Semiconductor Manufacturing Equipment Market : Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

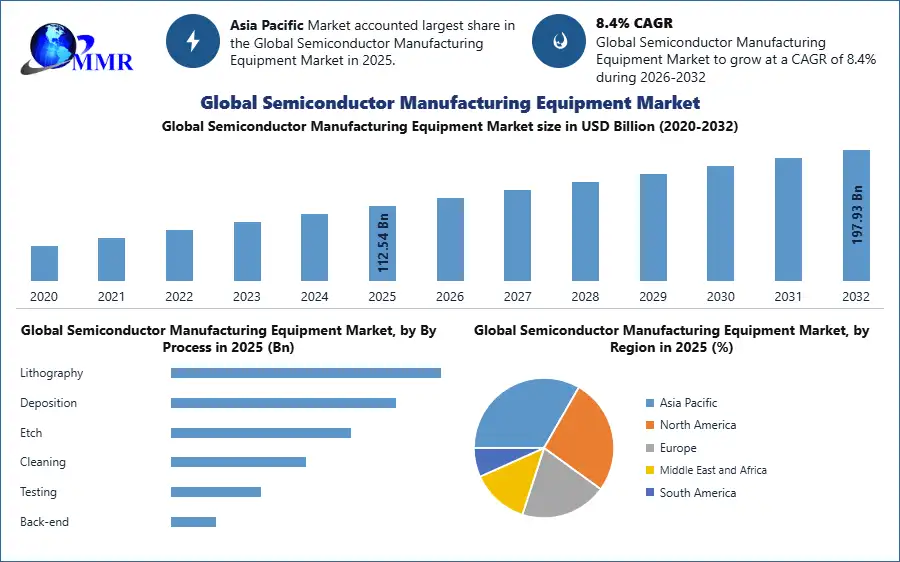

Semiconductor Manufacturing Equipment Market was valued at USD 112.54 Bn. in 2025 and is expected to reach USD 197.93 Bn. by 2032, at a CAGR of 8.4% during the forecast period.

Global Semiconductor Manufacturing Equipment Market Overview

Semiconductor manufacturing equipment refers to the machinery and tools used in the production of semiconductor devices, which are essential components of electronic devices such as computers, smartphones, and other electronic gadgets. The semiconductor manufacturing process involves the creation of integrated circuits (ICs) on semiconductor wafers. The semiconductor manufacturing equipment market is a dynamic and crucial sector within the broader semiconductor industry. The demand for advanced semiconductor devices, driven by innovations in areas such as artificial intelligence, 5G communication, autonomous vehicles, and the Internet of Things (IoT), has a direct impact on the semiconductor manufacturing equipment market.

The market is significant and has experienced steady growth over the years. The growth is fueled by the increasing complexity and miniaturization of semiconductor devices, as well as the demand for high-performance computing. The market is highly competitive, with several major players dominating different segments. Major companies involved in the semiconductor manufacturing equipment market include ASML, Applied Materials, Lam Research, Tokyo Electron Limited (TEL), KLA Corporation, and others. The semiconductor industry, including the equipment market, often experiences cyclical patterns influenced by factors such as global economic conditions, demand for electronic devices, and industry-specific investment cycles.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Semiconductor Manufacturing Equipment Market Dynamics

Rising Demand for Semiconductor Devices to boost Semiconductor Manufacturing Equipment Market growth

The increasing use of semiconductor devices in various applications, such as smartphones, computers, automotive electronics, and IoT devices, fuels the demand for semiconductor manufacturing equipment. Emerging technologies like 5G, artificial intelligence, and the Internet of Things contribute to a growing need for high-performance and specialized semiconductor components. The semiconductor industry has been driven by Moore's Law, which predicts a doubling of the number of transistors on a microchip approximately every two years, leading to increased computing power. To meet the requirements of smaller and more powerful semiconductor devices, Semiconductor Equipment manufacturers invest in cutting-edge equipment that enables the production of chips with smaller feature sizes.

Advancements in lithography, materials deposition, and other critical processes drive the demand for advanced semiconductor manufacturing equipment. As semiconductor devices become more sophisticated and feature-rich, the complexity of their designs also rises. This complexity requires advanced equipment that handles intricate manufacturing processes, such as multiple patterning, 3D integration, and FinFET technology. The demand for equipment capable of achieving high precision and accuracy in manufacturing processes is on the rise, which significantly boosts the Semiconductor Manufacturing Equipment Market growth.

Semiconductor manufacturers are continually moving to smaller technology nodes (e.g., 7nm, 5nm, and beyond) to enhance performance and energy efficiency. This transition involves the adoption of new materials and manufacturing techniques. Equipment that supports processes such as extreme ultraviolet (EUV) lithography, advanced deposition and etching methods, and innovative materials is in high demand. The rollout and adoption of 5G technology worldwide drive the demand for semiconductor devices that power 5G infrastructure and devices. This includes semiconductors for base stations, smartphones, and other components of the 5G ecosystem. The development and production of these devices necessitate advanced semiconductor manufacturing equipment.

The automotive industry's increasing reliance on electronics and the transition to electric vehicles contribute to the demand for specialized semiconductor components. Advanced driver-assistance systems (ADAS), in-vehicle infotainment, and electric powertrains rely on semiconductors, driving the need for equipment capable of producing these components with high precision and reliability. The location of semiconductor manufacturing facilities plays a crucial role in shaping the Semiconductor Manufacturing Equipment Market. Investments and expansions in semiconductor manufacturing capabilities, particularly in regions like Asia (e.g., Taiwan, South Korea, and China), influence the demand for equipment. Government incentives, strategic initiatives, and infrastructure development contribute to the global distribution of semiconductor manufacturing activities.

High Capital Cost to restrain Semiconductor Manufacturing Equipment Market Growth

The semiconductor manufacturing process requires significant capital investment in advanced equipment and technology. The high costs associated with purchasing, installing, and maintaining semiconductor manufacturing equipment are deterrent for smaller companies or those with limited financial resources, which significantly limits the Semiconductor Manufacturing Equipment Market growth. This barrier to entry limit market participation and competition. The semiconductor industry, including the equipment market, is characterized by cyclical patterns influenced by global economic conditions, consumer demand for electronic devices, and industry-specific investment cycles.

Periods of downturns or economic uncertainty lead to reduced capital spending by semiconductor manufacturers, impacting the demand for new equipment and restraints the Semiconductor Manufacturing Equipment Market growth. The development and commercialization of new semiconductor manufacturing technologies often involve long and complex cycles. The time required for research, development, and the transition to mass production is challenge for Semiconductor Manufacturing Equipment companies in terms of resource allocation and return on investment. This lengthy cycle also result in a lag between technology advancements and their widespread adoption.

The semiconductor industry evolves quickly, with new technologies and advancements continually replacing older ones. Equipment that becomes outdated due to rapid technological obsolescence may require manufacturers to make substantial investments in upgrading or replacing machinery to stay competitive. This poses a challenge for companies in managing their equipment lifecycle and staying current with industry trends. The semiconductor industry is sensitive to international trade policies and export controls. Changes in trade relations and regulations impact the movement of semiconductor equipment and materials across borders, affecting the global supply chain and potentially limiting Semiconductor Manufacturing Equipment market access for certain companies.

The semiconductor manufacturing process involves the use of various chemicals and materials, some of which have environmental and regulatory implications. Compliance with environmental regulations, waste disposal, and adherence to safety standards add complexities and costs to the manufacturing process. Stricter environmental regulations also influence the development of new, eco-friendly manufacturing technologies.

Semiconductor Manufacturing Equipment Market Segment Analysis

In the Semiconductor Manufacturing Equipment Market (2025), lithography emerges as the dominant process segment due to its critical role in nanoscale pattern formation and transistor definition. Lithography systems enable the transfer of circuit patterns onto silicon wafers using deep ultraviolet (DUV) and extreme ultraviolet (EUV) radiation, directly influencing feature size, device density, and overall chip performance. The process follows the Rayleigh resolution principle, where shorter wavelengths and higher numerical aperture improve pattern precision at sub-7 nm nodes. Additionally, lithography is highly capital-intensive, with EUV systems costing over $200 million per unit, contributing significantly to total equipment spending. The requirement of multiple lithography steps per wafer and its role as a scaling enabler for advanced technologies such as AI and high-performance computing further reinforce its dominant market position.

Semiconductor Manufacturing Equipment Market Regional Insights

Rapid Growth in Semiconductor Demand to boost Asia Pacific Semiconductor Manufacturing Equipment Market growth

The Asia Pacific region, particularly countries like China, South Korea, Taiwan, and Japan, has witnessed a surge in the demand for semiconductors. This demand is driven by various industries, including consumer electronics, automotive, telecommunications, and industrial applications. The need for advanced semiconductor manufacturing equipment to meet this growing demand acts as a significant driver. Countries in the Asia Pacific region have been actively expanding their semiconductor manufacturing capabilities. For instance, China has made substantial investments in building new semiconductor fabs to reduce its reliance on imports. Taiwan and South Korea continue to invest in upgrading existing facilities and constructing new ones.

This expansion fuels the demand for state-of-the-art semiconductor manufacturing equipment. To maintain competitiveness in the global semiconductor market, companies in the Asia Pacific region continuously adopt advanced manufacturing technologies and transition to smaller process nodes. This involves the deployment of cutting-edge semiconductor manufacturing equipment, including lithography machines, deposition tools, and etching equipment, to produce more powerful and energy-efficient chips. The overall economic growth and industrialization in the Asia Pacific region contribute to increased demand for electronic devices. As a result, semiconductor manufacturers invest in expanding production capacities and upgrading equipment to keep up with the rising demand. This trend propels the semiconductor manufacturing equipment market forward.

China has been a significant player in the semiconductor industry, and it has heavily invested in expanding its semiconductor manufacturing capabilities. As part of its efforts to become more self-reliant in the production of semiconductors, China imports a substantial amount of semiconductor manufacturing equipment, which significantly boosts the Asia Pacific Semiconductor Manufacturing Equipment Market growth. The exact percentage vary, but given China's emphasis on technological advancement, the share of SMEs in its total imports is notable. South Korea is home to major semiconductor manufacturers, and its semiconductor industry is a key driver of the country's economy. South Korea produces and imports semiconductor manufacturing equipment to maintain its position in the global semiconductor market.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 25 February 2026 | Applied Materials | The company reached a settlement with the Department of Justice (DOJ), agreeing to pay a penalty of $252 million. | The resolution addresses long-standing regulatory inquiries, providing the company with greater financial and operational clarity for the 2026 fiscal year. |

| 18 December 2025 | ASML | The company successfully shipped its inaugural High-NA EUV (0.55 NA) lithography system to Intel for approximately $400 million. | This delivery marks the commercial start of next-generation patterning, enabling the production of chips at the 2nm node and beyond. |

| 03 September 2025 | Tokyo Electron (TEL) | The company announced the opening of new engineering and support offices in Dholera, Gujarat, and Assam to support Tata Electronics' fab projects. | The expansion places 200 to 300 specialized engineers on-site to facilitate the installation and maintenance of front-end wafer processing equipment in India. |

| 15 August 2025 | Universal Chiplet Interconnect Express (UCIe) | The industry consortium ratified the new UCIe standard to accelerate the development of multi-vendor chiplet ecosystems. | This standardization is expected to drive a surge in demand for advanced packaging and hybrid-bonding tools from suppliers like Besi and EVG. |

| 12 April 2025 | TSMC | The company broke ground on its third fabrication facility in Arizona, designated for N2 (2nm) and A16 process technologies. | The project will require massive procurement of EUV scanners and ALD chambers, contributing to a projected $65 billion total investment in the region. |

Global Semiconductor Manufacturing Equipment Market Scope: Inquire before buying

| Global Semiconductor Manufacturing Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 112.54 USD Billion |

| Forecast Period 2026-2032 CAGR: | 8.4% | Market Size in 2032: | 197.93 USD Billion |

| Segments Covered: | By Process | Lithography Deposition Etch Cleaning Testing Back-end |

|

| By Fab Facility | Automation Chemical Control Gas Control Others |

||

| By Product Type | Memory Logic Analog Components Optoelectronic Components Discrete Components Others |

||

| By Dimension | 2 D 2.5 D 3 D |

||

| By End-User | Foundries OSATs IDMs |

||

Semiconductor Manufacturing Equipment Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Semiconductor Manufacturing Equipment Key Players

- ViTrox Corporation

- Lam Research

- Pentamaster

- Mi Technovation

- ASMPT

- Aemulus

- VisDynamics

- ASML Holding N.V.

- Applied Materials

- Tokyo Electron Limited

- KLA Corporation

- ASM International

- SCREEN Semiconductor Solutions

- Hitachi High-Tech

- Advantest

- Canon

- Nikon

- Tokyo Seimitsu

- DISCO

- Kokusai Electric

- Veeco Instruments

- Kulicke & Soffa

- EV Group

- SUSS MicroTec

- Onto Innovation

- Cohu

- SEMES

- NAURA Technology Group

- AMEC

- ACM Research

- Nordson

- Oxford Instruments Plasma Technology

- Ushio

- Mattson Technology

- Wonik IPS

- Hanmi Semiconductor

- Kingsemi

- HERMES-Epitek

- Modutek