Plastic Market Size by Product Type, Additives, Resin Types, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

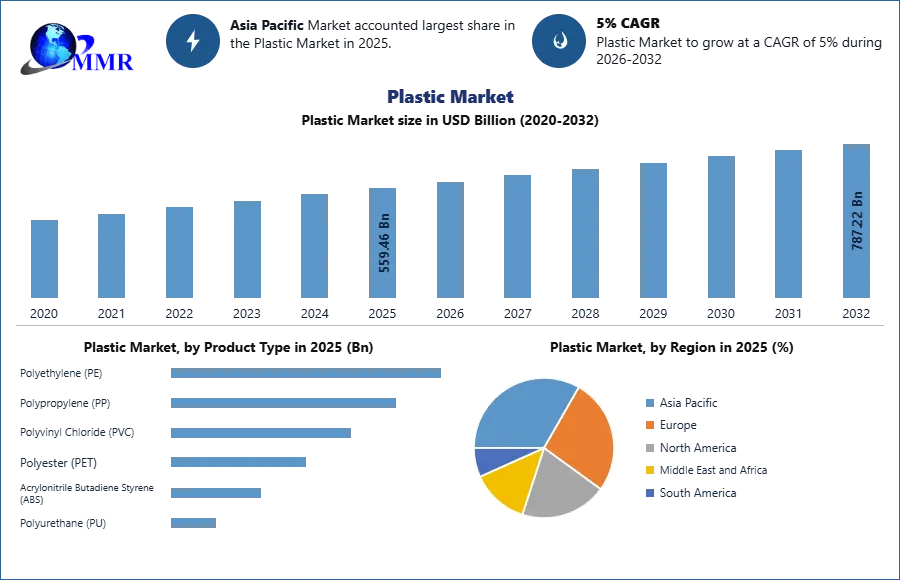

The Plastic Market size was valued at USD 559.46 Billion in 2025 and the total Plastic revenue is expected to grow at a CAGR of 5% from 2026 to 2032, reaching nearly USD 787.22 Billion in 2032.

Plastic Market Overview:

Plastics are synthetic or semi-synthetic materials made from long-chain polymers derived mainly from petrochemicals, though bio-based alternatives have been increasing gradually. Their versatility lightweight, durable, moldable, and cost-efficient made plastics one of the world’s most widely used materials. Global plastic production reached around 400 million tonnes per year, with packaging accounting for 40% of total plastic consumption globally. Commodity plastics such as polyethylene (PE), polypropylene (PP), and PVC historically represented over 70% of total plastic usage due to their low cost and ease of processing. Engineering plastics like ABS and polycarbonate captured about 15–18%, while high-performance polymers such as PEEK and PPS remained below 2–3% of total demand due to their specialized applications.

This report analyzes the Plastic Market as the 2026 Middle East crisis triggers a systemic shock to global petrochemical feedstocks. With the Strait of Hormuz disruption cutting off 25% of global polyethylene and polypropylene exports and driving crude toward $120/bbl, the industry is facing unprecedented force majeure declarations and a 37% spike in resin prices. We explore the strategic shift toward bio-based resins and circular economy models to bypass volatile fossil-fuel dependencies. By evaluating the pivot toward regionalized "security-of-supply" sourcing and lightweighting in the EV sector, this study provides decision-makers with frameworks to navigate a high-inflation landscape where resource autonomy is the new competitive baseline.

To know about the Research Methodology :- Request Free Sample Report

Plastic Market Dynamics:

Sustainability, Material Innovation, Industrial Expansion & Technological Advancements Boosts the Plastic Market Growth

The global Plastic Market is being driven by a combination of industrial expansion, performance-oriented material innovation, and mounting sustainability mandates across economies. Packaging remains the dominant force, accounting for around 40% of total plastic consumption worldwide (EMF). This dominance has strengthened due to the rapid expansion of e-commerce, which has grown by 20%+ annually across major Asian economies such as India, Indonesia, and China. As online retail expands, so does the demand for lightweight plastic films, flexible pouches, bubble packaging, and rigid protective formats making plastics indispensable for last-mile logistics.

The automotive and transportation industries are also major driving sectors. Plastics support substantial lightweighting benefits, enabling 10–15% vehicle weight reduction compared with metallic components. Such weight reduction directly enhances fuel efficiency in conventional vehicles and extends driving range for electric vehicles (EVs). Engineering plastics—including ABS, PC, nylon (PA), PEEK, and PPS—are being increasingly adopted as OEMs transition from metal parts to advanced polymers. This shift has intensified as EV adoption accelerates, pushing manufacturers to integrate lightweight, thermally stable, and durable plastics into battery casings, cable connectors, sensors, and interior components.

The construction sector has emerged as another powerful demand driver. PVC remains one of the most widely used polymers in the sector, accounting for nearly 60% of all global plastic pipe usage. Rapid urbanization in India, China, Bangladesh, Vietnam, and Southeast Asia fuels large-scale demand for plumbing systems, insulation foams, waterproofing membranes, and window profiles. Construction and infrastructure activities collectively account for around 20% of total global polymer consumption, reflecting the critical role plastics play in modern building technologies.

Material innovation also significantly contributes to plastic market momentum. Global production of biodegradable plastics reached 2.2 million tonnes in 2025 and is expected to exceed 6 million tonnes by 2032, driven by regulatory pushes, compostable packaging adoption, and bio-based resin development. High-performance polymers—such as PEEK, PPS, PTFE, fluoropolymers, and advanced nylon grades—are seeing rising use in aerospace, renewable energy, medical implants, surgical devices, and high-temperature electronic components. Their ability to replace metals in extreme-performance environments strengthens long-term growth.

Sustainability pressures remain one of the most powerful driving factors. According to OECD, only around 9% of global plastic waste is recycled, while more than 400 million tonnes of plastic waste are generated each year. This imbalance has forced governments and corporations to enforce strict circular-economy policies. Over 75 countries have enacted bans, restrictions, or taxes on single-use plastics, accelerating demand for recyclable, compostable, and reusable materials.

Global brands—including Coca-Cola, Unilever, PepsiCo, and Nestlé—have committed to 25–50% recycled content in packaging by 2025, making post-consumer recycled (PCR) plastics a high-priority requirement for packaging suppliers. This regulatory and corporate shift toward sustainable plastics continues to reshape demand patterns across industries.

The integration of Industry 4.0 technologies into plastics manufacturing is improving efficiency and strengthening competitiveness. AI-enabled quality monitoring, robotics, and digital simulation tools have allowed manufacturers to reduce material waste by 20–30% in injection molding and extrusion. These technological enhancements strengthen the plastic market by lowering costs, reducing defects, and boosting throughput.

Bioplastics, Recycling Technologies, High-Performance Polymers & Smart Manufacturing Emerging Opportunities in the Global Plastic Market

The plastics industry is entering a transformative phase where sustainability, advanced materials, and manufacturing innovation are creating large-scale opportunities across the global value chain. One of the strongest opportunities lies in bio-based plastics, which currently represent about 1% of total global plastic production—approximately 2.2 million tonnes in 2025 are growing rapidly. With more than 75 countries enforcing bans or taxes on single-use plastics, demand for materials such as PLA, PHA, and bio-PET is expected to multiply. Global consumer brands are targeting 30–60% recyclable or bio-based content by 2032, making bio-resins a high-growth, high-margin segment for producers.

Recycling and circular economy systems represent another major opportunity. With global plastic waste generation surpassing 400 million tonnes annually, and recycling rates hovering below 10%, the plastic market holds vast potential for innovation. Chemical recycling technologies including pyrolysis, depolymerization, and solvent-based recovery can process up to 90% of mixed waste, far more than traditional mechanical recycling systems. As FMCG brands and retailers commit to 50–100% recyclable or reusable packaging, demand is quickly rising for high-purity PCR materials, food-grade rPET, and advanced recycled polypropylene.

High-value sectors such as aerospace, EV manufacturing, electronics, and medical devices present significant growth prospects. Engineering plastics currently account for less than 5% of total polymer demand, yet they deliver superior margins due to their performance in demanding environments. PEEK, PPS, flame-retardant PC, carbon-fiber reinforced nylon, and high-temperature fluoropolymers are increasingly used in battery modules, semiconductor components, lightweight aircraft parts, and medical implants. The rapidly expanding EV sector expected to produce over 40 million units annually by 2032 will substantially increase demand for lightweight, heat-resistant polymer solutions.

Smart manufacturing represents opportunity for Plastic Market. The adoption of robotics, automated handling systems, and real-time sensor monitoring in plastics factories improves accuracy and reduces production defects by 15–20%. 3D printing in plastics has grown by more than 300% over the past decade, enabling rapid prototyping, mass customization, and medical device fabrication. AI-driven material optimization is helping plastic companies innovate faster, reduce downtime, and minimize waste.

Plastic Market Segment Analysis:

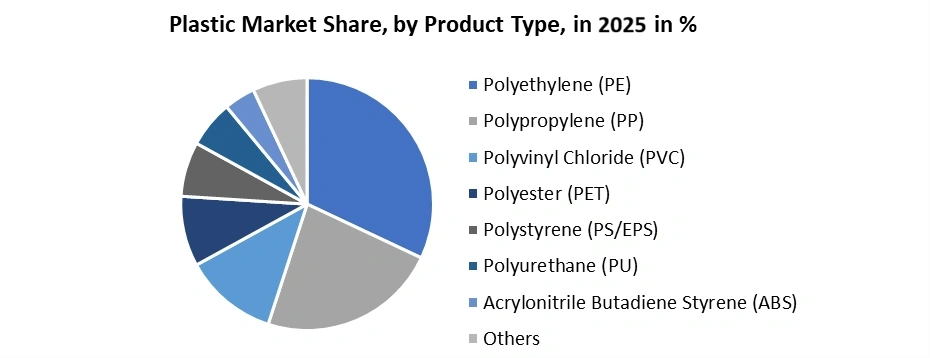

Based on Product Type, the Plastic Market is segmented into Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polyester (PET), Acrylonitrile Butadiene Styrene (ABS), and Polyurethane (PU). Among these, Polyethylene (PE) dominated the Plastic Market in 2025 and is expected to maintain its leading position throughout the forecast period. PE accounts for over 30–32% of total Plastic Market consumption, driven by its versatility, durability, and cost-efficiency. The Plastic Market benefits significantly from the widespread use of HDPE and LDPE films in packaging, where PE offers superior flexibility, moisture resistance, and excellent processing behavior. More than 55% of global flexible packaging films are PE-based, making it the foundational polymer of the Plastic Market. Beyond packaging, the Plastic Market also sees strong PE demand in construction films, geomembranes, household goods, and agricultural products, reinforcing its dominance.

The fastest-growing product segment in the Plastic Market is Polypropylene (PP), driven by its rising adoption in automotive, healthcare devices, and consumer goods. PP is gaining market share due to its lightweight nature, high fatigue resistance, and suitability for replacing metals and engineering plastics in advanced applications. The Plastic Market increasingly relies on PP for injection-molded components, which now represent millions of tonnes of annual PP output. In the automotive sector, PP’s role is expanding as manufacturers incorporate more lightweight polymers for dashboards, battery housings, and structural parts. With rising demand for recyclable and high-performance materials, PP is becoming the fastest-expanding segment within the Plastic Market.

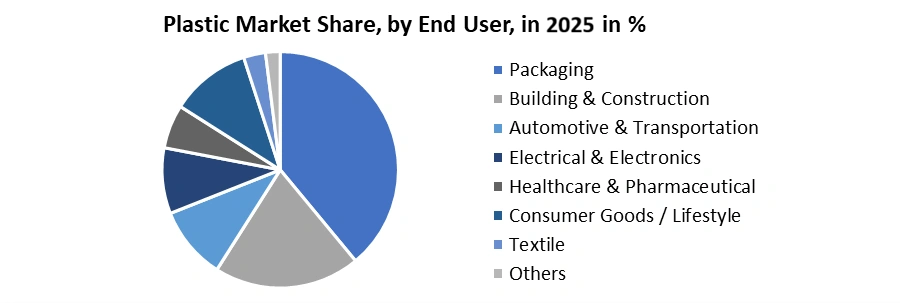

Based on End-User, the Plastic Market is segmented into Packaging, Automotive & Transportation, Building & Construction, Electrical & Electronics, and Healthcare & Pharmaceutical. Among these, the Packaging segment dominated the Plastic Market in 2024, accounting for approximately 40% of global plastic consumption. The Plastic Market is heavily driven by demand for food packaging, protective films, beverage bottles, and e-commerce packaging materials. Rapid growth in online retail—recording 20%+ annual expansion in major Asian markets—has further strengthened the dominance of packaging in the Plastic Market. Plastics such as PE, PP, and PET remain essential due to their superior barrier properties, lightweight nature, and cost advantage. Additionally, the Plastic Market is witnessing strong innovation trends in recyclable packaging, such as rPET bottles and bio-based films, supported by global sustainability mandates and EPR regulations.

The fastest-growing end-user segment in the Plastic Market is Healthcare & Pharmaceutical, supported by increasing consumption of disposable medical devices, diagnostic components, and sterile packaging. The Plastic Market benefits significantly from heightened demand for syringes, IV sets, catheters, inhaler components, and laboratory consumables. With rising healthcare expenditure, expanded hospital infrastructure, and increased preference for single-use medical plastics for infection control, this segment is rapidly accelerating. The Plastic Market is experiencing substantial growth from 3D-printed medical plastics, which have increased by more than 300% over the last decade, enabling patient-specific implants and surgical tools. As biotechnology applications and advanced drug-delivery systems expand, the Healthcare & Pharmaceutical segment continues to be the fastest-emerging sector within the Plastic Market.

Plastic Market Regional Analysis:

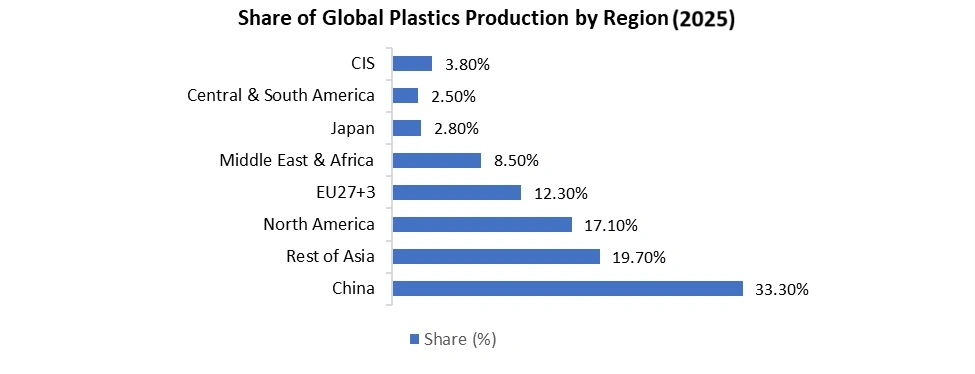

Asia-Pacific dominated the Plastic Market in 2024, accounting for the largest share globally, driven due to rapid industrialization, strong manufacturing output, and a massive consumer base. China remains the world’s largest producer and consumer of plastics, supported by large-scale petrochemical capacity, cost-effective labor, and extensive downstream industries. India and Southeast Asian economies including Indonesia, Vietnam, Thailand, and Malaysia continue to expand their plastic consumption due to booming packaging demand, rising infrastructure development, and growth in electronics manufacturing. The e-commerce surge across the region has increased the use of plastic films, pouches, and protective packaging. Moreover, APAC is a global hub for automotive and electrical manufacturing, which significantly boosts demand for PP, ABS, PC, and engineering plastics. Government-led initiatives promoting Make-in-Asia manufacturing, coupled with increasing investments in polymer recycling and bioplastic production, strengthen APAC’s leadership in the Plastic Market.

Recent Development

INNATE TF 220 Precision Packaging Resin

On June 30, 2025, Dow declared the launch of INNATE TF 220 Precision Packaging Resin, designed for high-performance biaxially oriented polyethylene (BOPE) films to improve recyclability in flexible packaging. The development supports mono-material designs and integrates post-consumer recycled (PCR) content via partnership with Chinese detergent brand Liby. This innovation addresses low recycling rates for flexible packaging by enhancing processability, extrusion stability, stiffness and heat resistance, while aligning with circular-economy goals. It marks a key step for Dow in shifting the Plastic Market toward circular, high-value packaging solutions.

Expansion of Advanced Recycling Capacity

On November 21, 2024, ExxonMobil declared a USD 200 million investment to expand its advanced recycling operations at its Baytown and Beaumont sites in Texas. The goal: achieve a global chemical-recycling capacity of 1 billion pounds of plastic waste per year by 2027. The move further positions ExxonMobil in the Plastic Market amid rising demand for circular plastics. The expansion will increase the processing of hard-to-recycle plastics into raw materials via pyrolysis, supporting brand owners’ sustainability goals for certified-circular plastics.

Plan to Triple Chemical Recycling Capacity (MoReTec)

On November 15, 2024, LyondellBasell unveiled its plans to build a second chemical-recycling plant using its proprietary MoReTec technology at its Houston refinery, potentially tripling its chemical-recycling capacity. The new facility would have approximately twice the capacity of the plant under construction in Germany. This development signals a material shift in the Plastic Market toward high-volume recycling of post-consumer plastic waste. The initiative is part of LyondellBasell’s strategy to convert plastic waste back into feedstock for new polymers and contribute to a circular plastics economy.

Plastic Market Scope: Inquire before buying

| Global Plastic Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 559.46 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5% | Market Size in 2032: | USD 787.22 Bn. |

| Segments Covered: | by Product Type | Polyethylene (PE) Polypropylene (PP) Polyvinyl Chloride (PVC) Polyester (PET) Acrylonitrile Butadiene Styrene (ABS) Polyurethane (PU) |

|

| by Additives | Plasticizers Flame Retardants Stabilizers Fillers |

||

| by Resin Types | Thermoplastics Thermosetting Plastics Bioplastics |

||

| by End-User | Packaging Automotive & Transportation Building & Construction Electrical & Electronics Healthcare & Pharmaceutical |

||

Plastic Market, by Region :

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Plastic Market Report in Strategic Perspective:

1. Dow Inc.

2. BASF SE

3. SABIC (Saudi Basic Industries Corporation)

4. INEOS Group

5. ExxonMobil Chemical

6. LG Chem

7. LyondellBasell Industries

8. DuPont de Nemours, Inc.

9. Chevron Phillips Chemical Company

10. Formosa Plastics Corporation

11. Borealis AG

12. Borouge

13. ALPLA Group

14. Amcor Plc

15. Berry Global Group, Inc.

16. Covestro AG

17. Solvay S.A.

18. Mitsubishi Chemical Group

19. Toray Industries, Inc.

20. Evonik Industries AG

21. Huntsman Corporation

22. Westlake Chemical Corporation

23. INEOS Olefins & Polymers

24. INEOS Styrolution

25. Sumitomo Chemical Co., Ltd.

26. Mitsui Chemicals, Inc.

27. Kuraray Co., Ltd.

28. Ube Industries, Ltd.

29. Trinseo S.A.

30. Celanese Corporation

Frequently Asked Questions

1.What is the current valuation and projected growth of the Plastic Market?

Ans. The Plastic Market size reached USD 559.46 Billion in 2025. With a 5% CAGR, Industry Growth Drivers will push the valuation to USD 787.22 Billion.

2. Which region leads the Plastic Market share and what drives its dominance?

Ans. Asia-Pacific leads the Plastic Market Share Analysis 2026. Dominance is driven by China’s massive petrochemical capacity, rapid industrialization, and booming e-commerce packaging demand across India.

3. What are the key Plastic Market growth drivers in the automotive sector?

Ans. Automotive lightweighting drives demand for engineering plastics. High-performance polymers enable 15% weight reduction, extending the driving range for EVs, a critical Plastic Market Growth Factor.

4. How is sustainability shaping the future Plastic Market landscape and material innovation?

Ans. Sustainability mandates accelerate the shift toward bio-based resins. The Plastic Market Outlook 2032 predicts biodegradable plastic production will triple, reaching 6 million tonnes via circular-economy models.

5. Which product segment is the fastest growing in the Plastic Market?

Ans. Polypropylene (PP) is the fastest-expanding segment. Its lightweight nature and high fatigue resistance make it essential for advanced automotive parts and recyclable medical devices globally.

6. How is technology like AI and Industry 4.0 improving plastic manufacturing efficiency?

Ans. AI-enabled monitoring and smart manufacturing reduce material waste by 30%. These Digital Transformation Trends in Plastic Market lower production costs and enhance overall competitive resource autonomy.