Point of care diagnostics Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

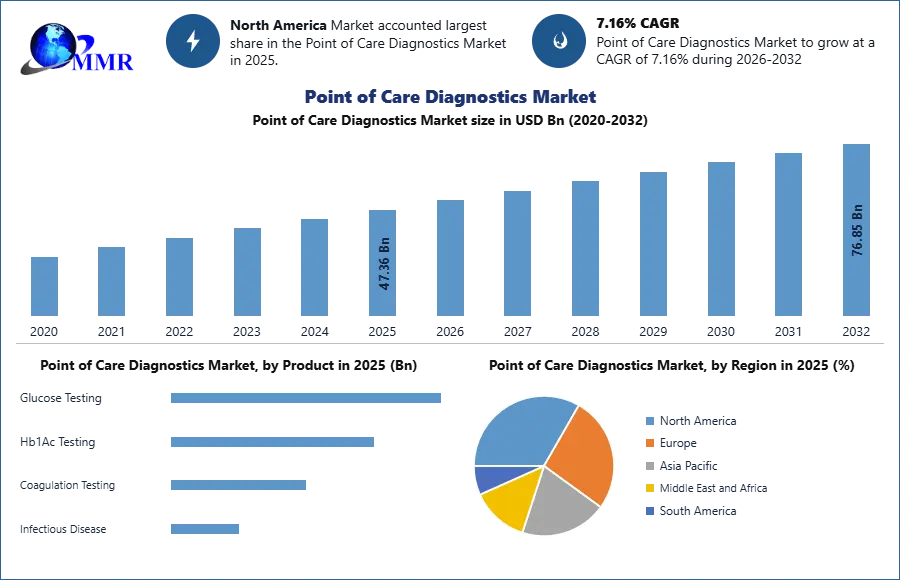

Point of care diagnostics Market was valued at USD 47.36 Bn in 2025. Global Point of care diagnostics Market size is expected to grow at a CAGR of 7.16% through the forecast period.

Point of care diagnostics Market Overview:

Point of care testing (POCT) is described as medical diagnostic testing at or point of care that is, at overall setting of patient consideration. The motivation behind POCT is to give immediate data to doctors about the patient's condition. POCT is a significant symptomatic device utilized in different areas in the medical clinic like the emergency unit, the operating room (OR), and the emergency division (ED). The market development is principally ascribed to increment in predominance of infectious disease, product development and dispatches, and rise in number of CLIA-deferred POC tests. The point of care diagnostics market is probably going to develop with the presentation of new items into the market, pointed toward conveying modest consideration at the offices situated at the nearest potential good ways from the patients' area. New advancements or items are being refined and improved to convey more straightforward to involve gadgets with gradual upgrades in logical execution. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

2025 is considered as a base year to forecast the market from 2026 to 2032. 2025’s market size is estimated on real numbers and outputs of the key players and major players across the globe. Past five years trends are considered while forecasting the market through 2032.

Point of care diagnostics Market Dynamics:

Market Drivers:

The coordination of computerized advancements is supposed to display a strong effect on the extension of POC arrangements in restricted asset settings. Expanding utilization of telehealth as new ordinary is a basic go-to-showcase technique for POCT players. According to the U.S. Places for Disease Control and Prevention, around 95% of wellbeing focuses in the U.S. given telehealth administrations during the pandemic. In this manner, the extension point of care, for example, PixCell Medical, a POC innovation for CBC tests, will positively influence the market development during the forecast period.

The rising significance of POC diagnostics in natural observing and general wellbeing additionally requests the coordination of advancements that work with simple systems administration, further making it helpful for medical services experts to decipher test results precisely. Organizations are creating reasonable POC with high particularity and awareness. Place of Care Diagnostics Market GrowthTrends is the ascent in the commonness of chronic disease in generating revenue. The commonness of ongoing illnesses, like diabetes, stiffness, or disease, is expanding worldwide, because of different reasons, for example, an expansion in the geriatric populace, stationary ways of life, undesirable food propensities, and natural variables. For example, chronic diseases kill many individuals every year, worldwide. Cardiovascular illnesses represent most constant sickness passings, yearly, trailed by tumors, respiratory infections, and diabetes. Techniques in microfabrication and microfluidics have advanced such a huge amount over the most recently that POC gadgets can be created for minimal price, are not difficult to utilize, versatile, and can produce fast outcomes. There are many exploration exercises on-going in the field of microfluidics innovation.

Market Restraints:

Despite the fact that rapid test kit units are exceptionally effective and exact they need to accomplish government approvals for commercialization and general use in medical care facilities. These administrative bodies have severe standards and to this end it takes more time for organizations to get approvals for their products and consequently restrain the general point of care diagnostics market development. The pricing pressure because of reimbursement cuts and absence of adequate spending plans restrain the development of the POC diagnostics market.

POC test results need legitimate arrangement with focal lab techniques because of an enormous number of pre-and post-scientific errors. Pre-scientific errors for POC testing include unsuitable indications for the performance of the test, improper sampling times and procedures, absence of data about understanding circumstances, and different factors like fasting before tests or variation in pose/position during comparative tests. Also, post-scientific mistakes incorporate lacking specialized approval, misleading task of results, and errors in information capacity.

POC testing is much of the time directed in crisis circumstances to work with fast clinical navigation. Most of the time, these tests are done by medical caretakers or clinical colleagues and not by doctors. Such circumstances can prompt improper request and result documentation. These issues might possibly prompt error findings and influence the nature of care gave to patients. Taking into account such issues, patients and specialists can choose not to select POC testing. This is one of the critical difficulties to the more noteworthy acknowledgment of POC testing. Moreover, there are sure inconveniences related with POC testing over focal lab strategies. These include: No cell-related investigation past fundamental indicative testing is conceivable through POC testing. POC testing gadgets can't distinguish lipemic, hemolyzed, and icteric examples. The expense per test in POC testing is higher than the tests performed on a focal research facility stage. All these factors can contribute to restrain the market development of point of care diagnostics.

Point of care diagnostics Market Segment Analysis:

Based on product, the point of care diagnostic market is segmented into glucose testing, Hb1Ac testing, coagulation testing and infectious disease. The infectious disease segment held the biggest income segment of more than 20.0%. Infectious disease testing has moved from concentrated to decentralized POC testing, bringing about better persistent consideration. The market is being driven by increased interest for fast tests, which has provoked industry players to convey POC answers for decentralized regions. For example, Abbott has presented ID NOW, the world's fastest sub-atomic POC test, which gives COVID-19 discoveries in a short time and is usable in an assortment of decentralized medical services settings like specialists’ workplaces and critical consideration centers.

The glucose testing segment had the second-biggest income share. The high predominance of diabetes, combined with the prerequisite of constant monitoring of glucose levels, is adding to the segment development. The developing predominance of diabetes and the introduction of portable diabetes testing kit will help the segment development during the forecast period. For example, research on the rise of glucose levels in hospitalized patients with local area procured pneumonia expected recording ordinary glucose information .The analysts utilized POC capillary blood glucose testing for checking the glucose in patients.

The cardiac segment may observe huge development during the forecast period. Every year, a huge number of patients report to the hospitals with side effects of a heart failure. Roughly, 31% of all deaths are because of cardiovascular illness. Key Players are evaluating the impending interest and starting product advancement techniques appropriately.

High precision rates related with these markers and the developing prevalence of target infections are a few essential drivers of this segment. Besides, the segment is supposed to observe a fast ascent in the entrance rates in the markets of North America and Europe. The developing geriatric populace and the prevalence of disease inducing way of life habits in these nations will fuel market development over the forecast period.

Based on the end use, the point of care diagnostic market is segmented into clinic, hospitals, homes and labs. The clinic segment dominated the market. Pharmacy and clinic facilities are the significant supporters of the income produced by this segment. Developing admittance to novel symptomatic advancements, further developing medical care, and reasonableness are the key factors that are growing the utilizations of POC diagnostics.

Along these lines, local area drug stores and retail facilities have arisen as potential clinical arrangements that perform such lab tests, particularly with respect to cholesterol and glycosylated hemoglobin (A1C) testing. Further developed medical care openness for the older populace, increased prevalence of infectious disease, and developing stress on conventional centers are key elements adding to market growth. As the reception of POCT increases in the emergency clinics, administrative bodies have regulated the approval/check setting for POC devices. For on-label POCT gadgets, a proper approval isn't needed, however needs to, confirm the accuracy, exactness, and insightful estimation range, among other center boundaries characterized under CLIA.

The home end-use segment will witness the quickest development pace during the forecast period. Home consideration is a worthwhile segment inferable from the expense viability and comfort level of POCT gave to patients at home. POC in the home medical services area likewise engages patients to address medical services difficulties at home and take choices quickly. As the accentuation of medical services is moving toward early recognition and avoidance of sicknesses, the POC diagnostics-based home medical services market is will observe rewarding development during the forecast period.

Regional Insights:

The North America region dominated the market with 40.0 % share in 2025.

The region will continue to keep predominant situation all through the forecast period by virtue of the rapidly increasing infectious diseases alongside the presence of major participants in the U.S. also, Canada. For example, Canada-based Company, bioLytical Laboratories Inc. received CE stamping for the iStatis COVID-19 Antigen Home Test. This will also empower the organization to enter the European market.

The Asia-Pacific region is expected to witness significant growth at a CAGR of 4.7% through the forecast period. The point of care diagnostics market in the Asia Pacific is driven by a rising pool of local diagnostic units and reagents producers around here to offer an extensive variety of testing solutions for the determination of various diseases. The countries are constantly increasing their abilities to support disease testing.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 03 February 2026 | Siemens Healthineers | Partnered with World Athletics to deploy point-of-care testing at global endurance events for real-time athlete health monitoring. | Expands the use of POCT beyond clinical settings into high-performance sports and emergency medicine. |

| 22 January 2026 | Abbott | Reported that its Rapid Diagnostics and Point of Care segments achieved significant international growth, offsetting declines in COVID-related testing. | Demonstrates a market shift toward routine infectious disease and cardiometabolic POC testing in post-pandemic healthcare. |

| 20 January 2026 | Siemens Healthineers | Awarded a $983K grant from the Gates Foundation to develop AI-powered maternal health screening algorithms for portable devices. | Accelerates the development of affordable POC diagnostics for underserved regions and decentralized primary care. |

| 30 July 2025 | BD | Received FDA 510(k) clearance for the BD Veritor™ System for SARS-CoV-2, transitioning the device from emergency use to full regulatory status. | Solidifies the long-term presence of digital POC platforms in physician offices and retail clinics. |

| 29 May 2025 | Danaher | Announced a strategic partnership with AstraZeneca to scale precision medicine diagnostics through its Leica Biosystems and Cepheid units. | Links companion diagnostics directly to therapy selection at the point of care, enhancing oncology treatment workflows. |

| 14 April 2025 | Baebies | Obtained FDA Breakthrough Designation for the first point-of-care heparin monitoring test, providing results in under 15 minutes. | Improves critical care safety by enabling immediate coagulation management at the bedside. |

The objective of the report is to present a comprehensive analysis of the global Point of care diagnostics market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Point of care diagnostics Market dynamic, structure by analyzing the market segments and projecting the Point of care diagnostics Market Market size. Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies, and regional presence in the Point of care diagnostics Market make the report investor’s guide.

Point of care diagnostics Market Scope: Inquire before buying

| Point of Care Diagnostics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 47.36 USD Bn |

| Forecast Period 2026-2032 CAGR: | 7.16% | Market Size in 2032: | 76.85 USD Bn |

| Segments Covered: | by Product | Glucose Testing Hb1Ac Testing Coagulation Testing Infectious Disease |

|

| by End Use | Clinics Hospitals Homes Labs |

||

| by Platform | Lateral Flow Assays Dipsticks Microfluidics Molecular Diagnostics Polymerase Chain Reaction(PCR) Isothermal Nucleic Acid Amplification Technology (INAAT) Other Molecular Diagnostic Technologies Immunoassays |

||

| by Mode of Purchase | Prescription-based Products OTC Products |

||

| by Sample | Blood Urine Nasal and Oropharyngeal Swabs Other Samples |

||

Point of care diagnostics Market by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/ competitors profile covered in brief in Point of Care Diagnostics Market report in strategic perspective

- F. Hoffmann-La Roche Ltd.

- Danaher

- BD

- Qiagen

- Abbott

- Siemens Healthcare AG

- bioMerieux SA

- Zoetis, Inc.

- Thermo Fisher Scientific Inc.

- QuidelOrtho Corporation

- Nova Biomedical

- Chembio Diagnostics, Inc.

- EKF Diagnostics Holdings plc

- Trinity Biotech

- Quest Diagnostics Incorporated

- Sysmex Corporation

- Hologic, Inc.

- Bio-Rad Laboratories, Inc.

- Sekisui Diagnostics

- Nipro Corporation

- Trivitron Healthcare

- Fujirebio Holdings, Inc.

- Fluxergy

- DiaSys Diagnostics

- Mesa Biotech