India Gaming Market Size by Type, Category – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2030

Overview

The India Gaming Market size was valued at USD 1.54 Billion in 2023. The total India Gaming revenue is expected to grow at a CAGR of 28.5% from 2024 to 2030, reaching nearly USD 8.92 Billion by 2030.

India Gaming Market Overview:

India's gaming market growth is driven by widespread smartphone use, affordable internet access, and a tech-savvy youth demographic. This dynamic sector presents substantial growth potential. The India gaming market is rapidly growing, providing substantial economic, social, and technological benefits. The Indian game industry drives technological advancements, fosters innovation and entrepreneurship, promotes digital literacy, and increases India's recognition. Additionally, it serves as a platform for brand marketing, contributing to tourism and local economies.

The COVID-19 pandemic has deeply affected the India gaming market.The disruptions in the supply chain led to hardware shortages and price increases while closures of physical stores and event cancellations resulted in revenue losses. However, increased internet access and a rise in mobile gaming offered new possibilities. The pandemic accelerated digital adoption, influencing esports' growth and new gaming genres' emergence. Despite challenges, it created opportunities, such as increased gaming time, new user acquisition, and exploring innovative business models. The long-term impact requires further research, considering diverse factors like age, demographics, and socioeconomic status. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

India Gaming Market Dynamics

Increase in Players & Studios across India

The market is diversifying with the emergence of new game genres, attracting a broader player base. Increased investment from venture capitalists is fuelling ambitious projects. India has evolved into a gaming hub with the number of studios skyrocketing from 15 in 2009 to 275 in 2022. Mobile gaming dominates and draws developers. E-sports is booming, creating opportunities and viewership. This growth of India's gaming market has socio-economic impacts such as generating jobs, fostering skill development, and promoting social interaction. However, challenges like limited infrastructure in rural areas and the need for innovative monetization strategies and intellectual property development remain. Addressing these challenges is crucial for sustaining and enhancing the India gaming industry's standing.

The Metaverse Revolutionizing the India Gaming Industry

The India gaming market metaverse a virtual realm fostering interactive experiences stands poised to reshape India's gaming sector profoundly. Integrating virtual reality and augmented reality, promises increased player immersion with personalized avatars and interactive environments. Innovative revenue streams, such as play-to-earn models and in-game purchases, emerge, while subscription models offer exclusive content access. Cloud gaming enhances accessibility, especially for the mobile-dominated India gaming market, fostering inclusivity through vernacularization. This transformative landscape offers market access for India developers, enabling collaboration and the creation of novel game genres. Challenges include infrastructure, privacy concerns, and regulatory frameworks, yet embracing the metaverse positions the India gaming industry for substantial growth on both domestic and fronts.

Popularity of Real-Money Online Gaming

The real-money Online Gaming (RMG) has ignited a dual response in the India gaming market, wielding both promise and peril. On the positive side, RMG propels robust industry growth attracting investments and fostering sport’s growth. It drives technological innovation in fintech and gaming diversifying the user base. However, negative aspects include addiction concerns, cyber security risks, an unregulated India gaming market, and ethical issues. The impact on India gaming market necessitates a nuanced approach, acknowledging both contributions and challenges. Responsible gaming practices, clear regulations, increased awareness, innovation, and collaborative efforts are imperative for steering RMG toward a sustainable and responsible future in India's gaming landscape.

Smartphone penetration and affordable internet

The rise in smartphone penetration and accessible internet have driven the India gaming market into a gaming powerhouse, renowned for its explosive growth. This transformative duo has broadened gaming accessibility, reaching over 600 million smartphone users, even in rural areas. Affordable smartphones and data plans have shattered entry barriers, fostering a diverse player demographic. The mobile-centric approach dominates the India gaming market, emphasizing casual gaming and free-to-play models. E-sports, particularly in games like PUBG Mobile and Free Fire, thrives. Economic growth and job creation rise in game development, in-app purchases contribute to revenue, and substantial investments fuel India's gaming industry growth. Challenges include innovative monetization, infrastructure development, and creating top-tier content. Navigating these challenges while capitalizing on opportunities fortify India's gaming market as a leader.

India Gaming Market Segment Analysis

Based on Category, the Action segment dominated the India gaming market with the highest share of 25% in 2023. The segment is further expected to grow at a CAGR of 6.8% and maintain its dominance at the end of the forecast period. Action games deliver heart-pounding excitement, attracting thrill-seekers with diverse subgenres like FPS, battle royals, and hack-and-slash. Optimized for mobile devices in India gaming market titles like PUBG Mobile and Call of Duty Mobile thrive with sports scenes. Social features, from multiplayer to leaderboards, enhance player experiences and community building. Top games include PUBG Mobile, Call of Duty Mobile, Free Fire, Apex Legends Mobile, and the GTA franchise. Revenue streams rely on in-app purchases, offering cosmetics, weapons, season passes, and randomized loot systems. Popular among males aged 15-35, action games engage students and young professionals, foreseeing future trends in enhanced social features, sports growth, AR/VR experiences, cross-platform play, and continued mobile optimization. As a result India gaming market is growing in the forecast period.

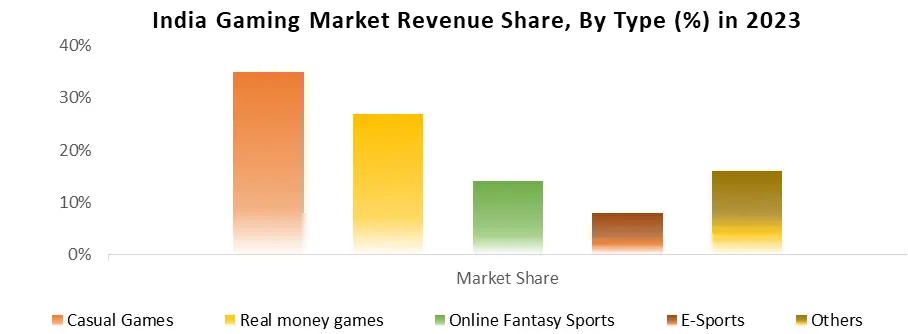

Real Money Games (RMGs) are a dynamic force in the India gaming market commanding a robust 20-25% market share, set to hit ₹29,000 crores in 2023. This genre spans card games such as Rummy and Poker, fantasy sports with Dream11 and MPL, and casual games such as Ludo and Carom. Revenue streams include entry fees, rake charges, and in-app purchases. Challenges, including regulatory uncertainty, addiction concerns, and India gaming market saturation, underscore the need for responsible gaming practices. The future holds promise with esports integration, technological advancements, and regional customization, contingent on clearer regulations to ensure fair competition and foster responsible growth.

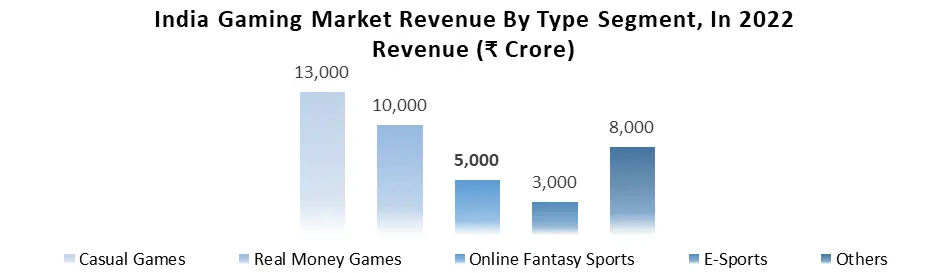

Based on Game Type Casual Games dominated the game type segment in 2022 and are estimated to hold the largest revenue share of the market during the forecast period. Real Money Games are expected to grow at a significant CAGR of 5.6 % during the forecast period. The user base is expected to increase by more than 50% by 2030, from 433 million to 657 million. Casual games, in which players play to pass the time real-money games, in which players wager real money in online games; online fantasy sports, in which players build fantasy teams and win money based on points earned; and e-sports, which are professional gaming, in which players compete for prize money. This might be attributed to the increased quantity of mobile apps and inexpensive smartphones catering to India gaming market.

India Gaming Market States Insights:

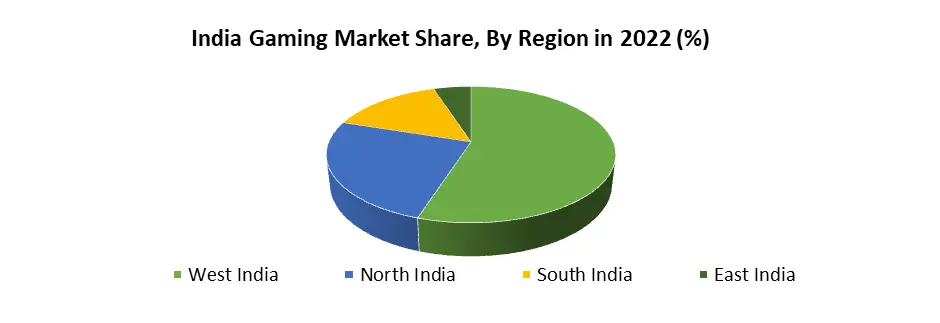

The regions in the India gaming market are segmented into North India, South India, East India, and West India. The western region in the country, especially Mumbai city is the financial capital of India. The population of Mumbai city is over 20 million which is a big factor as the adoption of smartphones is also high. Therefore, these factors dominate the India gaming market in this region and hence there is an increasing dependency on sports platforms in this region. In addition, states like Maharashtra and Gujarat are developing and the growth of small and medium-sized businesses are the major driving forces for the India gaming market and its development.

The objective of the report is to present a comprehensive analysis of the India gaming market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of macro-economic factors on the India gaming market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which give a clear futuristic view of the India gaming industry to decision-makers. The report also helps in understanding the India gaming market dynamics, and structure by analyzing the market segments and projecting the India gaming Market size. Clear representation of competitive analysis of key players by Type, price, financial position, Type portfolio, growth strategies, and regional presence in the India gaming Market make the report an investor’s guide.

India Gaming Market Scope: Inquire before buying

| India Gaming Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 1.54 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 28.5% | Market Size in 2029: | US $ 8.92 Bn. |

| Segments Covered: | by Type | Casual Games Real Money Games Online Fantasy Sports E-Sports Others |

|

| by Category | Action Shooter Role-Playing Sports Others |

||

India Gaming Market Key Players

1. Hyperlink InfoSystem

2. Sony Corporation

3. Unanimous Studios

4. Nintendo

5. Scientific Games

6. Microsoft Corporation

7. Griptonite Games

8. HData Systems

9. GSN Games

10.Nimblechapps

11.Rolocule

12.Nautilus Mobile

13.Electronic Arts

14.Timuz

15.Nazara Technologies

16.Spartan Group

17.Zensar Technologies

18.White Widget

19.TCS

20.Fgfactory

21.Scand

22.HData Systems

23.Dream 11

24.99 Games25.

Frequently Asked Questions:

1] What segments are covered in the Market report?

Ans. The segments covered in the Market report are based on Type, Application, and Region.

2] Which region is expected to hold the highest share in the Market?

Ans. The Western region is expected to hold the largest share of theMarket. Mumbai city is the capital of the country which holds the largest share of the market.

3] What is the market size of the Market by 2029?

Ans. The market size of the Market by 2030 is expected to reach USD 1.54 Bn.

4] What is the forecast period for the Market?

Ans. The forecast period for the Market is 2024-2030.

5] What was the market size of the Market in 2023?

Ans. The market size of the Market in 2023 was valued at USD 1.54 Bn.