India Electric Motor Market - Industry Structure Evaluation, Demand Drivers Analysis, Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2034

Overview

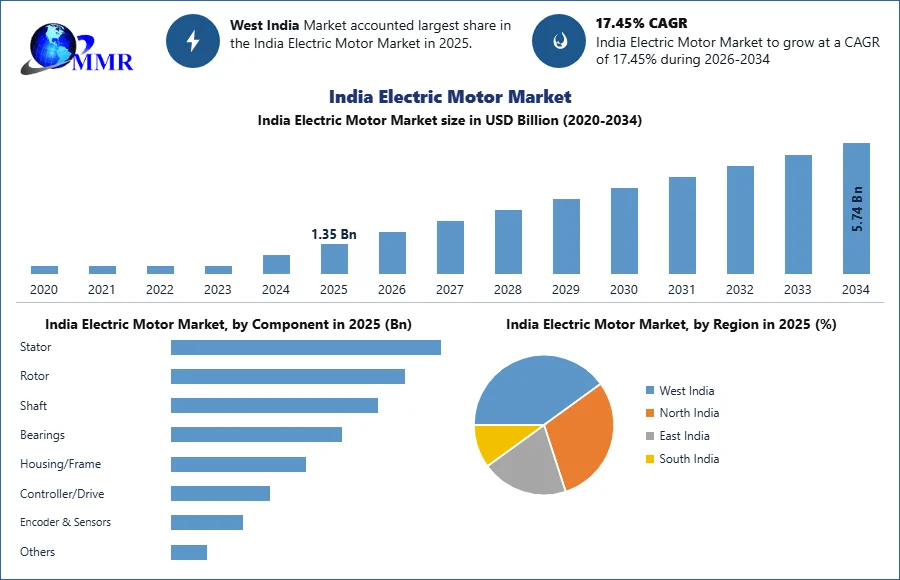

India Electric Motor Market size reached USD 1.35 billion in 2025 and is expected to reach USD 24.97 billion by 2034, growing at a CAGR of 6.2 % during the forecast period.

India Electric Motor Market Overview:

Electro-mechanical devices like electric motors operate on the principle of electromagnetic induction. They are highly efficient, long-lasting, low-maintenance, energy-efficient, and can endure strong voltage fluctuations. Furthermore, electric motors are substantially less expensive than fossil-fuel engines. There are 12 different types of electric motors available in the market. Hysteresis motors, pancake or axial rotor motors, synchronous reluctance motors, and stepper motors are some of the types of electric motors.

To know about the Research Methodology:- Request Free Sample Report

India Electric Motor Market Dynamics:

Rising Industrial Automation and Energy-Efficient Motor Adoption Driving Market Growth

The India electric motor market is witnessing robust growth, supported by rapid industrialization, infrastructure development, and the increasing adoption of energy-efficient technologies. Electric motors account for nearly 45–50% of total industrial electricity consumption, making them one of the most critical components in manufacturing operations. Consequently, industries are increasingly replacing conventional IE1 and IE2 motors with high-efficiency IE3 and IE4 motors to reduce operating costs and comply with energy conservation regulations. High-efficiency electric motors can achieve efficiencies above 95%, compared with 30–40% overall energy efficiency of conventional internal combustion engine (ICE)-based systems, making them a preferred choice across industrial and transportation applications.

India's manufacturing sector continues to expand rapidly under initiatives such as Make in India, the National Infrastructure Pipeline (NIP), and the PM Gati Shakti Master Plan, which together are accelerating investments in industrial machinery, HVAC systems, pumps, compressors, conveyors, and automation equipment. The country's manufacturing sector contributes approximately 17% of GDP, with the government targeting 25% by 2047, creating sustained demand for electric motors across multiple industries. Increasing investments in water treatment, smart buildings, renewable energy, and industrial automation are further strengthening market demand.

Government Policies Accelerating Market Growth

Government initiatives continue to play a significant role in expanding the electric motor market. Programs such as Make in India, Smart Cities Mission, AMRUT, Production Linked Incentive (PLI) schemes, and the Bureau of Energy Efficiency (BEE) standards are encouraging manufacturers and end users to adopt high-efficiency motors. The transition toward IE3 and IE4 efficiency classes is accelerating, particularly in industrial applications where electricity costs represent a significant portion of operating expenditure. In 2024, ABB India reported that sales of its IE4 low-voltage motors increased by over 100% during 2023, contributing to cumulative industrial energy savings exceeding 500 GWh across India.

Electric Vehicle Adoption Creating Strong Demand for Advanced Motors

The rapid growth of India's electric vehicle industry has emerged as one of the strongest demand drivers for electric motors. Permanent Magnet Synchronous Motors (PMSM), Brushless DC (BLDC) motors, and induction motors are increasingly used across electric two-wheelers, three-wheelers, passenger vehicles, and commercial vehicles.

According to the International Energy Agency (IEA), India remained the world's second-largest electric two-wheeler market in 2025, recording approximately 1.3 million electric two-wheeler sales. India also remained the largest global market for electric three-wheelers, where more than two-thirds of all new three-wheelers sold were electric, while electric bus sales exceeded 4,000 units during 2025 under government-supported procurement programs. These developments are significantly increasing domestic demand for traction motors and associated motor control technologies.

Expanding Application Base Across Industries

Electric motors continue to find widespread adoption across automotive manufacturing, steel production, mining, HVAC systems, agriculture, food processing, renewable energy, consumer appliances, robotics, and factory automation. Brushed DC motors remain widely used in steel mills, conveyor systems, treadmills, and industrial machinery, whereas BLDC motors dominate applications such as electric vehicles, drones (UAVs), hard disk drives, home appliances, and precision industrial equipment. Simultaneously, increasing deployment of industrial automation, robotics, CNC machines, and smart manufacturing solutions is creating substantial opportunities for servo motors, stepper motors, and high-efficiency AC motors.

The convergence of industrial modernization, stringent energy efficiency regulations, government incentives, infrastructure expansion, and accelerating electric vehicle adoption is expected to sustain strong long-term growth of the India electric motor market.

India Electric Motor Market Segment Analysis:

By Motor Type

The AC motor segment dominated the India Electric Motor Market in 2025, accounting for the largest share due to its widespread adoption across industrial, commercial, infrastructure, and utility applications. The dominance of AC motors is primarily attributed to their high efficiency, reliability, low maintenance requirements, and compatibility with India's expanding industrial automation ecosystem. Industries such as manufacturing, oil & gas, cement, mining, power generation, food processing, water & wastewater treatment, and HVAC systems extensively deploy AC induction motors for continuous-duty operations. With electric motors consuming nearly half of industrial electricity in India, industries are increasingly replacing older IE1 and IE2 motors with premium-efficiency IE3 and IE4 AC motors to reduce operational costs and comply with Bureau of Energy Efficiency (BEE) regulations. The government's emphasis on industrial modernization through initiatives such as Make in India, Production Linked Incentive (PLI) schemes, Smart Cities Mission, and PM Gati Shakti has further accelerated investments in industrial machinery and automation equipment utilizing AC motors.

By Component

The stator segment held the dominant position in the India Electric Motor Market in 2025, as it forms the core stationary component responsible for generating the rotating magnetic field required for motor operation. Every electric motor, irrespective of whether it is an AC motor, DC motor, BLDC motor, servo motor, or stepper motor, requires a stator, making it an indispensable component across virtually all motor categories. The increasing production of industrial motors, electric vehicle traction motors, HVAC equipment, pumps, compressors, and consumer appliances has substantially boosted demand for high-performance stators. The transition toward premium-efficiency IE3, IE4, and IE5 motors has further increased the requirement for high-quality stator laminations utilizing low-loss electrical steel and superior magnetic materials. Government initiatives promoting domestic manufacturing under the Make in India program, combined with localization efforts by leading motor manufacturers, have encouraged investments in stator production facilities across the country.

India Electric Motor Market Regional Insights:

West India dominated the India Electric Motor Market in 2025, accounting for the largest regional share owing to its strong industrial base, advanced manufacturing ecosystem, and significant investments in automotive, engineering, chemicals, and infrastructure sectors. States such as Maharashtra, Gujarat, and Goa serve as major manufacturing hubs, housing thousands of industrial facilities that extensively utilize electric motors in pumps, compressors, conveyors, HVAC systems, machine tools, and automated production lines. Maharashtra remains India's leading industrial state with major manufacturing clusters in Mumbai, Pune, Nashik, Aurangabad, and Nagpur, while Gujarat has established itself as a center for petrochemicals, chemicals, pharmaceuticals, textiles, ports, and renewable energy projects. The region also benefits from a well-developed logistics network, reliable power infrastructure, and the presence of leading domestic and multinational motor manufacturers.

Increasing investments in industrial automation, smart factories, metro rail projects, commercial buildings, and data centers have further accelerated the demand for high-efficiency AC, BLDC, and servo motors. Moreover, West India has emerged as one of the country's largest electric vehicle manufacturing regions, with major OEMs and component suppliers driving demand for traction motors and motor components. Government initiatives such as Make in India, Production Linked Incentive (PLI) schemes, the Delhi-Mumbai Industrial Corridor (DMIC), and state-level industrial policies continue to attract manufacturing investments. Combined with growing renewable energy installations, expanding water and wastewater infrastructure, and increasing adoption of energy-efficient IE3 and IE4 motors, these factors ensure that West India remains the dominant regional market for electric motors in 2025 and is expected to maintain its leadership throughout the forecast period.

Recent Developments

February 2025 – ABB India Ltd. Expands Energy-Efficient Motor Portfolio

In February 2025, ABB India Ltd. strengthened its electric motor business by expanding its portfolio of high-efficiency IE4 and IE5 low-voltage motors for industrial applications. The company focused on helping Indian manufacturers reduce electricity consumption and improve operational efficiency in sectors such as cement, metals, mining, water treatment, chemicals, food & beverage, and HVAC. ABB also expanded its digital motor monitoring solutions by integrating predictive maintenance and condition monitoring technologies into its industrial motor offerings. These smart solutions enable real-time monitoring of vibration, temperature, and energy consumption, helping industries minimize unplanned downtime and maintenance costs.

November 2024 – Siemens India Ltd. Expands Manufacturing and Digital Motion Solutions

In November 2024, Siemens India Ltd. announced further expansion of its industrial automation and motion technologies business by strengthening the supply of high-efficiency electric motors and digital drive systems for Indian industries. The company focused on integrating electric motors with variable frequency drives (VFDs), industrial automation platforms, and digital monitoring software to improve productivity and energy efficiency. Siemens continued supporting sectors including automotive, pharmaceuticals, food processing, cement, steel, and infrastructure projects. The company also emphasized localization of manufacturing under the Make in India initiative while increasing investments in smart manufacturing technologies.

India Electric Motor Market Scope: Inquiry Before Buying

| India Electric Motor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 1.35 USD Billion |

| Forecast Period 2026-2034 CAGR: | 17.45% | Market Size in 2034: | 5.74 USD Billion |

| Segments Covered: | by Motor Type | AC Motor DC Motor Brushless DC (BLDC) Motor Stepper Motor Servo Motor Universal Motor Others |

|

| by Component | Stator Rotor Shaft Bearings Housing/Frame Controller/Drive Encoder & Sensors Others |

||

| by Voltage | Low Voltage Medium Voltage High Voltage |

||

| by Power Rating | Up to 1 kW 1–10 kW 10–100 kW 100–500 kW Above 500 kW |

||

| by Application | Pumps Fans & Blowers Compressors Conveyors HVAC Systems Machine Tools Robotics & Automation Electric Vehicles Others |

||

| by End-Use Industry | Automotive Industrial Manufacturing Oil & Gas Power Generation Water & Wastewater Food & Beverage Chemicals & Petrochemicals Mining & Metals Building & Construction Aerospace & Defense Healthcare Others |

||

Key players/Competitors profiles covered in the India Electric Motor Market report in a strategic perspective

- Bharat Heavy Electricals Ltd. (BHEL)

- CG Power and Industrial Solutions Ltd.

- Bharat Bijlee Limited

- Kirloskar Electric Company Ltd.

- ABB India Ltd.

- Siemens India Ltd.

- WEG Industries (India) Pvt. Ltd.

- Nidec India Private Limited

- Marathon Electric India

- Regal Rexnord India

- Toshiba Transmission & Distribution Systems India

- Hindustan Electric Motors

Table of Contents

- India Electric Motor market size estimation and growth outlook (2025–2034)

- Comprehensive definition of the electric motor industry and product classification

- Inclusion criteria and exclusions were considered within market estimation

- Electrical efficiency standards governing electric motor manufacturing

- Government quality standards and compliance requirements

- Energy efficiency norms impacting motor design and development

- Import regulations and tariff structures affecting market competitiveness

- Compliance challenges faced by manufacturers and importers

- Future regulatory outlook shaping industry operations

- Overview of stators, rotors, copper winding wires, magnets, controllers, and bearing ecosystem

- Industry value chain structure from raw material suppliers to end-use industries

- Standard units, metrics, and forecasting methodologies used globally

- India Electric Motor Market Trends

- India Electric Motor Market DROC Analysis

- Drivers

- Restraints

- Opportunities

- Challenges

- PORTER’s Five Forces Analysis

- Supplier power

- Buyer power

- Threat of substitutes

- Threat of new entrants

- Competitive rivalry

- PESTLE Analysis

- Influence of GDP growth on industrial activity

- Infrastructure development driving motor demand

- Manufacturing sector expansion supporting industrial motor consumption

- Urbanization and smart city projects increasing HVAC and pump demand

- Growth in automation and industrial machinery investments

- Expansion of EV ecosystem supporting traction motor demand

- Evolution of energy-efficient industrial systems

- Development of brushless DC (BLDC) motor technologies

- Smart and connected motor innovations

- High-efficiency IE3 and IE4 motor advancements

- Lightweight and compact motor design developments

- Noise and vibration reduction technologies

- AI- and IoT-enabled predictive maintenance systems

- Digital monitoring technologies for industrial applications

- Future technology roadmap for next-generation electric motors

- Current demand trends across industrial and commercial applications

- Domestic manufacturing capacity assessment

- Import dependency affecting supply-demand balance

- OEM procurement and distributor stocking practices

- Seasonal demand fluctuations linked to construction and agriculture

- Forecast analysis of market equilibrium through 2034

- Import trends for motors, copper winding wires, magnets, and components

- Export performance of Indian electric motor manufacturers

- Dependency on China and Southeast Asia for components

- Global supply chain shifts influencing sourcing strategies

- Tariff structures impacting international competitiveness

- Future outlook for exports and localization opportunities

- Shift toward energy-efficient motor systems

- Rising demand for BLDC and smart motors

- Increasing preference for compact and lightweight motors

- Industrial automation driving advanced motor adoption

- Electrification trends supporting traction motor demand

- Integration of digital motor control systems

- Manufacturing sector dominance in industrial motor consumption

- HVAC industry driving compressor and fan motor demand

- Automotive and EV industries increasing traction motor demand

- Agriculture sector supporting pump motor consumption

- Infrastructure and water treatment projects boosting industrial motor demand

- Renewable energy installations creating specialized motor demand

- Lifecycle assessment of electric motors from production to disposal

- Copper recycling ecosystem development in India

- Energy-efficient motor adoption reducing power consumption

- Sustainable manufacturing and green production initiatives

- Eco-friendly packaging and recyclable component adoption

- Circular economy initiatives in motor refurbishment and recycling

- Future outlook for sustainable electric motor technologies

- Dependence on imported magnets, semiconductors, and controllers

- Domestic production capabilities and localization trends

- Supply gaps influencing import requirements

- Government initiatives supporting self-reliance in manufacturing

- Challenges in reducing dependency on Chinese imports

- Future outlook for domestic production expansion

- Infrastructure projects increasing industrial motor demand

- Metro, railway, and highway projects driving equipment motor consumption

- Real estate growth influencing HVAC and pump motor demand

- Urbanization trends supporting residential appliance motor demand

- Industrial maintenance activities boosting aftermarket demand

- Long-term infrastructure pipeline supporting future market growth

- Construction equipment and industrial machinery driving motor adoption

- Manufacturing sector expansion increasing industrial motor usage

- Metalworking and assembly operations requiring precision motors

- Cement, mining, and heavy industries demanding heavy-duty motors

- Industrial automation trends influencing advanced motor requirements

- Future industrial expansion supporting long-term market demand

- Automotive manufacturing growth driving motor demand

- EV production increasing traction motor requirements

- Expansion of EV charging and mobility ecosystem

- OEM standards influencing motor specifications

- Automation in automotive assembly lines boosting smart motor demand

- Future automotive trends shaping motor innovation

- Solar projects increasing pump and drive motor demand

- Wind energy installations requiring advanced generator motors

- Factory automation driving precision motor usage

- Smart manufacturing ecosystem supporting connected motor adoption

- Industrial maintenance cycles influencing replacement demand

- Future energy transition impacting motor consumption patterns

- Size of motor service and repair market in India

- Revenue split between OEM-authorized and independent service providers

- Key service segments including rewinding and retrofit services

- Pricing benchmarks for repair versus replacement

- Margin profile and economics of service businesses

- Regional service hub concentration and workforce availability

- Predictive maintenance and condition monitoring service trends

- Annual maintenance contract (AMC) business opportunities

- Role of distributors and dealers in market expansion

- OEM channel dominance in industrial motor sales

- Industrial contracts ensuring steady B2B demand

- E-commerce platforms emerging for small motor sales

- Logistics infrastructure supporting nationwide distribution

- Omnichannel strategies improving market accessibility

- Increasing awareness regarding energy efficiency benefits

- Brand preference influencing purchasing decisions

- Price sensitivity affecting premium motor adoption

- Importance of warranty and after-sales service support

- Influence of OEMs and contractors on supplier selection

- Digital platforms shaping industrial procurement decisions

- Future consumer trends driving smart motor demand

- Adoption of IoT-enabled connected motor systems

- Predictive maintenance reduces operational downtime

- Digital platforms enabling real-time monitoring and diagnostics

- Automation improves industrial workflow efficiency

- AI integration enhancing motor performance optimization

- Future digital transformation trends reshaping industry operations

- Volatility in copper, steel, and magnet prices

- Supply chain disruptions affecting component availability

- Regulatory changes creating compliance challenges

- Counterfeit products are impacting organized market players

- Obsolescence risks for low-efficiency motors

- Growth opportunities in energy-efficient motors

- EV and traction motor expansion opportunities

- Smart motor and automation system demand growth

- Localization opportunities for components and winding wires

- Export opportunities for Indian motor manufacturers

- Future investment potential across industrial applications

- Make in India & Manufacturing Promotion Initiatives

- Production Linked Incentive (PLI) Schemes for Electrical Equipment & EV Ecosystem

- Energy Efficiency Regulations (BEE, IE2, IE3 & IE4 Standards)

- FAME II & State EV Policies Driving Traction Motor Demand

- Import Regulations, Tariff Structures & Localization Policies

- MSME Support, Industrial Clusters & Skill Development Programs

- Renewable Energy, Infrastructure & Smart City Policies Supporting Motor Demand

- Copper winding wire demand by motor category

- Consumption trends across industrial applications

- Major winding wire manufacturers and supplier ecosystem

- Copper vs aluminum winding trends and efficiency comparison

- Pricing trends and raw material volatility impact

- Localization opportunities in winding wire manufacturing

- Future demand outlook for enamelled copper winding wires

- Capex investments by leading motor manufacturers

- FDI trends in the electrical equipment and EV motor sector

- Government incentives supporting manufacturing expansion

- Investments in advanced motor technologies and automation

- Mergers, acquisitions, and strategic alliances

- VC and PE funding trends in smart motor startups

- Greenfield Brownfield Manufacturing Expansion Trends

- Value chain overview from raw materials to final assembly

- Domestic manufacturing ecosystem and vendor base

- Dependence on imported magnets and critical components

- Supply chain constraints, including logistics and material volatility

- Copper winding wire supply ecosystem analysis

- Localization opportunities under the Make in India initiatives

- Cost structure analysis across motor manufacturing

- India Electric Motor Market Size and Forecast, By Motor Type

- AC Motor

- Induction AC Motor

- Synchronous AC Motor

- DC Motor

- Brushed DC Motor

- Brushless DC Motor (BLDC)

- Servo Motor

- Stepper Motor

- Gear Motor

- Traction Motor

- Others

- AC Motor

- India Electric Motor Market Size and Forecast, By Component

- Motor Stator

- Rotor, Shaft & Bearings

- Permanent Magnet

- Copper Winding Wire

- Casing & Housing

- Wiring & Connectors

- Others

- India Electric Motor Market Size and Forecast, By Voltage

- Low Voltage Motors

- Medium Voltage Motors

- High Voltage Motors

- India Electric Motor Market Size and Forecast, By Power Rating

- Up to 1 HP

- 1 HP to 10 HP

- 11 HP to 100 HP

- Above 100 HP

- India Electric Motor Market Size and Forecast, By Application

- Industrial Machinery

- Pumps & Compressors

- HVAC Systems

- Consumer Appliances

- Automotive & EV

- Agriculture Equipment

- Robotics & Automation

- Power Generation Equipment

- Water & Wastewater Equipment

- India Electric Motor Market Size and Forecast, By End-Use Industry

- Manufacturing

- Automotive

- Consumer Appliances

- Agriculture

- Power & Utilities

- Oil & Gas

- Chemicals & Petrochemicals

- Mining & Metals

- Water Treatment

- India Electric Motor Market Size and Forecast, By Distribution Channel

- OEM

- Aftermarket

- India Electric Motor Market Size and Forecast, By Distribution Channel

- North India

- South India

- East India

- West India

- Overview

- Business Portfolio

- Financial Overview

- SWOT Analysis

- Strategic Analysis

- Recent Developments

- Bharat Heavy Electricals Ltd. (BHEL)

- CG Power and Industrial Solutions Ltd.

- Bharat Bijlee Limited

- Kirloskar Electric Company Ltd.

- ABB India Ltd.

- Siemens India Ltd.

- WEG Industries (India) Pvt. Ltd.

- Nidec India Private Limited

- Marathon Electric India

- Regal Rexnord India

- Toshiba Transmission & Distribution Systems India

- Hindustan Electric Motors

- Overview of competitive intensity among major electric motor manufacturers

- Strategic initiatives adopted by companies to strengthen market presence

- Differentiation strategies based on energy efficiency, smart motor technologies, and product reliability

- Competitive benchmarking across pricing, efficiency, performance, and distribution capabilities

- Market entry barriers affecting new participant competitiveness and expansion

- Future competitive outlook driven by EV motors, automation, and smart motor adoption

- Expansion strategies focusing on manufacturing capacity and regional distribution growth

- Product diversification strategies covering industrial, HVAC, EV, pump, and automation applications

- Strategic collaborations enhancing smart motor systems and digital monitoring capabilities

- Investment in research and development for BLDC, IE3, and IE4 motor technologies

- Market penetration strategies targeting industrial clusters and Tier II/III cities

- Long-term growth strategies aligned with localization and sustainability goals

- Overview of AC, DC, BLDC, servo, and traction motor product offerings

- Industrial-grade motor portfolio covering heavy-duty applications

- Specialized motors designed for automotive, HVAC, water treatment, and industrial automation industries

- Product differentiation based on efficiency, torque, speed, durability, and digital integration

- New product launches addressing industrial and commercial user requirements

- Future product development strategies aligned with smart and connected motor demand

- Revenue trends of leading electric motor companies over recent years

- Profit margin analysis across industrial and commercial motor categories

- Capital expenditure trends supporting manufacturing and localization initiatives

- Investment patterns in automation, smart motor systems, and energy-efficient technologies

- Financial stability and growth potential of major market participants

- Future financial outlook based on expansion and technological innovation strategies

- Overview of manufacturing facilities and geographic production distribution

- Production capacity utilization trends across major electric motor manufacturers

- Investment in advanced automation and smart manufacturing technologies

- Expansion of assembly plants supporting rising domestic and export demand

- Supply chain integration improving manufacturing and operational efficiency

- Future production expansion plans aligned with forecasted market growth

- Distribution strategies covering OEM, industrial, dealer, and aftermarket channels

- Role of distributors and system integrators in market penetration and expansion

- E-commerce platforms influencing small motor and spare parts sales

- Logistics and warehousing efficiency impacting nationwide product availability

- Strategic partnerships with industrial buyers, contractors, and OEMs

- Future distribution expansion targeting underserved industrial regions

- Investment in R&D for BLDC, servo, and energy-efficient motor technologies

- Focus on smart connected motors and IoT integration initiatives

- Collaboration with technology partners for automation and controller innovation

- Patent filings and intellectual property strategies within the electric motor industry

- Development of customized motors for specialized industrial applications

- Future innovation roadmap aligned with digitalization and sustainability trends

- Overview of recent mergers and acquisitions in the electric motor industry

- Strategic alliances enhancing technology and market expansion capabilities

- Joint ventures supporting localized manufacturing and sourcing initiatives

- Impact of acquisitions on competitive positioning and market share growth

- Partnership strategies with OEMs, EV manufacturers, and industrial clients

- Future outlook on consolidation trends within the electric motor market

- Brand positioning strategies targeting industrial and commercial customers

- Marketing campaigns promoting energy efficiency, reliability, and performance benefits

- Digital marketing initiatives enhancing customer engagement and brand visibility

- Sponsorships and industry partnerships strengthening market recognition

- Customer loyalty programs driving repeat procurement and long-term contracts

- Future branding strategies focusing on sustainability and smart motor positioning

- Key customer segments across industrial, automotive, HVAC, utility, and agriculture sectors

- Long-term contracts with infrastructure and manufacturing companies

- OEM partnerships influencing industrial motor demand and procurement agreements

- Customer retention strategies enhancing loyalty and after-sales engagement

- Feedback mechanisms improving product quality and performance standards

- Future customer acquisition strategies targeting emerging industrial sectors

- Export performance of Indian electric motor companies across global markets

- Key export destinations contributing significantly to revenue growth

- Competitive advantages in international motor markets and positioning strategies

- Challenges in global expansion including certification and compliance requirements

- Strategies for increasing international footprint and brand visibility

- Future export opportunities across emerging and developed economies

- Raw material sourcing strategies for copper, magnets, steel, and components

- Supplier relationships influencing cost efficiency and quality control

- Inventory management practices optimizing operational efficiency

- Logistics strategies reducing transportation costs and delivery timelines

- Risk management approaches addressing global supply chain disruptions