefining legume enhancement. The project's focus on enhancing photosynthesis efficiency not only aims to propel productivity but also offers a lifeline amid shifting climatic challenges. This endeavor leverages cutting-edge technologies from the Center for Advanced Algal and Plant Phenotyping (CAAPP), unraveling unprecedented insights into plant health and resilience. The Photosynth nature, a game-changer in plant phenotyping, provides affordable yet advanced instruments for real-time measurements related to photosynthesis, aiding researchers and farmers worldwide.

Simultaneously, the Dynamic Environmental Phenotyping Imager (DEPI) replicates field conditions in specialized chambers, unveiling intricate plant responses to diverse weather scenarios. These technological strides enable rapid field trials, accelerating the identification of resilient gene platCategorys in beans and cowpeas under environmental stresses. The collaborative effort spans across continents, with teams in Zambia and Michigan utilizing these platforms to decode the genetic makeup facilitating improved plant platforms. With such groundbreaking technology, the Legumes Market not only foresees amplified yields but also anticipates a paradigm shift toward sustainable and resilient agricultural practices, paving the way for enhanced food security and economic empowerment in regions facing agricultural challenges.

Restrain

Challenges in Pest Management and Disease Control Impact on Legumes Market Viability

Pest infestation and diseases directly affect the quantity and quality of legume yields. In severe cases, they lead to crop failures or substantial reductions in harvests. This poses a financial burden on farmers and impacts market supply, potentially leading to price fluctuations. To combat these issues, farmers adopt intensive pest and disease management strategies. These measures often involve the use of pesticides, fungicides, or other chemical interventions. These methods are costly, and excessive reliance on chemical control leads to environmental concerns and resistance among pests. Developing disease-resistant varieties demands significant investment in research and development. This includes breeding programs aimed at creating legume strains that are more resilient to prevalent diseases and pests. These programs are time-consuming and costly, affecting the accessibility of improved varieties for small-scale farmers. Over reliance on chemical interventions for pest and disease control poses concerns about the long-term sustainability of agricultural practices. The excessive use of chemicals not only impacts soil health, water quality, and biodiversity but also disrupts the ecological balance within agricultural landscapes. In the Legumes Market, this reliance underscores the need for sustainable pest management practices to maintain the health of agricultural ecosystems.

Legumes Market Segment Analysis

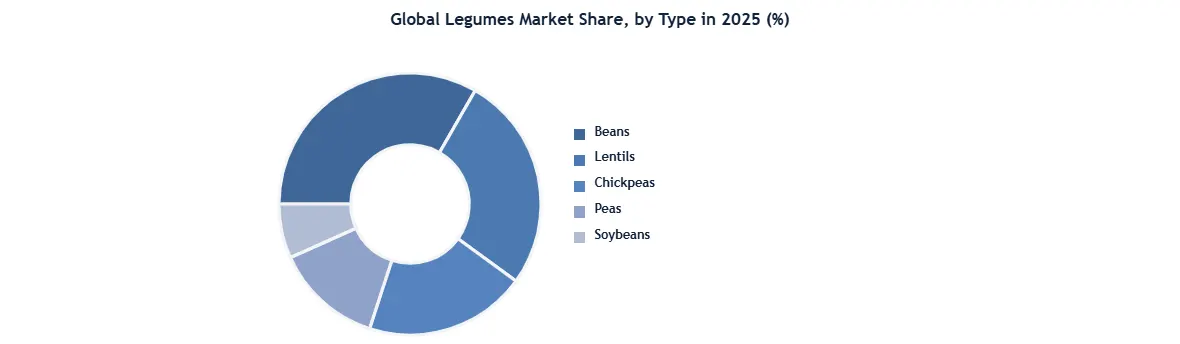

Based on Type, Beans dominate the Legumes Market in 2025 and are expected to continue their dominance over the forecast period. Beans are nutritional powerhouses, packed with protein, fiber, vitamins, and minerals. They offer an excellent plant-based protein source, appealing to health-conscious consumers seeking meat alternatives or balanced diets. Beans are incredibly versatile in the kitchen. They are cooked in diverse ways - soups, stews, salads, dips, and as standalone dishes. This adaptability in various recipes makes them an essential ingredient in many cuisines globally, enhancing their market demand. Beans have a strong presence in diets worldwide. They're a staple in numerous cuisines, from Latin American dishes like black beans to Middle Eastern hummus made from chickpeas. This broad usage contributes to their widespread consumption. Beans are grown and distributed widely, making them easily accessible in most regions. Their availability in different varieties of kidney beans, black beans, navy beans, etc. ensures a diverse market offering. Many cultures have integrated beans into their traditional diets for centuries. This historical significance has solidified beans' place in culinary practices, ensuring their continued demand which boosts the Legumes Market growth.

Beans often serve as a cost-effective protein source compared to meat or other protein alternatives, making them popular in regions where affordability is a concern. Beans stand out for their high protein content, containing all nine essential amino acids crucial for the body's repair and maintenance. While many legumes lack complete proteins, beans, particularly soybeans, possess this essential feature. Beyond protein, beans offer an array of health advantages. They're a treasure trove of folate, vital for healthy red blood cells and fetal neural tube development during pregnancy. Rich in antioxidants like polyphenols, beans combat free radicals, potentially reducing disease risks.

Spain is a significant producer of legumes, with an annual volume reaching substantial figures. The country's legumes market showcases a consistent production volume, contributing significantly to both domestic consumption and export activities, positioning Spain as a notable player in the global Legumes Market.

Legumes Market Regional Insights

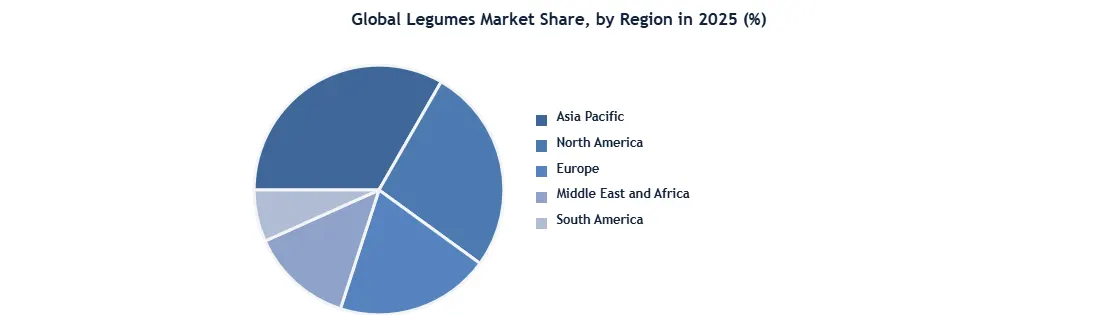

Asia Pacific held the largest share in 2025 and is expected to dominate the market during the forecast period. The Asia-Pacific region stands as a vital hub for the Legumes Market, attributing its significance to diverse factors. Legumes play a crucial role in this region, addressing nutritional needs, agricultural sustainability, and economic balance. While staple cereal crops enjoy self-sufficiency in many nations, the availability of legumes remains low, leading to substantial imports, particularly impacting affordability for rural and urban families. Despite the dominance of a few legumes in commercial markets like soybean, groundnut, chickpea, and lentil, numerous indigenous varieties such as adzuki bean, horse gram, and moth bean remain underexplored. The Seminar on Processing and Utilization of Legumes, hosted in Japan by the Asian Productivity Organization, highlighted the significance of legumes in household food security, soil enhancement, and agricultural diversification across Asian countries.

The Asia-Pacific region's increased focus on boosting legume production signifies a pivotal change in agricultural strategies. Legumes, once considered secondary crops, now garner acknowledgment for their pivotal role in food security, notably as a primary protein source, augmenting the dietary needs of diverse rural and urban populations. In the Legumes Market, this shift underscores the significance of legumes in addressing nutritional demands and fostering food security across demographics. With a population exceeding three billion, the Asia-Pacific region stands as a significant hub for nutritional resources, where legumes fulfill essential dietary needs by providing protein, fat and vital micronutrients to rural and urban communities. Countries like China, India, Myanmar and Vietnam have seen a surge in legume production, driven by expanded cultivation and enhanced productivity. Soybean cultivation in China and India has played a crucial part in addressing food crises, such as India's shortage of edible oil.

India's pulse production plays a pivotal role in the Asia-Pacific region's influence on the Legumes Market. With India being a major pulse producer, its contributions significantly impact global trade dynamics. The country's robust production not only addresses local consumption needs but also reflects its export potential. Collaborative efforts in research, innovation, and policy within this region drive agricultural productivity and ensure nutritional security across diverse populations.

Legumes Market Competitive Landscape

The Competitive Landscape of the Legumes market covers the number of key companies, company size, their strengths, weaknesses, barriers and threats. It also focuses on the power of the company’s competitive rivals, potential, new market entrants, customers, suppliers and substitute products that drive the profitability of the companies in the Legumes industry. The global Legumes markets include several market players at the country, regional and global levels. Some of the key players are Cargill, Archer , Daniels Midland Company (ADM), Bunge Limited, Louis Dreyfus Company (LDC), Olam International, Ingredion Incorporated, The Scoular Company, SunOpta Inc., AGT Food and Ingredients, Sun Agro, Bonduelle and others. Many companies conducted research and development activities to increase their product portfolio and fulfil Legumes Market. For instance, In , Cargill made significant progress in its legume development efforts. The company invested in new research and development, expanded its legume production capacity, and launched new legume-based products. Cargill is committed to developing new and innovative legume varieties with improved yields, disease resistance, and nutritional value. In , the company made significant progress in this area. For example, Cargill developed a new variety of chickpea that is resistant to drought and heat stress. This new variety is expected to help farmers in India and other developing countries increase their chickpea yields and improve their livelihoods.

Legumes Market Recent Development

- In July 2025, Bunge Global SA completed its merger with Viterra Limited, strengthening global legumes origination, processing, storage, and distribution capabilities across key agricultural markets.

- In June 2025, Louis Dreyfus Company was selected to operate the Burns Harbor export facility in the United States, expanding legumes export storage capacity and improving global pulse trade logistics.

- In March 2025, AGT Food and Ingredients announced capacity upgrades across multiple pulse processing facilities to support increasing global demand for lentils, peas, and plant-based protein ingredients.

- In December 2025, BASF Nunhems agreed to acquire Noble Seeds Pvt. Ltd. to strengthen its vegetable seed portfolio and expand market presence in India’s legumes and vegetable seed sector.

- In March 2025, the Government of India approved procurement of 37.39 lakh tonnes of gram and lentils through Nafed and NCCF under the Price Support Scheme to strengthen domestic pulse supply and farmer income support.

- In 2025, Cargill and Ingredion Incorporated expanded investments in plant-based protein and pulse ingredient processing to meet rising global demand for alternative protein products.

- In 2025, Roquette Frères continued expanding pulse protein ingredient solutions for plant-based food manufacturing and sustainable nutrition applications globally.

- In August 2024, India’s Council of Agricultural Research released 69 climate-resilient pulse varieties aimed at improving legumes productivity, drought resistance, and sustainable agricultural output.

Legumes Market Scope : Inquire Before Buying

| Global Legumes Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 14.23 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.5% | Market Size in 2032: | 20.7 USD Billion |

| Segments Covered: | by Type | Beans Lentils Chickpeas Peas Soybeans Others |

|

| by Category | Conventional Organic |

||

| by End User | Food and Beverage Animal Feed Others |

||

| by Distribution Channel | Supermarkets/Hypermarkets Online Retail Specialty Stores Others |

||

Legumes Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Legumes Key Players

1. Cargill

2. Archer Daniels Midland Company (ADM)

3. Bunge Limited

4. Louis Dreyfus Company (LDC)

5. Olam International

6. Ingredion Incorporated

7. The Scoular Company

8. SunOpta Inc.

9. AGT Food and Ingredients

10. Sun Agro

11. Bonduelle

12. Emsland Group

13. Bean Growers Australia

14. Arbel

15. Diefenbaker Seed Processors

16. Sleaford Quality Foods Ltd.

17. Farmer’s Cooperative

18. Earth Expo Company

19. S&W Seed Company

20. Hancock Farm & Seed Company

21. Pulse Australi