Hirudin Market Size by Product Type, Application, Price Range, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

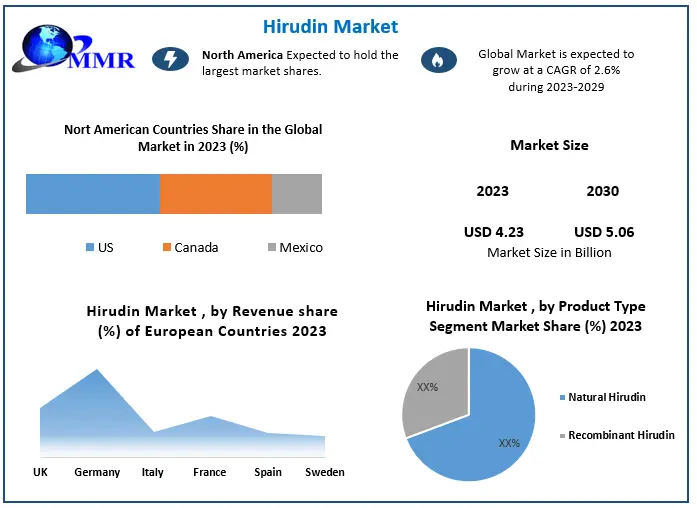

The Hirudin Market size was valued at USD 4.23 Bn. in 2023 and the total Hirudin revenue is expected to grow at a CAGR of 2.6% from 2024 to 2030, reaching nearly USD 5.06 Bn. by 2030.

Hirudin Market Overview:

Hirudin is an anticoagulant that occurs naturally in the secretions of leeches. It functions by binding to the enzyme thrombin, which is responsible for blood coagulation. Hirudin is used to prevent or treat blood clotting and in some cancer treatments.

The report discusses the market size of the Hirudin market which is been forecasted to reach 5.06 Bn USD by the year 2030 with a CAGR of 2.6%. The growth is affected by various market dynamics such as treatment of cardiovascular diseases, development of new hirudin products and use of hirudin in cancer treatment. The report discusses these dynamics and the strategies the companies to implement to leverage upon to opportunities and mitigate the threats. The hirudin market is also been analysed based upon the segments such as Product Type, application, Price Range , End-user and region and how each segment have different growth potential for the Hirudin Market. The report also discusses the various key players in the Hirudin Industry and their internal and external strategy to thrive in the rapidly evolving market.

Hirudin Market Research Methodology

The report covers an in-depth analysis of the industry. Key insights of the report include the Hirudin Market size and the growth rate. A thorough regional analysis of the Hirudin industry is conducted at a global, regional and country level. Such an analysis provides valuable information on market penetration, regional dominance and growth strategies adopted by the key players in the market. The major countries in each region are mapped according to their revenue contribution to the global Hirudin Market. To understand the competitive landscape of the Hirudin Market, key players and new entrants in the market are listed. Growth indicators such as company profiles, revenue and share, core competitors, recent developments, new growth strategies, technological advancements and mergers and acquisitions are covered. The report provides a competitive analysis of Hirudin Market drivers, restraints, opportunities and growth strategies.

PESTLE, SWOT and Porter’s five forces were used for industry analysis of the Hirudin Market. Swot analysis is used to identify the strength and weaknesses of the market. The bottom-up approach was used to estimate the Hirudin Market size. The report includes the Hirudin Market’s major strategic developments, comprising R&D, new product launches, M&A, partnerships, agreements, collaborations, joint ventures and regional growth of the key competitors. The report includes an analysis of the global, regional and country levels. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Hirudin Market Dynamics

Increasing Demand for Biosimilars

The appeal for biosimilars, including hirudin, that are reduced-cost duplicates of biologic medicines is on the upswing. Biologic medicines utilize living microorganisms and are commonly more expensive than classic chemical medicines. The growing attraction for biosimilars is foreseen to propel the advancement of the Hirudin Market. Biosimilars offer an economic substitute for the original biologic medicines, permitting them to be easily accessible to a more comprehensive populace. This cost-effectiveness aspect assumes a central position in triggering the craving for hirudin as more patients can now execute this crucial treatment. As the Hirudin Market for biosimilars widens, it is projected that the longing for hirudin will advance further. The supply of less-expensive preferences encourages patient obedience to ordered remedies, securing more favourable governance of CVDs and correlated conditions.

Increasing Prevalence of Cardiovascular Diseases (CVDs)

Cardiovascular diseases (CVDs) are becoming a global health issue. CVDs killed 17.9 million people in 2019, according to WHO data. Experts expect 23.6 million by 2030. Age is one of the main risk factors for CVDs, which have increased. CVDs are rising because to global ageing. Heart attacks, strokes, and other cardiovascular illnesses affect older persons disproportionately. Due to hormonal and genetic variations, males are more prone to acquire CVDs than females.

Heredity also increases the risk of CVDs, highlighting its importance. Finally, smoking, obesity, physical inactivity, and poor diets are major contributors to CVD cases. Lifestyle decisions worsen cardiovascular health and increase CVD risk. The rising prevalence of CVDs will increase demand for blood-thinning drugs like hirudin, which prevents blood clots and heart attacks and strokes. Hirudin may become a more important preventative and therapeutic option as CVDs become more common which is expected to drive the growth of the Hirudin Market.

Government Initiatives to Support the Development of New Hirudin Products:

Governments worldwide have proactively taken steps to promote the creation of novel hirudin commodities. This pledge seeks to uncover and launch better remedial alternatives for CVDs and other blood clot-related illnesses. The capital infusion into research and development is poised to boost the expansion of the hirudin industry. Government enterprises center on encouraging pioneering thoughts in the healthcare realm, with a specifically substantial weightage on propelling hirudin-based commodities. These endeavours comprise allotting funds for studies, presenting more reliable and secure healthcare opportunities for professionals. With greater government financing, the discovery of innovative hirudin products is expected, generating progress in patient care and an increase in the Hirudin Market.

Rising Awareness about the Benefits of Hirudin:

Hirudin has received widespread recognition as a remarkable solution for preventing and treating numerous ailments, including cardiovascular diseases (CVDs), deep vein thrombosis (DVT) and pulmonary embolism (PE). The word about hirudin's incredible benefits is rapidly spreading, resulting in an exponential surge in the demand for this drug. Hirudin has a potent blood-thinning effect that has been proven to be both safe and well-tolerated by patients. It is an enticing treatment option for those in dire need of blood-clot prevention or treatment, owing to its effectiveness and safety profile. With an ever-increasing awareness among healthcare practitioners and patients of the favourable outcomes attributed to hirudin, the demand for Hirudin Market is expected to rise steadily.

Hirudin-made products come with a hefty price tag

The exorbitant cost of goods derived from hirudin poses a major predicament in the market. Hirudin, known for its intricate molecular structure, is challenging to manufacture, consequently driving up production expenses. Additionally, hirudin drugs are prevalent in high-stakes situations, such as heart surgeries, where precision and effectiveness play a pivotal role in saving lives. All these factors culminate in the overall cost of hirudin-made goods. For instance, a solitary shot of the medication Lepirudin, synthesized from hirudin, can rack up to $1,000 in value. The exorbitant costs make hirudin products inaccessible and unaffordable, mainly in low-resource areas like impoverished countries or budget-strapped hospitals.

Hirudin-made products are hard to come by: The short supply of hirudin goods presents challenges, exerted by several factors. Scarce hirudin products on the market lead back to the elevated production costs and complex manufacturing process. Further, some countries do not necessitate hirudin products, causing limited availability. As a result, many regions in Africa and Asia face challenges in accessing hirudin products. The shortage complicates the use of hirudin-made products, primarily in areas with minimal accessibility like low-income countries or under-equipped hospitals that fail to meet the prerequisites to obtain and render hirudin goods.

Hirudin Market Segment Analysis

In terms of type, the global market is segmented into recombinant hirudin and natural hirudin. The highest revenue in the global market is generated by the recombinant hirudin segment due to challenges in sourcing the anticoagulant from its natural state. According to MMR research study, the United States government allocated approximately USD 7.7 billion for biotechnology development, a figure expected to further increase in the coming years as the demand for advanced bio-research continues to grow.

Hirudin Market Regional Analysis

The report discusses the regional analysis of different regions and has observed various parameters which help in evaluating the Hirudin Market growth potential. The report observed that North America, which has a 35% market share in 2023 for the Hirudin Market accounts for the largest share due to its vast application for hirudin in cardiovascular disease treatment. Europe comes in second with around 25% market share. During the forecast period, it is observed that Asia Pacific is the fastest growing market (currently having a 20% market share). This is due to the technological advancements in the Asian countries which they are implementing in their healthcare infrastructure.

South America's hirudin market is presently the smallest in the world, it accounted for 10% of the global market in 2023. Despite this, market expansion is anticipated to be substantial in the future years. This region's market expansion is primarily driven by the rising prevalence of cardiovascular diseases and the increased adoption of new technologies.

The report dives into the deep understanding of how the market share of each region is going to act by the Hirudin Market dynamics and how the hirudin manufacturer could understand these regional insights and align their strategy accordingly.

Recent Developments

1. In August 2022, Merck & Co., a prominent American multinational pharmaceutical company, disclosed the approval granted by the US Food and Drug Administration (FDA) for its groundbreaking investigational anticoagulant therapy known as MK-2060. This innovative therapy is anticipated to play a crucial role in mitigating the risk of significant thrombotic cardiovascular events in patients facing the advanced stage of renal disease.

2. In December 2020, NATCO Pharma Limited made a noteworthy announcement about introducing RPIGAT, a Rivoraxaban molecule, into the Indian pharmaceutical market. This product, classified as an anticoagulant medicine, is designed for the effective treatment of blood clots. Notably, at the time of its launch, Rivaroxaban was marketed under the brand name Xarelto by Bayer.

Hirudin Market Scope: Inquire before buying

| Global Hirudin Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 4.23 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 2.6% | Market Size in 2030: | US $ 5.06 Bn. |

| Segments Covered: | By Product Type | Natural Hirudin Recombinant Hirudin |

|

| By Application | Anticoagulant therapy Thrombosis therapy Research applications Others |

||

| By Price Range | Premium Economy |

||

| by End-User | Hospitals Clinics Research laboratories Others |

||

Hirudin Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Hirudin Market Key Players:

North America:

1. Pfizer Inc. (United States)

2. Bristol Myers Squibb Company (United States)

3. Johnson & Johnson (United States)

4. Eli Lilly and Company (United States)

5. Merck & Co., Inc. (United States)

6. Gilead Sciences, Inc. (United States)

7. Amgen Inc. (United States)

8. Biogen Inc. (United States)

9. AbbVie Inc. (United States)

10. Novartis International AG (Switzerland)

11. Roche Holding AG (Switzerland)

Europe:

1. GlaxoSmithKline plc (United Kingdom)

2. AstraZeneca PLC (United Kingdom)

3. Bayer AG (Germany)

4. Sandoz International GmbH (Germany)

Asia Pacific:

1. Dr. Reddy's Laboratories Ltd. (India)

2. Cipla Limited (India)

3. Takeda Pharmaceutical Company Limited (Japan)

4. Sinopharm Group Co., Ltd. (China)

5. Sinovac Biotech Ltd. (China)

6. Astellas Pharma Inc. (Japan)

7. CSL Limited (Australia)

8. Serum Institute of India Pvt. Ltd. (India)

9. Biocon Limited (India)

FAQs:

1. Which region has the largest share in Global Hirudin Market?

Ans: North America region holds the highest share in 2023.

2. What is the growth rate of Global Hirudin Market?

Ans: The Global Hirudin Market is growing at a CAGR of 2.6% during forecasting period 2024-2030.

3. What segments are covered in Global Hirudin market?

Ans: Global Hirudin Market is segmented into Product Type, Application, Price Range End-user and region.

4. Who are the key players in Global Hirudin market?

Ans: The important key players in the Global Hirudin Market are – Pfizer Inc. (United States), Sanofi S.A. (France), GlaxoSmithKline plc (United Kingdom), Novartis International AG (Switzerland), Bristol Myers Squibb Company (United States), AstraZeneca PLC (United Kingdom),Johnson & Johnson (United States),Eli Lilly and Company (United States) and Others.

5. What is the study period of this market?

Ans: The Global Hirudin Market is studied from 2023 to 2030.