Paper Straws Market Size by Material Type, Product Type, Straw Length, Sales Channel, End Use, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

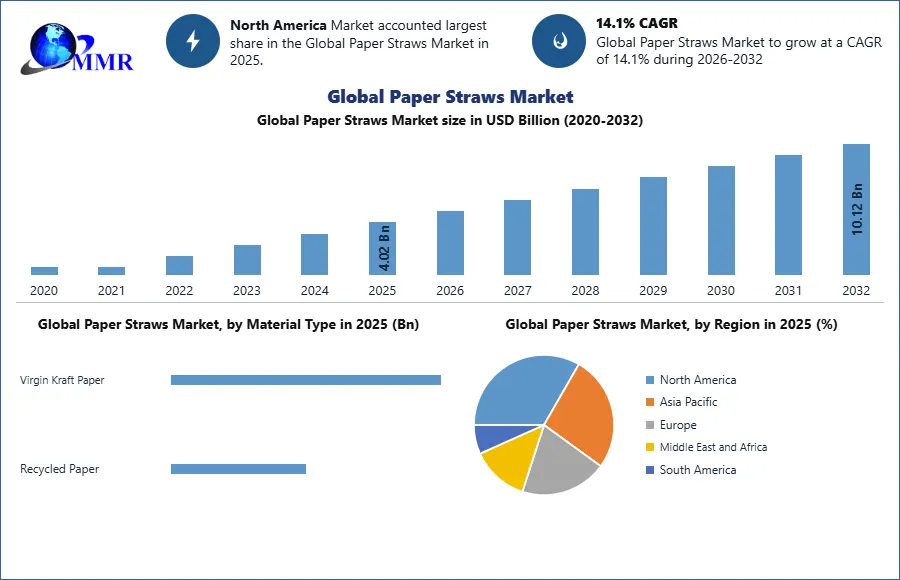

Paper Straws Market size was valued at USD 4.02 Bn. in 2025, and the total Paper Straws Market revenue is expected to grow by 14.10% from 2026 to 2032, reaching nearly USD 11.55 Bn.

Paper Straws Market Overview

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Paper Straws Market Dynamics

Sustainability regulations and foodservice adoption support market expansion

The global Paper Straws Market is witnessing strong growth due to rising environmental awareness and government restrictions on single-use plastics. Countries including India, China, United States, and several parts of Europe have introduced regulations limiting plastic straws, encouraging the shift toward biodegradable alternatives. Foodservice providers, beverage brands, airlines, and hospitality companies are rapidly adopting paper straws to meet environmental goals and consumer expectations. Major global restaurant chains are integrating paper-based products into packaging to align with ESG commitments and sustainable procurement standards. Growth in takeaway beverages, ready-to-drink juices, and online food delivery is also supporting market expansion. Improved product availability across supermarkets and retail channels further boosts demand. Manufacturers are investing in recyclable food-contact paper and advanced production technologies to increase output and reduce costs. The increasing use of eco-friendly packaging across cafés, restaurants, and institutional catering is creating sustained demand. As consumers increasingly prefer biodegradable products, paper straws are becoming a standard component of sustainable food packaging, supporting long-term growth through commercial adoption and regulatory enforcement.

Durability issues and higher manufacturing cost remain key barriers

Despite increasing adoption, the Paper Straws Market faces challenges related to product performance and cost competitiveness. Paper straws often soften after prolonged exposure to liquids, especially in cold beverages, smoothies, and carbonated drinks, which affects consumer satisfaction. Many users still prefer plastic alternatives due to longer usability and stronger structural performance. This creates resistance among foodservice operators that prioritize customer convenience. Manufacturers also face rising raw material costs for food-grade kraft paper, adhesives, biodegradable coatings, and specialty inks. Production of moisture-resistant straws requires multilayer paper processing and specialized bonding systems, which increases capital investment and operating expenses. Small restaurants and independent beverage outlets often find paper straws more expensive than plastic substitutes, limiting wider penetration in price-sensitive markets. In developing countries, inconsistent quality standards and low-cost plastic availability remain major barriers. Transportation and storage conditions also affect paper straw durability in humid environments. These issues compel manufacturers to invest in stronger paper formulations and coating technologies, but such innovation increases overall cost. As a result, balancing product performance, consumer acceptance, and affordability continues to be a major challenge for long-term market expansion.

Product innovation and industrial-scale packaging expansion create growth potential

The Paper Straws Market offers strong opportunities through material innovation and expansion into packaged beverage applications. Manufacturers are developing high-strength paper straws with water-resistant coatings, plant-based adhesives, and recyclable barrier layers to improve usability. These advancements help solve traditional limitations such as sogginess and short usage duration. The packaged beverage sector, especially milk, fruit juice, and aseptic cartons, is creating significant demand for paper straws compatible with automated filling systems. Growing adoption in school meal programs, healthcare institutions, and airlines is also increasing industrial-scale consumption. Companies are investing in automated paper converting equipment to improve production speed and reduce unit cost. Expansion of eco-friendly food packaging in emerging economies supports further market opportunities. Rising investment in compostable packaging materials and FSC-certified paper products is attracting beverage manufacturers seeking sustainable supply chains. Custom printing, flexible sizing, and premium designs for cafés and events are adding commercial value. In addition, consumer demand for plastic-free lifestyle products continues to rise, encouraging innovation in disposable tableware. With technological improvements and growing regulatory support, manufacturers can expand into new applications across foodservice, retail, and packaged beverage industries worldwide.

Paper Straws Market Segmentation

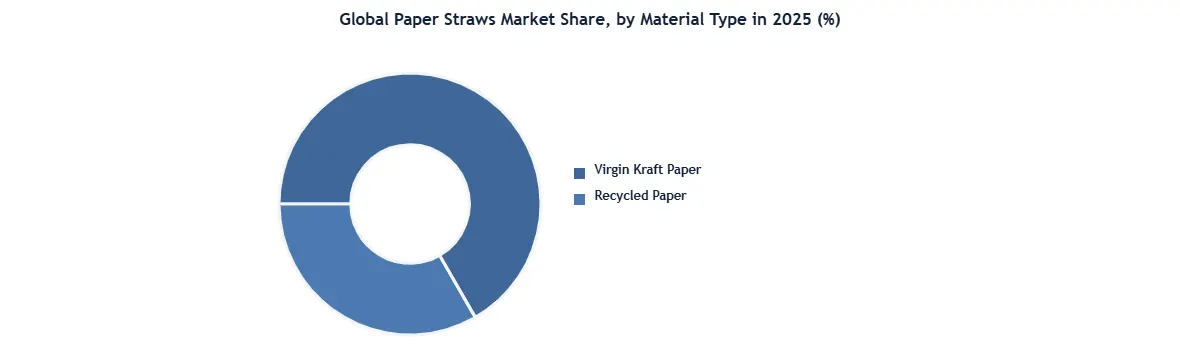

Based on Materials,The Virgin Kraft Paper segment holds the dominant share in the Paper Straws Market due to its superior strength, hygiene, and food-contact safety. Manufacturers prefer virgin kraft paper because it offers better structural integrity, making straws more durable in cold drinks, juices, milkshakes, and carbonated beverages. Its longer fiber structure improves resistance to soaking and deformation, which is essential for maintaining performance during extended beverage consumption. Virgin kraft paper also meets strict food safety and packaging regulations in markets such as United States, Germany, and Japan, where certified materials are required for direct food contact. Many global foodservice companies prefer this material because it ensures product consistency, clean appearance, and premium quality. It is widely used in branded straws for restaurants, cafés, airlines, and packaged beverage applications. In addition, virgin kraft paper supports high-speed manufacturing and custom printing, making it suitable for commercial-scale production. Its compatibility with moisture-resistant coatings further enhances product lifespan. These advantages make virgin kraft paper the preferred material for premium and large-volume paper straw production in 2025.

The Recycled Paper segment is gaining traction as sustainability goals become more important across the packaging industry. Recycled paper is increasingly used by manufacturers seeking to reduce environmental impact and lower raw material costs. It supports circular economy initiatives and helps brands strengthen eco-friendly positioning, especially in institutional catering, local foodservice, and event-based packaging. Countries such as India, China, and United Kingdom are promoting recycled paper use through waste reduction programs and sustainable procurement policies. The material is often selected for short-duration beverage applications where premium durability is less critical. However, recycled paper typically has shorter fiber length, which can reduce strength and liquid resistance compared with virgin kraft paper. Additional processing is often needed to improve safety, cleanliness, and product performance, increasing complexity. Despite these limitations, rising investments in recycling technology and sustainable packaging innovation are supporting segment growth. The segment is expected to expand significantly as governments and beverage companies continue to prioritize recyclable and lower-emission packaging materials in the global paper straws industry.

Paper Straws Market Regional Analysis

North America dominates the global paper straws market

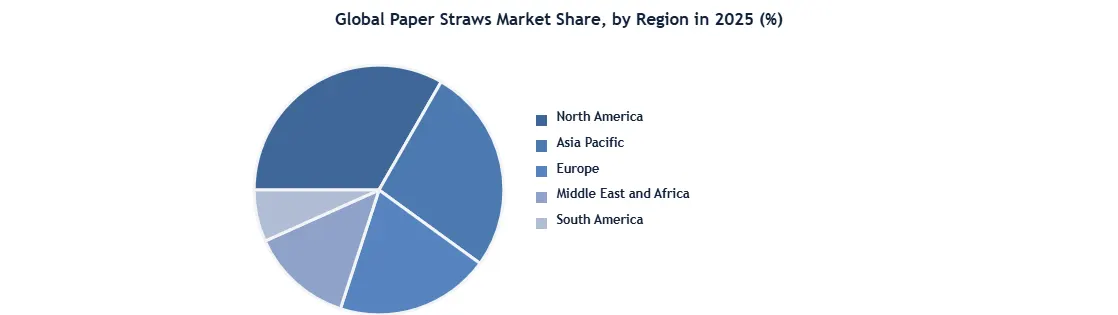

North America dominates the global Paper Straws Market due to strong environmental regulations, high consumer awareness, and early adoption of sustainable food packaging. The United States and Canada are major contributors, driven by municipal and state-level bans on plastic straws across restaurants, cafés, and public institutions. Large foodservice chains, hotels, cinemas, and beverage companies are actively replacing plastic straws with paper alternatives to align with sustainability targets. The region also benefits from established paper converting infrastructure, strong distribution networks, and high penetration of ready-to-drink beverages. Consumer preference for biodegradable products supports rapid acceptance in retail and hospitality sectors. Manufacturers in the region are focusing on recyclable coatings and stronger multilayer paper structures to improve performance. Major investments in sustainable packaging innovation and circular economy programs are strengthening the regional supply chain. The demand for eco-friendly disposables is particularly high in urban centers where waste management regulations are strict. Additionally, corporate ESG initiatives among multinational food and beverage brands are accelerating adoption. These factors continue to position North America as the leading revenue-generating region in the global paper straws industry.

Asia-Pacific is the fastest-growing regional market

Asia-Pacific is the fastest-growing region in the Paper Straws Market due to expanding manufacturing capacity, rising environmental awareness, and strong foodservice demand. China leads regional production because of its large paper manufacturing base, export capabilities, and increasing restrictions on single-use plastics. India is emerging as a key growth market due to government initiatives promoting biodegradable products and increased investments in sustainable packaging industries. Countries such as Japan and South Korea are driving premium demand through technologically advanced foodservice and convenience packaging sectors. Rapid urbanization, expansion of quick-service restaurants, and increasing online food delivery support regional consumption. Local manufacturers benefit from low labor costs and access to raw paper materials, making production cost-effective. The growing dairy and juice packaging industry is also increasing demand for paper straws used in carton beverages. Rising exports from Asian manufacturers to Europe and North America further strengthen the market. Supportive environmental policies and investments in automated production systems are helping the region achieve rapid growth, making Asia-Pacific a major future hub for paper straw manufacturing and global supply.

Paper Straws Market Competitive Landscape

There is intense competition in the global paper straw market, primarily driven by two manufacturers, Huhtamaki Oyj from Finland (25% market share) and Footprint from the United States (15% market share).

Huhtamaki has established itself as the leading firm and has carved a large niche market with its proprietary straws manufactured with its AquaShield technology; their drinking straws are resistant to liquids for 4+ hours of liquid integrity. Huhtamaki has captured 40% of the bubble tea market in Asia-Pacific and 30% of the quick service restaurant (QSR) market in Europe through its existing contracts with McDonald's and KFC. Huhtamaki has registered over 50 patents and earns 2 billion USD annually from straws. Footprint is gaining market share with their exclusive relationships with Starbucks (15,000+ North American locations) and Tetra Pak, specializing in plant-based compostable straws using EU-certified inks and QR-code brand identity. They earned XX billion USD in revenue per year. Footprint is cheaper to produce (bulk pricing is 5-10% lower) and better for the consumer (4+ hour integrity), while Footprint is committed to sustainability through marine-degradable solutions (the printed and QR-code breakdown in 6 months versus Huhtamaki's 12 months to break down) and premium branding products.

Paper Straws Market Key Developments

• May 2025, Huhtamaki (Finland) launched AquaShield water-resistant paper straws, made with a proprietary coating to hold their structure up to 4 hours in liquids. These straws were designed for bubble tea and iced drinks, and were first released in the Asia-Pacific region with a global launch scheduled for 2026.

• April 2025, Footprint LLC (USA) and Starbucks partnered to develop compostable straws with custom printing using plant-based inks that are EU compliant. Now looking ahead, the straws reside in over 15,000 Starbucks stores and contain QR codes linking to sustainability initiatives designed to foster consumer engagement.

• March 2025, Aardvark Straws (USA) introduced Flex Straw, a bendable paper straw made from layers of recycled paper providing 30% more durability. The targeted market is fast food chains, and it has pilot testing already occurring with McDonald's Canada to provide a plastic-free straws option.

• June 2025, Tetra Pak (Sweden) launched the Paper Straw. An FSC-certified straw placed directly into beverage cartons to eliminate separate packaging. The straw's inaugural run was with school milk programs in Scandinavia, and successfully provided both convenience and food safety compliance.

Paper Straws Market Key Trends

1. Premiumization & Branding

Printed straws and branded straws are gaining momentum as cafes and hotels start to use custom-designed straws as part of their marketing. Starbucks is at the forefront using branded straws with QR codes that connect customers to stories around their sustainability efforts. Luxury brands use aesthetically pleasing straws for an enhanced customer experience.

2. Functional Innovations

Coating innovations, like Huhtamaki’s AquaShield™, extend the duration of standard straws from mere minutes to 4 hours in ambient beverages. New entrants have emerged with edible straws (available from Bambrew) and marine biodegradable (available from Sulapac) straws. Tetra Pak has integrated straws into its cartons, making the final product zero-waste.

3. E-Commerce Growth

B2B platforms such as Alibaba are establishing strong opening order programs with printed straws; orders by the caravan are increasing. New DTC Startups are utilizing subscription models for households and offices that veer away from plastic straws, and are catering to eco-conscious consumers.

4. Emerging Markets Rise

Asia is leading with demand for bubble tea in China and local production in India. The Middle East has entered the luxury space, and they are now adopting premium straws. The foodservice industry in Latin America has been slow to switch, but it is changing.

Paper Straws Market Scope: Inquire before buying

| Global Paper Straws Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 4.02 USD Billion |

| Forecast Period 2026-2032 CAGR: | 14.1% | Market Size in 2032: | 10.12 USD Billion |

| Segments Covered: | by Material Type | Virgin Kraft Paper Recycled Paper |

|

| by Product Type | Printed Non-printed |

||

| by Straw Length | <7 cm 7 – 10 cm 10-15 cm >15 cm |

||

| by Sales Channel | Manufacturers Distributors Retailers e-Retail |

||

| by End Use | Food Service Institutional Household |

||

Paper Straws Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Paper Straws Market, Key Players

- Huhtamaki Oyj

- Aardvark Straws LLC

- Hoffmaster Group Inc.

- Transcend Packaging Ltd

- Tetra Pak International SA

- Fuling Global Inc.

- Tembo Paper B.V.

- BioPak

- Eco-Products Inc.

- Green Paper Products

- Footprint International Holdings Inc.

- Uflex Ltd

- Canada Brown Eco Products Ltd

- Karat Packaging Inc.

- IPI Srl

- Vegware Ltd

- Lollicup USA Inc.

- GP PRO

- The Paper Straw Co.

- Biopac UK Ltd

- OkStraw

- Strawland Packaging Co. Ltd

- Soton Daily Necessities Co. Ltd

- Ningbo Henvcon Package Co. Ltd

- U.S. Paper Straw

- Charta Global Inc.

- Nippon Paper Industries Co. Ltd

- SIG Group

- Novolex

- Duni Group