Vehicle-To-Grid Technology Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

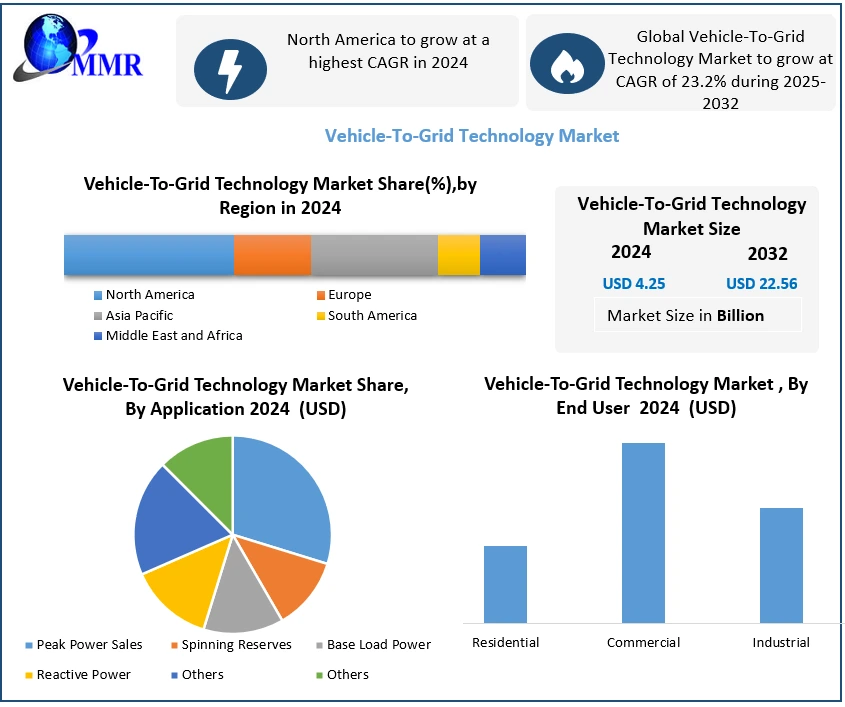

Vehicle-To-Grid Technology Market was valued at USD 4.25 Bn. in 2024 and the total Global Vehicle-To-Grid Technology Market revenue is Expected to grow at a CAGR of 23.2% from 2025 to 2032 reaching nearly USD 22.56 Bn. by 2032.

Vehicle-to-grid (V2G) technology enables electric vehicles (EVs) to interact with the power grid, allowing them to both draw electricity from the grid to charge their batteries and to discharge electricity back to the grid, providing grid services such as demand response, peak shaving, and energy storage. The Vehicle-To-Grid Technology Market is expected rapid growth driven by the concept of Grid to Vehicle (G2V), which facilitates smart charging schedules to control EV battery charging rates based on grid demand. G2V enables unidirectional power flow between the grid and EVs, optimizing power grid operations by providing auxiliary services such as spinning reserve and power grid control.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

The implementation of G2V requires energy trading policies between EV owners and power utilities to incentivize off-peak charging, reducing peak-hour loads and maximizing system profits. However, V2G services, including peak load shaving and voltage control, are crucial for grid stability but are currently limited. Vehicle-To-Grid Technology Market developments include notable mergers and acquisitions, such as Hitachi's acquisition of a majority stake in ABB Power Grids, and partnerships such as The Lion Electric Co. and Nuvve Corporation's collaboration on V2G technology. Additionally, new launches like Boulder Electric Vehicle's testing of vehicle-to-grid technology demonstrate the growing momentum in this sector, indicating a promising future for V2G technology as a key player in enhancing grid flexibility and sustainability.

Vehicle-To-Grid Technology Market Dynamics:

Increasing EV Adoption Rates Globally are Expanding the Pool of Vehicles Available for Vehicle-To-Grid (V2G) Programs, Enhancing Grid Stability

The increasing adoption of electric vehicles (EVs) globally, particularly in countries like Norway and China, is expanding the pool of vehicles available to participate in V2G programs, thereby enhancing grid stability. Government initiatives and incentives, such as subsidies for EV purchases and tax credits, further stimulate demand for V2G solutions, while advancements in smart grid infrastructure facilitate seamless integration of V2G systems into existing grid networks. Moreover, the growing focus on grid resilience, driven by concerns over extreme weather events and grid disruptions, is prompting utilities to invest in V2G technology as a means to improve grid reliability during emergencies.

Environmental sustainability goals and ambitious renewable energy targets are driving the adoption of V2G technology worldwide, with countries like Germany leveraging V2G solutions to support renewable energy integration and reduce reliance on fossil fuels. Ongoing technological innovations in battery storage, vehicle-to-grid communication protocols, and software algorithms are also enhancing the efficiency and performance of V2G systems, while partnerships and collaborations between automotive manufacturers, energy companies, and technology providers are fostering innovation and Vehicle-To-Grid Technology Market growth. Furthermore, emerging markets with growing EV adoption rates, such as India and Brazil, present significant opportunities for V2G technology providers to capitalize on, further driving industry growth and Vehicle-To-Grid Technology Market growth.

Inadequate charging infrastructure and grid connectivity hinder access to V2G services, particularly in regions with insufficient infrastructure

The Vehicle-To-Grid Technology Market faces several restraints and challenges that impede its widespread adoption and growth. Infrastructure limitations, such as inadequate charging infrastructure and grid connectivity, hinder access to V2G services for EV owners in regions with insufficient infrastructure. Moreover, concerns about battery degradation due to frequent cycling in V2G applications raise questions about long-term battery health, as demonstrated by Nissan's V2G pilot project in Denmark. Regulatory hurdles and lack of standardized protocols further complicate V2G integration, creating uncertainties for stakeholders and slowing Vehicle-To-Grid Technology Market development. Additionally, limited consumer awareness and education about V2G technology, coupled with security and privacy concerns surrounding data exchange between EVs and the grid, pose significant barriers to market acceptance and adoption.

Interoperability challenges stemming from the absence of standardized communication protocols between V2G systems and various EV models hinder system integration and scalability. Economic viability remains a concern due to high upfront costs of V2G infrastructure installation and uncertainties surrounding revenue streams and return on investment (ROI) for V2G projects. Grid stability and reliability issues arise from integrating large numbers of EVs into the grid for V2G services, potentially exacerbating grid congestion and voltage fluctuations without proper grid management. Limited scalability, technological complexity, and the need for sophisticated technical expertise further exacerbate implementation challenges, delaying deployment and increasing project costs.

Vehicle-To-Grid Technology Market Segment Analysis:

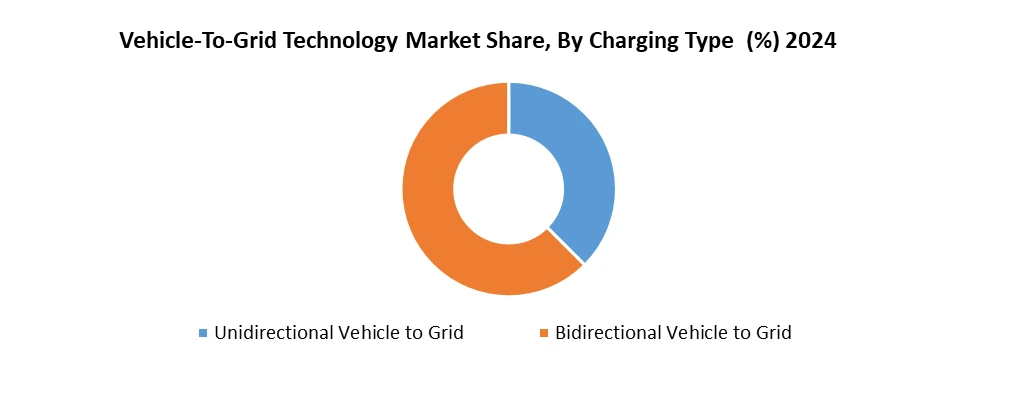

Based on Type, Unidirectional V2G systems primarily enable electric vehicles (EVs) to discharge electricity back to the grid, providing grid services such as demand response and peak shaving. These systems are widely adopted in applications where grid stabilization and ancillary services are paramount, such as in regions with high renewable energy penetration. On the other hand, bidirectional V2G systems allow for both charging and discharging of EV batteries, offering greater flexibility and potential revenue streams for EV owners through participation in energy markets and grid services. Bidirectional V2G technology is gaining traction in markets where grid integration and energy trading are prioritized, fostering innovation and Vehicle-To-Grid Technology Market growth.

Based on Application the Market is segmented into Peak Power Sales, Spinning Reserves, Base Load Power, Reactive Power and Others. Peak to Power Sales segment dominated the market in 2024 and is expected to hold largest share during the forecast period. Dominance due to increasing need to manage high energy demand during peak load periods. V2G systems allow electric vehicles to discharge stored energy back into the grid, helping utilities meet short-term surges without investing in additional infrastructure. This not only stabilizes the grid but also creates a revenue stream for EV owners and fleet operators, making it a financially viable and scalable application for early V2G adoption.]

Vehicle-To-Grid Technology Market Regional Insights:

North America Dominated the Vehicle-To-Grid Technology Market

The Vehicle-To-Grid Technology Market exhibits diverse regional dynamics, driven by varying regulatory landscapes, infrastructure development, and market maturity. In North America, particularly in the United States, robust government support and favorable policies, such as tax incentives for electric vehicle (EV) adoption and grid modernization initiatives, stimulate Vehicle-To-Grid Technology Market growth. Strategic collaborations between automotive manufacturers, utilities, and technology providers propel innovation and deployment of V2G solutions. In Europe, stringent emissions regulations and ambitious renewable energy targets drive demand for V2G technology, with countries like Germany and the UK leading in V2G adoption and deployment. The European Union's clean energy initiatives and funding programs further accelerate V2G market development. In the Asia-Pacific region, rapid urbanization, increasing EV adoption, and investments in smart grid infrastructure fuel V2G market growth. Countries like China and Japan are at the forefront of V2G innovation, leveraging government incentives and industry partnerships to advance V2G deployment. Emerging markets in Southeast Asia, such as Singapore and Thailand, present untapped opportunities for V2G technology adoption, driven by growing awareness of energy sustainability and grid resilience.

Vehicle-To-Grid Technology Market Competitive Landscape:

The Vehicle-To-Grid Technology Market is characterized by strategic partnerships, collaborations, and product innovations driving competitive dynamics. Notably, in November 2020, The Lion Electric Co. partnered with Nuvve Corporation to integrate V2G technology into Lion's zero-emission school buses, allowing dynamic energy storage and discharge. This collaboration underscores the trend towards incorporating V2G capabilities as a standard feature in electric vehicle offerings. Furthermore, Boulder Electric Vehicle's launch of its V2G technology in December 2020 signifies a significant product expansion, with the company testing bidirectional electric vehicle charging systems to reduce energy loads and utility expenses. Additionally, mergers and acquisitions contribute to Vehicle-To-Grid Technology Market consolidation, as demonstrated by Hitachi's acquisition of a majority stake in ABB Power Grids in July 2020. These key developments underscore the industry's focus on technological innovation, strategic partnerships, and Vehicle-To-Grid Technology Market growth to capitalize on the growing demand for V2G solutions globally.

Vehicle-To-Grid Technology Market Scope:Inquire before buying

| Global Vehicle-To-Grid Technology Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 4.25 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 23.2% | Market Size in 2032: | USD 22.56 Bn. |

| Segments Covered: | by Charging Type | Unidirectional Vehicle to Grid Bidirectional Vehicle to Grid |

|

| by Vehicle Type | Battery Electric Vehicles (BEVs) Plug-in Hybrid Electric Vehicles (PHEVs) Fuel Cell Electric Vehicles (FCEVs) |

||

| by Component | Smart Meters Electric Vehicle Supply Equipment (EVSE) Software Home Energy Management (HEM) Systems |

||

| by Application | Peak Power Sales Spinning Reserves Base Load Power Reactive Power Others |

||

| by End User | Residential Commercial Industrial |

||

Vehicle-To-Grid Technology Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Vehicle-To-Grid Technology Market Key Players:

Major Contributors in the Vehicle-To-Grid Technology Industry in North America:

1. AC Propulsion Inc., United States

2. Boulder Electric Vehicle, United States

3. Coritech Services Inc., United States

4. Edison International, United States

5. Enerdel, United States

6. EV Grid, United States

7. Next Energy, United States

Leading Figures in the European and Asian Vehicle-To-Grid Technology Sector:

1. DENSO Corporation, Japan

2. Hitachi, Japan

3. Honda Motor Co., Ltd., Japan

4. Mitsubishi Motors Corporation, Japan

5. Nissan, Kanagawa Prefecture, Japan

6. ENGIE Group, France

7. Groupe Renault, France

8. OVO Energy Ltd, United Kingdom

FAQs:

1] What Major Key players in the Global Vehicle-To-Grid Technology Market report?

Ans. The Major Key players covered in the Vehicle-To-Grid Technology Market report are AC Propulsion, Edison International, DENSO Co., Boulder Electric Vehicle, Nissan, Enerdel, EV Grid, Hitachi, Next Energy, NRG Energy.

2] Which region is expected to hold the highest share in the Global Vehicle-To-Grid Technology Market?

Ans. North America region is expected to hold the highest share in the Vehicle-To-Grid Technology Market.

3] What is the market size of the Global Vehicle-To-Grid Technology Market by 2032?

Ans. The market size of the Vehicle-To-Grid Technology Market by 2032 is expected to reach 22.56 USD Billion.

4] What is the forecast period for the Global Vehicle-To-Grid Technology Market?

Ans. The forecast period for the Vehicle-To-Grid Technology Market is 2024-2032.

5] What was the market size of the Global Market in 2024?

Ans. The market size of the Market in 2024 was valued at USD 4.25 Billion.