Smart Factory Market Size by Product Type, Technology, End User Industry, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

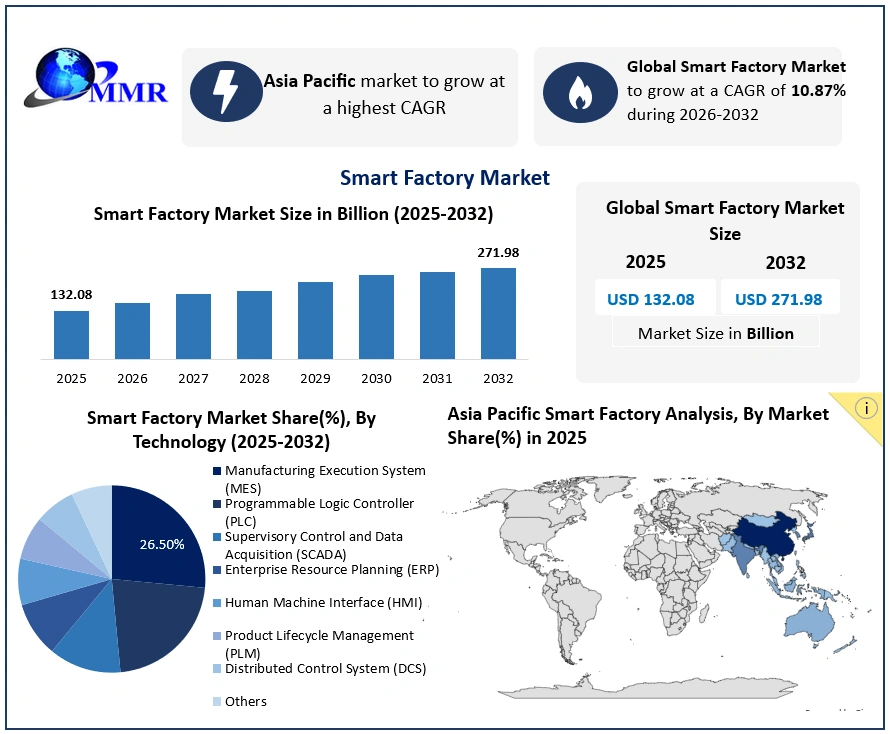

The Global Smart Factory Market was valued at USD 132.08 billion in 2025 and is projected to grow at a CAGR of 10.87% from 2026 to 2032, reaching approximately USD 271.98 billion by 2032. Market growth is driven by accelerating Industry 4.0 adoption, rising deployment of industrial automation, artificial intelligence (AI), industrial IoT (IIoT), robotics, and increasing demand for real-time data analytics, predictive maintenance, and digital manufacturing solutions across global manufacturing industries.

Smart Factory Market Overview

The Smart Factory Market represents a core transformation layer within modern industrial production, enabling intelligent manufacturing, automated decision-making, and real-time operational optimization across factory environments. Smart factories integrate cyber-physical systems (CPS), IoT-enabled sensors, cloud computing, AI-driven analytics, robotics, and automation systems to create a highly connected and adaptive manufacturing ecosystem.

Smart manufacturing environments enable seamless communication between machines, systems, and human operators, improving production efficiency, reducing downtime, and optimizing energy and resource utilization. The shift from traditional automation to intelligent, data-driven manufacturing systems is redefining industrial competitiveness and productivity.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

In 2024, smart factory technologies achieved an estimated penetration rate over 58% across large-scale manufacturing facilities, particularly in automotive, electronics, and industrial equipment sectors. Adoption is increasingly driven by lifecycle cost optimization, productivity gains, and sustainability targets, rather than upfront capital considerations alone.

Key highlights:

• Asia Pacific dominated the Smart Factory Market in 2025, accounting for over 41% market share, supported by strong manufacturing bases in China, Japan, and South Korea, rapid Industry 4.0 deployment, and proactive government-backed digitalization initiatives.

• Industrial Robotics dominated the equipment segment, reflecting high demand for precision manufacturing, continuous production, and labor cost optimization.

• AI and Machine Learning technologies are becoming central to smart factory deployments, particularly in predictive maintenance, quality inspection, production planning, and energy management.

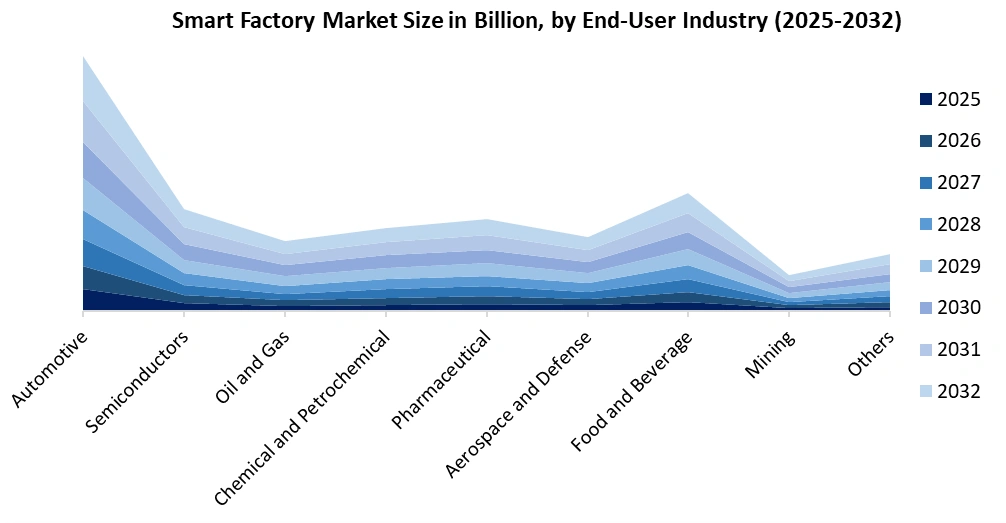

• Automotive manufacturing remained the leading end-user segment, driven by automation-intensive assembly lines, EV production expansion, and demand for digital twins and real-time analytics.

Smart Factory Market: Demand Drivers and Growth Catalysts

Growth in the Global Smart Factory Market is supported by a combination of cost pressures, efficiency requirements, and digital transformation mandates:

• Rising emphasis on operational efficiency, reduced downtime, and production cost optimization

• Increasing adoption of Industry 4.0 principles, including interoperability, decentralization, and information transparency

• Growing deployment of AI, ML, industrial IoT, and robotics to enable predictive maintenance and intelligent decision-making

• Expansion of smart manufacturing solutions across automotive, electronics, aerospace, healthcare, and heavy industries

• Integration of smart factories with energy-efficient systems, including intelligent HVAC infrastructure and industrial flow control solutions

Despite strong demand fundamentals, high initial capital investment, system integration complexity, and skilled workforce shortages continue to act as adoption barriers, particularly for small and medium-sized enterprises (SMEs).

Smart Factory Market: Segment Analysis

Adoption and Utilization Trends (2025–2032)

By Product Type:

Industrial Robotics held the largest market share in 2025, driven by continuous production requirements, precision manufacturing, and labor optimization. These systems deliver long-term cost benefits through improved throughput, reduced waste, and enhanced quality consistency.

By End User:

The Automotive industry dominated the Smart Factory Market due to heavy reliance on robotics, AI-driven quality inspection, and predictive maintenance. Increasing EV production, autonomous vehicle development, and global competition continue to accelerate smart factory investments.

Overall, adoption of smart manufacturing solutions is expanding steadily as manufacturers transition from isolated automation toward fully integrated, intelligent production ecosystems.

Overall, adoption of smart manufacturing solutions is expanding steadily as manufacturers transition from isolated automation toward fully integrated, intelligent production ecosystems.

Smart Factory Market: Regional Analysis

The Asia Pacific Smart Factory Market leads global adoption, supported by large-scale industrialization, export-oriented manufacturing, and aggressive Industry 4.0 roadmaps in China, Japan, South Korea, and India. Government incentives, R&D investments, and smart city initiatives are further strengthening regional dominance.

Panasonic Smart Factory Solutions has recorded 2,000+ export shipments to nearly 80 verified buyers across key manufacturing markets such as India, the Philippines, and Vietnam. In parallel, the company has managed 300+ import shipments, reflecting active inbound sourcing across multiple supplier locations. An analysis of Panasonic Smart Factory Solutions’ trade activity highlights its key buyers, destination markets, supplier origins, and underlying product flow dynamics, underscoring its strong integration within global smart manufacturing supply chains.

North America remains a key growth region, driven by advanced manufacturing technologies, strong adoption of AI and data analytics, and increasing retrofitting of legacy factories with smart automation systems. Sustainability targets and energy optimization initiatives are reinforcing smart factory investments across industrial sectors.

Smart Factory Competitive Landscape Analysis

The Smart Factory Market is characterized by technology-intensive competition, with vendors differentiating through AI capabilities, platform interoperability, cybersecurity, and system integration expertise. Players offering end-to-end smart manufacturing solutions—from hardware to analytics—are gaining a competitive advantage.

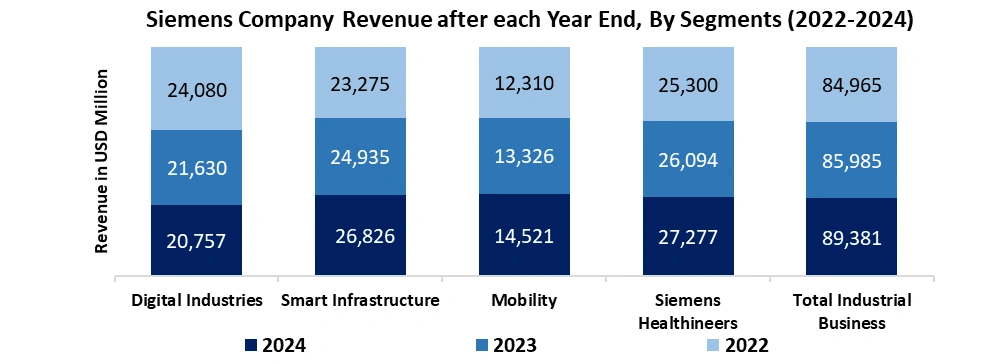

Leading companies such as Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell operate globally distributed automation and digital manufacturing portfolios. Collectively, these players account for a significant share of global smart factory deployments, particularly in automotive, electronics, and process industries.

Asia Pacific is the dominating region, whereas China has the largest market share (%). North America & Europe are the fastest-growing regions.

Recent Developments:

Recent Developments:

| Date | Company | Development | Impact |

| Jul 2025 | Siemens AG | Expanded its smart manufacturing portfolio with a comprehensive industrial automation suite featuring enhanced digital twin and predictive analytics capabilities. | Strengthens Siemens’ position in intelligent manufacturing and enables deeper integration of digital twins for optimized production workflows. |

| Apr 2025 | Rockwell Automation & AWS | Announced a strategic collaboration to integrate Rockwell’s automation platforms with AWS cloud services for scalable IoT data analytics and asset performance management. | Enhances real-time visibility, operational efficiency, and cloud connectivity across customer smart factory deployments. |

| Mar 2025 | Panasonic Smart Factory Solutions | Launched a next-generation modular smart factory system with real-time machine data capture, automated process controls, and integrated robotics orchestration. | Improves production flexibility, increases uptime, and accelerates the adoption of autonomous manufacturing workflows. |

| Feb 2025 | Mitsubishi Electric India | Introduced enhanced no-code data analytics and industrial IoT integration tools for its manufacturing execution systems (MES) and SCADA platforms. | Simplifies data-driven decision-making for manufacturers and increases accessibility of smart factory insights for mid-sized enterprises. |

| Oct 2025 | Stratasys Ltd. | Unveiled advanced additive manufacturing portfolios designed for high-throughput smart factory environments, including robust materials and faster printing capabilities. | Drives broader use of additive technologies for prototyping and small-batch production, reducing lead times and enhancing customization within smart manufacturing. |

Strategic Outlook and Future Prospects

Between 2025 and 2032, the Global Smart Factory Market is expected to witness robust growth as manufacturers prioritize digital transformation, sustainability, and operational resilience. Smart factories will increasingly integrate with adjacent markets such as the Industrial Automation Market, Smart Factory Market, and Building Automation Systems Market, creating intelligent, energy-efficient, and fully connected industrial ecosystems.

As manufacturing shifts toward autonomous, data-centric, and AI-enabled environments, smart factories will remain central to global industrial competitiveness, productivity, and long-term value creation.

Smart Factory Market Scope: Inquire before buying

| Global Smart Factory Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 132.08 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 10.87% | Market Size in 2032: | USD 271.98 Bn. |

| Segments Covered: | by Product Type | Machine Vision Systems Cameras Processors Software Enclosures Frame Grabbers Integration Services Lighting Industrial Robotics Articulated Robots Cartesian Robots Cylindrical Robots SCARA Robots Parallel Robots Collaborative Industry Robots Control Devices Relays and Switches Servo Motors and Drives Sensors Communication Technologies Wired Wireless Others |

|

| by Technology | Product Lifecycle Management (PLM) Human Machine Interface (HMI) Enterprise Resource Planning (ERP) Manufacturing Execution System (MES) Distributed Control System (DCS) Supervisory Control and Data Acquisition (SCADA) Programmable Logic Controller (PLC) Others |

||

| by End User Industry | Automotive Semiconductors Oil and Gas Chemical and Petrochemical Pharmaceutical Aerospace and Defense Food and Beverage Mining Others |

||

Global Smart Factory Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Smart Factory Key Players

1. Industrial Automation & Smart Manufacturing Solution Providers

These companies provide factory automation systems, industrial controls, PLCs, robotics, and smart manufacturing platforms.

North America

1. Rockwell Automation, Inc. – United States

2. Honeywell International Inc. – United States

3. Emerson Electric Co. – United States

Europe

1. Siemens AG – Germany

2. ABB Ltd. – Switzerland

3. Schneider Electric SE – France

4. Bosch Rexroth AG (Robert Bosch GmbH) – Germany

Asia Pacific

1. Mitsubishi Electric Corporation – Japan

2. Fanuc Corporation – Japan

3. Omron Corporation – Japan

4. Yokogawa Electric Corporation – Japan

2. Industrial Robotics & Factory Automation Companies

These companies specialize in industrial robots, robotic automation, machine handling, and automated production systems.

Europe

1. ABB Ltd. – Switzerland

2. Siemens AG – Germany

Asia Pacific

1. Fanuc Corporation – Japan

2. Kawasaki Heavy Industries, Ltd. – Japan

3. Mitsubishi Electric Corporation – Japan

4. Panasonic Smart Factory Solutions – Japan

5. Samsung Electronics Co., Ltd. – South Korea

6. Foxconn Technology Group – Taiwan

North America

1. Rockwell Automation, Inc. – United States

3. Industrial IoT, Cloud & Digital Transformation Providers

These companies provide IIoT platforms, cloud infrastructure, connectivity, analytics, and smart factory digitalization solutions.

North America

1. Microsoft Corporation (Azure IoT) – United States

2. IBM Corporation – United States

3. Cisco Systems, Inc. – United States

4. PTC Inc. (ThingWorx) – United States

5. General Electric Digital (GE Digital) – United States

Europe

1. SAP SE – Germany

2. Dassault Systèmes SE – France

Asia Pacific

1. Huawei Technologies Co., Ltd. – China

2. Fujitsu Limited – Japan

3. Hitachi, Ltd. – Japan

4. Industrial Software, Digital Twin & Manufacturing Execution System (MES) Providers

These companies develop software platforms for digital twins, factory simulation, manufacturing execution systems (MES), asset management, and production optimization.

North America

1. PTC Inc. – United States

2. General Electric Digital (GE Digital) – United States

Europe

1. AVEVA Group plc (Schneider Electric Software) – United Kingdom

2. Siemens Digital Industries Software – Germany

3. Dassault Systèmes SE – France

4. SAP SE – Germany

Asia Pacific

1. Hitachi, Ltd. – Japan

2. Fujitsu Limited – Japan

5. Machine Vision, Inspection & Industrial Sensing Companies

These companies provide machine vision systems, industrial sensors, quality inspection solutions, and factory intelligence technologies.

North America

1. Cognex Corporation – United States

Europe

1. Siemens AG – Germany

Asia Pacific

1. Keyence Corporation – Japan

2. Omron Corporation – Japan

3. Panasonic Smart Factory Solutions – Japan

Frequently Asked Questions:

Q1: What is the market size and forecast period for the Smart Factory Market?

Ans: The Global Smart Factory Market was valued at approximately USD 132.08 billion in 2025 and is projected to expand significantly over the forecast period from 2026 to 2032

Q2: Who are the key players in the Smart Factory Market?

Ans: The Smart Factory Market is highly competitive and technology-intensive, with leading players operating across automation, industrial IoT, software, and analytics domains. Major participants include Siemens AG, ABB Ltd., Schneider Electric SE, Rockwell Automation Inc., Honeywell International Inc., General Electric (GE Digital), Mitsubishi Electric Corporation, Fanuc Corporation, Bosch Rexroth, Emerson Electric Co., and Panasonic Smart Factory Solutions.

Q3: Which industries are the largest adopters of smart factory solutions?

Ans: Automotive manufacturing is the largest adopter of smart factory solutions due to its high automation intensity and need for precision manufacturing.

Q4: What are the main growth drivers of the Smart Factory Market?

Ans: Key growth drivers include increasing emphasis on operational efficiency, rising adoption of Industry 4.0 principles, growing deployment of AI-driven predictive maintenance, demand for real-time production visibility, labor shortages in manufacturing, and the need to reduce downtime and production costs.

Q5: What challenges limit the adoption of smart factory technologies?

Ans: Despite strong growth prospects, smart factory adoption is challenged by high initial capital investment, complex system integration, cybersecurity risks, and the shortage of skilled professionals capable of managing advanced digital manufacturing systems.