Global Healthcare Assistive Robot Market Size by Segment Analysis and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

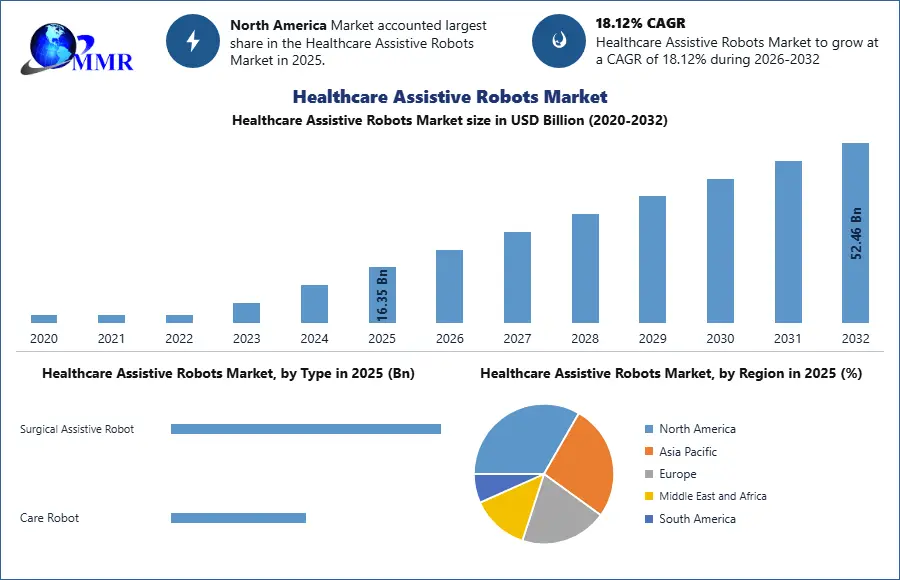

Healthcare Assistive Robot Market size is expected to reach US$ 52.46 Bn. by 2032, at a CAGR of 18.12% during the forecast period.

Healthcare Assistive Robot Market Overview

Healthcare assistive robots are designed to support patients, caregivers, surgeons, and rehabilitation professionals in improving treatment efficiency, patient mobility, and long-term care management. These robotic systems are widely utilized in hospitals, rehabilitation centers, elderly care facilities, and home healthcare environments for surgical assistance, rehabilitation therapies, mobility support, patient monitoring, and social interaction. The growing prevalence of neurological disorders, orthopedic injuries, chronic diseases, and age-related disabilities is accelerating the need for robotic healthcare solutions globally. Advancements in artificial intelligence, machine learning, sensor technologies, and cloud-connected healthcare platforms are significantly improving robotic precision, adaptive learning, and patient engagement capabilities. Governments and healthcare organizations are increasingly investing in smart healthcare infrastructure and digital medical technologies to improve healthcare accessibility and reduce operational burdens on medical professionals. Additionally, rising healthcare workforce shortages and increasing demand for remote patient monitoring are driving hospitals and care facilities toward robotic automation.

To know about the Research Methodology:-Request Free Sample Report

Healthcare Assistive Robot Market Dynamics

Trend

The growing integration of artificial intelligence and socially interactive robotics into patient care and rehabilitation systems. Healthcare providers are increasingly deploying AI-enabled assistive robots capable of speech recognition, emotion detection, real-time patient monitoring, and adaptive learning functions to improve patient engagement and therapy outcomes. Socially assistive robots are gaining significant traction in elderly care, mental health support, and long-term rehabilitation environments where companionship and emotional interaction are becoming important healthcare priorities. Another emerging trend is the expansion of home healthcare robotics driven by rising demand for remote care solutions and telehealth services. Rehabilitation robots and robotic exoskeletons are increasingly being integrated with IoT-enabled platforms and cloud-based monitoring systems to support personalized therapy programs and real-time healthcare management. Humanoid robots are also being adopted in hospitals for patient communication, medicine delivery, and infection-control support.

Driver

The primary driver accelerating the Healthcare Assistive Robot Market is the rapidly increasing elderly population combined with the growing prevalence of chronic diseases, neurological disorders, and mobility-related disabilities. Healthcare systems worldwide are facing mounting pressure to provide long-term patient care, rehabilitation therapies, and elderly assistance while managing healthcare workforce shortages. Assistive robots help improve patient independence, therapy consistency, and healthcare efficiency while reducing the workload on caregivers and medical staff. Rehabilitation robots are increasingly used for stroke recovery, spinal cord injury rehabilitation, orthopedic therapy, and mobility assistance, enabling faster and more precise recovery outcomes. Surgical assistive robots are also witnessing growing demand due to their ability to improve surgical accuracy, minimize invasive procedures, and reduce post-operative recovery time. Governments across major economies are investing heavily in healthcare digitization, AI-based medical technologies, and smart hospital development to improve patient care quality and healthcare accessibility.

Restraint

Assistive robots integrated with artificial intelligence, machine learning, advanced sensors, and real-time monitoring technologies require substantial capital expenditure for deployment, software integration, infrastructure modification, and technical maintenance. Many small hospitals, rehabilitation centers, and healthcare providers in developing economies face financial limitations that restrict large-scale adoption of robotic healthcare technologies. Additionally, integrating robotic systems into existing healthcare workflows and IT infrastructure can be operationally complex and time-consuming.

Regulatory approval procedures for medical robotic systems are also stringent due to patient safety, cybersecurity, and healthcare compliance requirements, often delaying commercialization and market entry. Another major challenge is the shortage of trained robotics specialists and healthcare professionals capable of operating and maintaining sophisticated robotic systems effectively. Ethical concerns regarding patient privacy, reduced human interaction, emotional dependency on robots, and cybersecurity vulnerabilities further create hesitation among healthcare providers and patients.

Healthcare Assistive Robot Market Segment Analysis

By Type , The Surgical Assistive Robot segment dominated the Healthcare Assistive Robot Market in 2025 due to the increasing demand for minimally invasive surgical procedures and precision-based robotic-assisted operations across healthcare institutions. Surgical assistive robots provide enhanced accuracy, flexibility, visualization, and control compared to conventional surgical methods, significantly improving patient outcomes and reducing recovery periods. These robotic systems are widely used in orthopedic, neurology, gynecology, urology, cardiovascular, and laparoscopic surgeries where precision and minimal tissue damage are critical.

Hospitals are increasingly investing in robotic-assisted surgical platforms to improve operational efficiency, reduce surgical complications, and enhance procedural consistency. Technological advancements in robotic navigation systems, AI-enabled surgical planning, and real-time imaging integration are further improving surgical performance and adoption rates. The growing prevalence of chronic diseases, cancer cases, and age-related health conditions requiring surgical intervention is accelerating segment growth globally. In addition, increasing healthcare investments in advanced surgical infrastructure and digital operating rooms are strengthening market demand.

By Product , The Rehabilitation segment dominates the Healthcare Assistive Robot Market due to the increasing prevalence of stroke, spinal cord injuries, neurological disorders, and orthopedic conditions requiring long-term physical therapy and mobility restoration. Rehabilitation robots are extensively used in hospitals, rehabilitation centers, and home healthcare environments to improve motor function recovery, muscle coordination, mobility assistance, and therapy efficiency. These robotic systems provide repetitive, accurate, and programmable rehabilitation exercises that enhance patient recovery outcomes while reducing dependency on manual therapy.

The segment is witnessing strong adoption of robotic exoskeletons, gait training systems, upper-limb rehabilitation robots, and AI-driven physical therapy platforms. Rising geriatric populations and increasing incidence of age-related mobility disorders are further supporting demand for rehabilitation robotics globally. Integration of artificial intelligence, motion sensors, and real-time monitoring technologies is enabling personalized therapy programs and adaptive rehabilitation solutions. Healthcare providers are increasingly deploying robotic rehabilitation systems to address therapist shortages and improve rehabilitation consistency in high-patient-volume healthcare facilities.

Healthcare Assistive Robot Market Regional Analysis

Asia Pacific dominated the Healthcare Assistive Robot Market in 2025 due to rapid healthcare modernization, rising elderly populations, and strong government support for robotics and smart healthcare technologies. Countries such as Japan, China, South Korea, and India are significantly investing in healthcare automation, rehabilitation robotics, and AI-enabled patient care systems to improve healthcare efficiency and address increasing healthcare demands. Japan remains one of the largest adopters of healthcare assistive robots because of its rapidly aging population and severe caregiver shortages, which are accelerating demand for rehabilitation robots, humanoid healthcare assistants, and elderly care automation systems.

China is rapidly expanding healthcare robotics manufacturing and smart hospital infrastructure through large-scale investments in digital healthcare transformation and artificial intelligence technologies. Rising healthcare expenditure, improving medical infrastructure, and increasing awareness regarding robotic-assisted rehabilitation are further strengthening regional market growth. Asia Pacific is also witnessing growing demand for home healthcare robots and socially assistive robots for remote patient monitoring and elderly companionship applications.

Recent Developments

March 2024, Intuitive Surgical launched the next-generation da Vinci 5 robotic surgical platform with enhanced computing power, improved imaging, and force feedback technology for minimally invasive procedures. The development focused on improving surgical precision, surgeon control, and patient recovery outcomes. The system also supports advanced workflow automation and better integration with digital operating rooms. Increasing adoption of robotic-assisted surgery in hospitals and specialty surgical centers is expected to strengthen the company’s healthcare robotics position globally. The launch reflects growing demand for AI-enabled surgical robotics and smart healthcare technologies designed to improve operational efficiency and clinical performance across complex surgical applications.

November 2024, Medtronic expanded its robotic-assisted surgery business by strengthening the capabilities of its Hugo robotic surgery platform through advanced surgical instrument technology integration. The company focused on improving minimally invasive surgical procedures, robotic precision, and operational flexibility across hospitals and healthcare facilities. The development supports growing demand for digital surgery systems and AI-enabled healthcare automation. Medtronic also increased investments in robotic-assisted healthcare infrastructure and advanced visualization technologies to improve patient outcomes and reduce surgical complications. The company continues focusing on expanding robotic surgery adoption in orthopedic, laparoscopic, and general surgery applications across global healthcare markets.

Scope of Global Healthcare Assistive Robot Market: Inquire before buying

| Healthcare Assistive Robots Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 16.35 USD Billion |

| Forecast Period 2026-2032 CAGR: | 18.12% | Market Size in 2032: | 52.46 USD Billion |

| Segments Covered: | by Type | Surgical Assistive Robot Care Robot |

|

| by Product | Surveillance & Security Humanoid Rehabilitation Socially Assistive Others |

||

| by Technology | Simultaneous Localization Mapping Real-Time Locating System Others |

||

| by Portability | Fixed base Mobile |

||

| by Application | Stroke Orthopedics Cognitive & Motor Skills Sports Others |

||

Healthcare Assistive Robot Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key players/Competitors profiles covered in the Healthcare Assistive Robot Market report in strategic perspective

- Intuitive Surgical, Inc. (USA)

- Stryker Corporation (USA)

- Medtronic plc (Ireland)

- Cyberdyne Inc. (Japan)

- Ekso Bionics Holdings, Inc. (USA)

- ReWalk Robotics Ltd. (Israel/USA)

- Hocoma AG (Switzerland)

- Zimmer Biomet Holdings, Inc. (USA)

- ABB Ltd. (Switzerland)

- KUKA AG (Germany)

- Toyota Motor Corporation (Japan)

- Honda Motor Co., Ltd. (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- Omnicell, Inc. (USA)

- Kinova Robotics (Canada)

- Bionik Laboratories Corp. (Canada)

- Ottobock SE & Co. KGaA (Germany)

- DIH Medical Group (China/Global)

- Diligent Robotics (USA)

- CMR Surgical (UK)

- Hyundai Robotics (South Korea)

- Toshiba Corporation (Japan)

- Barrett Technology LLC (USA)

- Adept Technology, Inc. (USA)

- PARO Robots (Japan)