Sheet Metal Fabrication Services Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

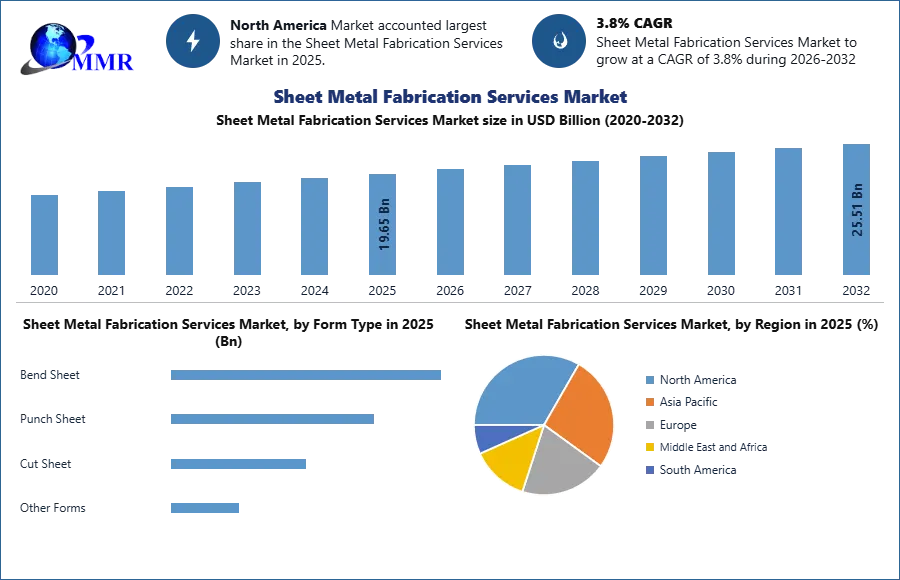

Sheet Metal Fabrication Services Market size was valued at USD 19.65 Billion in 2025 and the total Sheet Metal Fabrication Service revenue is expected to grow at a CAGR of 3.8% from 2026 to 2032, reaching nearly USD 25.51 Billion by 2032.

Sheet metal fabrication is a critical process that serves as the backbone of multiple industries, including construction, automotive, aerospace, electronics, and renewable energy. The sheet metal fabrication services have experienced substantial evolution, driven by technological advancements, automation, and a growing demand for customized components. The global sheet metal fabrication market is expected to witness steady growth, with a compound annual growth rate (CAGR) of approximately 4-6% over the next seven years.

Sheet metal fabrication is the third-largest industry in North America based on employment. The most commonly used materials in fabrication are stainless steel, aluminum, and steel. These metals are favored for their durability, strength, and ease of machining. Sheet metal fabrication plays a role in almost every industry, with products such as air conditioning ducts, shelving, light fixtures, and electronic enclosures all relying on precision fabrication.

The industry has high penetration across key sectors such as automotive, construction, and heavy machinery manufacturing. The ongoing infrastructural developments, rapid urbanization, and increased investment in industrial automation are major factors contributing to the market expansion. The demand for stainless steel fabrication is particularly high in industries that require corrosion-resistant and durable components, including medical, food processing, and marine applications.

Sheet metal fabrication is a critical process that serves as the backbone of multiple industries, including construction, automotive, aerospace, electronics, and renewable energy. The sheet metal fabrication services have experienced substantial evolution, driven by technological advancements, automation, and a growing demand for customized components. The global sheet metal fabrication market is expected to witness steady growth, with a compound annual growth rate (CAGR) of approximately 4-6% over the next seven years.

Sheet metal fabrication is the third-largest industry in North America based on employment. The most commonly used materials in fabrication are stainless steel, aluminum, and steel. These metals are favored for their durability, strength, and ease of machining. Sheet metal fabrication plays a role in almost every industry, with products such as air conditioning ducts, shelving, light fixtures, and electronic enclosures all relying on precision fabrication.

The industry has high penetration across key sectors such as automotive, construction, and heavy machinery manufacturing. The ongoing infrastructural developments, rapid urbanization, and increased investment in industrial automation are major factors contributing to the market expansion. The demand for stainless steel fabrication is particularly high in industries that require corrosion-resistant and durable components, including medical, food processing, and marine applications.

The global Sheet Metal Fabrication Services Market is undergoing a fundamental structural shift as the 2026 Middle East crisis destabilizes high-energy manufacturing. With the Hormuz blockade driving crude to $120/bbl, electricity-intensive laser cutting and welding overheads have surged 30%, while 400% maritime freight surcharges disrupt global steel and aluminum trade. Market leaders are prioritizing near-shored automated facilities and AI-driven logistics to bypass volatile corridors. This strategic transition is essential for maintaining the 6.5% CAGR, ensuring industrial resilience amidst historic energy-driven supply disruptions.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Research Methodology:

The Sheet Metal Fabrication Services market analysis is based on primary and secondary research. Both secondary and primary data are investigated using the Bottom-Up Approach. Nationalized and global data sources, yearly and financial reports from important market participants, press releases, and so on are examples of secondary data sources. To collect primary data, interviews, surveys, expert and trained professional opinions, and other approaches were employed. Current developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, the influence of domestic and major & localized market players, changes in market regulations, and strategic market growth analysis are also included in the research.

To produce the final quantitative and qualitative data, all possible components impacting the markets covered in this report were investigated, thoroughly researched, validated through primary research, and analyzed. Market size is balanced for top-level markets and sub-segments, and the influence of inflation, economic downturns, policy changes, and other variables is considered in market forecasting. The data is supported with comprehensive inputs and analysis throughout the report. Intensive primary research was conducted to acquire information and check and confirm the essential numbers arrived at after extensive market engineering and calculations for market statistics such as market size estimations, estimates, segmentation, and data analysis and interpretation.

Sheet Metal Fabrication Services Market Dynamics:

The rapid adoption of advanced metal fabrication technologies is a key driver for market growth.

The rapid adoption of innovative metal fabrication technologies is a significant driver driving demand and is expected to drive global revenue growth. The use of computer-aided design (CAD) software technologies to shape metal during production is becoming more common. The system software generates 3D models and keeps you up to speed on any modifications to the fabrication design. This is anticipated to increase the usage of metal fabrication and drive the market's revenue growth. Another element driving metal fabrication adoption is the increased need for automated fabrication techniques. Automation has transformed the manufacturing process in recent years, as fabrication technology has become more capable of programming. This technology allows machines to execute projects with minimum human intervention. This is expected to drive the market's revenue growth during the forecast period.

Rising demand for Sheet Metal Fabrication Services due to their numerous applications including low cost and long-term reliability

Rising metal fabrication utilization due to its ability to go through a larger range of processes such as chipping, deep drawing, casting, welding, and soldering is driving revenue growth in the sheet metal fabrication market. The capacity of sheet metal to be squeezed or stretched without breaking or cracking is growing the use of the metal fabrication process, which is expected to drive market revenue growth. The rising demand for metal fabrication to power electrical systems is expected to drive the metal fabrication market's revenue growth.

Metals that have been fabricated, such as copper and steel, are commonly utilized in the development of energy production systems. This is raising the usage of metal fabrication, which is driving the market's revenue growth. Metal manufacturing is anticipated to see increased usage due to its low cost and long-term durability. Rising die casting metal fabrication usage is anticipated to improve metal fabrication adoption in various industrial applications. Die casting reshapes molten metal in a die rather than a mold.

Problems with supplementary finishing processes during metal manufacturing

Metal fabrication frequently and necessarily requires a supplementary finishing procedure to make it more durable and attractive, resulting in a greater cost of installation and finishing, which is expected to restrain the market growth. Coatings must be placed to preserve the metal while also providing a certain aesthetic. This might raise concerns about further finishing operations following metal manufacture, stifling market revenue growth. Nevertheless, metal finishing necessitates the dressing of welds, frequent maintenance, and the removal of sharp edges, all of which might raise the entire installation cost throughout the production process, restricting the market growth.

Key Industry Drivers Influencing the Sheet Metal Fabrication Services Market

| Industry Driver | Description |

| Growing Demand in Construction & Infrastructure | Increasing urbanization and industrialization are driving the demand for sheet metal fabrication in structural applications. |

| Expansion of Automotive & Aerospace Industries | Lightweight, durable, and high-strength metal components are essential for vehicle and aircraft manufacturing. |

| Advancements in Manufacturing Technologies | Adoption of CNC machining, laser cutting, and automated welding improves precision and efficiency. |

| Rise in Custom Fabrication Needs | Demand for custom sheet metal components in medical, electronics, and consumer products is growing. |

| Sustainability & Recyclability of Metals | Stainless steel, aluminum, and copper are 100% recyclable, supporting eco-friendly production trends. |

| Stringent Industry Standards & Compliance | Regulations in aerospace, automotive, and construction sectors are boosting demand for high-quality metal fabrication. |

| Growth in Renewable Energy Sector | Increased fabrication of components for solar panels, wind turbines, and battery storage. |

| Cost Efficiency & Material Optimization | Advanced techniques like metal stamping and laser cutting help reduce waste and manufacturing costs. |

| Increasing Demand for High-Performance Alloys | Industries require corrosion-resistant, lightweight, and durable metals like titanium and aluminum. |

| Expanding E-commerce & Logistics Industry | Demand for fabricated metal storage racks, conveyor belts, and packaging equipment is increasing. Sheet Metal Fabrication Services Market Segment Analysis: |

By Material Type, the Steel segment held the largest market share of about xx% in 2025 and is expected to grow considerably during the forecast period. Steel demand is increasing since it is being used in the metal manufacturing process. It is driving the segment's growth. Rising usage of robust, easy-to-handle transportation materials has resulted in increased demand for steel sheet metal fabrication, which is expected to drive the segment's revenue growth. Other aspects such as continuous recyclable, high strength and durability are expected to increase demand for steel materials and drive the segment's growth. Rapid growth in the steel sector is also expected to drive the segment's revenue growth.

The Aluminum segment is anticipated to rise at a steady rate throughout the forecast period. The rising use of aluminum material in the metal manufacturing process in the automobile sector is also increasing its popularity. Rising acceptance of sustainable metal fabrication and increased recycling rate of aluminum material is driving the demand for aluminum metal fabrication. This is anticipated to rise the segment's revenue growth. Metal fabrication is an important step in the production of mechanicals. It also aids in the assembly of pieces and the connection of metals, hence increasing demand for metal fabrication. This is another aspect that is expected to drive the segment's revenue growth.

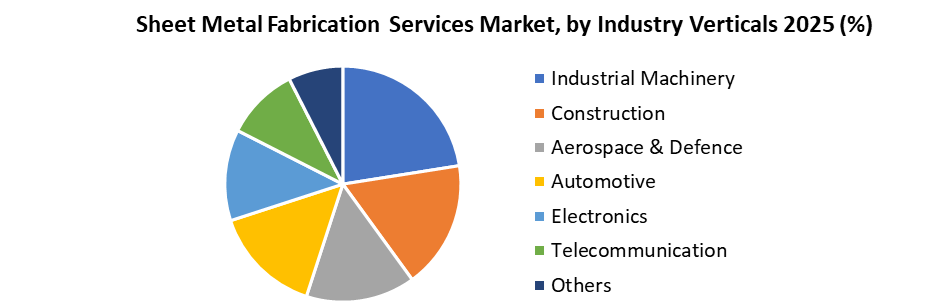

By Industry Verticals, the automotive segment held the largest market share of about xx% for the Sheet Metal Fabrication Services market in 2025 and is expected to maintain its dominance at the end of the forecast period. Because of the constantly shifting designs and material combinations in vehicle manufacture, the automotive sector is one of the greatest demand generators. Technological improvements and simplicity of operation have contributed to the production of long-term demand for sheet materials in a variety of sectors. Mechanical applications manufacturing is another significant industry area with widespread applicability.

Rising demand for sheet metal fabrication in Automotive to give custom-built designs and modern finishes are driving the segment's revenue growth. Metal fabrication is becoming more popular as the need for new and improved car designs grows. It is another aspect that is anticipated to boost the segment's growth. The rising usage of metals in vehicle manufacturing is also anticipated to boost revenue growth in the industry during the forecast period. Rising demand for lightweight and eco-friendly metals for automobile manufacturing are two more variables that are expected to drive the segment's revenue growth.

Sheet metal fabrications are extremely useful in the aerospace and defense industries. Fabricated metal sheets are in high demand in the market. Owing to the industry produces high-value products, the machines utilized in these sectors use cutting-edge technology to maintain high accuracy and quality. The exponential growth in Unmanned Aerial Vehicle (UAV) production in the industrial vertical has had a significant and positive influence on the market and is expected to boost growth further during the forecast period.

Sheet Metal Fabrication Services Market Regional Insights:

The North American market held the largest market share of about xx% for Sheet Metal Fabrication Services in 2025 and is expected to maintain its dominance at the end of the forecast period. Perforated metal advancements are being experienced in the North American metal fabrication sector. Perforation rollers are increasingly being used in the metal fabrication sector to produce even and consistent punches in metal sheets. Equipment makers are boosting their efforts to build project-specific rollers to fulfill clients' individual needs. These developments impact the growth of the North American sheet metal fabrication market.

There is an increasing need for perforation rollers that can punch through metal cold or heated to provide a clean punch every time. Because the heated pin in these rollers forms a strengthened ring around the hole to enhance the strength of the metal, these new rollers are offering incremental opportunities for sheet metal fabricating organizations. Lasers, on the other hand, have received a lot of attention for metal piercing. The rising need for sheet metal fabrication in aerospace and defense is growing its adoption in North America, enhancing the sheet metal fabrication market's revenue growth. Additionally, increased government laws requiring the use of recyclable and sustainable metals would drive revenue growth in the North American sheet metal fabrication sector.

The Asia-Pacific region is expected to grow rapidly during the forecast period for the Sheet Metal Fabrication Services market. The growth is attributed to the rising industrial activities in emerging countries like China, India, Japan, Vietnam, etc. Japan is one of the largest exporters of items from numerous sectors. The Japanese government has been developing strategies with regional corporations to assist private enterprises in developing stronger partnerships and engagement with other nations and companies. Additionally, the Japanese government and businesses are collaborating to strengthen their focus on sustainability as part of their science and technology strategic plan.

Over the forecast period, the European market is expected to grow at a constant CAGR. Rapid growth in the automotive and electronic industries drives demand for sheet metal fabrication, driving revenue growth in the sheet metal fabrication market. The strong presence of aluminum and steel producers in the region is expected to drive market revenue growth. Increased environmental commitments by replacing plastic fabrication with aluminum, steel, and other recyclable metals are anticipated to drive revenue growth in the European sheet metal fabrication industry.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 12 October 2025 | Salasar Techno Engineering | Finalized a Rs 200+ crore supply contract for heavy steel structures intended for renewable energy solar trackers. | Strengthens the renewable energy infrastructure supply chain through localized, large-scale sheet metal fabrication. |

| 15 July 2025 | Mayville Engineering Company (MEC) | Successfully completed the strategic acquisition of Accu-Fab, LLC to expand its precision fabrication footprint. | Expands MEC's market share and technical capabilities in custom metal forming and electronics enclosure fabrication. |

| 10 May 2025 | TRUMPF | Launched a new Smart Factory facility in Farmington, utilizing AI-driven autonomous sheet metal production. | Reduces lead times and enhances production accuracy for industrial machinery components via Industry 4.0 integration. |

| 14 March 2025 | TST Fabrication and Machine | Announced a $3 billion expansion of its Norfolk headquarters for fabricating U.S. Navy sheet metal parts. | Significantly boosts defense-sector fabrication capacity and regional employment in the precision metalworking industry. |

Sheet Metal Fabrication Services Market Scope: Inquire before buying

| Sheet Metal Fabrication Services Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 19.65 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.8% | Market Size in 2032: | 25.51 USD Billion |

| Segments Covered: | by Form Type | Bend Sheet Punch Sheet Cut Sheet Other Forms |

|

| by Material Type | Aluminum Copper Steel Others Tungsten |

||

| by Industry Verticals | Industrial Machinery Construction Aerospace & Defense Automotive Electronics Telecommunication Others |

||

Sheet Metal Fabrication Services Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Global Sheet Metal Fabrication Services Market key players

- Marlin Steel Wire Products LLC

- Mayville Engineering Company, Inc.

- Metcam, Inc.

- Moreng Metal Products, Inc.

- Noble Industries, Inc.

- O'Neal Manufacturing Services

- Ryerson Holding Corporation

- Standard Iron & Wire Works, Inc.

- The Metalworking Group

- All Metals Fabricating, Inc.

- BTD Manufacturing, Inc.

- Classic Sheet Metal, Inc.

- Dynamic Aerospace and Defense Group

- Ironform Corporation

- Kapco Metal Stamping

- Da Ming International Holdings Ltd.

- Otter Tail Corp.

- Amada America, Inc.

- Trumpf Group

- Bystronic Laser AG

- Yamazaki Mazak Corporation

- DMG Mori Co., Ltd.

- Dalsin Industries

- LVD Company NV

- Murata Machinery, Ltd.

Frequently Asked Questions

1.What is the current market size and forecast for the Sheet Metal Fabrication Services Market?

Ans. The market was valued at USD 19.65 billion in 2025. It will reach USD 25.51 billion by 2032, maintaining a 3.8% CAGR during the forecast period.

2. Which region leads the Sheet Metal Fabrication Services Market share analysis?

Ans. North America dominates the market share due to advanced aerospace demands, defense-sector investments, and the integration of specialized perforation rollers and smart factory technology across industries.

3. How is AI and automation influencing Sheet Metal Fabrication Services Trends 2026?

Ans. AI-driven autonomous production and CAD software optimize designs, while automated CNC machining and laser cutting minimize human intervention, significantly boosting operational efficiency and industrial revenue growth.

4. What are the primary industry growth drivers for stainless steel fabrication?

Ans. High demand for corrosion-resistant, durable components in medical, food processing, and marine applications fuels growth, alongside rising infrastructure needs and rapid urbanization across global markets.

5. What role does the automotive sector play in market revenue expansion?

Ans. The automotive segment leads demand through custom-built designs, lightweight aluminum integration, and eco-friendly material requirements, securing its position as a dominant vertical for precision fabrication.

6. How do sustainability trends impact the sheet metal fabrication service industry?

Ans. Increasing environmental commitments drive the replacement of plastic with 100% recyclable aluminum and steel, supported by government regulations promoting sustainable manufacturing and circular economy practices.

7. What are the major challenges restraining sheet metal fabrication market growth?

Ans. High installation costs associated with supplementary finishing processes, such as weld dressing and protective coatings, act as market restraints by increasing total production expenses significantly.