Orthopedic Braces and Supports Market Size by Product, Type, Application, End-User, and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2029

Overview

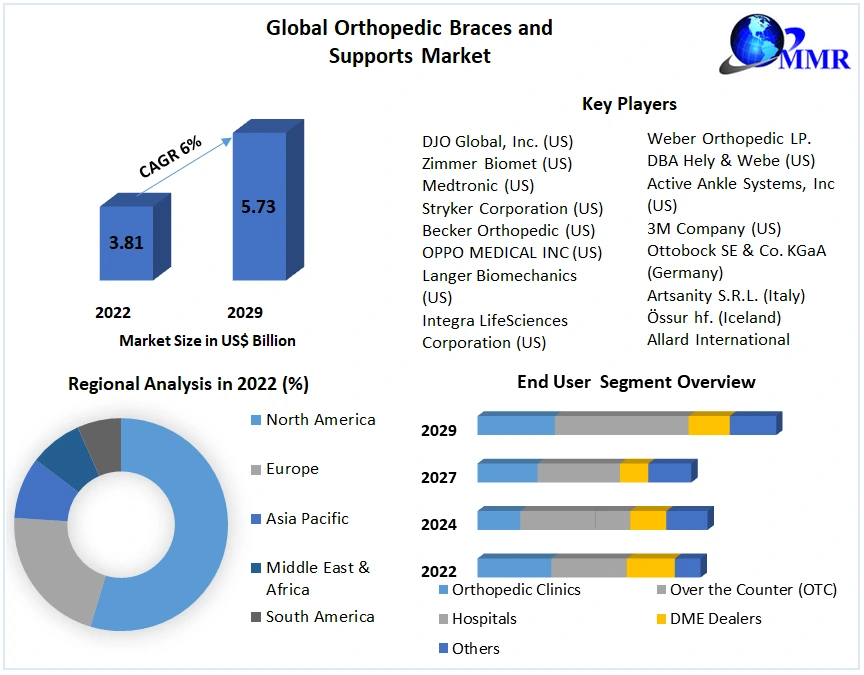

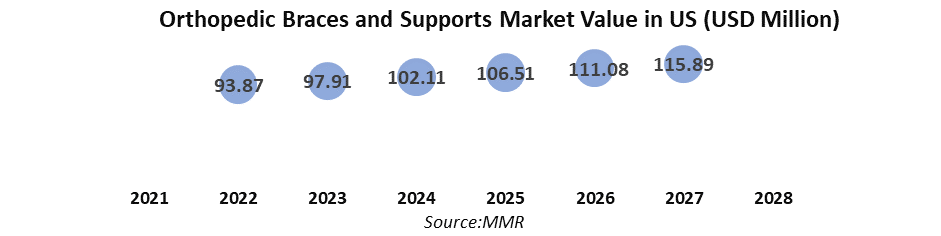

Orthopedic Braces and Supports Market size was valued at USD 3.81 Bn. in 2022 and the total Orthopedic Braces and Supports revenue is expected to grow by 6 % from 2023 to 2029, reaching nearly USD 5.7 Bn.

Orthopedic Braces and Supports Market Overview:

The Orthopedic braces are medical devices that are used to properly align, correct the position, support, stabilize, and protect certain portions of the body (especially the muscles, joints, and bones) as they heal from injury or damage. Orthopedic braces are used in many specialized healthcare disciplines, including those dealing with healing and avoiding injuries, post-operative treatment, osteoarthritis care, and more. Growing osteoarthritis occurrences, a growing geriatric population, an increase in sport-related injuries, and a number of product releases by prominent market players in this industry are some of the factors likely to fuel the market growth during the forecast period. According to a National Center for Biotechnology Information article, osteoarthritis is the most prevalent joint ailment in the United States, affecting 12% of men and 15% of women aged 60 and over.

Any type of bone fracture frequently necessitates the use of orthopedic braces and support systems to create immobilization of the patient's shattered component. Fractures such as osteoporotic vertebral fractures, one of the most severe types of osteoporotic fractures, result in the widespread use of braces such as TLSO (Thoracic Lumbar Sacral Orthosis). According to a December 2020 article titled 'Vertebral Compression Fractures,' around 1 to 1.5 million vertebral compression fractures (VCF) occur yearly in the United States alone. According to the age and sex-adjusted incidence, 25% of women aged 50 and older had at least one VCF.

Additionally, the lifetime risk for hip, forearm, and vertebral fractures is approaching clinical attention at around 40% globally, which is comparable to the risk of cardiovascular disease. In developed nations, rising disposable income and a higher rate of adoption of new technology in hospitals and orthopedic centers are leading to earlier diagnosis and increased demand for orthopedic braces and support systems, making this market one of the key driving forces.

Report Scope:

The Orthopedic Braces and Supports research provides an in-depth analysis of the market's growth prospects, challenges, and projections. Research on Porter's five forces shows how networks of suppliers and customers can be formed in order to make lucrative decisions. The present Orthopedic Braces and Supports Market potential is ascertained through in-depth analysis, market size, and segmentation. The analysis, which also contains the elements expected to have a positive or negative impact on the company, will provide investors with a full picture of the future of the industry.

The analysis offers a full understanding of the market for those who want to make investments. In addition to the estimated market size, this report includes historical and contemporary scenarios for the Orthopedic Braces and Supports market.

Every facet of the market is covered in the report's comprehensive study of significant rivals, including market leaders, followers, and new entrants. The study includes strategic profiles of the leading industry players, a thorough analysis of their core strengths, and information on their company-specific plans for the launch of new products, growth, partnerships, joint ventures, and acquisitions. The research serves as a resource for investors with its clear depiction of competitive analysis of key companies by product, pricing, financial condition, product portfolio, growth strategies, and geographical presence in both the domestic and local market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Orthopedic Braces and Supports Market Dynamics:

Market Drivers:

Increased incidence of orthopedic illnesses and disorders

The increased prevalence of obesity and accompanying lifestyle problems is expected to increase the incidence of orthopedic illnesses and disorders in the forecast years since obese people are at a higher risk of orthopedic and musculoskeletal injuries, as well as diabetes. Orthopedic braces and supports provide various advantages over traditional solutions, including lower cost, improved effectiveness, more patient comfort, and ease of use. Thanks to these advantages, leading companies are rapidly creating specialized solutions for the treatment of various orthopedic illnesses as well as to meet unmet market demands.

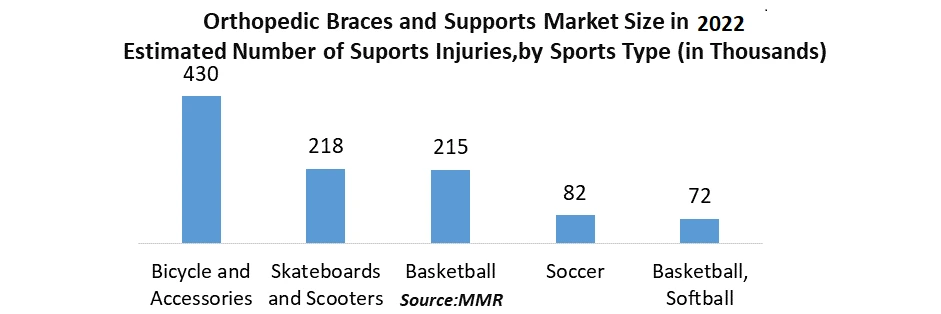

Patient demand for orthopedic braces is increasing in both established and emerging economies, owing to their low cost and ease of market access. Sports and other physical activity frequently result in musculoskeletal injuries such as sprains, ligament tears, and fractures. Moreover, the growing public engagement in such activities contributes to the prevalence of these illnesses. Orthopedic braces and supports are becoming a more successful clinical alternative to orthopedic surgery for illnesses such as rheumatoid arthritis, osteoporosis, gout, and fractures. Various public-private sports groups and medical experts are organizing conferences, workshops, and symposiums to raise public knowledge about the therapeutic care of orthopedic injuries. Increasing Sport Injuries

Increasing Sport Injuries

Increasing amateur sports and activity levels, the geriatric population in key markets around the world, and the number of elective orthopedic surgeries, such as knee replacement, are expected to drive demand for high-end products like Unloaded OA bracing products and postoperative bracing solutions. Growing osteoarthritis occurrences are a major orthopedic ailment influencing product demand. It is the most prevalent type of arthritis that affects people of all ages.

The Centers for Disease Control and Prevention (CDC) predicts that over 78.2 million U.S. individuals over the age of 18 will be diagnosed with arthritis by 2040. The aging population is thought to be one of the biggest drivers of demand for orthopedic braces and support. This demographic is predisposed to musculoskeletal diseases. Bones and connective tissues, such as ligaments and cartilages, deteriorate with age. This increases the chance of muscular damage, particularly in the elderly's knees and shoulders.

This stiffens the joints, even more, necessitating the use of braces and supports to promote movement. ACL sprains and tears are the most prevalent conditions affecting persons who participate in high-demand sports such as football, gymnastics, soccer, downhill skiing, and basketball. As mobility limitations were relaxed, injuries caused by the potential impact of detraining emerged as a major contributor to ACL injuries. Medical device products are subject to worldwide pricing pressures, regulations, and other price constraints. Pricing may change as a result of direct government action in price setting. In the United States, for example, competitive bidding for off-the-shelf spine and back braces went into effect in January 2022.

This is expected to raise pricing pressure on certain items. Similarly, in February 2020, the Indian Government published a notification that classified all medical devices and medical equipment markets in the nation as "drugs," bringing them within the current quality and safety regulatory system. The frequency of sports-related injuries is increasing as the number of sporting activities increases. Athletes are mostly interested in fitness-related activities such as running, cycling, and others.

While participating in such activities, kids are more prone to experience injuries, which can lead to ligament damage. Indoor athletes are particularly vulnerable to ankle ligament tears. As a result, ankle braces are expected to be in high demand. Ankle braces are also advised after an acute ankle injury. Athletes also utilize orthopedic braces to prevent themselves from additional harm while participating in sports. It assists them in limiting undesired movement during matches, allowing for more convenient play.

Market Restraints:

Lack of qualification

Bracing and support goods are used to successfully manage orthopedic problems and diseases, with physicians and orthopedic surgeons deeming these products clinically required in some cases. However, patients do not qualify for bracing goods in some circumstances (depending on the severity of the condition and its side effects, as well as the patient's physiology and age).

Innovative orthopedic braces are becoming more popular among large end-user institutions (such as hospitals, surgical centers, and orthopedic clinics) in developed countries such as the United States, Germany, the United Kingdom, and Japan. However, due to a lack of knowledge and affordability, end-user facilities in emerging and less-developed markets are hesitant to accept innovative goods. These consumers also prefer to use traditional/established items that have clinical proof to back up their therapeutic/diagnostic role.

Market Opportunities:

Increased sales of off-the-shelf and online products

Specific orthopedic braces may only be used under the supervision of medical practitioners or orthopedic technicians since they require customization or product modification based on patient characteristics. However, some braces (such as ankle braces, wrist/hand braces, shoulder braces, elbow braces, and face braces) are increasingly being offered by stores (off-the-shelf) and e-commerce websites since their use does not necessitate supervision. Patients routinely use such products to avoid injury.

Orthopedic Braces and Supports Market Segment Analysis:

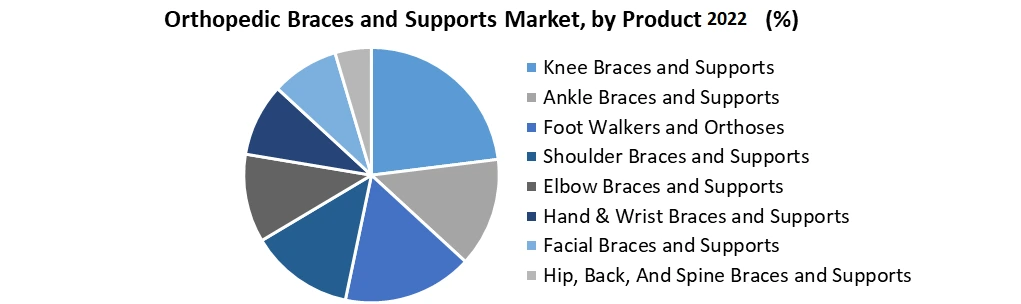

Based on Product, The orthopedic braces and supports market is divided into five product categories: knee braces and supports, ankle braces and supports, back, hip, and spine braces and supports, foot walkers and orthoses, hand and wrist braces and supports, shoulder braces and supports, elbow braces and supports, and facial braces and supports.

Knee braces and supports had the highest revenue share in 2022, owing to an increasing number of people suffering from knee joint-related diseases. Knee braces relieve strain on arthritis-affected knee joints. Individuals suffering from arthritis and other joint-related ailments, athletes, and people who have undergone knee surgery are the primary users of these items. Doctors prescribe walking boots for the stability of fractures, sprains, ligament injuries, or tendon rips in the foot or ankle area. However, owing to its restricted utilization, this category generates little money. Walking boots are further classified as pneumatic and non-pneumatic. Based on the Type, The orthopedic braces and supports market is divided into three types: soft and elastic braces and supports, hard braces and supports, and hinged braces and supports. During the forecast period, the soft & elastic braces and supports category is expected to increase at the fastest rate. The growing availability of improved goods, increasing acceptance and patient preference for orthopedic braces in post-operative and preventative care, and the supportive reimbursement landscape for target products across mature countries are driving growth in this market. Wearing elastic bands enhances the fit of the upper and lower teeth and/or jaws, resulting in a better bite. Elastic bands help to correct the bite and are crucial during the bite-fixing phase of orthodontic treatment, which is typically the longest and most difficult aspect of the whole process.

Based on the Type, The orthopedic braces and supports market is divided into three types: soft and elastic braces and supports, hard braces and supports, and hinged braces and supports. During the forecast period, the soft & elastic braces and supports category is expected to increase at the fastest rate. The growing availability of improved goods, increasing acceptance and patient preference for orthopedic braces in post-operative and preventative care, and the supportive reimbursement landscape for target products across mature countries are driving growth in this market. Wearing elastic bands enhances the fit of the upper and lower teeth and/or jaws, resulting in a better bite. Elastic bands help to correct the bite and are crucial during the bite-fixing phase of orthodontic treatment, which is typically the longest and most difficult aspect of the whole process.

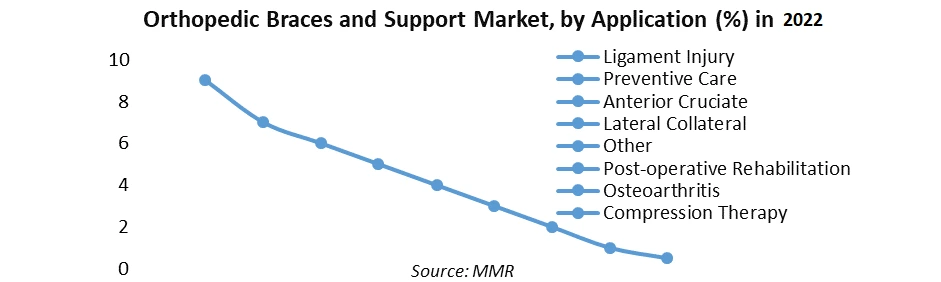

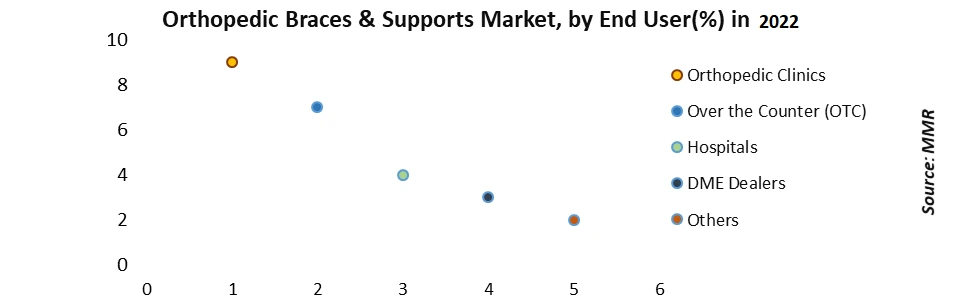

Based on the Application, The orthopedic braces and supports market is divided into several applications, including preventative care, ligament damage, post-operative rehabilitation, osteoarthritis, compression treatment, and others. In 2022, the ligament injury category is predicted to occupy the biggest market share. The growing public engagement in sports and athletic activities (combined with the rising frequency of sports-related injuries), the growing number of accidents globally, and the growing availability of medical coverage for ligament injuries all contribute to this segment's size. Based on the End User, The orthopedic braces and support systems market is divided into orthopedic clinics, hospitals, over-the-counter (OTC), DME Dealers, and other institutions based end-use. Orthopedic clinics had a market share of more than 30.0% in 2022. This is because orthopedic clinics are the primary point of treatment for people with musculoskeletal discomfort. Because of the enormous number of people seeking care at hospitals, particularly in cases of serious injuries, hospitals enjoyed a major market share. These can include spinal injuries, bone fractures, and injuries sustained in car accidents.

Based on the End User, The orthopedic braces and support systems market is divided into orthopedic clinics, hospitals, over-the-counter (OTC), DME Dealers, and other institutions based end-use. Orthopedic clinics had a market share of more than 30.0% in 2022. This is because orthopedic clinics are the primary point of treatment for people with musculoskeletal discomfort. Because of the enormous number of people seeking care at hospitals, particularly in cases of serious injuries, hospitals enjoyed a major market share. These can include spinal injuries, bone fractures, and injuries sustained in car accidents.

OTC-related orthopedic braces are expected to rise rapidly during the forecast period owing to their widespread availability in retail pharmacies. Patients suffering from acute muscular discomfort prefer to use over-the-counter medications. These products shorten healing time and allow for faster treatment of injured muscles and joints. Key company initiatives are expected to drive market growth. Companies joined Club Warehouse in Australia in February 2022 to market their product lines inside the country. As a result, the firm was able to provide its portfolio to a variety of orthopedic clinics and sports organizations, including the National Rugby League (NRL), the Australian Football League (AFL), and Rugby Union Clubs. Orthopedic Braces and Supports Market Regional Insights:

Orthopedic Braces and Supports Market Regional Insights:

North America dominated the market owing to the region's growth in musculoskeletal diseases and increasing incidence of sports-related injuries. According to data from the National Center for Injury Prevention and Control, Centers for Disease Control and Prevention (CDC), 22,887,137 individuals reported to the emergency room in the United States in 2020 for non-fatal injuries. Another element contributing to the market's growth is the growing geriatric population. According to the World Population Aging study, the number of individuals over the age of 65 in the United States is expected to increase from 53,340 thousand in 2019 to 84,813 thousand by 2030, with the 65-and-older age group's percentage of the overall population rising from 16.2% in 2019 to 22.4% by 2050. Because this population is more prone to discomfort, arthritis, joint pain, and other non-fatal pain and injuries, the market in the region is likely to rise. The major players are changing toward the use of 3D printing capabilities while collaborating with speciality technology businesses, and merger and acquisition opportunities are expected to develop internationally. The region features various small and medium-sized orthopedic manufacturers, as well as startups, tempting global businesses to participate in the US orthopedic braces and support industry. As a result of these factors, the United States is expected to have a considerable market share among all other nations in the area throughout the projected period.

The major players are changing toward the use of 3D printing capabilities while collaborating with speciality technology businesses, and merger and acquisition opportunities are expected to develop internationally. The region features various small and medium-sized orthopedic manufacturers, as well as startups, tempting global businesses to participate in the US orthopedic braces and support industry. As a result of these factors, the United States is expected to have a considerable market share among all other nations in the area throughout the projected period.

Orthopedic Braces and Supports Market Scope: Inquire before buying

| Orthopedic Braces and Supports Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2017 to 2022 | Market Size in 2022: | US $ 3.81 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 6% | Market Size in 2029: | US $ 5.73 Bn. |

| Segments Covered: | by Product | 1. Knee Braces and Supports 2. Ankle Braces and Supports 3. Foot Walkers and Orthoses 4. Shoulder Braces and Supports 5. Elbow Braces and Supports 6. Hand & Wrist Braces and Supports 7. Facial Braces and Supports 8. Hip, Back, And Spine Braces and Supports 1.2 Neck & Cervical Spine Braces and Supports 1.2 Lower Spine Braces and Supports |

|

| by Type | 1. Soft & Elastic Braces and Supports 2. Hard Braces and Supports 3. Hinged Braces and Supports |

||

| by Application | 1.Ligament Injury 1.1 Anterior Cruciate 1.2 Lateral Collateral 1.3 Other 2.Preventive Care 3. Post-operative Rehabilitation 4.Osteoarthritis 5.Compression Therapy 6. Other |

||

| by End-User | 1. Orthopedic Clinics 2.Over the Counter (OTC) 3. Hospitals 4. DME Dealers 5.Others |

||

by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players are:

DJO Global, Inc. (US)

1. Zimmer Biomet (US)

2. Medtronic (US)

3. Stryker Corporation (US)

4. Becker Orthopedic (US)

5. OPPO MEDICAL INC (US)

6. Langer Biomechanics (US)

7. Integra LifeSciences Corporation (US)

8. Globus Medical (US)

9. Frank Stubbs Company (US)

10.DeRoyal Industries (US)

11.NuVasive, Inc (US)

12.Weber Orthopedic LP. DBA Hely & Webe (US)

13.Active Ankle Systems, Inc (US)

14.3M Company (US)

15.Ottobock SE & Co. KGaA (Germany)

16.Artsanity S.R.L. (Italy)

17.Össur hf. (Iceland)

18.Allard International (Sweden)

19.Ascent Meditech Limited (India)

20.Alcare Co., Ltd (Japan)

21.Arshine Lifescience Co., Ltd. (China)

Frequently Asked Questions:

1] What segments are covered in the Global Orthopedic Braces and Supports Market report?

Ans. The segments covered in the Orthopedic Braces and Supports Market report are based on Product, Type, Application, End User, and Region.

2] Which region is expected to hold the highest share in the Global Orthopedic Braces and Supports Market?

Ans. The North America region is expected to hold the highest share in the Orthopedic Braces and Supports Market.

3] What is the market size of the Global Orthopedic Braces and Supports Market by 2029?

Ans. The market size of the Orthopedic Braces and Supports Market by 2029 is expected to reach US$ 5.73 Bn.

4] What is the forecast period for the Global Orthopedic Braces and Supports Market?

Ans. The forecast period for the Orthopedic Braces and Supports Market is 2023-2029.

5] What was the market size of the Global Orthopedic Braces and Supports Market in 2022?

Ans. The market size of the Orthopedic Braces and Supports Market in 2022 was valued at US$ 3.81 Bn.