Polyurethane Foam Market Size by Foam Type, Density Composition, Application, End-Use, and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

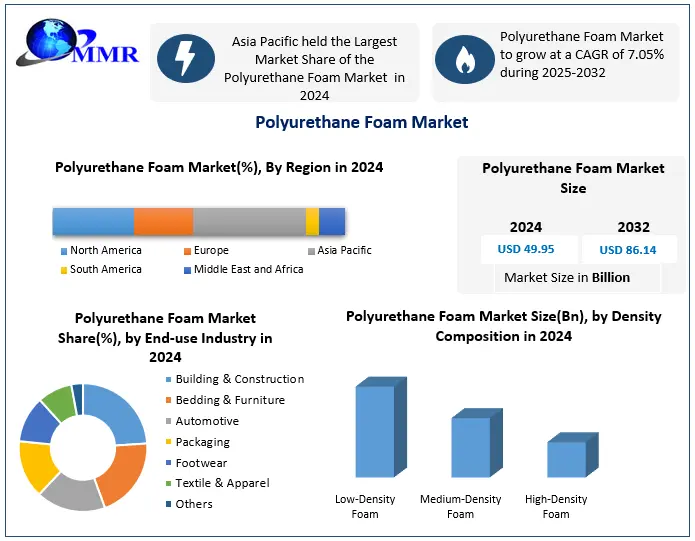

Global Polyurethane Foam Market size was valued at USD 49.95 Bn. in 2024, and the total Polyurethane Foam Market revenue is expected to grow by 7.05% from 2025 to 2032, reaching nearly USD 86.14 Bn.

Polyurethane Foam Market Overview:

Polyurethane foam is a versatile polymer material produced through the reaction of polyols and isocyanates, resulting in a lightweight, durable, and flexible foam. It is widely valued for its properties such as insulation, cushioning, sealing, and molded structural support.It is used in upholstery, mattresses, automotive interiors, building insulation, packaging, and appliances. Like many industrial materials, polyurethane foam has evolved from rigid and flexible foams made of petroleum to rigid flex foams, to custom-made product offerings such as bio-based foams, flame-retardant foams, high-resilience foams, spray foams, etc. the global Polyurethane Foam market has continued to grow and extend beyond expectations at this point, driven by urbanization, green building codes, the adoption of electric vehicles, and the need for energy-efficient thermal insulation performance. For example, spray polyurethane foam (SPF) is increasing in acceptance and popularity for both residential and commercial insulation, while flexible foam has strong demand in the Asia-Pacific region, which continues to grow in a rising economy with higher disposable incomes and housing.

The MMR report provides a comprehensive analysis of the primary growth drivers in the market to include sustainability initiatives, growth in the construction and automotive industries, government legislation regarding energy efficiency, and advancements and innovations in foam chemistry. The report explores the major market segments divided into foam by Foam type, material, foam by density, Application, and end-user industry. Some of the leading companies operating in the global polyurethane foam market include BASF SE, Dow Inc., Covestro AG, Wanhua Chemical Group, and Sekisui Chemical. These companies all dedicate investment to bio-based feedstocks, chemical recycling, and high-performance foams to accommodate the demand for more advanced Density Compositions. The report provides evidence that low-carbon PU formulations, circular economy, and lightweight foams for electric vehicles are three trends emerging in the space that are developing a new future for polyurethane foam around the globe. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Polyurethane Foam Market Dynamics

Increasing Demand for Sustainable Building Insulation to Drive the Polyurethane Foam Market Growth

The global energy crisis has driven the accelerated development of green buildings and sustainable construction projects, bringing sustainability to the forefront of the building development agenda. This encompasses a spectrum of procedures crucial during major construction stages, given their substantial environmental impact. Driven by increased investments in smart, energy-efficient commercial and residential structures, green buildings are making a prominent entrance into the construction market. Beyond offering financial prospects, these buildings align with environmental and federal requirements, addressing the escalating consumer demands for sustainability. The heightened efficiency of building materials has amplified the need for effective insulation materials to manage heating, ventilation, and air conditioning (HVAC) and curtail energy losses resulting from inadequate insulation.

Polyurethane (PU) foams have emerged as highly efficient insulation materials, yielding substantial energy savings. The use of PU adhesives in home frames, complemented by mechanical fasteners, provides robust resilience during extreme weather events. Manufacturers like NCFI Polyurethane showcase the Density Composition of their closed-cell spray polyurethane foam (ccSPF) as both an insulator and exterior material. This Density Composition, endorsed by community developers, builders, and homeowners, enhances homes' ability to withstand the impacts of high winds, storm surge, and flooding. These advancements are poised to contribute significantly to the growth of the Polyurethane Foam Market in the forecast period.

Increasing Demand for Lightweight and High-Performance Composites from the Automotive Industry to Drive Polyurethane Foam Market The adoption of thermoplastic polyurethane (TPU) in car components has revolutionized the automotive industry by significantly reducing the overall weight of vehicles. This intentional weight reduction, aimed at curbing fuel consumption and minimizing carbon emissions, has sparked a surging demand for plastics within the automotive sector. Polyurethane (PU), serving as a versatile alternative to metal, is extensively utilized in diverse automotive Density Compositions, including seats, instrument panels, exterior panels, engine encapsulation, and cables. The burgeoning growth of the automotive sector, propelled by rising income levels and industrialization, is poised to exert a positive influence on the global Polyurethane Foam Market. The diminished vehicle weight not only contributes to a reduction in carbon emissions but also enhances crucial aspects of vehicle performance, such as handling and acceleration.

Raw Material Price Volatility to Limit the Polyurethane Foam Industry Growth

Polyurethane, a versatile material, is meticulously crafted from key ingredients such as methylene diphenyl diisocyanate (MDI), toluene diisocyanate (TDI), and polyester and polyether polyols. MDI and TDI emerge as dominant players in the isocyanate landscape, owing to their cost-effectiveness when compared to alternatives like bi-tolylene diisocyanate and 1,5 naphthalene diisocyanate. This dominance positions MDI and TDI as pivotal drivers propelling the growth of the Polyurethane Foam Market throughout the forecast period. The global petrochemical landscape has encountered the impact of depleting crude oil supplies and unrest in the Middle East, leading to substantial fluctuations in prices. This market imbalance, coupled with erratic demand, has notably affected MDI and TDI, given their status as petrochemical derivatives crucial for polyurethane production.

The unfolding crisis in Eastern Europe had a significant influence on crude oil and derivatives prices, thereby leaving a discernible imprint on market share dynamics. the Organization for Economic Cooperation and Development (OECD) countries, responding to the crisis, have released 60 million barrels of oil from their reserves to alleviate price pressure. Sanctions imposed on Russia by major nations have further tightened the global crude oil supply, resulting in a surge in barrel prices. The anticipated impact on crude oil prices is expected to be limited and short-term due to the inherent risk of replenishment, which adds complexity to the ongoing price rise situation in the petrochemical domain.

Growing Environmental Concerns to Hamper the Growth of the Polyurethane Foam Market

Manufacturers in the Polyurethane Foam Market are grappling with substantial challenges, primarily stemming from toxic gas emissions associated with burning fossil fuels, which directly impact their industry standing. The production of petrochemical goods derived from crude oil significantly contributes to harmful gas emissions, escalating greenhouse gas concentrations, and amplifying the carbon footprint. the raw materials crucial for manufacturing polyurethane (PU), including TDI and MDI, present environmental risks. Leading nations such as the United States, Canada, the United Kingdom, and Germany have successfully curtailed carbon emissions through robust government environmental regulations. The industrial release of TDI compounds this challenge, leading to air pollution and exerting an impact on the market share of petrochemical manufacturers, especially in light of the growing prominence of environmental sustainability concerns.

TDI levels have undergone scrutiny by Environment Canada and Health Canada, revealing potential risks to human health. In response, Environment Canada has issued a Pollution Prevention (P2) Planning Notice to ensure adequate environmental management in case of TDI leaks. Regulatory bodies in the United States and Europe have implemented diverse regulations and directives to address these concerns. Notably, Europe has banned the disposal of waste tires and PU products in landfills, strategically aiming to harness the extensive potential of PU as an energy source comparable to coal while simultaneously mitigating environmental harm.

Growing Shift Toward Bio-based Polyurethane Over Petrochemical Alternatives to Create Opportunities in the Polyurethane Foam Market

Increasing concerns over the harmful effects of petrochemicals and the depletion of crude oil reserves are actively shaping market dynamics, giving rise to bio-based polymers like bio-based polyurethane. Stringent regulations in various countries, especially those prohibiting the use of petroleum-based plastics in specific Density Compositions like medical devices, are expected to fuel the market growth of bio-based polyurethane throughout the forecast period. The dominance of North America, Europe, and Asia Pacific in global bioplastic material production is set to drive the adoption of environmentally friendly polymers across diverse industries such as automotive, construction, packaging, consumer goods, and medical. This surge in demand for bio-based polyurethane is poised to positively influence market share dynamics and bolster the overall growth of the Polyurethane Foam Market.

The global concern over the utilization of petroleum-based plastics has ignited the demand for alternative materials, leading to a transformation in polyurethane foam market share dynamics. Manufacturers in the industry are now redirecting their focus toward the development of bioplastics, leveraging a rapid pace of innovation and new product development. Bio-based polyurethane is gaining significant traction across various sectors, including electrical and electronics, medical devices, construction, automotive, and consumer products. Its regulated breakdown qualities, both biotic and abiotic, along with shape memory behavior, make it suitable for Density Compositions in the biomedical sector, further contributing to the growing market share of bio-based polyurethane in the evolving landscape of sustainable materials.

Global Polyurethane Foam Market Segment Analysis

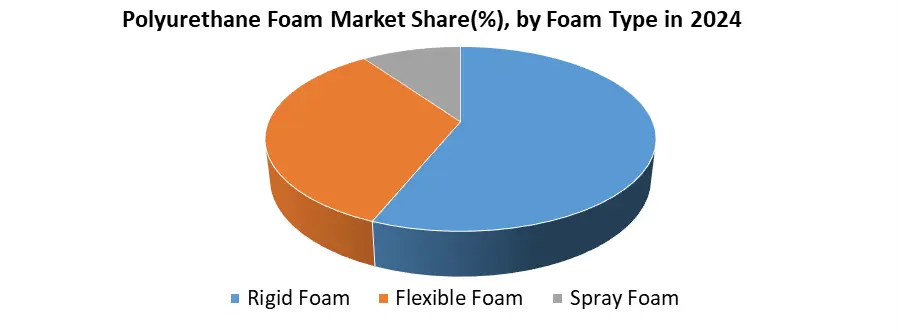

Based on Foam Type, the rigid segment dominated the polyurethane foam market in 2024. Rigid PU foams are high-performance closed-cell polymers that are used in end-use sectors such as transportation, packaging, and industrial insulation and appliances because of their structural stability, which allows producers to build thermally insulating goods. Rigid foams provide superior sound insulation, mechanical strength, and heat resistance, making them ideal for extreme weather and tough situations. Because of the boom in industrialization, China, India, and Indonesia dominate the Asia Pacific (APAC) market for stiff PU foams. The growth of the construction and furniture industries, as well as the presence of major automobile OEMs, is a significant factor propelling the rigid foam market in APAC. Government assistance to weatherize low-income houses and satisfy transitional criteria for green buildings is expected to push rigid PU foam demand in insulation Density Compositions even further. Based on the End-Use Industry, The Building & Construction segment is expected to dominate the Polyurethane Foam Market in 2024, driven by the widespread use of polyurethane foam in insulation, roofing, sealants, and energy-efficient building materials. The Bedding & Furniture industry follows closely, supported by growing demand for mattresses, cushions, and upholstered furniture. The Automotive sector also holds a significant share as polyurethane foam is widely utilized for seating, interior components, and noise insulation. Packaging is emerging as a fast-growing segment due to its lightweight, protective, and shock-absorbing properties. Meanwhile, the Footwear and Textile & Apparel industries contribute moderately to the market, with polyurethane foams being used in shoe soles, padding, and performance wear. Other industries, such as healthcare, electronics, and specialty applications, also provide incremental growth opportunities, further broadening the market scope.

Based on the End-Use Industry, The Building & Construction segment is expected to dominate the Polyurethane Foam Market in 2024, driven by the widespread use of polyurethane foam in insulation, roofing, sealants, and energy-efficient building materials. The Bedding & Furniture industry follows closely, supported by growing demand for mattresses, cushions, and upholstered furniture. The Automotive sector also holds a significant share as polyurethane foam is widely utilized for seating, interior components, and noise insulation. Packaging is emerging as a fast-growing segment due to its lightweight, protective, and shock-absorbing properties. Meanwhile, the Footwear and Textile & Apparel industries contribute moderately to the market, with polyurethane foams being used in shoe soles, padding, and performance wear. Other industries, such as healthcare, electronics, and specialty applications, also provide incremental growth opportunities, further broadening the market scope.

Polyurethane Foam Market Regional Insights

Asia Pacific dominated the Polyurethane Foam Market in the year 2024, capturing a substantial market share of xx% in total value, signifying the region's significant market penetration. The driving forces propelling the industry's growth in this area encompass a thriving automotive sector, increased PU utilization in construction and packaging, and the recovery of the automobile industry in growing economies like the United States and Germany. The escalating demand for lightweight materials in the automotive sector is a key contributor to the rising use of polyurethane, impacting both Polyurethane Foam market prices and overall market share dynamics. North America and Europe are expected to experience moderate growth rates of 3.4% and 3.0%, respectively.

The demand from key sectors such as automotive, electronics and appliances, packaging, and construction in emerging nations like China and India. The region benefits from a vast supply of cost-effective, trained labor and easy access to land, contributing to favorable Polyurethane Foam market share dynamics. Anticipated is a shift in the manufacturing landscape towards developing economies, particularly China and India, positively influencing the Polyurethane Foam Market growth over the forecast period. The construction, automotive, electronics, and other rapidly growing industries in the region offer significant growth potential for PU manufacturers, impacting both Polyurethane Foam market prices and overall market share. Flexible foam, used in various consumer and commercial Density Compositions such as furniture, mattresses, carpet cushions, fibers, and fabrics, is gaining prominence due to increased consumer awareness of the sustainability of lightweight and cost-effective PU. Rising construction investments, driven by the growing demand for sustainable infrastructure, coupled with increased demand for furniture and bedding items, are expected to boost product demand and impact market prices.

North America holds a substantial share of the global polyurethane foam market and is set to grow rapidly throughout the forecast period. The growth of key end-use sectors like construction and automotive, coupled with the adaptability of PU in new Density Compositions owing to its sustainability and lightweight features, is expected to fuel market growth. The increasing acceptance of TPU in critical end-use sectors like footwear, industrial machinery, automotive, electronics, and medical further contributes to this trend, influencing market share dynamics and overall market prices. The construction sector in North America is poised for significant growth due to the rising demand for non-residential projects like hospitals, commercial buildings, and colleges. Government initiatives supporting the housing sector's recovery are expected to positively impact future building patterns. Reconstruction efforts in the United States and infrastructure development in Canada and Mexico, driven by rising industrialization, are likely to generate substantial market potential for polyurethane foam in North America during the forecast period. This potential is expected to influence both market prices and market share dynamics in the region.

Polyurethane Foam Market Competitive Landscape

The Polyurethane Foam Market is fostering advancements among global chemical and material science companies, leading to multiple innovations across industries such as construction, automotive, furniture, and electronics.. Key players such as BASF SE and Dow Inc. have progressed quickly, particularly with respect to product development and sustainability. In 2024, BASF SE (Germany) reported approximately USD 8.5 billion in its Performance Materials segment and grew due to its biomass-balanced Elastoflex® foam systems, and also, low-emission insulation materials for appliances and EVs etc. In 2024, Dow Inc. (USA) reported around USD 5.2 billion in revenues from its Consumer Solutions segment for polyurethanes supported by its launch of VORANOL™ WK5750 polyol and the increase of overall production and investments at its plant in Freeport. Both companies are continuing to develop and invest in circular solutions including chemical recycling and carbon footprint reduction technologies, and these companies, along with others in the polyurethane market, are continuing to emphasize sustainability and circular commitments as the market becomes more and more affected by ESG commits and need for high-performance Density Compositions.

Polyurethane Foam Market Recent Development

• on March 27, 2025 ,BASF SE (Germany) announced, the introduction of a new biomass balance flexible polyurethane foam systems for the North American furniture industry within its Elastoflex family of products with the promise of up to 75% reduction of product carbon footprint when compared to traditional flexible foam systems.

• On December 12, 2024, Dow Inc. (USA) began production at its Freeport plant of the VORANOL™ WK5750 advanced polyether polyol for premium mattresses and furniture foams that provide superior softness, resilience, and purity.

• In January 2025, at COP29, Wanhua Chemical Group (China) introduced to the global attendees its alcoholysis recycling technology for polyurethane foam (up to 30 % polyol recovery, no degradation), clearly garnering noteworthy international attention.

• January 21, 2025, Covestro officially launched the Desmopan FLY thermoplastic polyurethane series in early 2025. This material is specifically engineered for supercritical fluid (SCF) injection foaming, enabling lightweight, high-performance, and recyclable midsoles (e.g., in footwear). It delivers fine-cell foam structure with superior cushioning, energy return, and durability with no chemical blowing agents—supporting circular economy goals.

Polyurethane Foam Market Recent Trends

| Category | Key Trend | Example Product | Market Impact |

| Sustainability | Shift toward bio-based and low-carbon PU foam formulations | BASF Elastoflex E 3496/103 (biomass-balanced foam system) | Supports decarbonization goals and improves appeal to eco-conscious manufacturers and consumers |

| Recycling Innovation | Development of chemical recycling technologies for used PU foam | Wanhua Alcoholysis Recycling Process | Enables circular economy in foam markets and helps meet global ESG mandates |

| High-Performance Foams | Demand for foams with better thermal, acoustic, and flame-retardant properties | Covestro's Baytherm Microcell Foam (for automotive and appliances) | Expands use in electric vehicles and energy-efficient construction |

Polyurethane Foam Market Scope: Inquire before buying

| Polyurethane Foam Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 49.95 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 7.05% | Market Size in 2032: | USD 86.14 Bn. |

| Segments Covered: | by Foam Type | Rigid Flexible Spray |

|

| by Material | MDI (Methylene Diphenyl Diisocyanate) Based Foam TDI (Toluene Diisocyanate) Based Foam Others |

||

| by Density Composition | High-Density Medium-Density Low-Density |

||

| by Application | Coatings & Adhesives Cushioning Insulation Others |

||

| by End Use Industry | Packaging Building & Construction Automotive Footwear Bedding & Furniture Textile & Apparel Others |

||

Polyurethane Foam Market by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Philippines,

Thailand, Vietnam, Rest of Asia Pacific)

Middle East and Africa (MEA) (South Africa, GCC, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Polyurethane Foam Market Key Players:

North America

1. Dow Inc. (USA)

2. Huntsman Corporation (USA)

3. Chemtura Corporation (now part of LANXESS) (USA)

4. DuPont (USA)

5. Cargill, Inc. (U.S.)

6. MCPU Polymer Engineering LLC (U.S.)

7. Rogers Corporation (USA)

8. Eastman Chemical Company (USA)

9. RTP Company (USA)

10. The Lubrizol Corporation (USA)

11. RAMPF Holding GmbH & Co. KG (USA branch, HQ in Germany)

12. Huntsman International LLC (U.S.)

13. Sinomax USA (U.S.)

Europe

1. Covestro AG (Germany)

2. BASF SE (Germany)

3. Bayer AG (Germany)

4. Saint-Gobain (France)

5. Recticel NV/SA (Belgium)

Asia Pacific

1. Wanhua Chemical Group Co. Ltd. (China)

2. Sekisui Chemical Co., Ltd. (Japan)

3. Tosoh Corporation (Japan)

4. Mitsui Chemicals (Japan)

5. DIC Corporation (Japan)

6. Mitsubishi Chemical Holdings (Japan)

7. INOAC Corporation (Japan)

8. Teijin Limited (Japan)

9. Toray Industries Inc. (Japan)

10. Miracll Chemicals Co. Ltd (China)

11. Foamindo Industri Uretan (Indonesia)

Frequently Asked Questions:

1] What segments are covered in the Global Polyurethane Foam Market report?

Ans. The segments covered in the Polyurethane Foam Market report are based on Foam Type, Material, Density Composition, Application, End Use Industry, and Region.

2] Which region is expected to hold the largest share of the Global Polyurethane Foam Market?

Ans. The Asia Pacific region is expected to hold the largest share of the Polyurethane Foam Market. The growth of the construction and furniture industries in China, India, Indonesia, etc., as well as the presence of major automobile OEMs, is a significant factor propelling the rigid foam market in APAC.

3] What is the market size of the Global Polyurethane Foam Market by 2030?

Ans. The market size of the Polyurethane Foam Market by 2032 is expected to reach USD 86.14 Bn.

4] What is the forecast period for the Global Polyurethane Foam Market?

Ans. The forecast period for the Polyurethane Foam Market is 2025-2032.

5] What was the market size of the Global Polyurethane Foam Market in 2024?

Ans. The market size of the Polyurethane Foam Market in 2024 was valued at USD 49.95 Bn.