Global Healthcare IT Integration Market Size by Product, Services, End User and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2029

Overview

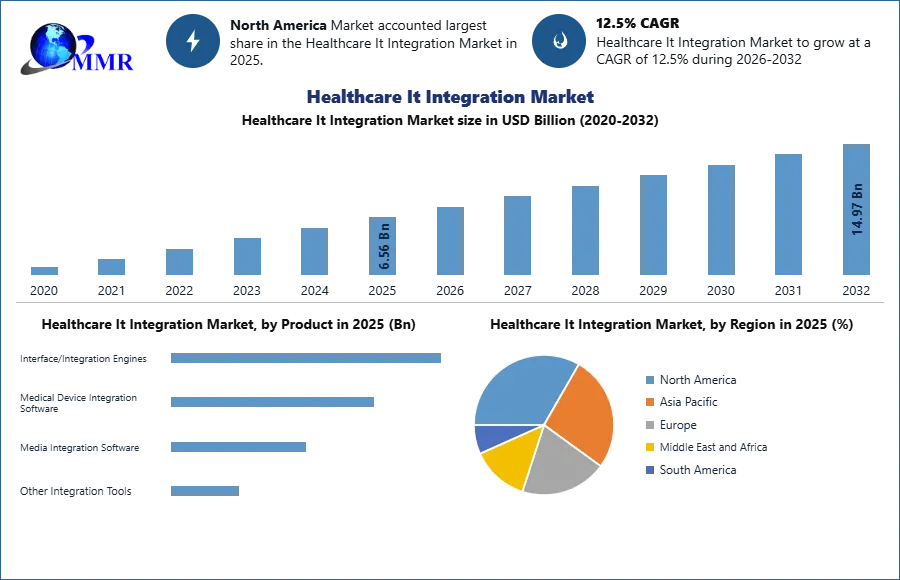

Healthcare IT Integration Market size was valued at USD 6.56 Bn. in 2025 and the total Healthcare IT Integration revenue is expected to grow at a CAGR of 12.5% from 2026 to 2032, reaching nearly USD 14.97 Bn.

Global Healthcare IT Integration Market Overview:

Healthcare IT integration allows healthcare devices to collect and exchange data with the cloud as well as with one another, allowing for the collection of data that can be precisely evaluated at breakneck speed. IoT integrates sensor output and communications to perform services that were previously considered notional, ranging from monitoring and diagnostics to delivery methods.

The sensors might be wearable, cloud-based, or inserted in a device. The healthcare business today has a dynamic collection of patient data to stimulate diagnoses and preventative care, as well as to estimate the likely outcome of preventive therapy, thanks to developments in sensors and ICT. Healthcare IT integration, such as automated drug dispensers in hospitals, contributes to improved efficiency. These integrated sensors are also utilized to monitor medicinal cold storage in warehouses and well-funded pharmacy shops with storage rooms.

Factors such as the growing utilization of electronic health records and other healthcare IT solutions, the rising need for telehealth services, and remote patient monitoring solutions are driving the market. Additionally, one of the most significant advances in artificial intelligence (AI) in healthcare is the use of machine learning to evaluate massive volumes of patient data and other information. Either a software database or electronic medical/health records are used to store patient data.

According to Selecthub research from 2025, electronic health record/ electronic medical record (EHR/EMR) use rates were 89% in 2025. According to the record, the healthcare industry is expected to experience major disruption due to technologies such as artificial intelligence (AI), blockchain, clinical decision support (CDS), and the existence of IT behemoths such as Epic and Cerner. The rapid improvements in technology were already influencing the future of electronic medical records. As AI and virtual assistants such as Alexa and Siri become more generally available and powerful, they are expected to be used in the health IT industry and drive market growth. However, a lack of trained professionals in the healthcare IT industry restrains the market growth during the forecast period. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Healthcare IT Integration Market Dynamics:

Rising emergence of electronic healthcare IT solutions to boost Healthcare IT Integration Market

Patient records are complicated, private, and sometimes unstructured. Integrating this data into the process of healthcare delivery is a barrier that must be overcome in order to achieve prospects for enhanced patient care. Even though EHRs have been in use for more than a decade, the market has lately gained steam as a result of government measures in many nations to increase patient data protection. In the United States, for example, the Health Information Technology for Economic and Clinical Health (HITECH) Act, adopted as part of the American Recovery and Reinvestment Act (ARRA), provided financing to hospitals and clinicians that demonstrated significant use of EHRs.

The HITECH regulatory requirements have accelerated the use of EHRs and EMRs. Another significant factor in the country is the growing number of accountable care organizations (ACOs), which raises the need for EHRs and EMRs. Government initiatives in other countries, like Denmark, Sweden, France, and Canada, are also supporting the adoption of EHRs and mandating their meaningful use in order to control rising healthcare costs and improve patient care quality.

Additionally, IT services provide an integration of many end users throughout the healthcare system, including hospitals, nursing care units, pharmacies, and medical insurance organizations. However, for healthcare professionals to make successful decisions, this data must be integrated and made available in real-time. As the market for EHR systems is expected to develop in the future years, hospitals would place a heavy emphasis on enhancing their capabilities by integrating multiple hospital systems with EHR, hence offering growth prospects for the healthcare IT integration industry.

Heterogeneity of health information systems a growth driver for Healthcare IT Integration Market

The heterogeneity of health information systems poses substantial constraints to the effective installation and use of healthcare IT solutions. Many nations lack specified information technology standards for data storage and sharing, resulting in interoperability concerns. Although different data storage, transit, and safety standards are in existence, healthcare providers and healthcare IT solution suppliers face significant challenges in implementing and integrating these interoperability standards. Because no one health information system addresses all of the administrative, clinical, technological, and laboratory needs of big healthcare providers, interoperability and interoperability standards are becoming essential.

Vendors also use diverse data formats and standards as a result of a lack of information or technical know-how about set standards, making it harder to communicate real-time data with partner systems and raising the cost of healthcare IT integration. Issues with data quality and integrity, a lack of conformity with specified standards, a paucity of experienced experts, and operating time disparities across entities delivering healthcare services are key impediments to developing fully interoperable healthcare IT infrastructure.

Rapid adoption of telehealth services for monitoring and consultation purposes

Telehealth services are in high demand for monitoring and consultation. Advances in healthcare systems have enabled the delivery of instructional information while also ensuring the continuous connection between patients and healthcare practitioners. The effective operation of remote patient monitoring systems is dependent on the successful integration of medical equipment and ICT, which allows healthcare services to be delivered over great distances. Because physicians and nurses spend a lot of their work time away from computers in hospitals, carrying patient records on the go is challenging.

As a result, multiple industry competitors began to offer mobile platforms, such as mobile applications, for healthcare IT solutions. Research done by HIMSS and Siemens Healthineers in Europe in July 2020 indicated that 93% of health institutions have deployed at least one sort of telehealth service or solution immediately before the COVID-19 outbreak.

IT advancements have resulted in an ever-expanding range of possibilities, including improved broadband networks, mobile devices and networks, remote patient monitoring, high-definition video conferencing, and EHRs. This has offered several possibilities for healthcare IT integration solution providers. Patients sitting at home can be remotely monitored for vital signs such as blood pressure, weight, glucose levels, ECG, and body temperature via an IoT healthcare network comprised of linked medical equipment, while patient data is automatically relayed to a nurse or a physician.

An integrated health environment enables clinicians to remotely monitor and manage a patient's condition. Smart sensing technologies, high-end connections, interface upgrades, and data analytics are all part of connected health technology. These developments assist to minimise healthcare expenses by increasing patient acceptability and reducing the number of clinical visits. Additionally, while implementation costs may be significant, such technologies assist many businesses to speed up their processes. These solutions are playing a significant role in enhancing remote monitoring and patient compliance, and hence their quality of life, as technology advances. As a result, the increased demand for remote monitoring systems and telehealth devices is expected to provide lucrative opportunities for healthcare IT integration solution providers.

Data integration security breaches

Patient data is collected in all departments and at all points of treatment within the healthcare organization, making the sector very information-intensive. However, obtaining reliable information by integrating massive amounts of data is critical in building comprehensive and accurate patient records. Because diverse medical devices and diagnostic tools are utilized inside healthcare systems, there is an increasing need to integrate all of these systems to help healthcare workers in providing rapid responses at various care delivery points.

Imaging techniques, email monitoring systems, database management systems, forms management systems, clinical information systems, workforce management systems, asset management systems, content management systems, revenue cycle management systems, clinical and non-clinical workflow systems, and customer relations management systems are just a few of the information management applications that many healthcare organizations have invested in. As more healthcare companies adopt various healthcare IT systems, there is a rising need to integrate diverse types of IT systems into the organization's IT architecture to enable maximum usage of these systems and help in precise decision-making. Healthcare IT system integration with other systems is a focus of IT infrastructure development initiatives in healthcare companies.

Healthcare IT Integration Market Segment Analysis:

By Product, the Interface/Integration Engines segment held the largest Healthcare IT Integration market share in the Healthcare IT Integration market in 2025 and is expected to grow at a CAGR of 11.9% during the forecast period. The rising use of electronic health records and healthcare IT solutions are the primary drivers driving the growth of the interface engines industry. Additionally, the demand for telehealth services and remote patient monitoring solutions is expected to drive interface engine market development during the forecast period.

An interface engine, often known as an integration engine, is a software program that processes data across different healthcare information technology systems. These integration engines assist IT organizations in tying different systems together, allowing physicians and other authorized users to access data stored in several EHRs or other applications. An interface engine's job is to facilitate workflow by allowing for changes in direction and sending alarms when any abnormal circumstance occurs.

In addition, this is a computer program that facilitates the transformation of syntactic and semantic structures in communication content during transmission from a sending system to a receiving system(s), enabling reliable communication delivery while avoiding information loss and semantic shift. Due to this, the demand from end-users is increasing rapidly.

An interface/ integration engine is middleware explicitly built to connect systems. The engine removes the requirement for separate system connections, orchestrates message flows, converts message formats as needed, and ensures message delivery. Integration engines go beyond interface engines to ease system interoperability by offering workflow (rather than just message) orchestration.

While interface and integration engines are not the same things, they are extremely similar and can be difficult to tell apart. The main distinction is in the breadth of functionality and capabilities that each supports. They provide varying levels of support for an organization's HL7 maturity, ranging from zero interoperability and integration (for example, isolated hospital information systems) to complete interoperability.

Streamlined healthcare processes and interface engines are critical components of product support and delivery. Cloverleaf, Corepoint, Rhapsody, Datagate, and IGUANA are some of the top interface engines discovered. The existence of rivals and the introduction of new products are driving market expansion. For example, as part of the country's health technology transformation, the Indonesian government deploy a healthcare data integration platform in Jakarta in August 2025. In addition, in 2025, Qvera released a new user interface for QIE version 5.0. It was used in cloud-based healthcare systems.

Government initiatives and healthcare IT research and development are also driving segment and eventually market growth. According to the National Public Health Observatory (NHPO) report dated May 2025, the Union Health Ministry is constructing a site that could act as an observatory for all public health program-related data in India. NHPO expects to develop an integrated command control center using the platform to monitor the policy implication framework across all states for public health initiatives in India. With the increasing importance of the interface engine, this segment is expected to increase rapidly during the forecast period.

Healthcare IT Integration Market Regional Insights:

North America dominated the Healthcare IT Integration Market with the largest share in 2025 and is expected to maintain its dominance through forecast period. The dominance is attributed to the well-established healthcare industry and better reimbursement facilities in the region. In addition, Factors such as the increasing application of clinical device connectivity and interoperability solutions to reduce rising healthcare costs, and stringent regulations and guidelines imposed by various government and non-government authorities such as the Federal Communications Commission (FCC) and the Centres for Medicare and Medicaid Services (CMS) are driving the growth of the healthcare IT integration market.

The United States dominates most of the market in the North American region, due to the increasing acceptance of digital healthcare in the country and the rising investments done by the major corporations. For example, the Federal Electronic Health Record Modernization (FEHRM) program office announced the Department of Veterans Affairs (VA), Department of Defense (DOD), and Department of Homeland Security's United States Coast Guard (USCG) expanded their joint health information exchange (HIE) network in the 2020 update.

The joint HIE is a modernized health data sharing capability that improves VA, DOD, and USCG's capacity to transmit data bidirectionally electronic health records (EHR) with collaborating community healthcare providers swiftly and securely. Additionally, organizational advancements and new product launches are strengthening the region's market. For example, Epic Systems, located in Wisconsin, said in May 2025 that it is striving to make COVID-19 antiviral medications simpler for patients and doctors to discover through its EHR, in response to the Biden administration's push to extend COVID-19 treatment availability.

GE Healthcare also announced its intention to launch the Edison Digital Health Platform, a vendor-agnostic hosting and data aggregation platform with an integrated artificial intelligence (AI) engine, during the 2025 Digital Health 9th Annual Innovation Conference & Expo. The platform is being developed to enable hospitals and healthcare systems to quickly integrate clinical, workflow, analytics, and artificial intelligence (AI) capabilities which might assist in the enhancement of care delivery and the promotion of high-efficiency operations.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 11 March 2026 | Avalue Technology | Launched the EAX-R680BP ATX industrial motherboard specifically designed to support AI and edge computing in healthcare integration environments. | Enhances real-time data processing at the point of care, reducing latency for critical medical device integration. |

| 04 February 2026 | Epic Systems | Rolled out AI Charting, an ambient listening tool that drafts clinician notes and suggested orders in real time during patient encounters. | Significantly reduces documentation burden, allowing for seamless integration of clinical data into the EHR without manual entry. |

| 01 January 2026 | Oracle Health | Released a 2026 roadmap highlighting the delivery of open integration standards (FHIR and SMART) for ECG viewers in partnership with Baxter. | Promotes vendor-neutral interoperability between diagnostic hardware and cloud-based clinical platforms. |

| 11 December 2025 | InterSystems | Announced the Health Gateway solution, enabling a single-interface connection to multiple national Health Information Networks (HINs). | Decreases administrative complexity and cost by eliminating the need for separate contracts and technical integrations for each network. |

| 01 June 2025 | Cognizant | Signed a multi-year strategic agreement with a major U.S. healthcare provider to lead AI-driven digital transformation and system integration. | Accelerates the shift toward modernized IT infrastructures that support advanced population health analytics. |

| 08 May 2025 | InterSystems | Deployed new integration accelerators that reduced connection time for clinical data feeds by 60% across its partner health systems. | Improves the speed-to-value for healthcare organizations implementing longitudinal health records. |

Healthcare IT Integration Market Scope: Inquire before buying

| Healthcare It Integration Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 6.56 USD Billion |

| Forecast Period 2026-2032 CAGR: | 12.5% | Market Size in 2032: | 14.97 USD Billion |

| Segments Covered: | by Product | Interface/Integration Engines Medical Device Integration Software Media Integration Software Other Integration Tools |

|

| by Services | Implementation & Integration Services Support & Maintenance Services Consulting Services |

||

| by Deployment | On-Premises Cloud-Based Hybrid |

||

| by End-User | Hospitals Laboratories Clinics Diagnostic Imaging Centers Ambulatory Surgical Centers Others |

||

Healthcare IT Integration Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Healthcare IT Integration Market Report in Strategic Perspective:

- Infor Inc.

- InterSystems Corporation

- Cerner Corporation (Oracle Health)

- Orion Health Group Limited

- NXGN Management LLC (NextGen Healthcare)

- iNTERFACEWARE Inc.

- Allscripts Healthcare LLC (Veradigm)

- Epic Systems Corporation

- Corepoint Health (Rhapsody)

- Oracle Corporation

- GE HealthCare

- IBM Corporation

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Accenture plc

- Cognizant

- UST

- Zymr, Inc.

- Lyniate

- Health Catalyst

- Change Healthcare

- Quality Systems, Inc.

- CSI Companies

- Medical Information Technology, Inc. (MEDITECH)

- MuleSoft (Salesforce)