Synthetic Aperture Radar Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Synthetic Aperture Radar Market size was valued at USD 4.65 Billion in 2024 and the total Synthetic Aperture Radar revenue is expected to grow at a CAGR of 12.5% from 2025 to 2032, reaching nearly USD 11.94 Billion.

Synthetic Aperture Radar Market Overview

Synthetic Aperture Radar (SAR) is a crucial tool in remote sensing, using microwave radar signals reflected off the Earth's surface to analyze various physical properties. Unlike optical technology, SAR functions effectively in challenging conditions like darkness, rain, and cloud cover, enabling the detection of habitat changes, moisture levels, human-made or natural alterations, and post-event shifts such as earthquakes. Its applications vary widely, from tracking oil spills' paths in delicate marshes to mapping Alaska's wetlands and studying Antarctic icebergs. Synthetic Aperture Radar (SAR) operates by emitting microwave signals and receiving their reflections, measuring distances in slant and ground ranges, while considering various angles such as flight direction (along-track or azimuth), perpendicular direction (across-track or range), look angle, and incidence angle.

These angles play a pivotal role in influencing the behavior of reflected signals, which in turn affects distinctive image attributes like layover and shadow regions. The significance of these parameters extends beyond imaging; they shape SAR technology's capabilities in diverse applications, impacting segments within the Synthetic Aperture Radar Market.

The Synthetic Aperture Radar (SAR) industry's growth is driven by its versatility across sectors and technological advancements. SAR's unique ability to function in adverse conditions aids environmental monitoring, disaster management, defense, agriculture, and infrastructure monitoring. Technological strides, especially in miniaturization and cost reduction, have made SAR systems more accessible and affordable for diverse applications. SAR's pivotal role in environmental monitoring includes precise assessment of deforestation, habitat changes, and climate studies. Synthetic Aperture Radar (SAR) technology significantly contributes to agriculture by assessing soil moisture levels, optimizing irrigation practices, and forecasting crop yields. Its role in defense applications, coupled with integration into advanced technologies such as AI and machine learning, amplifies the depth of data analysis and enhances insights.

These applications and advancements within SAR technology impact various segments of the Synthetic Aperture Radar market, reflecting its diverse utilization across sectors. Investments in SAR-dedicated satellites and partnerships bolster global data accessibility, reducing monitoring intervals and catering to rising demands for real-time geospatial information. This growth trajectory positions SAR as a vital tool in addressing global challenges and fostering sustainability. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Synthetic Aperture Radar Market Trends:

Integration of SAR technology with other advanced technologies such as Artificial Intelligence (AI) and Machine Learning

The fusion of Synthetic Aperture Radar (SAR) technology with Artificial Intelligence (AI) and Machine Learning (ML) heralds a transformative era in Earth Observation (EO) and remote sensing. SAR's complexity in data handling poses an encounter for leveraging its full potential. Initiatives such as the AI4SAR project, backed by entities such as ESA Φ-lab, strive to simplify SAR data, making it more accessible for broader utilization in ML. This collaboration aims to develop open-source tools, streamlining SAR data handling for temporal and spatial resolution management. Amalgamating SAR's intricate data with AI and ML algorithms, enables deeper insights from SAR imagery, fostering accurate and efficient analysis.

This integration not only simplifies SAR for wider adoption but also unleashes its power for scalable analytics, expediting SAR-driven analytics implementation across diverse sectors. AI and ML advancements empower SAR data, augmenting its interpretability and usability. The intricacy of SAR often dissuades scientists from unlocking its potential fully. Introducing AI into SAR analysis simplifies extracting profound insights from these complex datasets, thereby enhancing SAR's applicability and usability in the Synthetic Aperture Radar market landscape.

AI-enhanced SAR analysis aids in change detection, identifying subtle landscape alterations crucial for urban planning, environmental monitoring, and disaster management. Additionally, ML algorithms excel in classifying SAR images, and discerning specific objects, terrains, or land cover types with enhanced accuracy. This partnership fosters innovation, yielding tools like ICE cube that streamline SAR data intricacies while preserving rich information. These initiatives democratize SAR data accessibility, encouraging broader scientist engagement and innovation within the Synthetic Aperture Radar market domain.

The synergy between SAR, AI, and ML unlocks possibilities for novel applications including automated anomaly detection, predictive modeling, and real-time monitoring in sectors spanning agriculture, urban development, environmental conservation, and disaster response.

Synthetic Aperture Radar Market Dynamics

Increasing applications of the Synthetic Aperture Radar in disaster management and emergency response Boost Market Growth

The Synthetic Aperture Radar (SAR) market is rapidly expanding, largely driven by its pivotal role in disaster management and emergency response. Unlike traditional optical sensors, SAR overcomes limitations posed by cloud cover or low visibility, capturing high-resolution images in disaster-stricken areas. These images become invaluable for swift and accurate damage assessments, aiding emergency responders in gauging the scale of devastation, identifying critical zones needing immediate attention, and formulating effective response strategies. SAR's distinct strength lies in its capability to furnish detailed information regardless of environmental conditions; for instance, during floods, SAR precisely measures water levels, tracks change in river courses, and pinpoints affected regions, facilitating estimations of flood extents and enabling the planning of evacuation routes.

During earthquakes, Synthetic Aperture Radar (SAR) excels in pinpointing ground displacements, aiding early warnings and post-event structural assessments. Its uninterrupted day-and-night monitoring is crucial for wildfire tracking. These capabilities, relevant to disaster response and environmental monitoring, reflect SAR's diverse applications within the Synthetic Aperture Radar market landscape.

SAR contributes significantly by tracking fire boundaries and assessing spread, bolstering firefighting efforts and ensuring community safety. With the escalating frequency and severity of global natural disasters, the demand for advanced technologies to bolster disaster management has surged. Consequently, SAR technology is increasing adoption by governments, disaster response bodies, and humanitarian organizations worldwide. This growing emphasis on effective disaster preparedness propels significant growth within the SAR market. Further fueled by continuous investments in SAR technology, including improved imaging resolution and data processing, the market experiences substantial expansion. SAR's indispensable role in swiftly responding to emergencies solidifies its position as a primary driver behind the burgeoning Synthetic Aperture Radar Market growth.

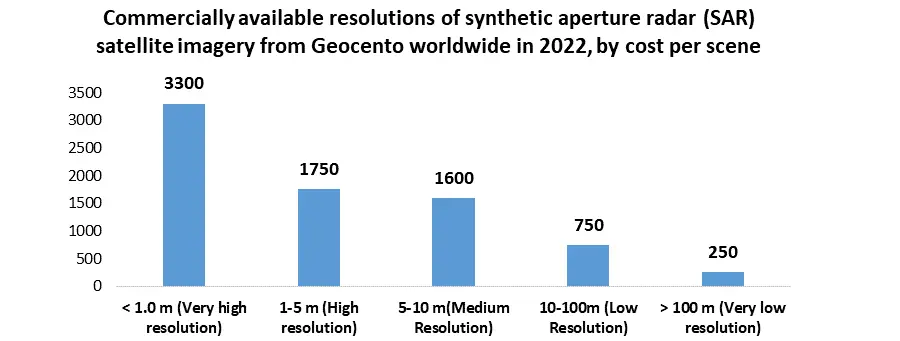

In Geocento offered a range of commercially available resolutions for synthetic aperture radar (SAR) satellite imagery, each varying in cost per scene. The availability of these diverse resolutions caters to different budgetary needs and specific application requirements. The expanding utilization of Synthetic Aperture Radar in disaster management and emergency response scenarios significantly fueled market growth. Its ability to provide precise, real-time information during crises has amplified its relevance and adoption across various sectors.

High Costs Associated with SAR Technology Development, Deployment and Data Acquisition to Hamper Market Growth

The Synthetic Aperture Radar (SAR) market faces a substantial restraint due to the considerable expenses tied to SAR technology development, deployment, and data acquisition. The complexity inherent in SAR systems demands extensive investments across various phases, from research and development to deployment. The initial setup costs for SAR satellites or systems encompass a wide range, covering manufacturing, launching, and ongoing maintenance of satellites or aerial platforms, creating a notable financial barrier. The complexity of processing SAR data demands advanced computational resources and specialized expertise, leading to increased operational expenses.

Such financial challenges hinder smaller organizations or countries with limited resources from accessing SAR technology, restricting its widespread adoption and accessibility within the market. While SAR offers unparalleled capabilities, the high costs associated with acquiring and interpreting SAR data restrict its utilization in certain industries and applications, thereby constraining the overall market expansion. Addressing these cost challenges through collaborative efforts, streamlined data processing techniques, or exploring alternative business models becomes imperative to enhance the accessibility and broader utilization of SAR technology in diverse sectors.

Synthetic Aperture Radar Market Segment Analysis

Based on Frequency Brand, the market is segmented into X, L, C, S, K/Ku/Ka, UHF/VHF and Others. C Frequency brand is a dominant Frequency Brand for the Synthetic Aperture Radar Market in 2024. The C-band frequency (5.3 GHz to 7.1 GHz) holds a dominant position in the Synthetic Aperture Radar (SAR) market owing to its balanced characteristics, making it versatile across various applications. Its moderate wavelength strikes an equilibrium between resolution and penetration capabilities, offering a compelling advantage for multiple industries. Its ability to capture images with relatively fine detail aids in infrastructure monitoring and disaster management, providing valuable data for urban planning and post-disaster assessments.

The moderate atmospheric impact of the C-band compared to higher frequencies ensures more consistent and reliable imaging, especially in areas susceptible to cloud cover or precipitation, establishing it as a favored choice within the Synthetic Aperture Radar Market. These collective attributes position the C-band as a dominant frequency band in SAR applications across diverse sectors.

X Frequency brand is expected to have the fastest growing rate for the Synthetic Aperture Radar Market during the forecast period. The X-band frequency (7.1 GHz to 10.9 GHz) is experiencing rapid growth in the Synthetic Aperture Radar (SAR) market due to its superior high-resolution imaging capabilities. Its shorter wavelengths enable detailed imaging, making it favored for military and defense applications where capturing fine details is crucial. Advancements in technology are enhancing X-band SAR systems, expanding their potential in remote sensing and precision applications like urban planning, infrastructure monitoring, and scientific research.

Synthetic Aperture Radar Market Regional Insights

North America dominated the largest Synthetic Aperture Radar Market share in 2024 and is expected to continue its dominance over the forecast period. North America holds a commanding position in Synthetic Aperture Radar (SAR) technology due to a convergence of factors driving its development, deployment and widespread use. The region's robust aerospace and defense industries serve as a cornerstone for SAR advancements. North America boasts a thriving aerospace sector, marked by significant investments in satellite technology. This environment fosters innovation and the deployment of SAR-equipped satellites. The presence of leading aerospace firms and research institutions enables the refinement of SAR systems, paving the way for technological breakthroughs and the continuous enhancement of SAR capabilities.

North America's strategic emphasis on research and development fuels SAR innovation. The area accommodates various research centers, academic institutions, and government bodies committed to progressing radar and remote sensing technologies, bolstering innovation and development in the Synthetic Aperture Radar Market. Collaborations among academia, government bodies, and industry players drive the evolution of SAR technology, integrating it into diverse applications across sectors.

North America showcases an extensive network of SAR applications spanning defense, security, environmental monitoring, agriculture, infrastructure management, and disaster response. Government agencies rely on SAR for national security, surveillance, and reconnaissance purposes, while industries leverage it for precision agriculture, resource management, and infrastructure monitoring. This wide-ranging utilization underscores the region's adeptness in harnessing SAR's capabilities across multifaceted domains, solidifying its leadership position. North America's conducive regulatory environment and supportive policies play a pivotal role in propelling SAR market growth. Favorable policies, research grants, and public-private partnerships incentivize SAR technology development and deployment. Regulatory frameworks encouraging satellite deployment and data sharing further bolster SAR adoption and application across various industries which boots Synthetic Aperture Radar Market growth.

Synthetic Aperture Radar Market Scope: Inquiry Before Buying

| Global Synthetic Aperture Radar Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 4.65 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 12.5% | Market Size in 2032: | USD 11.94 Bn. |

| Segments Covered: | By Frequency Brand | X L C S K/Ku/Ka UHF/VHF Others |

|

| By Component | Receiver Transmitter Antenna |

||

| By Mode | Single Mode Multimode |

||

| By Application | Defense and Security Environmental Monitoring Agriculture Disaster Management Infrastructure Monitoring Others |

||

Synthetic Aperture Radar Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Synthetic Aperture Radar Key Players

A competitive analysis of the Synthetic Aperture Radar (SAR) industry highlights the strategies, technological innovations, and market positioning of key players. Synthetic Aperture Radar Industry Leaders, such as Lockheed Martin and Airbus, utilize advanced radar systems to secure a significant market share across sectors such as defense, agriculture, and environmental monitoring. These leaders rely on product innovation, competitive pricing strategies, and well-established distribution networks to maintain their dominance. As the demand for high-resolution imagery and real-time data grows, emerging companies are playing an increasingly pivotal role in reshaping market dynamics. Identifying strategic partnerships, evaluating technological breakthroughs, and staying aligned with evolving regulatory frameworks are crucial to sustaining long-term success in this fast-paced industry. With an ever-expanding application range, the Synthetic Aperture Radar industry continues to evolve, driven by both established industry giants and innovative newcomers.

Global

1. Airbus Defence and Space (Ottobrunn, Germany)

2. Lockheed Martin Corporation (Bethesda, Maryland, United States)

3. Northrop Grumman Corporation (Falls Church, Virginia, United States)

4. Thales Group (Paris, France)

5. Raytheon Company (Waltham, Massachusetts, United States)

North America

1. SRC Inc. (Syracuse, New York, United States)

2. Harris Corporation (Melbourne, Florida, United States)

3. IMSAR LLC (Springville, Utah, United States)

4. MDA Information Systems (Gaithersburg, Maryland, United States)

5. Sandia National Laboratories (Albuquerque, New Mexico, United States)

6. Capella Space (San Francisco, California, United States)

7. BlackSky (Seattle, Washington, United States)

Europe

1. SAR AERO (Spain)

2. Saab AB (Stockholm, Sweden)

3. Surrey Satellite Technology Ltd (SSTL) (Guildford, United Kingdom)

4. Leonardo SpA (Rome, Italy)

5. Cobham PLC (Wimborne Minster, United Kingdom)

6. NovaSAR (United Kingdom)

7. TerraSAR-X (Munich, Germany)

Asia Pacific

1. ASELSAN AS (Ankara, Turkey)

2. Israel Aerospace Industries (Lod, Israel)

Frequently Asked Questions:

1] What was the Global Synthetic Aperture Radar Market size in 2024?

Ans: The Global Synthetic Aperture Radar Market size was USD 4.65 Billion in 2024.

2] Which region is expected to dominate the Global Synthetic Aperture Radar Market?

Ans. North America is expected to dominate the Synthetic Aperture Radar Market during the forecast period.

3] What is the expected Global Synthetic Aperture Radar Market size by 2032?

Ans. The Synthetic Aperture Radar Market size is expected to reach USD 11.94 Billion by 2032.

4] Which are the top players in the Global Synthetic Aperture Radar Market?

Ans. The major top players in the Global Synthetic Aperture Radar Market are Airbus Defence and Space (Ottobrunn, Germany), Lockheed Martin Corporation (Bethesda, Maryland, United States), Northrop Grumman Corporation (Falls Church, Virginia, United States), Thales Group (Paris, France), Raytheon Company (Waltham, Massachusetts, United States) and Others.

5] What are the factors driving the Global Synthetic Aperture Radar Market growth?

Ans. Advancements in SAR technology have enabled higher-resolution imaging and improved data processing capabilities and sing demand for accurate geospatial data for urban planning, infrastructure development, and natural resource management are expected to drive market growth during the forecast period.