Industrial Catalyst Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

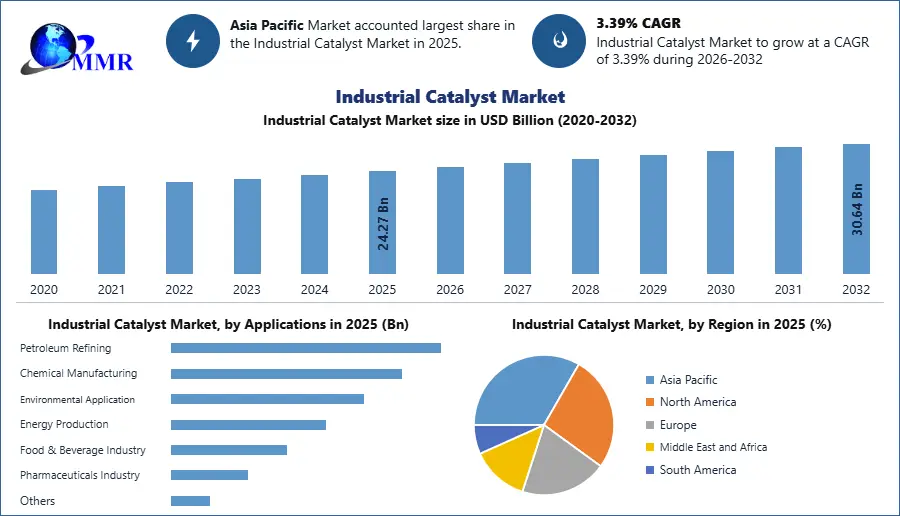

Industrial Catalyst Market size was valued at USD 24.27 Bn in 2025 and is expected to reach USD 30.64 Bn by 2032, at a CAGR of 3.39%

Overview of the Industrial Catalyst Market

The industrial catalyst market encompasses the trade of catalysts employed in diverse industrial processes to augment the speed of chemical reactions and enhance overall process efficiency. Catalysts, as substances, facilitate and expedite chemical reactions by reducing the activation energy necessary for these reactions to take place. Importantly, catalysts remain chemically unchanged at the end of the reaction and are reused in subsequent processes. By facilitating more efficient reactions, industrial catalysts contribute to improved yield and enable manufacturers to achieve desired product specifications. Additionally, they support the adoption of environmentally sustainable practices and help comply with stringent regulatory standards. The Industrial Catalyst Market is thoroughly elaborated by offering several pieces of information such as market size, key players and their market value, their recent developments as well as their partnerships, mergers, and acquisitions. The graphical representation and structural exclusive information showed the dominating region of the Industrial Catalyst Market. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the Industrial Catalyst Market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Industrial Catalyst Market Dynamics

Increasing Demand for Environment-Friendly and Sustainable Processes

The industrial catalyst market is driven by the growing emphasis on sustainable industrial practices and the need to minimize environmental impact. Catalysts enable manufacturers to implement cleaner processes, including emission control in power generation and automotive industries, water treatment, and waste management, aligning with global sustainability goals. Advancements in Catalyst Technology with continuous research and development efforts focused on enhancing catalyst performance, selectivity, and efficiency are propelling the industrial catalyst market. Innovations in catalyst design, composition, and synthesis techniques result in catalysts with improved activity, stability, and longevity, meeting the evolving requirements of diverse industries.

Stringent Regulatory Frameworks for Environmental Protection as governments and environmental agencies worldwide have implemented rigorous regulations to reduce emissions, combat pollution, and promote sustainable practices. Compliance with air quality standards, wastewater treatment guidelines, and emission controls necessitates the adoption of effective industrial catalysts, stimulating Industrial Catalyst market growth. Industrial catalysts contribute to energy conservation and cost reduction by facilitating process optimization and minimizing energy consumption. By improving reaction rates and yields, catalysts enable shorter reaction times, reduced energy requirements, and enhanced resource utilization. Consequently, industries seeking operational efficiency and cost savings embrace catalysts, bolstering Industrial Catalyst Market demand.

Opportunities, Restraints, and Trends in the Industrial Catalyst Market

Increasing Demand for Sustainable Catalysts and Advancement in technology are thriving the opportunities in industrial catalyst market

The industrial catalyst market has significant opportunities due to the rising focus on sustainability. Fundamentally, catalysts enable chemical reactions to be carried out with greater energy efficiency. While this is typically motivated by economic concerns rather than environmental ones, heterogeneous catalysts nonetheless play an important role in reducing the energy intensiveness and therefore carbon footprint of a vast array of commercial chemical processes. The expansion in the renewable energy sector opens up avenues for innovation and market expansion. The application of nanotechnology in catalyst development presents promising opportunities for the industrial catalyst market. Nanostructured catalysts offer advantages like improved surface area, enhanced reactivity, and better control over catalytic reactions. Capitalizing on these advancements in nanotechnology can lead to the development of high-performance catalysts for various industries.

The high cost of Catalysts, Limited Catalyst Lifespan and Activity, and Regulatory and Safety Challenges are the major restraints in the industrial catalyst market.

The cost of catalysts can be a limiting factor in their widespread adoption, especially for industries with tight profit margins. To overcome this restraint, catalyst manufacturers need to focus on developing cost-effective catalyst formulations and production processes that maintain quality while reducing costs. Catalyst deactivation and loss of activity over time can hinder their efficiency and increase operational costs. Addressing issues related to catalyst stability and durability is crucial to improving the performance and competitiveness of catalysts in the market. Developing catalysts with longer lifespans and improved activity retention is a challenge that needs to be addressed. The industrial catalyst market is subject to various regulations and safety standards. Compliance with these stringent regulations can pose challenges for catalyst manufacturers.

Shift toward Green and Bio-based Catalysts, Integration of Digital Technologies, and focus on adaptive catalysts are the important trends in the Industrial Catalyst Market

The market is witnessing a trend toward the development and adoption of green and bio-based catalysts. These catalysts, derived from renewable resources, offer environmental benefits and align with sustainable manufacturing practices. Industries require catalysts with precise activity, selectivity, and stability for specific reactions and processes. Catalyst manufacturers are investing in advanced catalyst design and engineering techniques to develop customized solutions that address the unique requirements of different industries. The integration of digital technologies like artificial intelligence (AI) and machine learning is transforming the industrial catalyst market. AI-driven catalyst design, virtual screening, and predictive modeling techniques are being employed to accelerate catalyst development and improve performance. The use of digital technologies enables faster and more efficient catalyst development processes, leading to improved outcomes.

Industrial Catalyst Market Segmentation Analysis

By Types

Heterogeneous Catalyst: Heterogeneous catalysts are solid substances that exist in a different phase from the reactants. They offer versatility and ease of separation from the reaction mixture, making them widely adopted in industrial applications for industrial catalyst market. Heterogeneous catalysts are present in two forms metal catalysts and metal dioxide catalysts. The metal catalyst includes Platinum, Palladium, and zeolites while metal oxide catalysts consist of Titanium dioxide and zeolite catalysts.

Homogenous Catalyst: Homogeneous catalysts are separated into phases such as in liquid or gaseous type. These molecular catalysts are soluble in the reaction medium and provide high selectivity, making them effective in catalyzing complex reactions. Transition metal complexes and acid/base catalysts are common examples of homogeneous catalysts.

By Applications

Petroleum Refining: These catalysts are majorly used in various refining processes of fuels and others in the industrial catalyst market. The catalysts used in the catalytic cracking process are mainly zeolites, similar to those used in petroleum refineries. ZSM-5, Y, silica-alumina, SAPO, MCM-41, SBA-15, and other zeolites were applied in this process to remove oxygen from bio-oils. Gasoline with anti-knocking characteristics is made with catalytic cracking of heavy hydrocarbons of selective catalysts and zeolites. Most of the petroleum refining catalysts in a modern refinery contain highly porous catalysts to provide adequate surface area for metals dispersion and the subsequent reaction to occur. The porosity of the catalyst plays a large role in the efficiency of the conversion reaction.

Chemical Manufacturing: Catalysts find widespread use in chemical manufacturing processes to enable desired reactions and increase yields. Some specific polymers have the ability to catalyze reactions with the formation of carbon-carbon and carbon-non-carbon linkages. Polyvinyl pyridine and sulfonated polystyrene are very useful and simple polymers that act as catalysts. Heterogeneous supported catalysts based on titanium compounds are used in polymerization reactions in combination with cocatalysts, and organoaluminum compounds such as triethylaluminium, Al (C2H5)3. This class of catalyst dominates the industrial catalyst industry.

Regional Analysis of the Industrial Catalyst Market

Asia Pacific: Asian countries such as China, India, and Korea are leading in the industrial catalyst market. These countries hold a large market share of the industrial catalyst market. China is the dominant market holder, as this region is experiencing major growth in past years as well as rapid industrialization, economic growth, and advancement in technology are the major key factors that drive the industrial catalyst market in the Asia Pacific region.

North America: North American industrial catalyst market is divided into key countries like the United States, Canada, and Mexico. This region is rapidly heightened in the petroleum refining industry as well as advanced chemical manufacturing companies which totally rely on research and development. Stringent environmental regulations and a growing emphasis on sustainable practices drive the adoption of catalysts in North America.

Europe: Europe is a prominent player in the industrial catalyst market. The region boasts a well-developed chemical industry and a strong commitment to sustainable practices. Countries such as Germany and France are major contributors to the market, with continuous advancements in catalyst technology and a push for cleaner and more efficient processes.

Industrial Catalyst Market Competitive Analysis

BASF has prioritized the development of catalysts for various industrial sectors such as automotive, chemicals, and refining. They have made substantial investments in research and development to enhance catalyst performance. In 2021, BASF acquired the assets of ZedX Inc., a leading provider of digital agriculture solutions. This acquisition bolsters BASF's portfolio of digital solutions for the agriculture industry. BASF offers a wide range of industrial catalysts, including those for automotive emissions control, chemical production, and petrochemical refining. Clariant focuses on the development of sustainable catalyst solutions for diverse industries. Their efforts are centered on catalysts that enable cleaner and more efficient processes. In 2020, Clariant collaborated with ExxonMobil and Saudi Basic Industries Corporation (SABIC) to develop a new catalyst for converting CO2 into plastics. This collaboration aims to advance circular economy solutions. Clariant provides catalysts for various applications, including fuel processing, chemical synthesis, and environmental applications in the Industrial catalyst market.

Johnson Matthey has made significant investments in research and development to pioneer advanced catalyst technologies for the Industrial catalyst market. They prioritize catalysts for sustainable processes and renewable energy applications. In 2021, Johnson Matthey partnered with SINOPEC to develop and commercialize advanced catalyst systems for the Chinese refining industry. The partnership aims to enhance refining processes' efficiency and sustainability. Johnson Matthey offers catalysts for a wide range of industries, including automotive, pharmaceutical, and chemical manufacturing. Albemarle has expanded its catalyst portfolio to meet emerging market demands. They concentrate on catalyst technologies for clean fuels and renewable energy applications. In 2021, Albemarle acquired Grace's Fine Chemistry Services (FCS) business, strengthening its capabilities in the custom and fine chemistry services market. Albemarle provides catalysts for various industries, including petrochemicals, specialty chemicals, and environmental applications. Haldor Topsoe has been actively developing catalyst technologies for sustainable energy production and emission control. Their focus includes catalysts for ammonia production, hydrogen production, and emissions abatement and it is clearly benefiting the industrial catalyst market. In 2020, Haldor Topsoe partnered with Nel ASA to develop high-efficiency electrolyzers for green hydrogen production. This collaboration aims to advance the commercialization of green hydrogen technologies. Haldor Topsoe offers catalysts for various industries, including ammonia production, methanol synthesis, and refining processes.

Industrial Catalyst Market Recent Industry Developments (2025–2026)

| Date | Company | Development | Impact |

|---|---|---|---|

| 19 March 2026 | BASF SE | The company started up the world’s first industrial-scale production plant for 3D-printed X3D catalysts at its Ludwigshafen site. | This technology allows for custom-designed geometries that reduce reactor pressure drop and increase active surface area for higher throughput. |

| 05 March 2026 | Topsoe A/S | The company officially appointed Elena Scaltritti as President and CEO following the completion of its 2025 fiscal year. | The leadership transition is aimed at accelerating the company's energy transition strategy and sustainable aviation fuel (SAF) catalyst portfolio. |

| 26 February 2026 | Clariant AG | The company reported a 5% growth in its Catalyst business unit for Q4 2025, driven specifically by high demand for Ethylene and Syngas catalysts. | Strong catalyst sales contributed to a 240-basis point margin improvement, offsetting declines in other specialty chemical segments. |

| 15 December 2025 | Johnson Matthey | The company opened its first hydrogen internal combustion engine (H2ICE) testing facility in Gothenburg, Sweden, with a £2.5 million investment. | The facility focuses on developing emission-control catalysts specifically for hydrogen-fueled heavy-duty truck and bus engines. |

| 12 May 2025 | Honeywell International Inc. | Honeywell completed the acquisition of Johnson Matthey’s blue hydrogen technology and associated catalyst licensing business. | This acquisition consolidates Honeywell's position in the carbon capture and hydrogen production market by integrating specialized catalyst intellectual property. |

Global Industrial Catalyst Market Scope: Inquire before buying

| Industrial Catalyst Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 24.27 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.39% | Market Size in 2032: | 30.64 USD Billion |

| Segments Covered: | by Type | Heterogeneous Catalyst Homogenous Catalyst Others |

|

| by Material | Chemical Zeolites Organometallic Materials Others |

||

| by Process Type | Fixed Bed Catalysis Fluidized Bed Catalysis Batch Catalysis Continuous Catalysis Electrocatalysis Photocatalysis |

||

| by Reaction Type | Oxidation Reactions Hydrogenation Reactions Dehydrogenation Reactions Cracking Reactions Polymerization Reactions Reforming Reactions |

||

| by Applications | Petroleum Refining Chemical Manufacturing Environmental Application Energy Production Food & Beverage Industry Pharmaceuticals Industry Others |

||

Industrial Catalyst Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Market Players of the Industrial Catalyst Market

1. BASF SE (Germany)

2. Clariant International Ltd (Switzerland)

3. Johnson Matthey (United Kingdom)

4. Albemarle Corporation (United States)

5. Haldor Topsoe A/S (Denmark)

6. W.R. Grace & Co (United States)

7. Evonik Industries AG (Germany)

8. Shell Global Solutions International BV (Netherlands)

9. UOP LLC (United States)

10. ExxonMobil Corporation (United States)

11. Chevron Phillips Chemical Company LLC (United States)

12. Axens (France)

13. Honeywell UOP (United States)

14. Croda International Plc (United Kingdom)

15. Dow Chemical Company (United States)

16. SABIC (Saudi Arabia)

17. Zeolyst International (United States)

18. Univation Technologies LLC (United States)

19. Arkema Group (France)

20. Mitsubishi Chemical Corporation (Japan)

Frequently Asked Questions and Answers of Industrial Catalyst Market

1. How does the industrial catalyst market contribute to sustainable development?

Ans: The industrial catalyst market contributes to sustainable development by enabling cleaner and more efficient industrial processes, reducing emissions and waste generation, facilitating the production of renewable energy sources, and supporting the development of green and sustainable technologies.

2. What are the emerging trends in the industrial catalyst market?

Ans: Emerging trends in the industrial catalyst market include the development of catalysts for green and sustainable processes, the integration of digital technologies for catalyst optimization, and the exploration of catalysts for emerging energy storage and conversion technologies.

3. What are the challenges faced by the industrial catalyst market?

Ans: Some challenges faced by the industrial catalyst market include high costs associated with catalyst development and manufacturing, the need for continuous innovation to meet evolving industry requirements, and the impact of catalyst deactivation and poisoning during the industrial process.

4. What is the market estimation of the Industrial Catalyst Market?

Ans: The Industrial Catalyst Market is estimated CAGR is 3.4 %.

5. What are the key drivers of growth in the industrial catalyst market?

Ans: Some key drivers of growth in the industrial catalyst market include increasing demand for cleaner and more efficient industrial processes, stricter environmental regulations, the need for sustainable and renewable energy solutions, and advancements in catalyst technologies.