Respiratory Protection Equipment Market Size by Product Type, End User, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

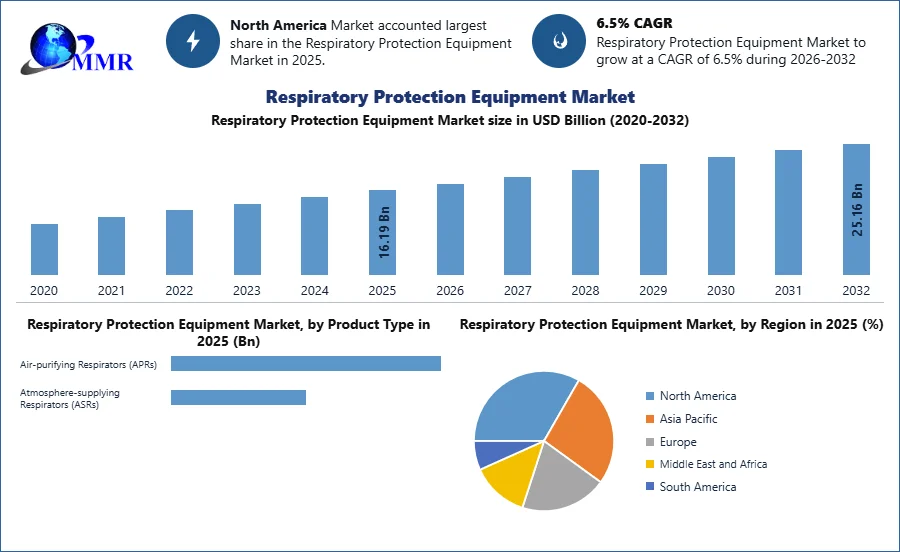

The Respiratory Protection Equipment Market size was USD 16.19 Billion in 2025 and is predicted to grow with a CAGR of 6.5% by generating a revenue of USD 25.16 Billion by 2032.

Respiratory Protection Equipment Market Overview:

Respiratory Protective Equipment (RPE) is a specialized form of Personal Protective Equipment (PPE) designed to shield individuals from inhaling hazardous substances present in the workplace environment. It is regarded as a final option in the hierarchy of control measures, only to be utilized when other methods have proven insufficient in adequately managing exposure risks. Employers are obligated to prioritize strategies such as eliminating the hazard at its source, followed by substitution with less harmful alternatives, implementing engineering controls like ventilation systems, and adopting administrative measures such as restricted access to hazardous areas. PPE, including RPE, is considered a last resort due to its limitations, including the potential for misuse or failure, such as selecting the wrong type of RPE for the task at hand. The reliance on RPE alone leads workers to develop a false sense of security, highlighting the importance of comprehensive risk management strategies.

The Respiratory Protection Equipment (RPE) market covers a wide array of products designed to safeguard individuals from inhaling harmful substances in various occupational environments. This market is driven by stringent workplace safety regulations, growing awareness regarding the health risks associated with respiratory hazards, and increasing industrialization across sectors such as manufacturing, construction, healthcare, and mining. Additionally, heightened awareness among workers regarding the long-term health consequences of exposure to hazardous substances is driving demand for RPE. Individuals are becoming more proactive in protecting themselves from respiratory ailments such as lung diseases, asthma, and occupational lung cancers, thereby fueling the adoption of respiratory protective equipment. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Respiratory Protection Equipment Market Dynamics:

Empowering Workers through Respiratory Protection

Stringent workplace regulations, such as those enforced by the Occupational Safety and Health Administration (OSHA) in the United States, mandate the use of respiratory protection in environments with hazardous airborne contaminants, stimulating demand for RPE. Additionally, rapid industrialization across sectors like manufacturing, construction, and mining necessitates respiratory protection for workers exposed to airborne pollutants, further fueling market growth. Heightened awareness among workers about the long-term health consequences of respiratory hazards also contributes to market growth, as individuals prioritize respiratory protection to mitigate risks. Technological advancements in RPE, including improved filtration systems and ergonomic designs, enhance user comfort and safety, driving demand for innovative respiratory protective equipment.

The global pandemics, such as COVID-19, have heightened awareness of respiratory hygiene and driven a surge in demand for respiratory masks and respirators, both in healthcare settings and across various industries. Initiatives promoting occupational health and safety standards, emerging healthcare challenges, environmental concerns regarding air quality, worker empowerment programs, and continued investments in research and development further propel market growth for respiratory protection equipment. These factors underscore the importance of respiratory protection in various occupational settings and drive the ongoing growth of the Respiratory Protection Equipment Market. Misuse and Non-Compliance Risks in RPE Usage are restraining Respiratory Protection Equipment Market Demand

Misuse and Non-Compliance Risks in RPE Usage are restraining Respiratory Protection Equipment Market Demand

The significant challenge is the cost associated with acquiring and maintaining respiratory protection equipment. For small businesses with limited financial resources, the high initial investment required to purchase specialized respirators and conduct fit-testing procedures can be prohibitive. Additionally, ongoing expenses for replacement filters, maintenance, and training add to the overall cost burden, further hindering market growth, particularly in sectors with tight budgets or fluctuating economic conditions.

Another critical challenge revolves around comfort and compliance issues. Workers may resist wearing respiratory protective equipment if it causes discomfort or interferes with their ability to perform tasks efficiently. Ill-fitting respirators, in particular, can lead to non-compliance and compromise worker safety. For instance, workers in hot and humid environments may find wearing respiratory masks uncomfortable, leading to improper usage or even refusal to wear them altogether, posing significant challenges to market growth.

Furthermore, the need for proper training and education presents a considerable hurdle in maximizing the effectiveness of respiratory protection equipment. Ensuring that workers receive comprehensive instruction on respirator selection, fitting, and maintenance is essential for mitigating risks effectively. However, inadequate training programs or lack of awareness about correct usage procedures can undermine the efficacy of RPE. Industries with high turnover rates or transient workforces struggle to maintain consistent training protocols, exacerbating this challenge and impeding Respiratory Protection Equipment Market growth.

Fit testing and seal verification procedures are also critical yet time-consuming aspects of respiratory protection. Ensuring the proper fit and seal of respirators is vital for their effectiveness in safeguarding against airborne hazards. However, scheduling and conducting fit testing for large numbers of employees can be logistically challenging, particularly in industries with diverse workforce sizes and shifts. Delays or gaps in fit testing procedures can compromise worker safety and hinder market growth by eroding trust in respiratory protection programs. Supply chain disruptions represent another significant challenge for the RPE market.

Disruptions such as material shortages, transportation delays, or geopolitical tensions can impact the availability of respiratory protection equipment. For instance, the COVID-19 pandemic caused global supply chain disruptions, leading to shortages of N95 respirators and other critical PPE items. These disruptions not only strain the availability of respiratory protection equipment but also undermine confidence in the market's ability to meet demand during crises, posing challenges to Respiratory Protection Equipment Market growth.

Navigating complex regulatory compliance requirements presents additional hurdles for manufacturers and end-users of respiratory protection equipment. With evolving standards and varying requirements across regions, ensuring compliance can be a daunting task. Compliance complexity increases administrative burdens and may lead to confusion or compliance gaps, hindering market growth due to uncertainty and regulatory risks. Misuse and non-compliance with respiratory protection protocols pose significant challenges to the effectiveness of RPE. Instances of improper use, such as wearing respirators incorrectly or failing to perform seal checks, can compromise worker safety and erode trust in respiratory protection programs.

Resistance or reluctance among workers to adhere to safety protocols due to perceived discomfort or inconvenience further exacerbates this challenge, hindering market growth in industries where social norms influence behaviour. Moreover, the limited availability of specialized respiratory protection equipment tailored to specific hazards or environments presents challenges for end-users seeking adequate protection solutions. Industries with unique respiratory hazards may struggle to find suitable equipment options, limiting their ability to address specific workplace risks effectively and restricting Respiratory Protection Equipment Market growth.

Surge in Healthcare Demand Fuels Respiratory Protection Equipment Market Growth

The expansion of the healthcare sector, especially in light of the COVID-19 pandemic, has led to increased demand for respiratory masks and respirators to protect frontline workers from airborne pathogens. Technological advancements play a crucial role in enhancing the effectiveness and usability of respiratory protection equipment, with innovations such as improved filtration systems and ergonomic designs driving market expansion. Additionally, emerging applications in aerospace and defence sectors, where workers face exposure to airborne contaminants during maintenance operations, offer new avenues for growth. Focus on worker comfort and compliance, coupled with the rising adoption of industrial hygiene practices, presents opportunities for manufacturers to develop more user-friendly and effective respiratory protection solutions.

Furthermore, the growing emphasis on sustainability and environmental impact encourages the development of eco-friendly respiratory protective equipment, catering to environmentally conscious consumers and industries. Global regulatory harmonization facilitates market access and promotes innovation, while the increasing demand for personalized protection solutions drives customization and diversification in the market. Expansion in emerging markets, particularly in Asia-Pacific regions, offers significant growth potential as industrial sectors continue to evolve and prioritize occupational health and safety. The integration of smart technologies such as sensors and data analytics into respiratory protection equipment enhances situational awareness and safety, driving adoption in industries where real-time monitoring is essential. Collectively, these growth opportunities underscore the dynamic nature of the Respiratory Protection Equipment Market and the potential for innovation and expansion in meeting evolving respiratory protection needs across diverse industries.

Respiratory Protection Equipment Market Segment Analysis:

Based on the product type segment, the air-purifying respirators segment is estimated to hold the largest market share in 2024. High development mainly attributed to the increasing demand for disposable respirators in the healthcare & and pharmaceuticals industry. The increasing number of surgical workforce in hospitals globally is expected to drive the market for air-purifying respirators during the forecast period. The air-purifying respirators segment is poised to dominate the market during the forecast period, primarily due to the surging demand for disposable respirators within the healthcare and pharmaceutical industries. The rising number of surgical procedures worldwide is a key driver propelling the market for air-purifying respirators.

Hospitals globally are witnessing an increase in their surgical workforce, necessitating respiratory protection for healthcare workers during procedures to mitigate the risk of exposure to airborne pathogens and contaminants. In the healthcare and pharmaceutical sectors, where stringent infection control measures are paramount, disposable respirators offer a convenient and effective solution for protecting workers against airborne hazards. The ease of use and disposal associated with disposable respirators make them highly preferred among healthcare professionals, driving significant market demand.

Additionally, the ongoing COVID-19 pandemic has further intensified the need for respiratory protection in healthcare settings, further bolstering the demand for air-purifying respirators. The increasing emphasis on infection control, coupled with the rising number of surgical procedures and healthcare personnel globally, positions the air-purifying respirators segment as a leading contender in the respiratory protection equipment market during the forecast period.

Competitive Landscape:

On May 5, 2022, Honeywell revealed two new NIOSH-certified respiratory offerings aimed at meeting the demands of healthcare workers. The DC365 Small Surgical N95 Respirator, designed as the next-generation surgical N95 respirator, addresses the needs of frontline workers with smaller facial features, ensuring a secure fit and enhanced safety. This expansion of Honeywell's PPE portfolio aims to address challenges, particularly affecting women in the healthcare industry. Additionally, the RU8500X series half-mask respirator provides heightened filtration efficiency, a secure fit, and breathing comfort for extended wear during long shifts in clinical settings. Featuring a filtered exhalation valve and HEPA P100 filter, this reusable respirator offers high-performing protection (99.9%) and source control, benefitting both the wearer and those in their vicinity.

On December 6, 2023, A contract worth $35 million was awarded to MSA by the U.S. Air Force. The agreement aims to equip air-base fire brigades with advanced respiratory protective equipment. Under this contract, MSA will supply its G1 Self-Contained Breathing Apparatus (SCBA) model, along with associated facepieces, chemical warfare component (CWC) masks, and supplied air respirator (SAR) kits. These units replace older model MSA air masks and will be utilized by U.S. Air Force fire brigades stationed at various air bases worldwide. This initiative underscores the Air Force's commitment to ensuring the safety and preparedness of its personnel operating in potentially hazardous environments.

Scope of the Global Respiratory Protection Equipment Market: Inquire before buying

| Global Respiratory Protection Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 16.19 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.5% | Market Size in 2032: | US $ 25.16 Bn. |

| Segments Covered: | by Product Type | Air-purifying Respirators (APRs) Atmosphere-supplying Respirators (ASRs) |

|

| by End User | Healthcare & Pharmaceuticals Defense & Public Safety Services Oil & Gas Manufacturing Mining Construction Others |

||

Respiratory Protection Equipment Market, By Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Respiratory Protection Equipment Market Key Players are:

Leading Respiratory Protection Equipment Manufacturers in the North America:

1. 3M Company (United States)

2. Honeywell International Inc. (United States)

3. MSA Safety Incorporated (United States)

4. Kimberly-Clark Corporation (United States)

5. Alpha Pro Tech, Ltd. (United States)

6. Bullard (United States)

7. Moldex-Metric, Inc. (United States)

8. Gentex Corporation (United States)

9. Mine Safety Appliances Company (United States)

10. Prestige Ameritech (United States)

11. RPB Safety LLC (United States)

12. Lakeland Industries, Inc. (United States)

Top Respiratory Protection Equipment Providers in Europe:

1. Delta Plus Group (France)

2. Sundström Safety AB (Sweden)

3. Respro (United Kingdom)

4. Avon Rubber p.l.c. (United Kingdom)

5. Drägerwerk AG & Co. KGaA (Germany)

6. uvex group (Germany)

Major Respiratory Protection Equipment Market Players in Asia-Pacific:

1. Ansell Limited (Australia)

2. Venus Safety & Health Pvt. Ltd. (India)

FAQs:

1. What are the growth drivers for the Respiratory Protection Equipment market?

Ans. Increasing consumer awareness and demand for healthier options drive the growth of the Respiratory Protection Equipment market. Rising prevalence of diseases and lifestyle-related health concerns fuels the demand for Respiratory Protection Equipment market.

2. What are the major restraints for the Respiratory Protection Equipment market growth?

Ans. Price sensitivity among consumers may limit the market penetration of Respiratory Protection Equipments due to their higher cost compared to other options. Regulatory hurdles may pose challenges for manufacturers in terms of compliance and product claims substantiation, potentially slowing market growth.

3. Which region is expected to lead the global Respiratory Protection Equipment market during the forecast period?

Ans. North America is expected to lead the global Respiratory Protection Equipment market during the forecast period. North America's well-established healthcare infrastructure, high consumer awareness, aging population, favorable regulations, and presence of key market players contribute to its expected leadership in the global Respiratory Protection Equipment market.

4. What is the projected market size and growth rate of the Respiratory Protection Equipment Market?

Ans. The Respiratory Protection Equipment Market size was valued at USD 16.19 Billion in 2025 and the total Respiratory Protection Equipment revenue is expected to grow at a CAGR of 6.5% from 2026 to 2032, reaching nearly USD 25.16 Billion by 2032.

5. What segments are covered in the Respiratory Protection Equipment Market report?

Ans. The segments covered in the Respiratory Protection Equipment market report are Product type, end user, and Region.