Warehouse Robotics Market Size by Product, Function, Payload Capacity, Industry, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

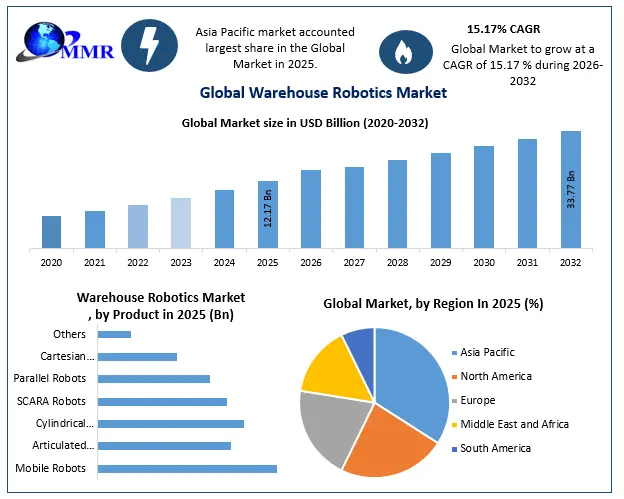

The Warehouse Robotics Market size was valued at USD 12.17 Billion in 2025 and the total Warehouse Robotics revenue is expected to grow at a CAGR of 15.7% from 2026 to 2032, reaching nearly USD 33.77 Billion.

Warehouse Robotics Market Overview

Warehouse robotics revolutionizes logistics by using automated systems to perform tasks such as order picking, packing, palletizing, material handling, inventory management, sorting, quality control, and unloading. Key types include Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs), Automated Storage and Retrieval Systems (AS/RS), palletizer robots, robotic arms, drones, and collaborative robots (cobots). These robots enhance efficiency, accuracy, safety, and space utilization while reducing labor costs. The growing e-commerce market, demand for faster order fulfillment, and labor shortages drive the adoption of warehouse robotics. Before investing, businesses should consider warehouse layout, operational requirements, cost-benefit analysis, scalability, vendor reputation, workforce training, and system integration to ensure a seamless implementation. The deployment of robotics in the warehouse to perform functions such as pick-place, packaging, transportation, packaging, and palletizing. The integration of warehouse and robotics technology has increased warehouse storage space and operational efficiency while ensuring accuracy and automation. The global warehouse robotics market is largely driven by increased demand for automation as a result of increased e-commerce competition, an increase in the number of stock-keeping units, and technological advancements.

To know about the Research Methodology :- Request Free Sample Report

Warehouse Robotics Market Dynamics

Rising E-Commerce Demand and Omnichannel Retailing to Drive the Market Growth

Robotic automation is revolutionizing e-commerce by streamlining operations, improving efficiency, and enhancing customer experiences. In warehouses, robots handle tasks like picking, packing, sorting, and inventory management using advanced sensors and AI. They ensure accurate stock levels and quality control. Autonomous delivery robots reduce delivery times and costs, handling last-mile deliveries and returns efficiently. Robots offer speed, accuracy, strength, and flexibility, augmenting human capabilities and creating more efficient processes. The surge in e-commerce and the shift towards omnichannel retailing are significant drivers of growth in the warehouse robotics market. With consumers increasingly shopping online, businesses are pressured to enhance their supply chain efficiency, speed, and accuracy to meet rising expectations. Warehouse robotics, including automated guided vehicles (AGVs) and robotic picking systems, offer a solution by streamlining operations, reducing errors, and accelerating order fulfillment processes. As retailers aim to provide seamless customer experiences across multiple sales channels, the integration of robotics becomes crucial in managing inventory, processing returns, and optimizing warehouse space. This trend is expected to propel the demand for advanced robotic solutions, driving substantial growth in the warehouse robotics sector.

Automation offers a range of benefits for warehouses, from increasing productivity to reducing risk related to labor. U.S. e-commerce represented 22.0% of total retail sales, as per U.S. Department of Commerce data. Industrial Procurement Services excels as an expert in automation and robotics, driving the Warehouse Robotics Market forward with innovative solutions. Specializing in warehouse automation and integration, we optimize operations through cutting-edge robotic technologies. Their services encompass the entire spectrum from receiving and sorting to picking, packing, and shipping, enhancing efficiency and accuracy across e-commerce and fulfillment sectors. They leverage advanced robotics such as Autonomous Mobile Robots (AMRs) for dynamic tasks like goods-to-person picking, significantly boosting productivity. With a focus on scalability and flexibility, our solutions adapt to evolving business needs, ensuring sustainable growth and operational excellence.

Advances in AI and Machine Learning Technologies to Boost the Market Growth

Advancements in artificial intelligence (AI) and machine learning (ML) technologies are revolutionizing warehouse robotics, making them more intelligent, adaptable, and efficient. These technologies enable robots to learn from their environments, optimize their tasks, and collaborate with human workers more effectively. Enhanced AI capabilities allow robots to perform complex tasks such as object recognition, path planning, and decision-making with greater precision and speed. This results in improved productivity, reduced operational costs, and enhanced flexibility in warehouse operations. As AI and ML continue to evolve, their integration into warehouse robotics will drive significant growth, enabling businesses to achieve higher levels of automation and efficiency in their supply chain management.

The warehousing industry is expected to see a significant increase in the use of robotic systems to reduce operational time and costs while increasing warehouse throughput. The market is expected to grow significantly due to the rising demand for automation and increased awareness of the importance of safety and high-quality production. Warehouse robotics is widely regarded as one of the most effective methodologies for reducing pressures associated with labor costs and availability and improving operational competencies. The robots lift heavy loads and efficiently complete tasks in the facility such as picking, placing, transportation, packaging, and palletizing. The proliferation of the Internet of Things (IoT), Artificial Intelligence (AI), machine learning, and other similar technologies, which have already made an impact in the warehousing industry, is expected to fuel Warehouse Robotics Market growth.

Expansion into Small and Medium Enterprises (SMEs) to Influence the Market Growth

Companies like Locus Robotics and InVia Robotics are expanding their market presence, particularly in item and case-level automation. Additionally, investments in autonomous forklifts from companies such as Balyo, OTTO Motors, and Seegrid are on the rise, aiming to enhance warehouse efficiency amid evolving economic conditions. In there were approximately 882,770 small and medium-sized enterprises (SMEs) in the construction sector in the United Kingdom, the most of any sector in that year. The sector with the second-highest number of SMEs was the Professional, Scientific and Technical activities sector, with 770,475 SMEs.

The expansion of warehouse robotics into small and medium enterprises (SMEs) presents a unique growth opportunity in the market. Historically, the high costs and complexity of robotic systems have limited their adoption by large enterprises. However, recent developments in cost-effective and scalable robotic solutions are making automation accessible to smaller businesses. SMEs now leverage robotics to enhance their operational efficiency, reduce labor costs, and compete with larger players in the market. This democratization of warehouse robotics technology opens a vast, untapped market segment, offering substantial growth potential. As more SMEs adopt these solutions, the overall demand for warehouse robotics is expected to increase, driving Warehouse Robotics Market growth and innovation.

High Initial Investment to Pose the Challenge for Market Growth

The adoption of warehouse robotics, while promising significant improvements in efficiency and accuracy, is often hindered by the high initial investment required. Implementing advanced robotic systems entails substantial upfront costs, including the purchase of sophisticated robots, installation of specialized infrastructure, and integration with existing warehouse management systems. For many businesses, especially small to mid-sized enterprises, these costs are prohibitive. Additionally, ongoing maintenance and the need for skilled personnel to operate and manage these systems add to the financial burden. This substantial initial outlay deters companies from embracing robotic automation, despite the potential long-term benefits. As a result, the challenge of high initial investment remains a significant restraint in the widespread adoption of warehouse robotics, limiting its accessibility to larger corporations with substantial capital reserves. Another major restraint on the growth of the warehouse robotics market is the complexity involved in integrating these advanced systems with existing warehouse operations. Warehouses often utilize a variety of legacy systems and processes that may not be readily compatible with new robotic technologies. The integration process can be both time-consuming and costly, requiring extensive customization and testing to ensure seamless operation.

Warehouse Robotics Market Segment Analysis

By Product:

In 2025, the mobile robots segment held the largest Warehouse Robotics Market share and it is expected to grow significantly over the forecast period. Mobile robots are an important part of the global warehousing industry because they are used to move small payloads around the facility, particularly in the retail and consumer electronics industries, and they offer more flexibility than most traditional automation systems. Due to their ability to perform warehouse operations such as material handling, picking and placing, and loading and unloading, among others, the Cartesian robots segment is expected to grow significantly over the forecast period. Because of the thoroughness with which they perform tedious tasks, articulated robots, which are used for heavy-duty tasks in the facility, held a significant market share in 2025. This Warehouse Robotics Industry growth is attributed to the fact that they are simple to align with various planes and provide operational and main services.

By Function:

Based on function segment the Transportation segment held the largest Warehouse Robotics Market share in 2025. This growth is driven by the expanding retail and e-commerce industries, along with rising demand for automated robots to enhance efficiency and reduce costs in logistics operations. Also, integrating robots for transport functions helps address labor shortages by automating various tasks. For example, KNAPP AG partnered with eMAG.ro, MALL.CZ, HPTRONICS, and Alza.cz to bolster logistics capabilities, solidifying its position as a leading technology provider for e-commerce logistics in Central and South Eastern Europe. The continuous technological advancements that have made robots more efficient, precise, and adaptable for such tasks. For instance, ABB introduced the SWIFTI CRB1300 industrial collaborative robot in December , tailored for tasks ranging from machine tending and palletizing to pick-and-place and screw driving. Additionally, declining costs have made pick-and-place robots more accessible to smaller businesses and manufacturers, contributing to their increased adoption.

Warehouse Robotics Market Regional Analysis

Asia Pacific dominated the largest Warehouse Robotics Market share in 2025. The Asia Pacific Warehouse Robotics Market is experiencing rapid growth due to expanding e-commerce, rising labor costs, and increasing investments in smart logistics infrastructure across China, Japan, South Korea, and India. China dominates the regional market because of large-scale warehouse automation adoption by companies such as Alibaba, JD.com, and Cainiao, while Japan and South Korea lead in robotics innovation and industrial automation technologies. The demand for Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), robotic picking systems, and automated storage & retrieval systems (ASRS) is increasing significantly in retail, automotive, healthcare, and third-party logistics sectors. Governments across Asia Pacific are also supporting Industry 4.0 and smart manufacturing initiatives, accelerating warehouse digitalization. The growing penetration of AI-enabled robotics, cloud-based warehouse management systems, and same-day delivery models is driving market expansion. Rising investments by key players including Geek+, GreyOrange, Daifuku, and Toyota Industries are further strengthening the competitive landscape.

Recent Developments

On, May 2025, Amazon Robotics introduced “Vulcan,” an AI-powered warehouse robot equipped with advanced touch-sensing capabilities to improve item handling and warehouse automation efficiency. The robot can identify, grasp, and organize products with greater precision, helping automate nearly 75% of warehouse inventory operations. Amazon also accelerated deployment of autonomous robotic systems across fulfillment centers to improve sorting speed, reduce operational costs, and support high-volume e-commerce logistics. The development reflects increasing investment in AI-enabled warehouse robotics, machine vision, and intelligent automation technologies aimed at improving productivity, warehouse safety, and real-time inventory management capabilities globally.

On April 2025, Geek+ expanded its intelligent warehouse automation portfolio by introducing AI-driven robot arm picking stations and advanced autonomous mobile robot solutions for fully unmanned warehouse operations. The company focused on integrating embodied AI technologies, real-time warehouse analytics, and robotic picking systems to improve storage optimization and order fulfillment efficiency. Geek+ also reported strong growth in warehouse robotics deployments across North America and global logistics markets during 2025.

Global Warehouse Robotics Market Report Scope: Inquire before buying

| Warehouse Robotics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 12.17 USD Billion |

| Forecast Period 2026-2032 CAGR: | 15.7% | Market Size in 2032: | 33.77 USD Billion |

| Segments Covered: | by Product | Mobile Robots Articulated Robots Cylindrical Robots SCARA Robots Parallel Robots Cartesian Robots Others |

|

| by Payload Capacity | < 200 Kg 200 to 400 Kg 400 to 600 Kg 600 to 900 Kg > 900 Kg Others |

||

| by Function | Pick & Place Palletizing & De-palletizing Transportation Packaging Others |

||

| by Industry | Automotive E-commerce Semiconductor & Electronics Food and Beverages Healthcare Others |

||

Global Warehouse Robotics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Warehouse Robotics Market report in strategic perspective

- Amazon Robotics

- Geek+

- GreyOrange

- Locus Robotics

- Symbotic

- Swisslog Holding AG

- Dematic Corporation

- Honeywell Intelligrated

- ABB Ltd.

- KUKA AG

- FANUC Corporation

- Yaskawa Electric Corporation

- Daifuku Co., Ltd.

- Ocado Group plc

- Exotec

- Berkshire Grey

- 6 River Systems

- Fetch Robotics

- AutoStore Holdings Ltd.

- Knapp AG

- TGW Logistics Group

- Seegrid Corporation

- IAM Robotics

- inVia Robotics

- Covariant AI

- Boston Dynamics

- Attabotics

- Unbox Robotics

- Brightpick

- Fabric Inc.