Anthracite Market Size by Grade, Application, End User, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

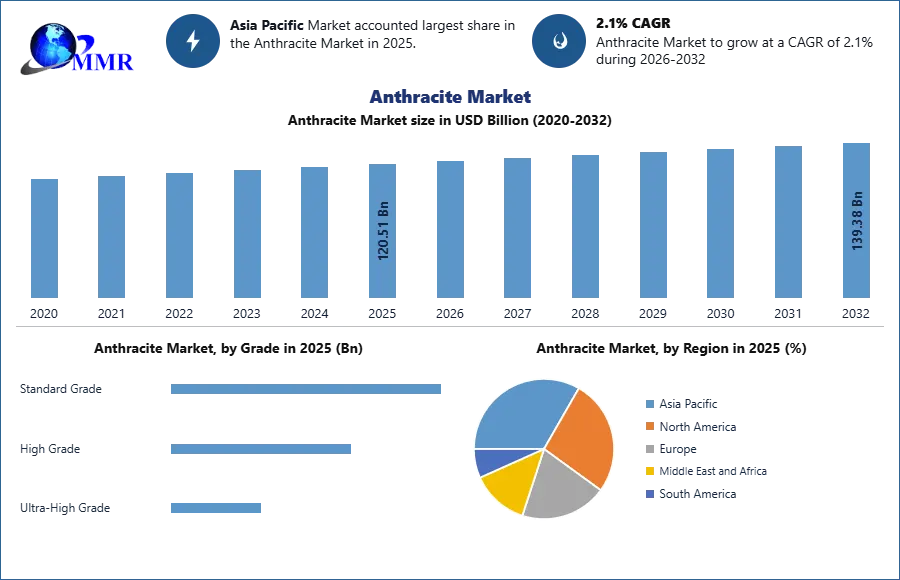

Anthracite Market Size was valued at USD 120.51 Bn. in 2025 and the Anthracite Market is expected to grow by 2.1 % from 2026 to 2032, reaching nearly USD 139.38 Bn.

Anthracite Market Overview:

The anthracite market refers to the global trade and consumption of a high-grade type of coal characterized by its unique properties, including high carbon content, low volatile matter, and excellent energy efficiency. Anthracite is a hard and shiny coal variety that burns with minimal smoke and produces high heat output. Primarily anthracite used for heating purposes within residential, commercial, and industrial sectors, as well as for electricity generation within the industry. The market revolves around the mining, production, distribution, and trade of anthracite to meet the demand for efficient and clean-burning energy sources. An opportunity within the anthracite market lies in its use as a substitute for coking coal in steel production. Anthracite's high carbon content and low impurities make it suitable for use as a reducing agent in the steelmaking process. As per the World Steel Association, global crude steel production reached approximately 1.89 billion metric tons in 2023.

To know about the Research Methodology :- Request Free Sample Report

Anthracite Market Dynamics:

Environmental Regulations and Clean Energy Demand to Boost the Anthracite Market Growth

One of the primary drivers of the anthracite market is the increasing emphasis on environmental regulations and the growing demand for cleaner energy sources. As governments and industries strive to reduce carbon emissions and air pollutants, the use of coal with lower sulfur content becomes crucial. Anthracite's naturally low sulfur and volatile matter content make it an attractive option for industries seeking to comply with emission standards and transition towards cleaner energy alternatives. Anthracites’ exceptional energy density and efficiency make them a favoured choice for energy-intensive applications. Anthracites are high-quality coal resources that drive the demand for anthracite and are expected to boost market growth during the forecast period. Industries seeking coal with low ash content, high carbon content, and minimal impurities turn to anthracite for applications ranging from metallurgical processes to power generation. This scarcity positions anthracite as a valuable and sought-after resource.

Anthracite's significance in the metallurgical industry is a major driver. Its use as a reducing agent in steelmaking, especially in blast furnaces, aids in the efficient conversion of iron ore into steel. Anthracite's low ash and high carbon content play a pivotal role in reducing Coke consumption, resulting in cost savings and reduced environmental impact. Anthracite's stable combustion characteristics make it a dependable source of energy for critical industries that require continuous operations. Industries such as power generation, cement production, and chemical manufacturing rely on anthracite's consistent heat output to ensure uninterrupted processes and operations. As urbanization continues, the demand for clean and efficient heating solutions for residential and commercial spaces increases. Anthracite's ability to provide high heat output over an extended duration, coupled with its cleaner combustion, positions it as an attractive option for meeting heating needs while minimizing environmental impact. Anthracite's unique properties extend beyond energy generation to specialized applications. Its high carbon content and porous nature make it an effective medium for water filtration and purification processes. Anthracite's adsorption capabilities are valued in water treatment plants, where it removes contaminants and impurities from drinking water sources.

Dependency on Weather Conditions to hamper the Anthracite Market Growth

A significant restraint facing the anthracite market is the growing global emphasis on environmental sustainability and the shift towards cleaner energy sources. The combustion of coal, including anthracite, releases greenhouse gases and other pollutants that contribute to air pollution and climate change. Stringent environmental regulations, carbon pricing, and international agreements such as the Paris agreement have led to reduced demand for coal-based energy, which has impacted the anthracite market.

These alternatives offer cleaner and more sustainable energy options, attracting investments and policy support globally. As the costs of renewable technologies continue to decrease and their efficiency improves, industries and governments are increasingly favouring these alternatives over coal, diminishing the demand for anthracite. Public concerns about air quality, health impacts, and climate change have led to negative perceptions of coal-based energy, including anthracite. Social acceptance of cleaner energy sources and a shift towards sustainable practices have resulted in reduced support for coal extraction and consumption. The negative image associated with coal can lead to regulatory hurdles, public opposition, and challenges in securing investments for anthracite projects.

The anthracite market is subject to price fluctuations driven by factors such as supply-demand dynamics, geopolitical events, and energy policies. Volatile commodity prices can impact profitability and investment decisions for anthracite producers and consumers. Uncertainties related to global economic conditions and energy market shifts can lead to market volatility, affecting long-term planning and investment strategies. Governments worldwide are implementing energy transition policies aimed at reducing reliance on fossil fuels. As a result, investment preferences are shifting towards renewable energy projects and technologies. Anthracite producers may face challenges in securing financing and investments due to the changing landscape of energy-related funding and support.

Opportunity in the Global Anthracite Market:

The development and deployment of advanced emission reduction technologies provide an opportunity for the anthracite market. Research and investment in carbon capture, utilization, and storage (CCUS) technologies can enhance the environmental performance of anthracite combustion. By demonstrating the feasibility of cleaner coal-based energy, anthracite could potentially play a role in the transition to low-carbon energy systems. The steel industry's ongoing efforts to reduce carbon emissions present an opportunity for anthracite to be used as a cleaner substitute for coking coal in steelmaking.

Innovations in direct reduction processes and alternative iron production methods provide avenues for anthracite to contribute to reducing the environmental impact of steel production. The concept of carbon-neutral energy projects, which involve offsetting emissions through measures like reforestation or investing in renewable energy, creates an opportunity for anthracite producers. By implementing carbon offset initiatives or partnering with renewable energy projects, anthracite stakeholders can mitigate their carbon footprint and enhance their environmental credentials. The growing demand for sustainable urban heating solutions presents an opportunity for anthracite's clean combustion characteristics. Anthracite can be promoted as an eco-friendly option for district heating systems and residential heating in urban areas, offering an efficient and cleaner alternative to traditional heating methods.

Anthracite Market Segment Analysis:

Basde on Grade, High Grade anthracite dominated Anthracite Market. This grade holds the largest market share due to its superior carbon content, low impurities, and high energy efficiency. High Grade anthracite is primarily used in industrial processes that require high-quality, clean-burning coal, such as in steel production and power generation. This grade has a lower ash content, which makes it more valuable for processes where purity is crucial. Furthermore, High Grade anthracite is increasingly favored due to its ability to generate more energy with less environmental impact compared to lower-grade anthracite. Although Ultra-High Grade anthracite is gaining attention for specialized applications, High Grade remains the most dominant due to its balance of performance, cost-effectiveness, and availability. As industries continue to focus on efficiency and sustainability, the demand for High Grade anthracite is expected to remain strong.

Based on Application, the steel production held the largest share in 2025 . Anthracite is a key ingredient in steelmaking, where it is used as a fuel and a reducing agent in the production of steel from iron ore. Due to its high carbon content and low impurity levels, it serves as an efficient substitute for coke in many steel mills. This application drives the largest share of demand in the anthracite market, particularly in countries with robust steel industries. Steel production requires high-quality carbon for efficient and cost-effective operations, and anthracite's properties make it a preferred choice. Additionally, its low ash content enhances the quality of the steel produced, contributing to the dominance of steel production as the leading application in the market. The strong steel demand, driven by construction and infrastructure projects, ensures that this application remains the largest for anthracite.

Anthracite Market Regional Insights:

The Asia‑Pacific anthracite market is driven by rapid industrialization, robust steel production capacity, and expanding energy demand. China remains the dominant consumer and producer in the region due to its extensive steel and manufacturing base, with India, Japan, and Southeast Asian economies also contributing significantly to regional demand. The market’s growth is supported by ongoing infrastructure development, urbanization, and industrial fuel requirements that favor anthracite’s high carbon content and low impurity profile for metallurgical and energy uses. Metallurgical demand, particularly for steelmaking and ferroalloy processes, represents a substantial portion of regional consumption, while power generation and water filtration sectors also contribute to steady uptake. Asia‑Pacific’s strategic importance is further underscored by government investments in energy and industrial projects, along with efforts to balance reliance on coal with environmental and efficiency considerations. As a result, the region is expected to sustain strong anthracite market expansion over the coming years.

Europe's anthracite market has been significantly exaggerated by environmental concerns and the continent's push toward renewable energy sources. While anthracite was historically used for heating and industrial applications, there has been a decline in demand due to the adoption of natural gas and renewables. However, certain European countries still utilize anthracite for residential heating, particularly in areas with limited access to alternative energy sources. The region's efforts to reduce carbon emissions have led to a heavy urge in demand for anthracite.

Anthracite Market Competitive Landscape:

The competitive landscape of the anthracite market is influenced by a complex interplay of factors, including regional demand variations, technological advancements, environmental regulations, and the global shift towards cleaner energy sources. Key players within the industry are strategically positioned themselves to navigate these challenges while exploiting opportunities for growth and sustainability. This in-depth analysis examines the competitive landscape of the anthracite market, highlighting major players, market strategies, and prospects.

Blaschak Coal and Reading Anthracite are prominent players within the U.S. anthracite market and have established a strong position due to their extensive mining operations and focus on quality control. The company's vertical integration, from mining to distribution, enables them to ensure consistent product quality and supply chain reliability. Also, their commitment to reclamation and restoration of mined lands aligns with increasing environmental concerns. This company focuses on high-quality anthracite for industrial applications, catering to the steel, chemical, and energy sectors.

Recent Developments

24 Dec 2025 — China Shenhua Energy Company

In December 2025, China Shenhua Energy Company announced a major strategic acquisition plan worth roughly USD 19 billion to buy 12 subsidiaries from its controlling shareholder. This move aims to expand vertical integration across coal mining, power generation, coal‑to‑chemicals, logistics, and transportation, effectively consolidating its anthracite and broader coal assets under one publicly traded entity. The acquisition is expected to nearly double the company’s recoverable coal reserves and significantly boost production capacity, strengthening its position in both domestic and export markets. By integrating these units, Shenhua can optimize operations, improve efficiencies amid declining coal demand pressure, and support its role as a cornerstone supplier for energy and industrial applications. The deal reflects a broader strategy to adapt to shifting market dynamics while maintaining leadership in China’s coal industry.

15 Nov 2023 — Sibanthracite Group

In November 2023, Sibanthracite Group, the world’s largest ultra‑high‑grade anthracite producer, was acquired by Bashkir Industrial Holding LLC, marking a significant ownership change for this Russian coal giant. Under new ownership, the company has pursued intensified development of mining licenses and expanded production potential, with a focus on growing annual output and maintaining its status as a key exporter to Asia‑Pacific markets. In 2023–2024, Sibanthracite also secured additional mining licenses in the Kuzbass region and saw significant revenue and profit gains from its anthracite and metallurgical coal operations. Management continuity was preserved by retaining experienced executives, underscoring its commitment to production growth and strategic expansion in metallurgical coal markets. This development positions the group for strengthened role in supplying high‑quality anthracite to steel and industrial customers globally.

Anthracite Market Scope: Inquire Before Buying

| Anthracite Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 120.51 USD Billion |

| Forecast Period 2026-2032 CAGR: | 2.1% | Market Size in 2032: | 139.38 USD Billion |

| Segments Covered: | by Grade | Standard Grade High Grade Ultra-High Grade |

|

| by Application | Power Stations Steel Production Water Treatment & Filtration General Industrial Others |

||

| by End Use | Metallurgical Energy & Power Chemicals Others |

||

Anthracite Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Key players/Competitors profiles covered in the Anthracite Market report in strategic perspective

- Blaschak Coal Corporation

- Reading Anthracite Company

- Atlantic Coal Plc

- Lehigh Anthracite

- Jeddo Coal Company

- Siberian Anthracite

- China Shenhua Energy Company

- Cokal Limited

- Black Diamond Corporation

- Xcoal Energy & Resources

- Jastrzębska Spółka Węglowa

- Henan Shenhuo Coal & Power Co., Ltd

- Yangquan Coal Group

- Shanxi Jincheng Anthracite Coal Mining Group Co., Ltd.

- Zululand Anthracite Colliery (Pty) Ltd.

- Feishang Anthracite Resources Limited

- Jindal Steel & Power Ltd

- Celtic Energy

- Sadovaya Group

- Western Carbon & Chemicals

- Atrum Coal

- Dongbei Special Steel Group

- Inner Mongolia Yitai Coal Company