Semiconductor Materials Market Type, Application, End User, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

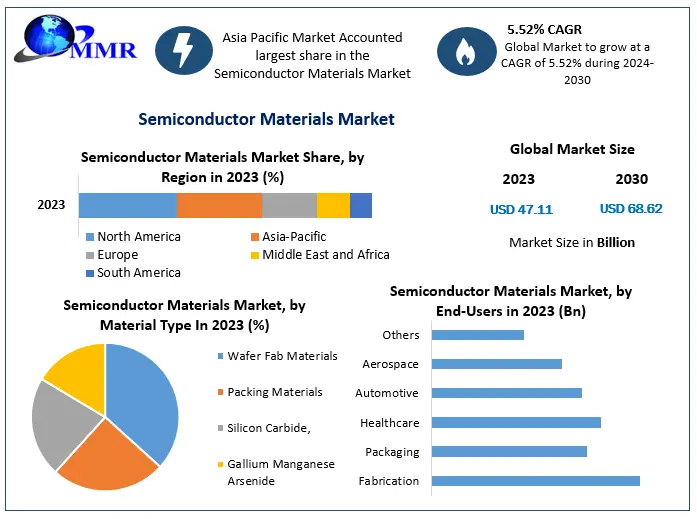

Semiconductor Materials Market size was valued at USD 66.27 Bn. in 2025 and is expected to reach USD 91.1 Bn. by 2032, at a CAGR of 4.65%.

Semiconductor Materials Market Overview

Semiconductor Materials are available in many varieties each with unique characteristics and application. Silicon, gallium, nitride, silicon carbide, and gallium phosphide are some Semiconductor materials. Silicon is the most common semiconductor material, known for its excellent stability, low cost, and mature processing technology. This is produced in various forms, such as single-crystal silicon, polycrystalline silicon, and amorphous silicon, with single-crystal silicon being the most widely used in the manufacturing of integrated circuits.

The Semiconductor Materials Market growth is driven by increasing demand for electronic elements in automotive, consumer electronics, and industrial applications. Also, the market is influenced by new technology advancements such as AI, IoT integration and others, which need advanced material.

To know about the Research Methodology :- Request Free Sample Report

Semiconductor Materials Market Dynamics

Technology Development in Electronic Materials and New Products Innovation To Drive the Market

The advancement and proliferation of wireless communication technologies are driving the semiconductor materials market growth. Wireless communication, including infrared, satellite, broadcast radio, microwave, mobile communications systems, Wi-Fi, Bluetooth, Zigbee, and RF power devices, all rely heavily on semiconductor materials for their functionality. Small devices capable of delivering several watts of RF power, which is commonly found in handheld applications such as cellphones, necessitate efficient semiconductor materials to ensure optimal power conversion and transmission. Also, high-power RF devices used in infrastructure applications, such as cellphone base stations, demand robust semiconductor materials to handle the high-power levels efficiently.

The development of wireless communication systems like 5G heavily relies on System-on-Chip (SoC) and Field-Programmable Gate Array (FPGA) devices, which are integral parts of the semiconductor materials market. These devices require advanced semiconductor materials to achieve high performance and power efficiency. As the Internet of Things (IoT) is steadily advancing, various types of things are being connected to the Internet including industrial equipment, home appliances, and vehicles in addition to PCs and smartphones. Several different semiconductor devices are required to advance the IoT, one of which is an edge device such as a sensor, and another is a high-performance device that stores and processes large volumes of collected data on servers and data centers.

For instance, DuPont materials innovation for EUV lithography and sustainability at SPIE Advanced Lithography + Patterning, focusing on addressing technical challenges in semiconductor scaling. DuPont offers advanced EUV underlayers and photoresists. Their research aims to enhance resolution, reduce line width roughness, and improve sensitivity. Also, they prioritize sustainability by developing non-fluorinated components for safer semiconductor materials. They're committed to sharing these advancements to accelerate sustainable material design across the semiconductor industry. End-to-end materials solutions to support the semiconductor manufacturing process and experience and innovation have deep roots in the semiconductor fabrication industry.

Low-energy microcontrollers (MCUs) enabling Bluetooth capabilities utilize semiconductor materials optimized for low power consumption, driving demand for energy-efficient materials and propel the Semiconductor Materials Market growth. The rise of wireless sensor networks for applications such as environmental monitoring, structural monitoring of bridges and buildings, and asset tracking underscores the importance of semiconductor materials in enabling these networks. These sensors often require specialized semiconductor materials tailored for specific environmental conditions and power constraints.

Government Support and Investment to Drive the Market

Government initiatives and investments in the Semiconductor Materials Industry, particularly in regions like Asia-Pacific, are supporting the growth of the market. These initiatives often focus on research and development, infrastructure development, and incentivizing semiconductor manufacturing. For instance,

CHIPS For America Announces Funding Opportunity To Expand U.S. Semiconductor Packaging: the U.S. Department of Commerce issued a Notice of Funding Opportunity (NOFO) to seek applications for research and development (R&D) activities that will establish and accelerate domestic capacity for advanced packaging substrates and substrate materials, a key technology for manufacturing semiconductors. The CHIPS for America program anticipate approximately $300 million in funding innovation across multiple technologies ranging from semiconductor-based to glass and organics. The Department of Commerce is overseeing $50 billion to revitalize the U.S. semiconductor industry and strengthen the country’s economic and national security. CHIPS for America R&D within the U.S. Department of Commerce is responsible for administering $11 billion to advance U.S. leadership in semiconductor R&D. CHIPS R&D is a critical part of President Biden’s agenda to support American innovation for decades to come. These factors help to drive the Semiconductor Materials Market growth.

The deployment of 5G technologies robust investments in cloud services and data centers and the increased digitization of various economies developed as well as developing will contribute to the growth of the semiconductor materials market. There's an increased demand for miniaturization of various electronics this demand is creating more opportunities for the growth of the semiconductor materials industry. The semiconductor materials market is also expected to grow well in the developing region as the consumer base for electronics in this region is growing spontaneously. Increased use of semiconductors in data storage devices is also expected to be a growth factor for this industry. The ongoing innovation and development of connectivity, data centers, communications, automotive, and advanced software. Increasing consumption of electronic components used in the safety, infotainment, and navigation of automobiles is expected to create a lucrative opportunity for Semiconductor Material Market growth.

Emerging Technologies Research for Semiconductor Materials to Create Lucrative Opportunity for Market Growth

The materials, such as gallium nitride (GaN), silicon carbide (SiC), and organic semiconductors, offer unique properties such as higher efficiency, faster processing speeds, and flexibility. They enable the development of smaller, lighter, and more energy-efficient electronic devices, from smartphones to electric vehicles and beyond. Advancements in materials science facilitate the creation of novel applications including flexible displays, wearable electronics, and efficient renewable energy systems. This helps to push the boundaries of traditional semiconductor materials, these innovations drive progress in various industries, enhancing performance, reducing costs, and opening doors to unprecedented technological capabilities and are expected to boost the Semiconductor Materials Market Growth.

The nanoscale and quantum scale phenomena in semiconducting materials create a myriad of opportunities to achieve novel, scalable, and integrable technologies with potential impact on diverse areas of science and engineering. To combine unique nanofabrication and integration processes to develop an atomistic understanding of the science of epitaxial growth of semiconductors and implement nanoscale probes to test their properties and functionalities. The associated research programs will strive for excellence and aim for the highest impact on advanced fundamental as well as technological implications for the next generation of nanoelectronics, optoelectronics, photonics, clean-energy harvesting, bio-integrable, and quantum technologies.

Supply Chain Disruptions to Restrain the Market Growth

The semiconductor materials market faces significant challenges due to disruptions in the global supply chain. Factors such as natural disasters, and geopolitical tensions, can hamper the production and distribution of key materials. These disruptions lead to shortages, increased lead times, and higher costs for manufacturers. For instance, the shortage of rare earth elements critical for semiconductor manufacturing has led to volatility in prices and constrained supply, affecting the overall market dynamics and profitability. The semiconductor industry operates on cutting-edge technologies with high levels of complexity. Developing and producing advanced materials require substantial investments in research, development, and infrastructure. The constant need for innovation to meet evolving technological demands adds to the cost burden. This high cost of entry poses a barrier for smaller companies and startups, limiting their ability to compete and innovate in the semiconductor materials market. However, Disruptions like the COVID-19 pandemic and geopolitical conflicts further exacerbate these challenges, leading to supply chain disruptions, inventory issues, and production constraints.

Semiconductor Materials Market Segment Analysis

Based on Type, the Silicon Carbide (SiC) segment held the largest Semiconductor Materials Market share in 2025. It provides higher thermal conductivity; higher electron mobility and lower power losses and these factors are primary drivers of the segment growth. SiC diodes and transistors also operate at higher frequencies and temperatures without compromising reliability. The main applications of SiC devices, such as Schottky diodes and FET/MOSFET transistors, include converters, inverters, power supplies, battery chargers and motor control systems.

Based on End User, the consumer electronics segment is expected to grow with the highest CAGR during the forecast. There is a high demand for semiconductors in wireless communication and it has a great application in mobile phones. The use of semiconductor material in the wireless technology is increasing every day due to the superior speed and the efficiency that it provides. The most familiar wireless application is the mobile phone, where smartphones now account for 55% of all mobile subscriptions globally. Today’s cell phones use 3G and 4G wireless communications systems. With the increasing innovation and developments in various tablets smartphones and varied gadgets people use the market for the semiconductor material. Semiconductor materials are used also used in satellite systems, and other communication devices, network equipment, and other hardware for data transmission. such factors are expected to boost the segment Semiconductor Materials Market size.

Semiconductor Materials Market Regional Insight

Asia Pacific dominated the largest Semiconductor Materials Market share in 2025. The region has a great demand for semiconductor materials as there's an increasing demand for wireless technologies and there is also an increase in the demand for consumer electronic products in these developing economies. Asian countries such as Japan, Taiwan, China, India and South Korea have played a leading role in the development of the semiconductor materials industry. Taiwan is the largest manufacturer of semiconductors in the world. As a result, many major market players are based in Taiwan such as Taiwan Semiconductor Manufacturing Company Limited, which held the largest market share. The increased government initiatives in the manufacturing of semiconductor materials in the South Korea, region are also expected to grow well during the forecast period.

For instance, the government of South Korea has announced to offer around KRW one trillion for manufacturing 8-inch wafer chip. This money offered by the government shall be allotted in the form of long-term loans. The Government of India is also pushing the development of the semiconductor industries to reduce the dependency of India on various other countries. The JV formation awaits necessary approvals from the Ministry of Electronics and Information Technology (MeitY) and subsidies from central and state governments. The investment breakdown includes US$205 million from CG, US$15 million from Renesas, and US$2 million from Stars, with the total equity capital representing 92.34 percent, 6.76 percent, and 0.90 percent, respectively.

In November 2023, CG disclosed plans to invest approximately US$791 million over five years for the OSAT venture. Such factors are expected to drive the growth of the semiconductor materials industry in the Asia Pacific region.

China imposes export controls on 2 metals used in semiconductors and solar panels. The government has announced buyers of two metals used in computer chips and solar panels will need to apply for export permits. The metals, gallium and germanium, are also used in military applications. China produces 60% of the world's germanium and 80% of the world's gallium. It also dominates supply chains for rare earth minerals used in many high-tech products, as well as the lithium, cobalt and graphite used in batteries. Semiconductors are essential components of consumer and industrial electronic products like smartphones, computers, and telecommunication equipment. As the world's largest manufacturing hub, China accounted for nearly 30% of global manufacturing output in 2022 and has been the world’s largest consumer of semiconductors, both for domestic use and exports. As a result of, increasing semiconductor demand there is a rise in the need for semiconductor materials and this factor drives the Semiconductor Materials Market growth.

North America Semiconductor Materials Market is expected to grow at a significant CAGR over the forecast period. Their efficient management and supply chain operations despite the rising consumption are expected to boost the market growth. The economic condition and the presence of established market players in the region have enabled the country to maintain the first-class design and offer an increased production rate. The GaN semiconductor is increasingly produced in the region as it is intensively utilized in LED lighting and wireless technologies. The demand for GaN semiconductors is increasing as the demand for LED lighting is rapidly increasing across the region. Also, the presence of renowned semiconductor manufacturing facilities across the region and the growing adaptation of portable devices are key factors that driving the semiconductor materials industry growth across North America.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 18 March 2025 | TSMC | Announced a major breakthrough in its A14 process (1.4nm equivalent), integrating a novel 2D channel material. | Creates immediate demand for new precursor chemicals and advanced polishing slurries required for sub-2nm nodes. |

| 22 May 2025 | Foxconn | Received official approval for a strategic joint venture with HCL to establish an advanced semiconductor unit in India. | Diversifies the global material supply chain and establishes a new regional hub for high-volume semiconductor manufacturing. |

| 04 August 2025 | Shin-Etsu Chemical | Commenced construction of its fourth lithography materials plant in Japan with a USD 560 million investment phase. | Strengthens the supply of high-end photoresists critical for EUV lithography used in next-generation chip production. |

| 14 January 2026 | Applied Materials | Released a suite of new engineering materials designed to enable copper wiring scaling for 2nm logic nodes and beyond. | Improves performance-per-watt in data center chips, directly influencing material requirements for high-performance computing. |

| 11 February 2026 | Samsung Electronics | Confirmed the mass production of HBM4 memory chips utilizing advanced hybrid bonding materials. | Shifts the market focus toward high-bandwidth packaging materials to support the ongoing AI infrastructure boom. |

Semiconductor Materials Market Scope: Inquiry Before Buying

| Semiconductor Materials Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 66.27 USD Bn |

| Forecast Period 2026-2032 CAGR: | 4.65% | Market Size in 2032: | 91.09 USD Bn |

| Segments Covered: | by Type | Silicon Carbide Gallium Manganese Arsenide Copper Indium Gallium Selenide Molybdenum Disulfide Bismuth Telluride Others |

|

| by Application | Packaging & Assembly Molding & Encapsulation Wafer Dicing Wire Bonding / Flip chip Wafer Fabrication Doping/Ion Implantation Photolithography Substrate Manufacturing |

||

| by End User | Consumer Electronics Telecommunication Manufacturing Defense & Aerospace Others |

||

Semiconductor Materials Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Key Players / Competitors Profiles Covered in Brief in Global Semiconductor Materials Market Report in Strategic Perspective:

- Air Liquide Electronics

- Applied Materials Inc.

- Avantor Inc.

- BASF SE

- Caplinq Europe B.V.

- Coherent Inc.

- CoorsTek Inc.

- Corning Incorporated

- DuPont de Nemours Inc.

- Entegris Inc.

- Ferrotec Holdings Corporation

- FURUKAWA CO. LTD.

- Hemlock Semiconductor Operations LLC

- Henkel AG & Company KGaA

- Hitachi Chemical Co. Ltd

- Honeywell International Inc.

- Indium Corporation

- Infineon Technologies AG

- Intel Corporation

- JSR Corporation

- JX Advanced Metals Corporation

- KYOCERA Corporation

- LG Chem Ltd

- Linde plc Electronics

- Merck KGaA

- Mitsubishi Chemical Corporation

- Nichia Corporation

- Nitto Denko Corporation

- Resonac Holdings Corporation

- Sumitomo Chemical Co. Ltd