Foot and Ankle Devices Market Size by Product, Application, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

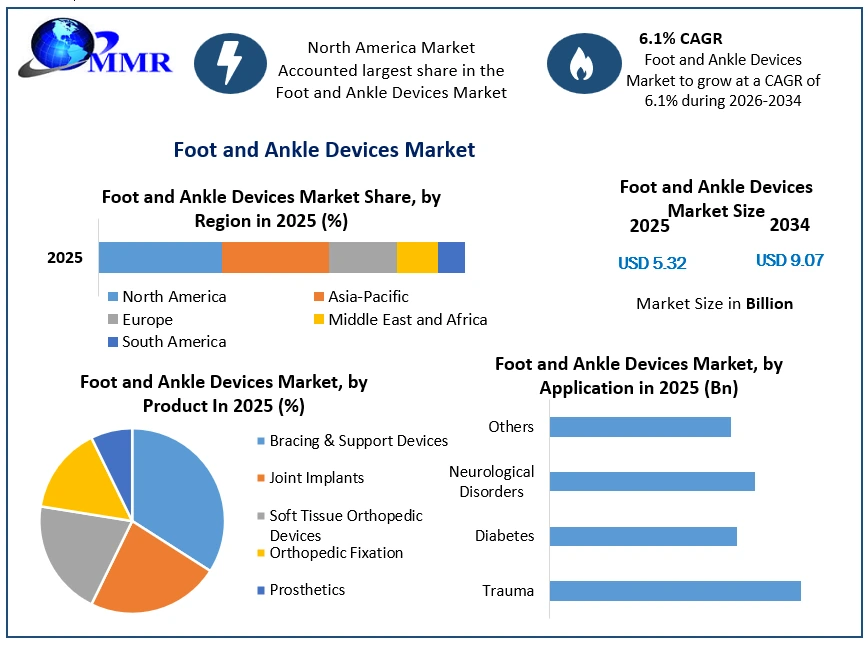

The Foot and Ankle Devices Market size was valued at USD 5.32 Billion in 2025 and the total Foot and Ankle Devices revenue is expected to grow at a CAGR of 6.10 % from 2026 to 2034, reaching nearly USD 9.07 Billion by 2034.

Foot and ankle devices include a range of medical tools and equipment tailored to address injuries, conditions, or deformities in the foot and ankle region, facilitating mobility, pain relief, and rehabilitation for patients. They aim to support, treat, or aid in the recovery process through orthotic inserts, braces, surgical implants, or prosthetics. The Foot and Ankle Devices Market is boosted by the growing prevalence of foot and ankle disorders, especially with the expanding global geriatric demographic.

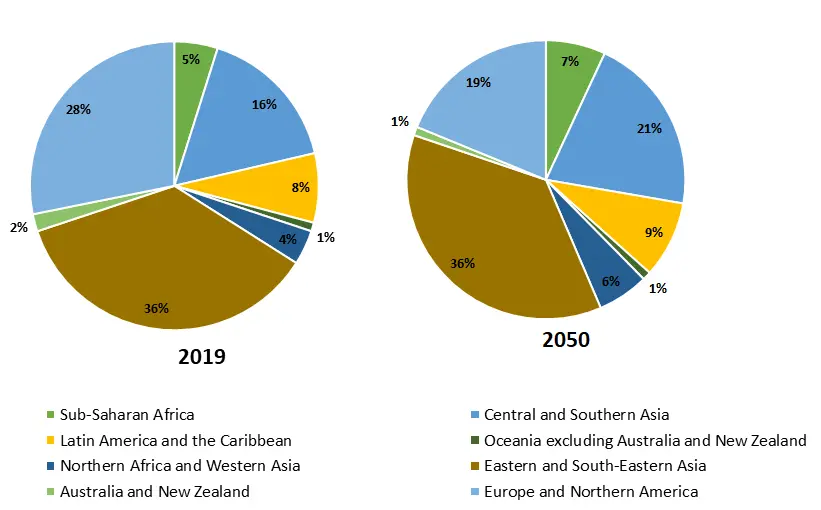

This trend is underscored by projections from the WHO's 2022 Ageing and Health report, forecasting a near doubling of the elderly population from 2015 to 2050, from 12% to 22%. The growing awareness regarding advanced treatment options, technological advancements in orthopaedic devices, and the rising demand for minimally invasive surgical procedures are contributing to market growth. The increasing adoption of innovative products such as orthopaedic implants, braces, supports, and orthotic insoles designed to provide better mobility and stability to individuals with foot and ankle ailments boosting the growth of Foot and Ankle Devices Market.

Foot and Ankle Devices Market Growth Outlook

To know about the Research Methodology:-Request Free Sample Report

Recent developments by key players in the market include strategic partnerships, product launches, and mergers & acquisitions aimed at expanding their product portfolio and market presence. For instance, in recent years, companies such as Stryker Corporation, Zimmer Biomet Holdings Inc., and Smith & Nephew plc have focused on launching advanced foot and ankle implants and surgical instruments, thereby enhancing their competitive position in the market. Technological advancements such as 3D printing and robotic-assisted surgeries are revolutionizing the treatment landscape, offering personalized solutions and improved surgical. The Foot and Ankle Devices Market is expected rapid growth driven by innovation, strategic collaborations, and the growing prevalence of orthopaedic disorders, with key players continuing to strive for advancements to meet the evolving needs of patients worldwide.

Foot and Ankle Devices Market Dynamics:

Rising aging population Driving Foot and Ankle Devices Market Growth

The rising aging population worldwide is significantly contributing to the rise in foot and ankle-related disorders driving the growth of Foot and Ankle Devices Market. With conditions such as osteoarthritis becoming more prevalent, there's a heightened demand for devices such as ankle replacement implants.

Global distribution of population aged 65 years or over by region, 2019 and 2050 (%)

Technological advancements play a major role in enhancing the effectiveness and longevity of foot and ankle devices. Innovations such as 3D-printed implants offer better customization and fit, leading to reduced complications and improved patient outcomes. Companies such as Stryker Corporation are at the forefront of investing in research and development to introduce such advanced products, thereby stimulating market growth. Advanced ankle-foot-orthosis (AFO) development now integrates anatomical landmarks and trim lines, revolutionizing personalized care for patients with central nervous system damage. By leveraging materials such as ABS and PLA, coupled with finite element analysis, these AFOs ensure optimal safety, comfort, and performance, marking a significant leap in foot and ankle device technology. The increasing incidence of sports injuries further fuels market growth as the demand for specialized devices for treatment and rehabilitation rises. Brands such as DJO Global cater to the needs of athletes with a range of sports medicine solutions, including braces and supports. This segment's growth contributes significantly to the overall growth of the foot and ankle devices market. These drivers collectively boost the market growth, promising a robust trajectory in the forecast period.

Recent Technological Developments in Foot and Ankle Devices

| Technological Development | Description |

| 3D Printing of Customized Implants | Utilizing 3D printing technology to create personalized implants for foot and ankle surgeries, allowing for better fit and improved patient outcomes. |

| Smart Orthotic Devices | Integration of sensors and wearable technology into orthotic devices to monitor gait, pressure points, and movement, providing real-time feedback and enhancing rehabilitation and treatment effectiveness. |

| Minimally Invasive Surgical Techniques | Advancements in arthroscopic and endoscopic procedures for foot and ankle surgeries, reducing incision size, recovery time, and post-operative complications while improving surgical precision. |

| Biocompatible Materials | Development of new biocompatible materials for implants and devices, such as titanium alloys and biodegradable polymers, to enhance durability, reduce rejection rates, and promote tissue integration. |

| Regenerative Medicine | Utilization of stem cell therapy, growth factors, and tissue engineering to promote healing and regeneration in foot and ankle injuries, offering alternatives to traditional surgical interventions. |

| Virtual Reality Rehabilitation | Implementation of virtual reality (VR) technology in foot and ankle rehabilitation programs, providing immersive environments for exercises, enhancing patient engagement, and facilitating recovery. |

| Computer-Assisted Navigation Systems | Integration of computer-assisted navigation systems in foot and ankle surgeries to improve accuracy, reduce surgical time, and minimize complications by aiding surgeons in precise implant placement. |

| Telemedicine for Remote Consultations | Adoption of telemedicine platforms for remote consultations, follow-ups, and monitoring of foot and ankle conditions, increasing accessibility to specialized care and reducing the need for in-person visits. |

| Shockwave Therapy | Application of extracorporeal shockwave therapy (ESWT) for treating various foot and ankle disorders, such as plantar fasciitis and Achilles tendonitis, offering non-invasive pain relief and promoting tissue healing. |

| Nanotechnology in Implant Coatings | Incorporation of nanotechnology in implant coatings to improve surface properties, reduce wear and friction, and enhance osseointegration, leading to longer-lasting and more successful implant outcomes. |

High-cost treatment Hinders the Foot and Ankle Devices Market Growth

The high cost of devices is a major barrier to access, particularly in regions with limited healthcare resources. For example, the expense associated with ankle replacement surgery, ranging from $5,000 to $10,000 for implants alone in the United States, deter patients from seeking treatment, ultimately limiting market growth. Stringent regulatory hurdles pose obstacles to market growth, often resulting in delays in product launches and increased development costs. For instance, FDA scrutiny delayed the approval of Wright Medical's total ankle replacement system in 2019, leading to prolonged market entry and heightened expenses for the company. These regulatory challenges hinder innovation and limit the introduction of new foot and ankle devices into the market.

Limited reimbursement policies impacting patient affordability and healthcare provider willingness to adopt new technologies. For example, the lack of insurance coverage for treatments like shockwave therapy for plantar fasciitis restricts patient access and adoption, hindering market gowth. These restraints, coupled with the risks of adverse events, competitive market landscape, and complex surgical procedures, underscore the multifaceted challenges facing the Foot and Ankle Devices market. Factors such as limited awareness and education, the threat of alternative treatments, patient preference for non-invasive options, and global economic uncertainty further compound the challenges, necessitating strategic interventions and collaborative efforts to overcome them for sustained market growth.

Foot and Ankle Devices Market Segment Analysis:

Based on Product, Bracing & Support products dominated the Foot and Ankle Devices Market in 2025 as they are widely adopted for treating various foot and ankle conditions, offering support and stability. Joint Implants, including ankle replacement implants, are crucial for addressing severe degenerative conditions and injuries, though their adoption may be limited due to high costs and surgical complexity. Soft Tissue Orthopedic Devices, such as tendon repair systems, play a vital role in treating soft tissue injuries and deformities, with growing adoption owing to advancements in minimally invasive techniques.

Orthopedic Fixation devices, such as plates and screws, are essential for stabilizing fractures and facilitating bone healing, widely utilized across orthopedic procedures, including foot and ankle surgeries. Prosthetic devices cater to patients requiring limb replacement due to amputations or severe deformities, offering functional restoration and improving mobility, albeit with varying degrees of adoption depending on patient needs and surgical indications. Overall, each product category serves distinct applications in addressing foot and ankle disorders, with adoption influenced by factors such as efficacy, cost, and surgical complexity.

Foot and Ankle Devices Market Regional Insights:

North America Dominance in the Foot and Ankle Devices Market

North America dominated the Foot and Ankle Devices Market in 2025 as it emerges as a major manufacturing region, driven by the presence of key manufacturers such as Stryker Corporation. The region's advanced healthcare infrastructure and high research and development investments contribute to its prominence in product innovation and manufacturing.

Europe stands out as a large utilizing region, with countries such as Germany and the UK boasting robust healthcare systems and high prevalence of foot and ankle disorders. These regions exhibit substantial demand for advanced devices, including ankle replacement implants and orthotic solutions. In terms of import-export dynamics, Asia-Pacific is a notable player, with countries like China and India emerging as major exporters of foot and ankle devices due to lower production costs and increasing manufacturing capabilities. Meanwhile, regions like the Middle East and Latin America witness significant import activities, driven by growing healthcare expenditure and increasing demand for advanced medical technologies. For instance, Brazil imports a considerable volume of orthopedic devices to cater to its aging population and rising incidences of sports injuries.

Foot and Ankle Devices Market Scope: Inquire before buying

| Global Foot and Ankle Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 5.32 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6.10% | Market Size in 2034: | US $ 9.07 Bn. |

| Segments Covered: | by Product | Bracing & Support Devices Joint Implants Soft Tissue Orthopedic Devices Orthopedic Fixation Prosthetics |

|

| by Application | Trauma Diabetes Neurological Disorders Others |

||

| by Application | Hospitals and Specialty Clinics Ambulatory Surgical Centers (ASCs) Orthopedic Clinics Rehabilitation Centers Others |

||

Foot and Ankle Devices Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Foot and Ankle Devices Market Key Players:

Major Contributors in the Foot and Ankle Devices Industry in North America:

1. Stryker Corporation - Headquarters: Kalamazoo, Michigan, USA

2. Johnson & Johnson (DePuy Synthes) - Headquarters: New Brunswick, New Jersey, USA

3. Zimmer Biomet Holdings - Headquarters: Warsaw, Indiana, USA

4. Arthrex - Headquarters: Naples, Florida, USA

5. DJO Global - Headquarters: Vista, California, USA

6. Orthofix Medical Inc. - Headquarters: Lewisville, Texas, USA

7. Acumed Llc - Headquarters: Hillsboro, Oregon, USA

Leading Figures in the European Foot and Ankle Devices Sector:

1. Smith & Nephew - Headquarters: London, United Kingdom

2. Össur - Headquarters: Reykjavik, Iceland

3. Medartis Holding AG - Headquarters: Basel, Switzerland

Frequently Asked Questions :

1] What Major Key players in the Global Foot and Ankle Devices Market report?

Ans. The Major Key players covered in the Foot and Ankle Devices Market report are Stryker Corporation, Johnson & Johnson, Zimmer Biomet Holdings, Arthrex, DJO Global, Orthofix Medical Inc.

2] Which region is expected to hold the highest share in the Global Foot and Ankle Devices Market?

Ans. North America region is expected to hold the highest share in the Foot and Ankle Devices Market.

3] What is the market size of the Global Foot and Ankle Devices Market by 2034?

Ans. The market size of the Foot and Ankle Devices Market by 2034 is expected to reach US$ 9.07 Billion.

4] What is the forecast period for the Global Foot and Ankle Devices Market?

Ans. The forecast period for the Foot and Ankle Devices Market is 2026-2034.

5] What was the market size of the Global Foot and Ankle Devices Market in 2025?

Ans. The market size of the Foot and Ankle Devices Market in 2025 was valued at US$ 5.32 Billion.