Petrochemicals Market by Type, Application, End Use Industry and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

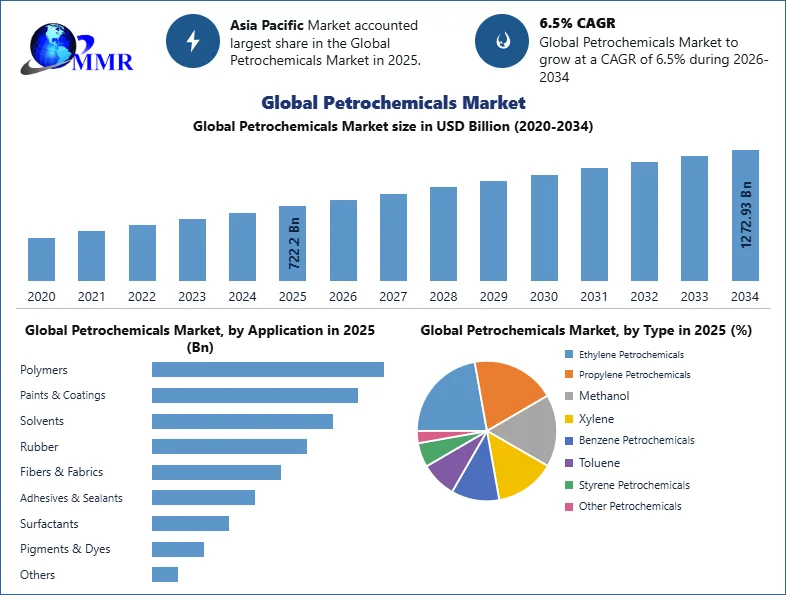

The Petrochemicals Market size was valued at USD 722.20 Billion in 2025, and the total Petrochemicals revenue is expected to grow at a CAGR of 6.5% from 2025 to 2034, reaching nearly USD 1272.93 Billion by 2034.

Petrochemicals Market Overview

Petrochemicals are derived from petroleum or natural gas. Petrochemicals are an important part of the chemical industry as the demand for synthetic materials is increasing continually and plays a major role in the growth of the economy. They are used in petrochemical products, plastics, medicines, cosmetics, furniture, appliances, electronics, solar power panels, and wind turbines. The automotive industry's growth, including the shift toward electric vehicles, impacts the demand for petrochemical materials used in vehicle production. Changing consumer preferences for convenience, durability, and lightweight materials contribute to the demand for petrochemical-based products. The Petrochemicals Market is highly competitive, leading to price pressures and thinner profit margins. Companies need to invest in innovation to stay ahead.

To know about the Research Methodology :- Request Free Sample Report

Petrochemicals Market Dynamics

Economic Development and Emerging Markets to boost the Petrochemical Industry growth

Robust economic growth, prominently observed within emerging economies, with a focal emphasis on the Asian markets, manifests as a pivotal driver behind the escalated consumer expenditure and heightened industrial activities, which, in turn, propel the demand for petrochemical products. As nations such as China and India continue their developmental trajectory, petrochemical consumption within these regions experiences a concurrent upswing. As the global population continues its steady expansion, paralleled by the ongoing urbanization trend, the concomitant surge in demand for consumer goods, housing, and infrastructure, particularly within urban and metropolitan zones, underscores the indispensable role of petrochemicals in facilitating the production of essential urban requisites like plastics, construction materials, and electronic components.

The petrochemical industry's reliance on hydrocarbons, which exhibit an intrinsic linkage with the energy sector, stipulates that the prevailing growth in energy consumption, encompassing the domains of oil and natural gas, significantly influences the availability and pricing of feedstocks fundamental to the petrochemical sector. The progressive march of technological innovations has bestowed upon the industry an arsenal of new and more efficient petrochemical production processes. These innovations have broadened the spectrum of producible petrochemical products, fostering enhancements in overall industry efficiency and sustainability. The burgeoning traction of the circular economy model, characterized by the recycling, reutilization, and repurposing of products and materials, is permeating the petrochemical landscape. Petrochemical enterprises are actively exploring avenues to engender materials that are more sustainable and amenable to recycling, aligning with the core tenets of the circular economy.

The petrochemical industry is highly interconnected globally, with complex supply chains that can be affected by trade policies, geopolitical tensions, and logistics disruptions. Changes in international trade agreements and global economic dynamics influence Petrochemicals Market dynamics. The availability and cost of feedstocks, such as crude oil and natural gas, significantly influence the Petrochemicals Market growth. Shale gas and other unconventional sources have altered the feedstock landscape, impacting the competitiveness of various regions. Consumer preferences for sustainable and environmentally friendly products have prompted companies to adapt their offerings. Increased consumer awareness of environmental and health-related issues influence the development of petrochemical products. Changing regulations related to chemical safety, emissions, and environmental protection can significantly impact the petrochemical industry.

Compliance with evolving regulations often requires investments in technology and process improvements. The ascendancy of plastics as a pivotal product category within the petrochemical domain is irrefutable. The burgeoning global demand for food necessitates a concurrent surge in the need for agricultural chemicals, sustaining the petrochemical industry's prominence. The transportation sector, particularly the automotive industry, relies substantially on petrochemical products. Petrochemicals are integral to the production of plastics, synthetic rubber, and an array of chemicals employed in vehicle manufacturing. The trajectory of the automotive sector wields a direct and profound influence on the Petrochemicals Market growth.

Volatility in Oil Price to restrain the Petrochemicals Market growth

The petrochemical industry maintains an intricate nexus with crude oil prices, as a substantial proportion of its raw materials are derived from oil. Oscillations in oil prices can exert profound influences on the cost of production for petrochemical companies. When oil prices surge, it translates into elevated operating expenses and diminished profit margins. Conversely, during periods of low oil prices, investments in exploration and production often decline, precipitating supply chain disruptions. The imposition of trade barriers and tariffs can exert a pronounced impact on the industry's global supply chains and profitability. Prolonged trade disputes and tariff conflicts can disrupt established trade routes and inflate costs for petrochemical enterprises. The perception of the Petrochemicals Market within the public sphere can serve as a significant restraint. The petrochemical sector exhibits a pronounced dependence on a limited set of key raw materials, including ethylene and propylene. This reliance on a constrained array of feedstocks renders the supply chain vulnerable and accentuates susceptibility to price fluctuations.

Opportunities in Petrochemical

Manufacturers' mounting environmental concerns fuels market growth. Policymakers have pushed businesses to take action and run the production process responsibly and environmentally friendly in response to growing environmental concerns. In order to comply with new pollution control requirements, a number of significant businesses are updating their operations. This is because reducing pollution from manufacturing facilities have essentials for reducing overall pollution and the effects of climate change. For instance, Dow stated in October 2022 that it build Alberta, Canada's first integrated net-zero carbon ethylene cracker and derivatives plant.

During the 2025–2034 forecast period, the petrochemicals market is expected to be strongly influenced by low-carbon capacity expansion, renewable energy procurement, and site-level decarbonization investments. Dow’s Fort Saskatchewan Path2Zero project in Alberta, Canada, remains a major example, as the company is developing what it describes as the world’s first net-zero Scope 1 and 2 emissions integrated ethylene cracker and derivatives facility. Dow’s latest update states that Phase 1 is now expected to start by year-end 2029 and Phase 2 by year-end 2030, following a two-year delay to align capital deployment with market conditions. The project is designed to triple Dow’s ethylene and polyethylene capacity at the site, decarbonize around 20% of Dow’s global ethylene footprint, and support growing demand for low-emission polyethylene and ethylene derivatives in packaging, infrastructure, wire and cable, pressure pipe, and food packaging applications through 2034.

MEGlobal Americas Inc., part of EQUATE Petrochemical Group, also supports the sector’s shift toward lower-emission production. The company’s Oyster Creek, Texas site began using 100% renewable electricity in 2023 through its partnership with Calpine Energy Solutions, not 2025 as previously stated. EQUATE reported that the agreement supports the retirement of renewable energy certificates and strengthens the group’s wider sustainability strategy, including Scope 1 and Scope 2 emissions reduction efforts. This type of renewable power procurement is expected to become increasingly important in the petrochemicals market through 2034 as producers face pressure from customers, regulators, and downstream brands to lower the embedded carbon footprint of petrochemical products.

Advanced petrochemical products with more inventive applications and greater environmental friendliness are required by numerous end-user industries, which is expected to boost the Petrochemicals Market growth. The quickly developing base chemical field is no different in this regard. Aviation, building and construction, agriculture, food and beverage, electrical and electronics, healthcare, and automotive are a few end-use industries that have a greater need for enhanced petrochemical products. This has prompted numerous petrochemical producers to create new technologies to better turn the petrochemicals into newer goods that are more eco-friendly and have more creative and practical uses.

Petrochemicals Market Segment Analysis

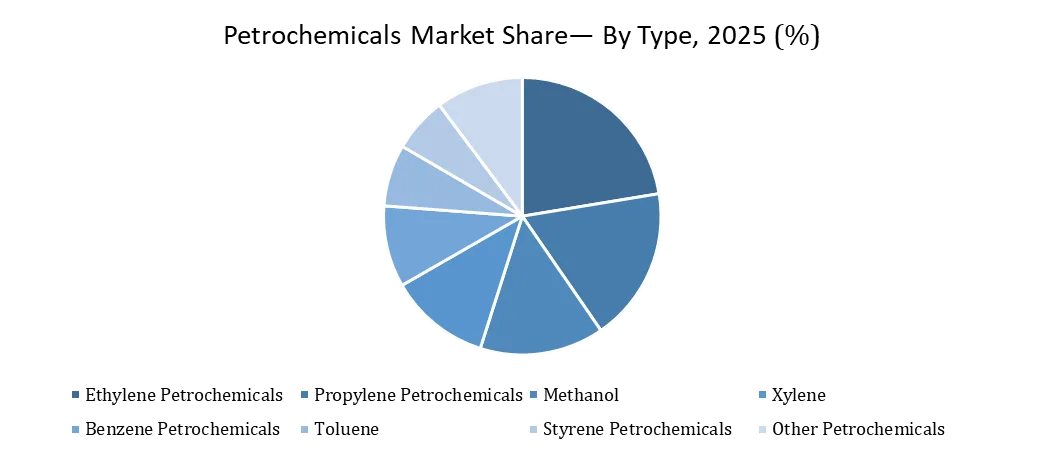

Based on Type, the market is segmented into Ethylene, Propylene, Methanol, Xylene, and Others. Ethylene, and Propylene segment dominated the market in 2025 and is expected to hold the largest Petrochemical share over the forecast period. In the Petrochemicals Market, ethylene and propylene stand out as two of the most pivotal and dominant segments. They are fundamental building blocks for a diverse array of products, finding extensive applications across a multitude of industries. Ethylene holds a pivotal role within the petrochemical industry, central to the production of plastics and a diverse array of chemical compounds. Its versatility and wide-ranging applications solidify its status as a dominant segment in the market. Propylene is instrumental in the creation of diverse chemical intermediates. It plays a key role in the manufacture of propylene oxide (used in polyurethane foam and glycol production), acrylonitrile (employed in acrylic fibers and plastics), and cumene (utilized in the production of phenol and acetone). Propylene constitutes a critical segment in the Petrochemicals Market, closely following ethylene in importance. Its adaptability in the production of plastics, chemicals, and synthetic materials renders it indispensable across various industries.

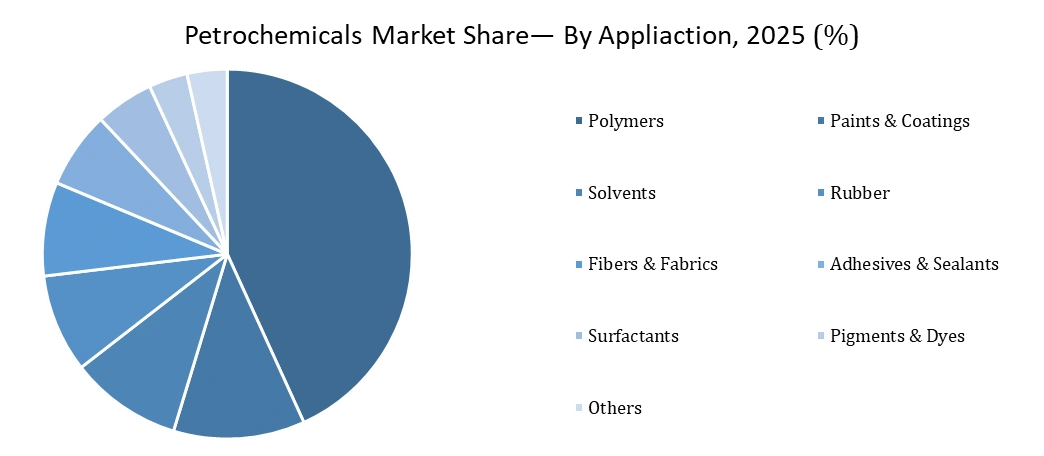

By application, polymers dominated the petrochemicals market in 2025, driven by large-scale consumption of polyethylene, polypropylene, PVC, PET, and polystyrene in packaging, consumer goods, construction, automotive, and industrial products. Market.us reports that polymers captured more than 43.2% of the petrochemicals market, while IMARC also identifies polymers as the largest application segment. Paints & coatings, solvents, rubber, fibers & fabrics, adhesives & sealants, surfactants, pigments & dyes, and others represented the remaining market share due to their extensive use in industrial manufacturing, textiles, construction materials, automotive components, and specialty chemical formulations

By end user industry, the plastics industry held the largest share in 2025, as petrochemicals are core raw materials for polyethylene, polypropylene, PVC, PET, and other plastic resins. The chemical industry also represented a major share because petrochemical intermediates are widely used to manufacture solvents, resins, synthetic rubber, coatings, adhesives, and specialty chemicals. Textile and apparel demand was supported by polyester, nylon, acrylic fibers, and other synthetic materials, while automotive, agriculture, aerospace, and other industries consumed petrochemicals through plastics, rubber, coatings, fertilizers, composites, and engineered materials. IEA highlights that petrochemicals are found across products such as clothing, tyres, packaging, detergents, and digital devices, supporting their broad end-use base.

Petrochemicals Market Regional Analysis

Investment in Research and Development sector in Asia Pacific to boost the Market growth

Governments and corporate entities alike are directing resources toward research and development endeavors aimed at the creation of innovative petrochemical products and processes. This encompasses the development of novel materials characterized by enhanced properties and reduced environmental impact. Evolving consumer lifestyles and the increased prevalence of product packaging for convenience and preservation have spurred the demand for petrochemical-based materials such as plastics and flexible packaging. These materials are integral to food packaging, beverage containers, and various other consumer products. The textile industry in the Asia-Pacific region reaps the benefits of synthetic fibers produced from petrochemicals. These fibers, encompassing polyester and nylon, facilitate the production of clothing and textiles that are both cost-effective and widely accessible, satisfying the needs of a burgeoning population. Several countries, including China, have undertaken measures to amplify domestic petrochemical production capacity. This often entails investments in new production facilities and the expansion of existing ones. The establishment of petrochemical manufacturing zones and industrial parks has attracted foreign direct investment, thereby contributing to the growth of the petrochemical industry in the region.

Petrochemicals Market Competitive Landscape

The competitive landscape of the petrochemicals market is characterized by intense competition among a wide range of players, from global giants to regional and specialized companies. Understanding the competition insights in this dynamic market is essential for both established and emerging players. Specialized petrochemical companies like LyondellBasell Industries, INEOS, and Celanese Corporation focus on specific niche areas within the petrochemical industry. They often excel in innovation, producing high-performance materials and specialty chemicals. Technological innovation is a critical competitive factor. Companies that invest in research and development to create novel materials, improve production processes, and enhance sustainability are better positioned to meet market demands. Adherence to stringent environmental and safety regulations is a key competitive factor. Companies that proactively address regulatory challenges and invest in compliance measures demonstrate a commitment to responsible operations. Mergers and acquisitions are common strategies to strengthen market position. Companies acquire competitors or complementary businesses to expand their product portfolios and geographic reach.

Recent development

March 2025 – ADNOC, OMV, Borealis, Borouge and NOVA Chemicals: ADNOC and OMV signed a binding framework agreement to combine Borouge and Borealis into Borouge Group International. Under the transaction, the combined entity will acquire NOVA Chemicals for USD 13.4 billion, including debt. With the planned Borouge 4 recontribution, the platform is positioned as a USD 60+ billion global polyolefins company and the fourth-largest polyolefins producer by nameplate capacity. This is one of the strongest petrochemical M&A developments of 2025 because it combines Middle East feedstock strength, European technology, and North American polyethylene capacity.

January 2026 – SABIC: SABIC signed two major portfolio-divestment agreements with a combined enterprise value of USD 950 million. The company agreed to sell its European Petrochemicals business to AEQUITA for USD 500 million and its Engineering Thermoplastics business in the Americas and Europe to MUTARES for USD 450 million, plus earn-out provisions. The European Petrochemicals assets include ethylene, propylene, LDPE, LLDPE, HDPE, PP, and value-added polymer compounds across sites in the UK, Netherlands, Germany, and Belgium, making this a major European petrochemical restructuring move.

May–September 2025 – Dow Inc.: Dow completed its strategic partnership with Macquarie Asset Management for Diamond Infrastructure Solutions, a U.S. Gulf Coast infrastructure company. Dow initially sold a 40% stake and later Macquarie increased its ownership to 49%, bringing Dow’s total cash proceeds to approximately USD 3.0 billion. Dow retained majority ownership and operational control, while Diamond Infrastructure Solutions continued serving more than 70 existing and new customers. This development is important because it shows how petrochemical producers are monetizing infrastructure assets while preserving operating control.

June 2025–May 2026 – LyondellBasell Industries Holdings B.V.: LyondellBasell entered into an agreement and exclusive negotiations with AEQUITA for the sale of selected European olefins and polyolefins assets, and completed the sale in May 2026. The assets included operations in Berre, France; Münchsmünster, Germany; Carrington, United Kingdom; and Tarragona, Spain. This is a strong restructuring example for the market, as European producers continue to reduce exposure to challenged commodity petrochemical assets and focus capital on more competitive operations.

January 2025 – Shell plc and CNOOC: Shell and CNOOC, through their CSPC joint venture, made a final investment decision to expand the Daya Bay petrochemical complex in Huizhou, China. The expansion includes a third ethylene cracker with 1.6 million tonnes per year of planned ethylene capacity and downstream specialty chemical units, including 320,000 tonnes per year of high-performance specialty chemicals such as polycarbonates and carbonate solvents. This development strengthens China’s position as a major growth center for integrated petrochemical production.

March 2026 – BASF SE: BASF inaugurated its world-scale Verbund site in Zhanjiang, China, after commencing production of the first core products in 2025. The site includes 18 plants covering 32 production lines and a steam cracker with 1 million metric tons per year of ethylene capacity. BASF also stated that the site is powered by renewable electricity and that the steam cracker uses electric drives for its main compressors. This is one of the most important Asia-Pacific petrochemical developments because it adds large-scale ethylene and downstream chemical capacity in China while integrating low-carbon power into site operations.

July 2025 – Exxon Mobil Corporation: ExxonMobil started up its Huizhou Chemical Complex in Guangdong, China. The company stated that the project was completed ahead of schedule and under budget, with approximately 84 million recorded work hours without major safety incidents. ExxonMobil also reported that the complex is designed to treat and reuse 60%–70% of wastewater in onsite cooling towers. This is a key development because it adds high-performance chemical and polymer capacity in China, one of the largest demand centers for petrochemical products.

2025–2027 – Chevron Phillips Chemical Company LLC and QatarEnergy: Chevron Phillips Chemical and QatarEnergy advanced the Golden Triangle Polymers project in Orange, Texas. The project has a total installed cost of USD 8.5 billion and includes a 2,080 KTA ethane cracker and two 1,000 KTA high-density polyethylene units. The facility is planned to start up in 2027 and is expected to create more than 500 full-time jobs. This is one of North America’s most important petrochemical capacity additions because it strengthens U.S. ethane-based polyethylene production and export competitiveness.

October–November 2025 – LOTTE Chemical Corporation: LOTTE Chemical completed its large petrochemical complex in Indonesia, with commercial operations beginning in October 2025. The complex has annual production capacity of 1 million tons of ethylene, 520,000 tons of propylene, 350,000 tons of polypropylene, 140,000 tons of butadiene, and 400,000 tons of BTX. This is a major Southeast Asian petrochemical development because it expands local olefins and polymer supply and reduces dependence on imported petrochemical feedstocks and resins.

February 2025 – Sinopec Shanghai Petrochemical Company Limited: Sinopec Shanghai Petrochemical announced a structural adjustment project involving refining-device optimization and the installation of 1.20 million tons per year of ethylene capacity along with downstream processing units. The development is important for the China petrochemicals market because it supports the shift from refining-led output toward higher-value ethylene derivatives, polymers, and advanced chemical materials.

October 2025 – Braskem S.A.: Braskem approved an investment plan of BRL 4.2 billion to expand ethylene and polyethylene production at its Rio de Janeiro petrochemical complex. The project includes 220,000 tons per year of additional ethylene capacity and equivalent polyethylene volumes. Braskem had also approved BRL 233 million for the basic engineering phase in February 2025. This is a strong South American development because it directly increases Brazil’s domestic ethylene and polyethylene production base.

April 2025 – Wanhua Chemical Group and Petrochemical Industries Company, Kuwait: Wanhua Chemical signed a joint venture agreement with Petrochemical Industries Company of Kuwait, under which PIC invested USD 638 million for a 25% equity stake in Wanhua Petrochemical (Yantai) Co., Ltd. The transaction is significant because it gives Kuwait strategic exposure to a large Chinese petrochemical platform while supporting Wanhua’s integrated petrochemical expansion in Asia.

February 2026 – OQ and Kuwait Petroleum International: OQ and Kuwait Petroleum International signed a Project Development Agreement for a jointly owned petrochemical complex in the Special Economic Zone at Duqm, Oman. OQ also highlighted more than USD 10 billion of strategic investment across Duqm’s energy value chain, including infrastructure, downstream operations, and petrochemicals. This development supports the Middle East’s strategy of building integrated refining and petrochemical hubs with export access to Asia, Europe, and Africa.

December 2025–April 2026 – Mitsui Chemicals, Idemitsu Kosan and Sumitomo Chemical: Japanese petrochemical producers advanced major restructuring steps. Idemitsu and Mitsui reached a final agreement to consolidate their Chiba ethylene operations, with production to be consolidated at Mitsui’s facility and Idemitsu’s facility to be closed. The combined ethylene production capacity involved is 920,000 tons per year. Mitsui, Idemitsu, and Sumitomo Chemical also signed a definitive agreement to integrate Sumitomo Chemical’s PP and LLDPE business into Prime Polymer, with Japan Fair Trade Commission clearance received in April 2026. This is a strong example of capacity rationalization in response to regional overcapacity and weaker domestic demand.

2025–2026 – Reliance Industries Limited: Reliance Industries continued executing its Oil-to-Chemicals expansion program, including an announced INR 75,000 crore investment plan. The company disclosed plans for a 3 MMTPA PTA plant and a 1 MMTPA PET plant at Dahej, both targeted for completion by 2026. Reliance also reported FY 2025–26 Oil-to-Chemicals revenue of INR 6,62,401 crore and EBITDA of INR 60,546 crore, showing the scale of its integrated refining, petrochemical, and polymer operations.

January 2025 – INEOS Group: INEOS advanced its Project ONE ethane cracker development in Antwerp, Belgium, with the first two furnace modules arriving at the Lillo site in January 2025. The project has a nameplate capacity of 1,450 kilotonnes per year of ethylene. Once operational, INEOS states that the project will support around 300 direct long-term jobs and 150 contractor jobs. This is one of Europe’s most important petrochemical investment projects because it adds a new large-scale ethane-based cracker in a region where many older naphtha-based assets face competitiveness pressure.

Petrochemicals Market Scope: Inquiry Before Buying

| Petrochemicals Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 722.20 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6.5% | Market Size in 2034: | USD 1272.93 Bn. |

| Segments Covered: | by Type | Ethylene Petrochemicals Propylene Petrochemicals Methanol Xylene Benzene Petrochemicals Toluene Styrene Petrochemicals Other Petrochemicals |

|

| by Application | Polymers Paints & Coatings Solvents Rubber Fibers & Fabrics Adhesives & Sealants Surfactants Pigments & Dyes Others |

||

| by End Use Industry | Plastics Industry Chemical Industry Textile and Apparel Industry Automotive Industry Agriculture Aerospace Industry Others |

||

Petrochemicals Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Petrochemicals Market, Key Players

North America

- Dow Inc.

- Chevron Phillips Chemical Company LLC.

- Exxon Mobil Corporation

- LyondellBasell Industries Holdings B.V.

- NOVA Chemicals Corporation

- Imperial Oil Limited

Europe

- BASF SE

- INEOS Group Ltd.

- Shell plc

- Linde plc

- Air Liquide

- Borealis AG

- ORLEN S.A.

- Repsol S.A.

Asia – Pacific

- Reliance Industries Limited

- Mitsubishi Chemical Group Corporation

- LG Chem Ltd.

- China National Petroleum Corporation (CNPC)

- China Petrochemical Corporation (Sinopec)

- PetroChina Company Limited

- Hengli Petrochemical Co., Ltd.

- Formosa Petrochemical Corporation

- Maruzen Petrochemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Wanhua Chemical Group Co., Ltd.

- GS Caltex Corporation

- Haldia Petrochemicals Limited

- Idemitsu Kosan Co., Ltd.

- Lotte Chemical Corporation

- Manali Petrochemicals Limited

- Mitsui Chemicals, Inc.

- Finolex Industries Limited

- Unicorn Petroleum Industries Pvt. Ltd

South America

- Saudi Basic Industries Corporation (SABIC)

- ADNOC

- Kuwait Petroleum Corporation

- Carbon Holdings Limited

- Duqm Refinery & Petrochemical Industries Company LLC

- Egyptian Petrochemicals Holding Company (ECHEM)

- Sasol Limited

Middle East & Africa

- Braskem S.A.

- Pampa Energía S.A.

Frequently Asked Questions:

1] What is the growth rate of the Global Petrochemicals Market?

Ans. The Global Petrochemicals Market is growing at a significant rate of 6.5 % over the forecast period.

2] Which region is expected to dominate the Global Petrochemicals Market?

Ans. Asia Pacific region is expected to dominate the Petrochemicals Market over the forecast period.

3] What was the Global Petrochemicals Market size in 2025?

Ans: The Global Petrochemicals Market size was USD 722.20 Billion in 2025.

4] Who are the top players in the Global Petrochemical Industry?

Ans. The major key players in the Global Petrochemicals Market are Pampa Energía S.A. , BASF SE, and Chevron Corporation.

5] Which factors are expected to drive the Global Petrochemicals Market growth by 2032?

Ans. Technological advancement in Petrochemical manufacturing is expected to drive the Petrochemicals Market growth over the forecast period (2026-2032).