Sulfur Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

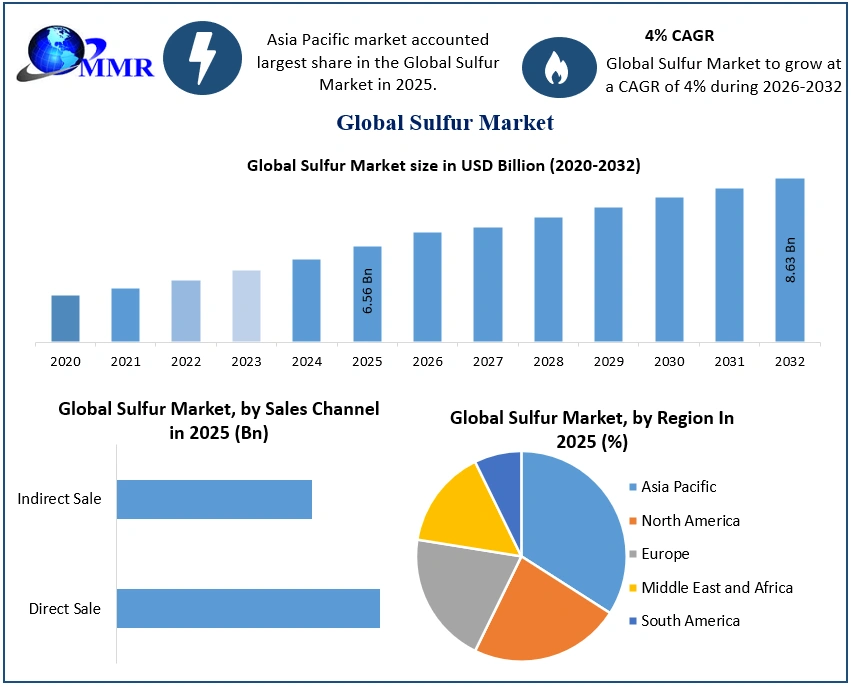

The Sulfur Market size was valued at USD 6.56 Billion in 2025 and the total Sulfur revenue is expected to grow at a CAGR of 4% from 2025 to 2032, reaching nearly USD 8.63 Billion by 2032.

Sulfur Market Overview:

Sulfur occurs naturally as an element in its purest form as well as in the form of sulphate or sulphide minerals. Mineral collectors can distinguish sulphur crystals from other crystal types thanks to their distinctive and vividly coloured polyhedron shapes. Sulfur was once mostly mined from salt domes, where it naturally occurs in pure form, but new technologies have rendered this approach obsolete.

To know about the Research Methodology :- Request Free Sample Report

Sulfur is one of the most important raw materials used in the chemical industry. It is mostly used as a derivative (in acid form) in a variety of industrial and chemical processes, and its single largest end use is the manufacturing of phosphate fertilizers requires a significant amount of it. The processing of rubber, cosmetics, and pharmaceutical applications are significant application areas. Owing to its importance to industrial economies and relative ease of transportation, it is a commodity of great interest.

It is a by-product of several processes, including petroleum refining, tar sands recovery, heavy oil and natural gas processing, coking and metallurgical operations. By using the Frasch method of traditional mining, elemental sulphur is extracted from the ores. It is acquired as a byproduct of the refining of sour crude, tar sand, and sour natural gas. 98.5% of the world's production of elemental sulphur comes from sulphur recovered during refining procedures.

Report scope:

The study seeks to provide market players with a full understanding of the sulfur market. The research looks at market developments from the past, the present, and what is expected for the future. Additionally, it offers a clear interpretation of complicated data. New entrants, market leaders, and followers are a few of the important actors who actively and completely conduct research. The analysis also presents the findings of the PORTER and PESTEL analyses in addition to potential outcomes of the microeconomic components of the market. Once internal and external aspects that have a good or negative impact on the organisation have been taken into account, decision-makers will have a clear futuristic perspective of the market.

Investors are able understand the dynamics and structure of the sulphur market with the market segmentation analysis and market size projection from the study. By clearly laying out the comparative study of the top sulfur companies by price, financial status, product, product portfolio, growth plan, and geographic presence, the research acts as a buyer's guide.

Research Methodology:

MMR began by gathering information on the revenues of the top suppliers in order to estimate and project the Sulfur market. In an effort to segment the market, providers' offers are taken into account by Product (Pharmaceutical Grade, Industrial Grade), By End Use Industry, and ( Fertilizers, Chemical Processing, Metal Manufacturing, Petroleum Refining, Others). After conducting primary research to confirm these divisions, extensive interviews with prominent individuals, including chief executive officers (CEOs), vice presidents (VPs), directors, and executives, were done.

The market's size is projected using bottom-up techniques. Primary and secondary research are used to identify the leading market participants in the sulphur market and determine their market revenues. Instead of conducting secondary research, the major manufacturers' annual and financial reports were analysed, and important opinion and business leaders in the industry, such as CEOs and marketing executives, were spoken with. In the global sulphur market, Nutrien, Ltd., Yara International ASA, The Mosaic Company, K+S, ICL, EuroChem Group and Nufarm Limited are the leading rivals. To enhance their market shares and growth potential, they will keep planning mergers and acquisitions over the course of the forecast year.

Sulfur Market Dynamics:

Market Drivers:

The market is growing as a result of increased fertiliser demand. Plants utilise a sizable amount of nitrogen, phosphorus, potassium, sulphur, calcium, and magnesium. Nutrients are lost from the environment for a variety of reasons, including crop removal, erosion, leaching, soil fixation, and others. When creating critical proteins, lipids, and amino acids in the early stages of development, this is particularly crucial. Its most major contribution to crop production is the creation of protein molecules and amino acids, which are necessary for the development of chlorophyll, lignin, and pectin. This is accomplished by supporting photosynthesis, which is how plants turn solar energy into chemical energy. The production of agricultural fertiliser uses around 55% of all recovered product produced globally.

In addition to being a sizable industry, the fertiliser market also contributes significantly to global food production. This level of productivity would not be possible without intensive agriculture and the usage of fertilisers. Grain production is the primary end-use market for fertilisers, followed by cash crops like vegetables, fruit, flowers, and vines. Economic and population growth are the main factors driving an increase in fertiliser use. Production must maintain pace with consumption's ongoing growth. The demand for the sulfur market is expected to increase in the forecast years, owing to the increasing population.

Eventually, food prices must be high enough to encourage spending and production growth. The generation of H2 SO4, which is largely used to create fertiliser, is one of the many industrial uses for elemental sulphur. The demand for phosphorus (P20s) fertiliser was forecast to be 47,403 thousand tonnes in 2020, and it is expected to increase to 49,097 thousand tonnes in 2021, according to the world fertiliser outlook.

Market Restraints:

Market growth is being hampered by negative exposure reactions. SO is an air pollution-causing sulfur-oxygen gas. Burning fuels like coal, oil, or diesel releases SO2 into the atmosphere. The US Environmental Protection Agency estimates that around 6.5 million tonnes of SO were released into the atmosphere in the US from man-made sources. The main sources of SO2 emissions are industrial boilers, electricity generation, and other industrial processes including metal processing and petroleum refining. Important sources of diesel engines include old buses and cars, locomotives, ships, and off-road diesel machinery. The majority of SO2 exposure occurs among those who reside and work close to these significant sources.

The conversion of SO2 into sulphate particles, which travels hundreds of miles, occurs when it is released into the atmosphere. High-level exposure that is sustained worsens respiratory symptoms and impairs lung function. During exercise, fast breathing and lip breathing both help SO2 enter the lower respiratory tract. The market growth is expected to be hampered owing to this factors.

Market Opportunities:

Chemical processing is driving up demand. The largest market among end-user industries is expected to be chemical processing, which in 2021 accounted for around 90% of the world's sulphur market. Sulfur dioxide is created by using around 90% of the sulphur that is produced or extracted and is then transformed into sulfuric acid. The majority of the acid is employed in the manufacture of phosphate fertilisers, a vital part of the food and beverage sector.

Demand for sulphuric acid is rising on the international market as agricultural output rises. By 2026, it is expected that the average daily calorie availability in the least developed countries will be 2,455 kcal and will exceed 3,050 kcal in other developing nations. On the global market, this is expected to raise demand for agricultural products, increased demand for phosphate fertilisers, growing demand for sulphur in chemical production.Fertilizer demand has increased as a result of rising crop prices. The demand for fertilisers has also increased as a result of the favourable weather in the key agricultural regions. The sulphur market is expected to grow throughout the forecast period as a result of these favourable aspects.

Sulfur Market Segment Analysis:

Based on Product, The Pharmaceutical Grade segment is expected to grow at the highest CAGR during the forecast period. The solutions from Pharmaceutical grade are the result of more than 30 years of research and development aimed at understanding and harnessing the potential of the biological fraction of the soil to improve soil health and increase crop quality and yield.

Blends provide better soil health, more fertility, and higher yields by combining naturally occurring microorganisms with organic acids and nutrients. Pharmaceutical grade respects the delicate processes and balance of nature. Additionally Sulfur is used in the pharmaceutical sector to manufacture medications. The development of sulphur medicines had a huge influence on the growth of the pharmaceutical business. Many medications and organic items contain functional groups that are made from sulphur. Sulfonamides, thioethers, sulfones, and penicillin are the most often used scaffolds in pharmaceuticals containing sulphur.

Based on End Use Industry, The Fertilizers segment is expected to grow at the highest CAGR during the forecast period. More than 55% of the market accounted by the fertilisers category. About 92–95 % of the collected elemental sulphur is used to create sulfuric acid. Thanks to fertilisers and derivatives of ammonium phosphate, this nutrient has gained in popularity recently. For around half of the world's output, fertilisers are the intended use. Around 88% of all fertilisers are made with phosphate, and a sizeable amount of ammonium sulphate is also produced. As a result, this industry is very dependent on the cyclical global phosphate fertiliser market.

The product is used in agriculture as a plant nutrient and also as a step in the production of phosphoric acid, which results in the production of phosphate fertilisers. H2S04, the most widely used inorganic chemical on the globe, is produced from almost all elements and is employed in a wide range of industrial, metallurgical, and agricultural processes.

Sulfur Market Regional Insights:

In 2025, the Asia-Pacific region dominated the global sulphur market. Owing to the rising demand for sulphur in fertiliser production and rubber processing from nations like China and India, the Asia-Pacific region led the market. The largest producer of sulphur internationally is China. The majority of the world's pyrites, or sulphur in all its forms, are produced in China (source). With 36% of all global imports coming from this nation, it is the top importer of sulphur, which is mostly used to make sulfuric acid.

Owing to its increasing concerns over its energy security, China is speeding up its oil and gas exploration efforts. At the moment, the nation imports 72% of the crude oil it refines. As a result, the nation is encouraging private and foreign enterprises to carry out oil and gas exploration and production in the area. Approximately two thirds of the sulfuric acid used in China is utilised in the manufacturing of fertilisers. Calcium, magnesium, and sulphur are examples of secondary fertilisers in the fertiliser sector. Yara China Limited and Nutrien Ltd are two businesses that sell secondary fertilizer-related products.

Additionally, nearly 95.05% of the demand for fertilisers in ASEAN is met by sugarcane, rubber, and oil palm. In the forecast years, plantations are expected to be the primary factor in the growth of the fertiliser business, which then influence the sulphur market.Natural rubber produced at plantations in Malaysia, Thailand, and Indonesia accounts for around one-third of all rubber use worldwide. One of the world's biggest producers and exporters of natural rubber is Thailand.

The aforementioned elements have a part in the region's rising demand for sulphur consumption.

The increased demand for the acid from end-use sectors, such as the chemical, pharmaceutical, and metal extraction industries, cause North America to experience significant growth. Mining activity growth supports market growth. The main use in metal extraction and purification processes is expected to see strong demand.

By the end of the forecast period, Europe is expected to have experienced tremendous growth. The main element affecting growth in the region is the high demand from end-use industries. Chemicals have a large consumer base, which is driving the demand for the product.

Sulfur Market Recent Industry Developments (2025–2026)

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 September 2025 | Southern Ionics | Announced a $34 million expansion of its sulfur chemicals production facility in Alabama. | The investment boosts sodium metabisulfite capacity and reduces North American reliance on imports. |

| 12 July 2025 | ICL Group Ltd. | Launched Sulfurball, a novel sulfur fertilizer featuring advanced spherical granules. | This product targets nutrient deficiencies in soybean and corn crops through gradual soil release. |

| 15 April 2025 | BASF SE | Invested in expanding production capacity for semiconductor-grade sulfuric acid in Germany. | The expansion meets high-purity requirements for chip fabrication and advanced electronics cleaning. |

| 20 March 2025 | Coromandel International Ltd. | Inaugurated a second sulfur manufacturing plant at its facility in Visakhapatnam, India. | This expansion doubled the company's bentonite sulfur capacity to 50,000 metric tons annually. |

| 10 February 2025 | SunSirs | Reported sulfur prices reaching a 2025 low of 1,661 RMB/ton before entering a bull market cycle. | Triggered a repricing of resources as demand from the new energy sector began to outpace supply. |

Sulfur Market Scope: Inquire before buying

| Global Sulfur Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 6.56 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4 % | Market Size in 2032: | USD 8.63 Bn. |

| Segments Covered: | by Product | Pharmaceutical Grade Industrial Grade |

|

| by End Use Industry | Fertilizers Chemical Processing Metal Manufacturing Petroleum Refining Others |

||

| by Application | Sulfuric Acid Synthesis Sulphonate Surfactants Synthesis Agrochemicals Metal Extraction Oil Refining Others |

||

| by Sales Channel | Direct Sale Indirect Sale |

||

Sulfur Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Sulfur Market, Key Players are

North America

1. Nutrien

2. The Mosaic

3. Koch

4. Compass Minerals

5. Kemin Industries

6. Global Nutritech

7. Tiger-Sul Products

8. Sulphur Solutions

Europe

9. K+S

10. SK Eurochem

11. Tessenderlo Group

12. Gazprom

13. Exxon Mobil

14. Rosneft

Asia Pacific

15. Nufarm

16. Deepak Fertilizers and Petrochemicals Ltd.

17. Coromandel International

18. Zuari Agro Chemicals

19. Sulphur Mills

20. Sinopec

Middle East and Africa

21. Israel Chemicals

22. Aramco

23. Abu Dhabi National Oil Company

South America

24. Petrobras

25. Vale

26. Pluspetrol

FAQs:

1. Which is the potential market for the Sulfur in terms of the region?

Ans. In Asia Pacific region, the growing business and educational sectors are expected to help drive the use of collaborative screens.

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is new initiatives from governments that provide funding for Sulfurs in educational institutes

3. What is expected to drive the growth of the Sulfur Market in the forecast period?

Ans. A major driver in the Sulfur Market is the prevalence of work from home and remote collaboration created by the COVID-19 pandemic

4. What is the projected market size & growth rate of the Sulfur Market?

Ans. The Sulfur Market size was valued at USD 6.56 Billion in 2025 and the total Sulfur revenue is expected to grow at a CAGR of 4% from 2025 to 2032, reaching nearly USD 8.63 Billion by 2032.

5. What segments are covered in the Sulfur Market report?

Ans. The segments covered are by Product, by End Use Industry, Application, Sales Channel, and, Region.