Mined Anthracite Coal Market- Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

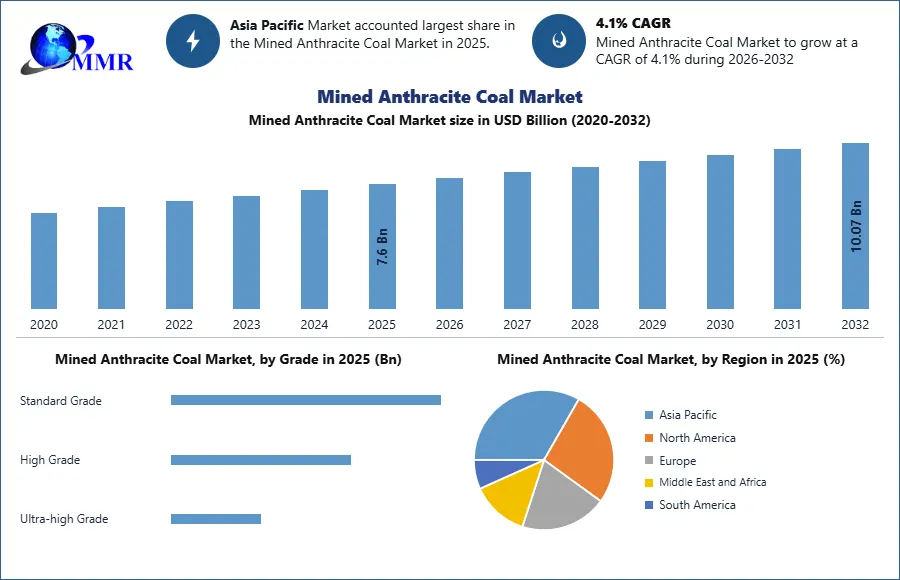

The Mined Anthracite Coal Market was valued at USD 7.6 Billion in 2025 and is estimated to grow at a CAGR of 4.1% over the forecast period, reaching USD 10.07 Billion by 2032.

The Connected Rail Market represents the ecosystem of digital, communication, control, monitoring, analytics, and passenger-facing technologies deployed across railway infrastructure, rolling stock, stations, and network operations. It covers real-time passenger information, train tracking and monitoring, automated fare collection, predictive maintenance, IP video surveillance, and digital signalling platforms such as Positive Train Control, CBTC, and ATC. As rail systems become more data-centric, connected rail has shifted from a support function to a strategic operating model for safety, punctuality, capacity utilization, and lifecycle cost optimization.

The strongest growth factors have been rising urbanization, the need for higher-capacity public transport, and the modernization of aging rail infrastructure. Transit agencies and national rail operators have been investing in intelligent transport systems to improve service reliability, reduce manual interventions, and manage increasing passenger volumes with greater operational precision. At the same time, digital rail technologies have gained policy relevance because governments increasingly view rail as a lower-emission transport mode that supports decarbonization goals and more efficient mobility planning. Rail carries only a modest share of transport emissions relative to its passenger and freight role, reinforcing investment interest in digitally enabled rail expansion.

Technological development has accelerated the market’s transformation. CBTC and ETCS-based signalling, cloud-enabled control architectures, AI-assisted inspection, digital twins, and asset condition monitoring are now moving from pilot scale to mainstream deployment. Operators are also prioritizing integrated control centers, onboard connectivity, and real-time data exchange between train, trackside, and central systems. The demand outlook remains favorable because rail agencies are under pressure to increase throughput, improve passenger communication, and extend asset life without proportionately increasing maintenance costs. As a result, the Connected Rail Market is expected to remain a key beneficiary of smart mobility investment, rail automation, and sustainability-led infrastructure spending.

To know about the Research Methodology:-Request Free Sample Report

Mined Anthracite Coal Market Growth Catalysts

High Carbon Efficiency Driving Metallurgical Demand Expansion

The Mined Anthracite Coal Market has been strongly influenced by the increasing requirement for high-carbon, low-impurity fuel in metallurgical processes, particularly in steel production and ferroalloy manufacturing. Anthracite coal typically contains more than 86% fixed carbon, which significantly enhances combustion efficiency and reduces slag formation in blast furnaces. This has made it a preferred substitute for coke breeze and other lower-grade carbon inputs in pulverized coal injection systems.

In 2025, nearly 40–50% of anthracite consumption globally was linked to metallurgical and steel-related applications, especially across China, India, and Eastern Europe. As infrastructure investments continue to expand globally—particularly in transportation, construction, and energy—steel demand remains robust, directly translating into consistent demand for mined anthracite. Additionally, anthracite’s lower volatile matter content improves furnace stability and reduces emissions intensity per ton of output, aligning with evolving industrial efficiency benchmarks.

Industrial Heating and Energy-Intensive Manufacturing Growth

The Mined Anthracite Coal Market is further supported by its extensive use in high-temperature industrial heating applications, including cement kilns, glass manufacturing, and chemical processing units. Anthracite coal provides a calorific value exceeding 7,500 kcal/kg, making it one of the most energy-dense solid fuels available for industrial use.

Industries requiring consistent and controlled heat output have increasingly shifted toward anthracite due to its stable combustion profile and reduced smoke emissions. In emerging economies, where natural gas infrastructure remains limited or expensive, anthracite serves as a reliable alternative fuel source. Furthermore, small and medium industrial clusters continue to rely on anthracite for cost-effective heating solutions, reinforcing steady demand.

Rising Demand in Water Filtration and Environmental Applications

A significant but often underrepresented driver in the Mined Anthracite Coal Market is the increasing use of anthracite in water treatment and filtration systems. Anthracite is widely used as a filtration medium due to its high density, hardness, and low impurity content, which allow it to effectively remove suspended particles and organic matter.

Government-backed investments in municipal water infrastructure, particularly in Asia-Pacific and the Middle East, have increased demand for anthracite-based filtration media. In large-scale water treatment plants, anthracite is often layered with sand filters to improve filtration efficiency and extend filter life cycles. With rising concerns around water scarcity and contamination, this application segment is expected to contribute meaningfully to long-term demand diversification.

Mined Anthracite Coal Market Limitations

Regulatory Pressure and Energy Transition Policies

The Mined Anthracite Coal Market is increasingly constrained by global decarbonization policies aimed at reducing dependence on fossil fuels. Governments across Europe and North America have implemented strict emission standards, carbon pricing mechanisms, and coal phase-out strategies, directly impacting coal mining activities.

For instance, coal-fired power generation is declining in several developed economies, reducing demand for anthracite in traditional energy applications. Although anthracite is cleaner than other coal types, it still falls under regulatory scrutiny due to its carbon footprint. This has led to reduced investment in new mining projects and increased compliance costs for existing operations.

Geological Constraints and High Extraction Complexity

Anthracite coal is typically found in deeper, more compact geological formations compared to other coal types, making extraction more technically challenging and cost-intensive. Mining operations often require advanced underground techniques, specialized equipment, and higher labor safety standards.

These factors result in production costs that are 20–30% higher than bituminous coal extraction in certain regions, limiting profitability margins. Additionally, the concentration of high-quality anthracite reserves in limited geographies—such as China, Russia, and parts of the United States—creates supply concentration risks and price volatility.

Mined Anthracite Coal Market Future Growth Potential

Growth in Specialty Carbon Applications and Chemical Processing

The Mined Anthracite Coal Market is increasingly exploring high-value applications beyond traditional fuel usage, particularly in carbon-intensive chemical processes and specialty carbon products. Anthracite is used in the production of activated carbon, carbon electrodes, and filtration media for industrial and environmental applications.

As industries shift toward higher-purity carbon inputs, ultra-high-grade anthracite is gaining traction in niche applications, including battery materials, metallurgy additives, and advanced filtration systems. This transition toward value-added applications is expected to improve margin profiles for producers.

Export-Oriented Growth in Resource-Rich Regions

Countries with significant anthracite reserves are increasingly focusing on export-driven strategies to capitalize on demand from regions with limited domestic production. For example, Southeast Asia, the Middle East, and parts of Africa are becoming key import markets due to rising industrialization and limited local resources.

Improved logistics infrastructure, including port expansions and rail connectivity, is enabling producers to access global markets more efficiently. This trend is expected to support stable long-term demand, particularly for high-grade anthracite.

Mined Anthracite Coal Market Operational & Strategic Barriers

One of the key barriers in the Mined Anthracite Coal Market is the fragmented supply structure, where a limited number of large-scale producers coexist with numerous small and regional mining operators. This fragmentation creates inconsistencies in product quality, supply reliability, and pricing structures.

Additionally, capital-intensive mining operations and long project development cycles pose challenges for new entrants. The requirement for environmental approvals, land acquisition, and infrastructure development further complicates project timelines, often extending beyond 5–7 years.

Mined Anthracite Coal Market Segmentation, by Type

In 2025, the High-Grade Anthracite segment was the largest in the Mined Anthracite Coal Market due to its superior carbon content, high calorific value, and low impurity levels, which made it highly suitable for metallurgical and industrial applications. High-grade anthracite was extensively adopted in steel manufacturing, particularly in blast furnaces and pulverized coal injection processes, where consistent heat output and efficiency were critical. The demand for high-grade anthracite was further driven by its ability to reduce emissions compared to lower-grade coal, aligning with environmental compliance requirements in industrial operations. Additionally, its application in water filtration, chemical processing, and high-temperature industrial heating strengthened its dominance. Industrial buyers preferred high-grade anthracite due to its performance reliability, cost efficiency over long-term operations, and compatibility with advanced manufacturing technologies, making it the most commercially viable segment in 2025.

Mined Anthracite Coal Market Regional Analysis

In 2025, Asia-Pacific was the leading region in the Mined Anthracite Coal Market, driven by strong industrial growth, expanding steel production capacity, and increasing infrastructure investments across China, India, and Southeast Asia. The region benefited from abundant reserves, large-scale mining operations, and well-established supply chains that supported consistent production and distribution. Policy support for industrial expansion and energy security further reinforced regional dominance, as governments prioritized domestic resource utilization. Technology leadership in mining automation and large-scale extraction methods improved operational efficiency and output capacity. Additionally, the presence of integrated industrial ecosystems, including steel plants, cement industries, and power generation facilities, ensured sustained demand. Infrastructure development, including rail connectivity and port logistics, facilitated efficient transportation and export of anthracite coal, making Asia-Pacific the dominant regional market in 2025.

Key Players/Competitors Profiles Covered in the Mined Anthracite Coal Market Report in Strategic Perspective

- Glencore

- Siberian Coal Energy Company

- Shanxi Jincheng Anthracite Mining Group

- Reading Anthracite Company

- Blaschak Coal Corporation

- Atlantic Coal Plc

- Atrum Coal Ltd.

- Celtic Energy

- VostokCoal

- Vietnam National Coal Mineral Industries Group

- Aspire Mining Limited

- Robindale Energy Services

- Hudson Coal Company

- Feishang Anthracite Resources

- Cokal Limited

- Bathurst Resources

- Lehigh Anthracite

- Sadovaya Group

- K&S Group

- Pagnotti Enterprises

- K&K Coal Company

- Crown Energy Corporation

- Coal Contractors Inc.

- Hugh McCulloch & Sons

- Glen Coal Company

Recent Developments

January 2025: A major anthracite mining operator announced the expansion of its underground mining operations in Asia-Pacific, integrating advanced automation technologies and AI-driven geological mapping systems. This investment aimed to increase extraction efficiency, reduce operational downtime, and improve safety standards. The project also included the deployment of real-time monitoring systems to optimize resource utilization and reduce environmental impact. This expansion reflects the growing demand for high-grade anthracite in steel manufacturing and industrial applications, while also aligning with sustainability goals through improved energy efficiency and reduced emissions in mining operations.

March 2025: A leading global mining company entered into a strategic partnership with a technology provider to develop next-generation clean coal processing solutions. The collaboration focused on enhancing the quality of anthracite through advanced beneficiation techniques and reducing sulfur and ash content. The initiative aimed to support industries transitioning toward cleaner fuel alternatives while maintaining cost efficiency. This development highlights the increasing importance of innovation in the Mined Anthracite Coal Market, particularly in addressing environmental concerns and improving product performance for industrial use.

July 2025: A multinational coal producer announced a significant investment in export infrastructure, including port expansion and logistics optimization, to strengthen its global supply chain for anthracite coal. The project was designed to improve transportation efficiency, reduce delivery timelines, and expand access to international markets. This development underscores the growing importance of global trade in the anthracite coal industry, as demand from emerging economies continues to rise. The investment also reflects a strategic shift toward enhancing distribution capabilities to meet increasing industrial demand worldwide.

Scope Of the Global Mined Anthracite Coal Market: Inquire before buying

| Mined Anthracite Coal Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 7.6 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.1% | Market Size in 2032: | 10.07 USD Billion |

| Segments Covered: | by Grade | Standard Grade High Grade Ultra-high Grade |

|

| by Mining | Surface Mining Underground Mining |

||

| by Application | Power Generation Steel Production Fertilizer Production Others |

||

Global Mined Anthracite Coal Market, Region wise Market Analysis & Forecast:

The report covers a geographic breakdown and a detailed analysis of each of the before said segments across North America, Europe, Asia Pacific, and SAMEA, and each countries under it –

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players/Competitors Profiles Covered in the Mined Anthracite Coal Market Report in Strategic Perspective

- Glencore

- Siberian Coal Energy Company

- Shanxi Jincheng Anthracite Coal Mining Group Co., Ltd.

- Feishang Anthracite Resources Limited

- Reading Anthracite Company

- Blaschak Coal Corporation

- Atlantic Coal Plc

- Atrum Coal Ltd.

- Celtic Energy

- VostokCoal

- Vietnam National Coal Mineral Industries Group

- Aspire Mining Limited

- Robindale Energy Services

- Hudson Coal Company

- Cokal Limited

- Bathurst Resources

- Lehigh Anthracite

- Sadovaya Group

- K&S Group

- Pagnotti Enterprises

- K&K Coal Company

- Crown Energy Corporation

- Coal Contractors Inc.

- Hugh McCulloch & Sons

- Glen Coal Company