Infusion Pumps Market Size by Type, Technology, Application, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

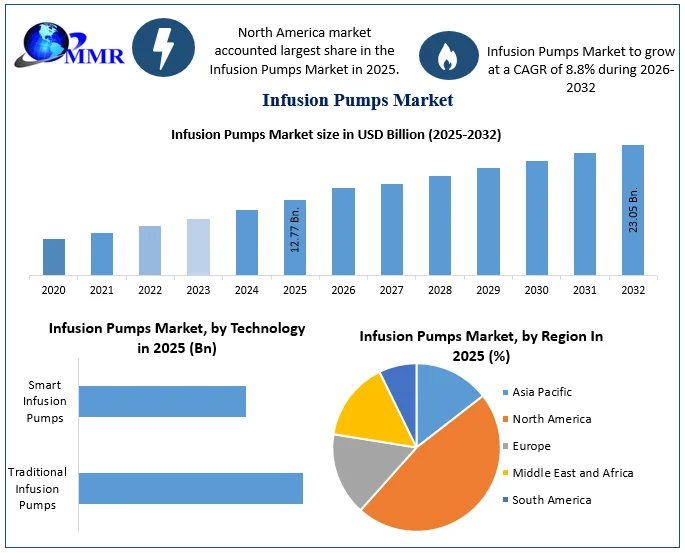

Infusion Pumps Market was valued at USD 12.77 Bn. in 2025, and total global Infusion Pumps Market revenue is expected to grow at a CAGR of 8.8% from 2026 to 2032, reaching nearly USD 23.05 Bn. Growing demand for home-based healthcare solutions.

Global Infusion Pumps Market Overview:

Infusion pumps supply fluids to patients, such as medications and nutrition. A skilled person operates the infusion pumps, and the fluid supply is controlled via the built-in software interface. Fluid infusion and medicine delivery accuracy are vital for the best care of a critically sick newborn. The recommended form of therapy in acute care is continuous and regulated intravenous administration of common drugs such as inotropic agents, vasodilators, aminophylline, insulin, heparin and others through an infusion pump. This is especially true for medications with short half-lives, to maintain a desired constant serum concentration, and in conditions requiring a continuous infusion of glucose.

Small neonates or those with poor renal, cardiac, or pulmonary function have limited fluid tolerance, hence infusion pumps are required to avoid accidental volume overload. More than one infusion pump is frequently necessary for critical care in small neonates when medication dose, concentration, interaction, and fluid volume necessitate various infusion rates. Infusion pumps have been recommended over manual flow control systems because they ensure precise and accurate administration of prescribed fluid amounts over a set time period and aid in improved nurse management.

The global infusion pumps market is expected to grow because of the increasing prevalence of chronic diseases, like cancer, diabetes, and others. Infusion pumps are widely used in the treatment of chronic diseases, thanks to the rising adoption of these devices due to the broadening applications of infusion pumps across the end-user. Infusion pumps are commonly utilized in chemotherapy, diabetes treatment, and a variety of other purposes. The increased frequency of chronic disorders all across the globe is generating several potentials for the industry's growth.

In addition, technological developments in consumer electronics, and manufacturers’ initiatives in creating innovative products that satisfy safety requirements and increase the implementation of devices are expected to drive revenue growth. For example, in February 2022, United Therapeutics announced the Remunity Pump for remodeling, which helps patients with pulmonary arterial hypertension live better lives (PAH). In addition, the main market players' development of infusion pump devices is driving the industry's growth. Mindray Medical, for example, expanded its product line by introducing the BeneFusion E series-ESP, EVP, and EDS infusion systems in February 2022.

To know about the Research Methodology :- Request Free Sample Report

Infusion Pumps Market Dynamics:

Increasing number of surgical operations performed across the world

The number of surgical operations conducted throughout the world has increased significantly over the years. This can be ascribed to a rising aging population as well as an increase in the incidence of obesity and other lifestyle disorders. Obesity is a major contributor to cardiovascular and orthopedic illnesses. Obesity raises the risk of coronary heart disease, joint and tissue damage, cancer (of the breast, colon, prostate, endometrial, kidney, and gallbladder), ischemic stroke, and type 2 diabetes mellitus. Infusion pumps are essential for the continuous and regulated delivery of medications during and after many types of surgery.

Infusion pumps' primary application areas include chemotherapy, gastroenterology, analgesia/pain management, and diabetes. Following bariatric surgery, cardiothoracic surgery, and laparoscopic cholecystectomy, infusion pumps are extensively utilized for the local delivery of narcotic analgesics and anesthetics. The need for infusion treatment is expected to grow as the number of surgeries conducted increases. And eventually rising the infusion pumps market revenue during the forecast period.

High Prevalence of Chronic Diseases

Infusion pumps offer significant benefits over conventional fluid delivery, such as the ability to infuse fluids in extremely tiny doses and at precise programmed rates. In many circumstances, such as cancer and diabetes disorders, these pumps are utilized to administer medicine to keep drug levels in circulation stable. According to the World Health Organization (WHO), cancer was anticipated to be the second leading cause of death globally in 2019, accounting for around 9.6 million fatalities. Cancer patients require chemotherapy to be administered to them in a continual way, which the pump can do.

However, the prevalence of diabetes would be around 785 million cases globally by 2025. Of these estimates of global cases, 63.5 million cases of diabetes were found in the United States, accounting for 10.5% of the total population. Insulin pumps are becoming more popular in the treatment of type 1 diabetes. To provide continuous drug administration, these patients require user-friendly self-controlled pumps. These reasons are driving the infusion pumps market growth in all regions.

Stringent regulations for new product production of Pumps

Infusion pumps are meant to administer liquid medicine as well as other solutions to a patient's body and are subject to stringent standards and regulations to ensure patients' health and safety. For the approval of new goods, the infusion pumps market is governed by different regulatory bodies, including the US Food and Drug Administration (FDA), the Medicines and Healthcare Products Regulatory Agency (MHRA), and the European Medicines Agency (EMA). In Europe, CE mark approval is required to lawfully sell and advertise infusion pumps.

Non-implantable infusion pumps are classed as Class II b devices, while implantable infusion pumps are classified as Active Implantable Medical Devices (AIMD). There are around 300 UK-specific medical device standards. The existing method of producing new infusion pumps across several regions is time-consuming and costly. This is expected to stymie the growth of the infusion pumps market revenue during the forecast period.

High implementation of specialty infusion systems

Various customized infusion pumps are becoming more widespread all over the globe. There are several types of specialty infusion pumps in the market, including patient-controlled analgesia (PCA) pumps, enteral pumps, insulin pumps, and others. PCA pumps provide regulated anesthesia and decrease the risks associated with anesthetics. These pumps are also commonly used to relieve pain during delivery and chronic conditions. Enteral infusion pumps are critical medical instruments for individuals suffering from indigestion as a result of recent surgery or functional inabilities of various digestive organs. The increasing prevalence of chronic conditions, the transition from parenteral to enteral feeding, and the rising frequency of premature deliveries have all contributed to the increased use of enteral infusion pumps. This creates lucrative opportunities for the players in the infusion pumps market.

Increasing medication errors and lack of wireless connectivity of Pumps

Medication errors are the leading cause of healthcare injuries, accounting for 19.4% of all adverse events. Intravenous (IV) infusions have been recognized as a common cause of pharmaceutical errors. Multihospital research published in BMJ Quality & Safety in 2016 discovered that 60% of IV infusions were administered incorrectly. By allowing nurses to program an hourly rate and volume, general infusion pumps increase the precision and consistency of IV infusions.

According to research, these devices are responsible for 35% to 60% of the estimated 770,000 adverse drug events (ADES) that occur each year. The majority of adverse events connected with IV infusion equipment are caused by nurses manually entering erroneous settings into the pump. Unit errors, multiple of ten errors, miscalculations, and push-button failures are the most prevalent infusion errors. Fatal mistakes arise as a result of decimal entry errors while programming infusion pumps (for example, programming morphine at 90 ml/hr rather than 9, 0 ml/hr. resulting in a tenfold overdose). As a result, these hamper the infusion pumps market growth.

Infusion Pumps Market Segment Analysis:

Based on type, volumetric infusion pumps held the largest market share of 32% and dominated the Infusion Pumps market in 2025. The segment is further expected to maintain its dominance at the end of the forecast period with the highest share. The high share of these pumps was owing to their ability to provide continuous and highly exact volumes of fluids at extremely slow to extremely rapid speeds. Volumetric infusion pumps offer a wide range of applications in illness management and parenteral nutrition, hence, their market potential is the largest when compared to other pumps' markets. Infusion pumps' safety, precision, and simplicity in the treatment of numerous therapeutic areas contribute to their high demand.

Volumetric infusion pumps are capable of estimating the fluid volume with microprocessor-based calculations, taking into account the size of the drop produced and the standardized diameter of the tubing. It can run on both main power and rechargeable batteries. If bubbles emerge in the tube, the alert bulb and warning buzzer sound at the same time, and the pump instantly stops. Apart from the standard audiovisual alerts of malfunctioning and air bubbles in the system, it informs the operator when the infusion is complete, the battery voltage is low, and the flow line is blocked.

The volumetric infusion pumps have diverse applications, benefits, increased utilization, and increased product introduction across various hospitals and facility centers in both emerging and established countries driving the segment revenue growth during the forecast period. For example, Fresenius Kabi received regulatory clearance from the United States Food and Drug Administration (USFDA) in March 2022 for its wireless Agilia connect infusion system, which includes the Agilia volumetric pump and the Agilia syringe pump with vigilant software suite-Vigilant Master Med technology.

The Agilia Connect volumetric pump and syringe pump is one of the first to be cleared by the Association for the Advancement of Medical Instrumentation (AAMI) in 2021 using TIR101 criteria. This product offering has enabled centralized drug library delivery, storage of infusion data for reporting and analysis, and wireless device maintenance and calibration. Meanwhile, the key players are emphasizing research and development initiatives, which are expected to drive the market segment's growth. For example, in November 2021, Zealand Pharma and DEKA Research & Development Corp. agreed to collaborate on the development of an infusion pump that may be used in conjunction with dasiglucagon to treat congenital hyperinsulinism (CHI). However, factors such as increased chronic illness prevalence and technology innovation enhance the segment's growth.

Based on end-user, the Ambulatory Care Settings segment held a significant share of the Infusion Pumps market in 2025 because these pumps are extensively preferred for the delivery of nutrients and medications. In both emergency and chronic diseases, ambulatory infusion pumps are used to give liquid nutrition and medicines to patients. Other pumps, such as patient-controlled analgesia (PCA) pumps, insulin pumps, and smart pumps, would contribute to the segment's supplementary growth. The growing preference for intravenous infusion pumps is being driven by increased demand for enteral and syringe pumps, which would contribute to segment revenue growth.

Smart pumps with controlled IV medication and error-prevention software are increasingly being used across various hospitals because they are equipped with advanced features such as drug libraries, which aid in storing the amount of medicated fluid given to the patient, and barcode technology, which aids in the verification of a patient's identity and also aids in the prevention of drug administration errors. Insulin infusion pumps, on the other hand, are expected to have a considerable CAGR throughout the forecast period. This is because the global prevalence of diabetes and its problems has increased in the previous decade, owing mostly to changing lifestyles and urbanization. This pump segment is expected to thrive in the future since it has a low rate of infections and delivery system failure during treatment.

Infusion Pumps Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 07 April 2025 | ICU Medical | The company secured U.S. FDA 510(k) clearance for its next-generation Plum Solo™ and Plum Duo™ precision IV pumps, alongside updated LifeShield™ safety software. | This initial launch expands their performance platform, delivering consistent ±3% dosing accuracy under real-world clinical conditions to remove external infusion setup variability. |

| 29 May 2025 | Iradimed | The manufacturer obtained FDA 510(k) clearance for its MRidium® 3870 infusion pump system, a non-magnetic device built explicitly for complex imaging suites. | The approval introduces advanced ultrasonic pump technology and wireless remote control capabilities to support uninterrupted drug delivery during sensitive MRI procedures. |

| 15 June 2025 | MEDITECH | The company introduced a new two-way communication interface linking its Expanse Electronic Health Record (EHR) platform directly with smart infusion pumps. | This bidirectional integration automates patient records and pump parameters, drastically reducing manual data entry errors and optimizing digital clinical workflows. |

| 26 August 2025 | Terumo India | The regional subsidiary officially launched its Terufusion™ Advanced Infusion Systems featuring intelligent digital connectivity for critical care environments. | By incorporating smart volumetric pumps and tracking software, the release streamlines ICU workloads via centralized remote monitoring and embedded drug libraries. |

Infusion Pumps Market Regional Insights:

North American regional market dominated the Infusion Pumps market with the highest share in 2025. The region is further expected to hold a major share of the infusion pump market with the highest CAGR of about 8.5% during the forecast period. The rise in chronic diseases, as well as the increased acceptance of technologically advanced goods, solutions, and types of equipment by patients and clinicians for routine treatment of chronic illness conditions, are driving regional market revenue growth. For example, the American Cancer Society estimates that there will be 1,918,030 new cancer cases in the United States by end of 2022.

However, according to the International Diabetes Federation (IDF) Diabetes Atlas, Tenth Edition figures, 32.2 million individuals in the United States had diabetes in 2022, and this number is expected to rise by 36.3 million by the end of 2045. As a result, the rising prevalence of chronic illnesses such as cancer and diabetes is expected to drive the growth of this Infusion Pumps market.

Additionally, the industry's growth is driven by the increased implementation of advantageous favorable reimbursement initiatives, which help in the region's growth. The healthcare reimbursement system in the United States is a combination of public and private third-party coverage, with businesses, individuals, and the government all contributing to healthcare expenditures. Individuals and employers pay private insurance companies premiums to cover healthcare costs; government coverage is provided to specific populations at the federal (Medicare, Department of Defense, Bureau of Indian Affairs) and state levels (Medicaid); and private insurers may also provide care coverage to citizens who receive government insurance (Medicare/Medicaid).

In addition, the length of inpatient stays has grown over the last several decades, resulting in a greater demand for infusion pumps for these patients. For example, the American Hospital Association announced in 2022 that approximately 36.2 million hospital admissions were documented in the United States in 2021. The increasing demand for high-end infusion pump systems for better patient care is expected to drive the growth of the infusion pumps market in North America.

The Asia Pacific market is expected to grow at a significant CAGR of 8.2% during the forecast period. The area countries are densely populated, with an increasing burden of chronic illnesses like diabetes, cardiovascular disease, and cancer. These countries are also well-known for their inexpensive treatment and surgery costs, making them a favorite destination for medical tourists. Emerging economies with well-developed healthcare infrastructure and amenities include China, Japan, and India. High illness burden, considerable government changes, acceptance of new technologies, and affordable treatment costs are paving the way for market growth.

Infusion Pumps Market Scope: Inquire before buying

| Infusion Pumps Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 12.77 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.8% | Market Size in 2032: | USD 23.05 Bn. |

| Segments Covered: | by Type | Volumetric Pumps Syringe Pumps Elastomeric Pumps Insulin Pumps Enteral Pumps Implantable Pumps Patient Control Analgesia (PCA) Pumps |

|

| by Technology | Traditional Infusion Pumps Smart Infusion Pumps |

||

| by Application | Chemotherapy/Oncology Diabetes Management Gastroenterology Pain Management Analgesia Paediatrics/ Neonatology Haematology Others |

||

| by End-User | Hospitals Home Care Settings Ambulatory Care Settings Academic and Research Institutes |

||

Infusion Pumps Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Leading Manufacturers in the Infusion Pumps Market are:

1. Becton, Dickinson and Company (US)

2. Baxter International Inc. (US)

3. ICU Medical, Inc. (US)

4. Smiths Medical (US)

5. Moog Inc. (US)

6. Avanos Medical, Inc. (US)

7. Insulet Corporation (US)

8. Tandem Diabetes Care (US)

9. InfuTronix Solutions LLC (US)

10. Zyno Medical LLC (US)

11. Teleflex, Inc. (US)

12. CODAN Medizinische Geräte GmbH & Co KG (Germany)

13. B. Braun (Germany)

14. Fresenius Kabi (Germany)

15. Medtronic PLC (Ireland)

16. Ypsomed Holding AG (Switzerland)

17. Roche Diagnostics (Switzerland)

18. Micrel Medical Devices SA (Greece)

19. Nipro Corporation (Japan)

20. Terumo Corporation (Japan)

21. JMS Co., Ltd. (Japan)

22. SOOIL Development Co., Ltd. (South Korea)

23. Shenzhen MedRena Biotech Co., Ltd. (China)

24. Mindray Medical International Limited (China)

25. Epic Medical (Singapore)

Frequently Asked Questions

1. What are the growth drivers for the Infusion Pumps market?

Ans. The global infusion pump market is driven by the increasing prevalence of chronic diseases, like cancer, diabetes, and others. Infusion pumps are widely used in the treatment of chronic diseases, thanks to the rising adoption of these devices due to the broadening applications of infusion pumps across the end-user. Infusion pumps are commonly utilized in chemotherapy, diabetes treatment, and a variety of other purposes. The increased frequency of chronic disorders all across the globe is generating several potentials for the industry's growth.

2. What is the major restraint for the Infusion Pumps market growth?

Ans. The Stringent Regulations on the Infusion Pumps adoption are expected to be the major restraining factor for the Infusion Pumps market growth.

3. Which region is expected to lead the global Infusion Pumps market during the forecast period?

Ans. The North American regional market is expected to lead the global Infusion Pumps market during the forecast period due to the rise in chronic diseases, as well as the increased acceptance of technologically advanced goods, solutions, and types of equipment by patients and clinicians for routine treatment of chronic illness conditions.

4. What is the projected market size & growth rate of the Infusion Pumps Market?

Ans. Infusion Pumps Market was valued at USD 12.77 billion in 2025, and total global Infusion Pumps Market revenue is expected to grow at a CAGR of 8.8% from 2026 to 2032, reaching nearly USD 23.05 billion.

5. What segments are covered in the Infusion Pumps Market report?

Ans. The segments covered in the Infusion Pumps market report are Type, Application, Technology, End-User, and Region.